Electronic Display Devices Market Size 2026-2030

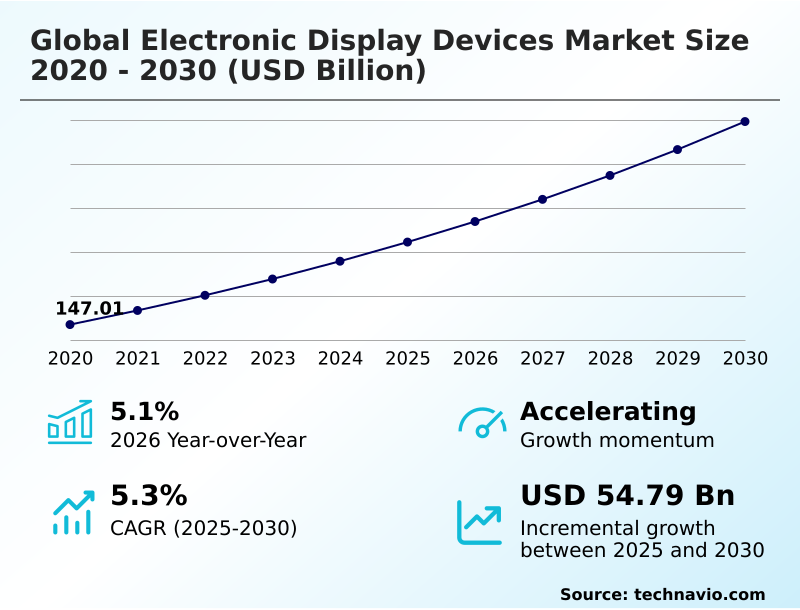

The electronic display devices market size is valued to increase by USD 54.79 billion, at a CAGR of 5.3% from 2025 to 2030. Increasing proliferation of smart devices and IoT integration will drive the electronic display devices market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 40.6% growth during the forecast period.

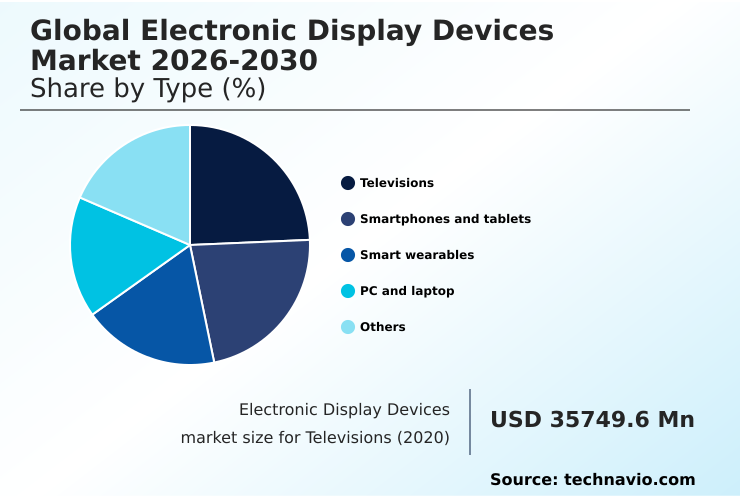

- By Type - Televisions segment was valued at USD 41.85 billion in 2024

- By End-user - Commercial segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 92.29 billion

- Market Future Opportunities: USD 54.79 billion

- CAGR from 2025 to 2030 : 5.3%

Market Summary

- The electronic display devices market is undergoing a period of profound transformation, characterized by rapid technological evolution and the expansion of application frontiers. Growth is driven by a strategic push toward creating more immersive, interactive, and seamlessly integrated visual experiences.

- This transition redefines the display's role from a simple output device to a central component of the human-machine interface in an increasingly connected world. Key developments include advancements in emissive technologies and innovation in form factors and embedded functionalities.

- For example, the convergence of sensing and display functions is a pivotal trend, particularly in mobile and wearable technology, where panels can now integrate biometric sensors. The automotive sector has emerged as a particularly strong driver of demand, with the evolution of the vehicle cockpit into a fully digital, software-defined environment necessitating larger, more complex display solutions.

- In a business context, optimizing the supply chain for specialized components like indium gallium zinc oxide backplanes for medical imaging equipment is critical. This involves managing inventory for diverse products ranging from camera-based digital mirrors to large-format screens requiring advanced optical bonding process, ensuring long operational lifecycles while balancing cost and innovation across sectors.

What will be the Size of the Electronic Display Devices Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Electronic Display Devices Market Segmented?

The electronic display devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

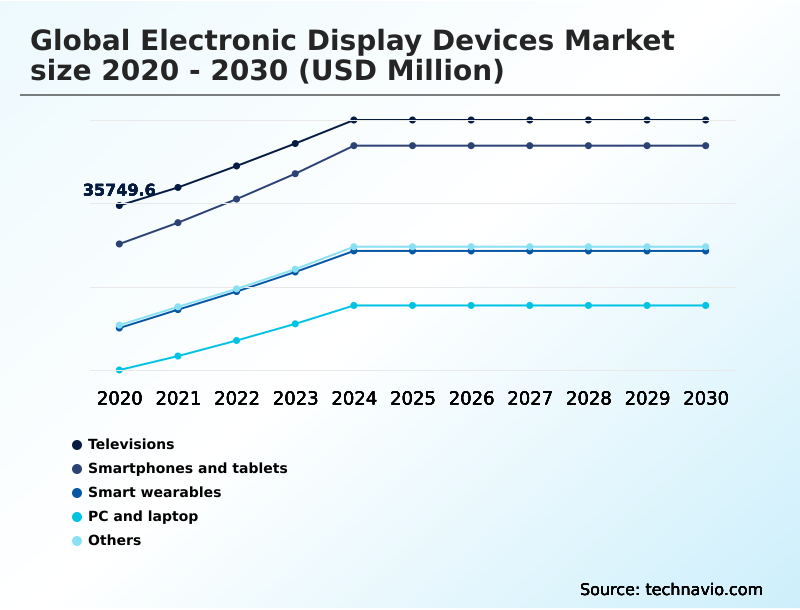

- Type

- Televisions

- Smartphones and tablets

- Smart wearables

- PC and laptop

- Others

- End-user

- Commercial

- Residential

- Technology

- LCD

- OLED

- LED

- Others

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Type Insights

The televisions segment is estimated to witness significant growth during the forecast period.

The televisions segment is a foundational arena for electronic display devices, driven by a persistent trend toward premiumization. Growth is increasingly fueled by value as consumers demand a superior premium visual experience.

This is pushing manufacturers to enhance liquid crystal display technology with features like mini-led backlighting and local dimming zones to improve high dynamic range performance.

Competing emissive display platforms such as organic light emitting diode are preferred for cinematic content due to their pixel-level light control.

The smart home ecosystem's expansion makes the television a central human-machine interface, with gaming needs driving adoption of high refresh rate panels.

Innovations in micro lens array technology are also improving brightness, achieving up to a 15% increase in power efficiency for residential models. These advancements cater to consumer electronics applications demanding continuous improvement.

The Televisions segment was valued at USD 41.85 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 40.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Electronic Display Devices Market Demand is Rising in APAC Get Free Sample

The APAC region is the epicenter of the electronic display devices market, serving as both the primary manufacturing hub and the largest consumer market, accounting for over 40% of incremental growth.

Countries in this region host leading panel manufacturers specializing in in-plane switching and amorphous silicon backplane technologies. The region's dominance is supported by extensive supply chain infrastructure for components like timing controllers.

Massive internal demand from consumer electronics and the construction of smart cities fuels growth in applications from professional-grade monitors to large-format immersive visual installations.

This combination of unparalleled manufacturing scale, with production yields improving by 10% annually, and vast internal demand for power-frugal displays creates a self-reinforcing cycle of innovation that defines the global market trajectory.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the display market requires a deep understanding of nuanced technological trade-offs. The debate over the cost of microled vs oled displays is central, as it directly impacts product positioning and profitability. For premium segments, firms must master oled burn-in mitigation techniques to ensure product longevity, a key consumer concern.

- In the competitive gaming sector, the performance difference between mini-led vs qd-oled for gaming can determine market leadership. For mobile applications, ltpo backplane power consumption benefits are critical for addressing the high refresh rate impact on mobile battery life.

- The industry also grapples with significant manufacturing hurdles, including the challenges in foldable display manufacturing and the complex microled mass transfer process challenges. In automotive, automotive pillar-to-pillar display integration is redefining interior design, while digital mirror system display requirements push for higher dynamic range and reliability.

- For niche applications, understanding flexible substrate materials for wearables and the energy efficiency of e-paper displays opens new revenue streams. Similarly, transparent oled retail display applications are transforming in-store experiences. Boardroom discussions must weigh the impact of esg criteria on display manufacturing against the technical demands of ruggedized displays for industrial environments.

- Analyzing the supply chain for driver integrated circuits reveals that sourcing from multiple vendors can reduce dependency risk and lower procurement costs by up to 15% compared to single-sourcing strategies.

- Finally, a clear comprehension of color gamut coverage for professional monitors, how variable refresh rate technology explained to consumers, and the cost comparison of ips vs va panels informs product development and marketing strategies.

What are the key market drivers leading to the rise in the adoption of Electronic Display Devices Industry?

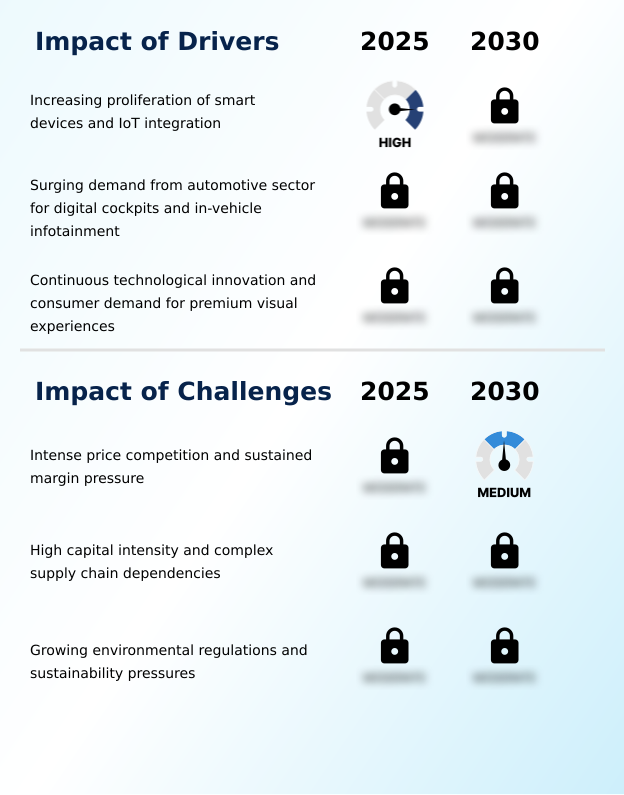

- The increasing proliferation of smart devices and deeper IoT integration is a key driver, making electronic displays the ubiquitous human-machine interface across a vast ecosystem of connected electronics.

- The proliferation of smart devices and IoT integration is a foundational driver, embedding displays as the principal interface in an expanding ecosystem of connected electronics. In automotive, the shift to a software-defined digital environment is transforming vehicle interiors.

- Digital cockpit solutions featuring in-vehicle infotainment systems and advanced driver-assist systems are generating substantial demand for freeform display panels. These systems, often requiring system-on-chip integration and capacitive touch technology, are central to the user experience.

- The trend towards pillar-to-pillar screens consolidates multiple displays, reducing component volume by 25%. This pervasive integration into high-volume addressable markets where automotive-grade requirements are stringent, including standards for sunlight legibility, ensures a diversified demand base.

What are the market trends shaping the Electronic Display Devices Industry?

- A defining market trend is the widespread proliferation of Mini-LED backlighting systems enhancing existing LCD architecture. This runs parallel to the strategic emergence of MicroLED technology as a next-generation emissive display platform.

- The market is shaped by the adoption of novel form factors that redefine product design and user interaction. The use of flexible oled substrates and ultra-thin bendable glass has enabled foldable pc technology, which improves multitasking efficiency by over 40%.

- Beyond foldable designs, the development of rollable and stretchable electrophoretic ink display variants promises new applications in wearables and smart textiles. Concurrently, gaming-specific features such as high pixel response times and adaptive sync technologies are becoming standard. This focus on dynamic motion clarity has led to a 60% increase in the adoption of panels with refresh rates above 120Hz.

- These trends signify a pivotal evolution toward dynamic and adaptable surfaces for commercial digital signage and personal use.

What challenges does the Electronic Display Devices Industry face during its growth?

- Intense price competition coupled with sustained margin pressure represents a key challenge, driven by high capital intensity and cyclical supply-demand imbalances within the market.

- The market confronts significant capital intensity challenges, as constructing advanced fabrication plants requires enormous upfront investment, with upgrade cycles increasing costs by over 30% every few years. These facilities depend on a complex and fragile global supply chain with high supply chain dependencies on a few providers of high-purity glass substrates and other critical materials.

- This concentration creates vulnerabilities to disruptions and adds cost pressure. Concurrently, growing environmental scrutiny and the need for sustainable manufacturing practices are escalating challenges. Regulations like right to repair legislation and a focus on end-of-life management and circular economy principles demand substantial investment in greener technologies and more modular designs, impacting firms' operational planning and profitability.

Exclusive Technavio Analysis on Customer Landscape

The electronic display devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the electronic display devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Electronic Display Devices Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, electronic display devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Apple Inc. - Delivering advanced electronic display devices with tandem OLED, mini-LED backlighting, and high refresh rates, setting benchmarks for visual performance and power efficiency in premium applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Apple Inc.

- BOE Technology Group Co. Ltd.

- Corning Inc.

- DuPont de Nemours Inc.

- E Ink Holdings Inc.

- Fujitsu Ltd.

- HP Inc.

- Innolux Corp.

- LG Display Co. Ltd.

- Mitsubishi Electric

- NEC Corp.

- Panasonic Holdings Corp.

- Powertip Technology Corp

- Royole Corp

- Samsung Electronics Co. Ltd.

- Sharp Corp.

- Sony Group Corp.

- TCL Industries Holdings Ltd.

- Universal Display Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Electronic display devices market

- In September, 2024, Continental AG showcased its Crystal Center Display, a 15-inch frameless automotive display utilizing MicroLED technology to achieve exceptional brightness and transparency for modern vehicle interiors.

- In November, 2024, AU Optronics Corp. demonstrated a 13.5-inch transparent MicroLED display, highlighting the technology's potential for automotive head-up displays and high-end retail signage applications.

- In January, 2025, LG Display Co. Ltd. introduced its third-generation OLED television panels featuring META Technology, which uses a Micro Lens Array to significantly boost brightness and energy efficiency.

- In April, 2025, Samsung Display showcased its Sensor OLED Display, which integrates fingerprint and blood pressure sensing capabilities directly into the panel, enabling more streamlined device designs.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Electronic Display Devices Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 323 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.3% |

| Market growth 2026-2030 | USD 54791.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.1% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The electronic display devices market is defined by intense technological competition, primarily between established liquid crystal display platforms and newer emissive display platforms. While an advanced liquid crystal display leverages innovations like mini-led backlighting and quantum dot enhancement film to enhance performance, organic light emitting diode technology excels with superior contrast and enables flexible oled substrates.

- The industry is now advancing toward microled technology and transparent oled displays, which promise further breakthroughs. In automotive, digital cockpit solutions are becoming standard, driving demand for in-plane switching, freeform display panels to create seamless pillar-to-pillar screens for in-vehicle infotainment and advanced driver-assist systems. Integrating augmented reality heads up displays requires significant R&D budget allocation, a critical boardroom decision.

- These systems rely on components like driver integrated circuits, timing controllers, and high-purity glass substrates. The use of low-temperature polycrystalline oxide backplanes with variable refresh rate technology has improved power efficiency by 20%, a key metric influencing both mobile device design and consumer choice.

- This complex interplay of technologies, from electrophoretic ink display to camera-based digital mirrors, shapes a dynamic and highly innovative landscape.

What are the Key Data Covered in this Electronic Display Devices Market Research and Growth Report?

-

What is the expected growth of the Electronic Display Devices Market between 2026 and 2030?

-

USD 54.79 billion, at a CAGR of 5.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Televisions, Smartphones and tablets, Smart wearables, PC and laptop, and Others), End-user (Commercial, and Residential), Technology (LCD, OLED, LED, and Others) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing proliferation of smart devices and IoT integration, Intense price competition and sustained margin pressure

-

-

Who are the major players in the Electronic Display Devices Market?

-

Apple Inc., BOE Technology Group Co. Ltd., Corning Inc., DuPont de Nemours Inc., E Ink Holdings Inc., Fujitsu Ltd., HP Inc., Innolux Corp., LG Display Co. Ltd., Mitsubishi Electric, NEC Corp., Panasonic Holdings Corp., Powertip Technology Corp, Royole Corp, Samsung Electronics Co. Ltd., Sharp Corp., Sony Group Corp., TCL Industries Holdings Ltd. and Universal Display Corp.

-

Market Research Insights

- The market's dynamics are influenced by a strategic push toward a more seamless visual appearance and an all-screen aesthetic in consumer devices. Innovations in under-display camera technology have improved the effective screen area by over 5%, enhancing user immersion.

- For commercial applications, firms deploying industrial control panels are realizing up to a 15% reduction in operational errors due to improved interface clarity and responsiveness. In automotive, the integration of multiple screens into a single, cohesive unit provides a streamlined user experience.

- This consolidation trend, focused on delivering a premium visual experience, underscores a market-wide shift where performance and design integration are paramount.

We can help! Our analysts can customize this electronic display devices market research report to meet your requirements.

RIA -

RIA -