Interventional Radiology Products Market Size 2026-2030

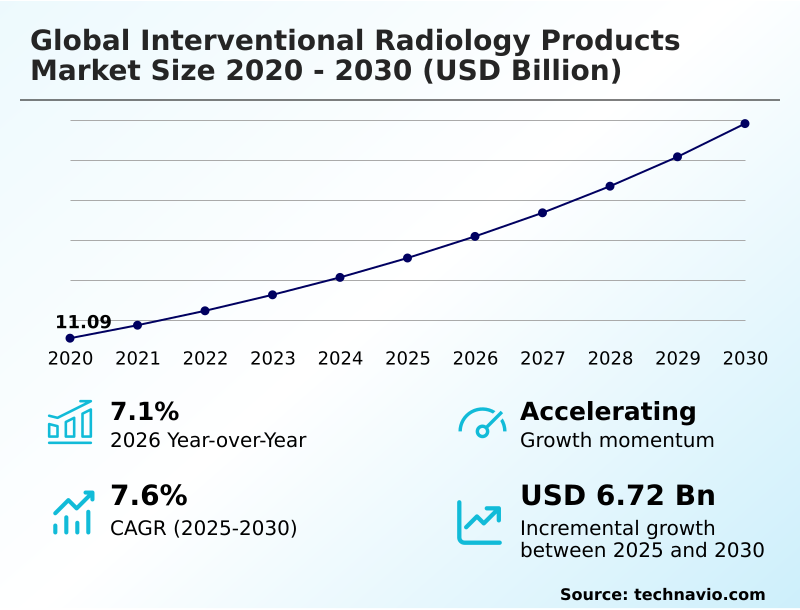

The interventional radiology products market size is valued to increase by USD 6.72 billion, at a CAGR of 7.6% from 2025 to 2030. Increasing global burden of chronic diseases and aging demographics will drive the interventional radiology products market.

Major Market Trends & Insights

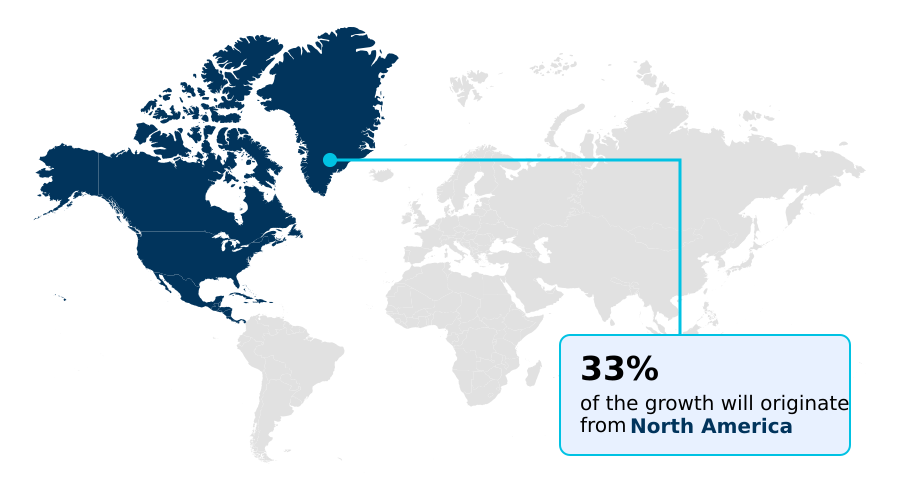

- North America dominated the market and accounted for a 32.6% growth during the forecast period.

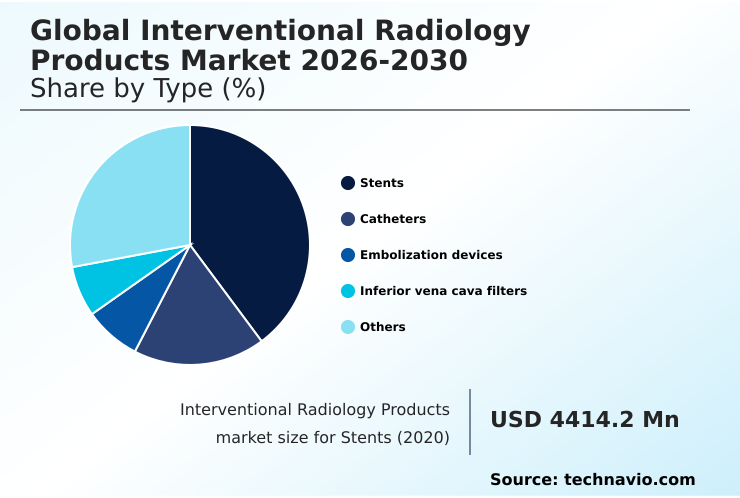

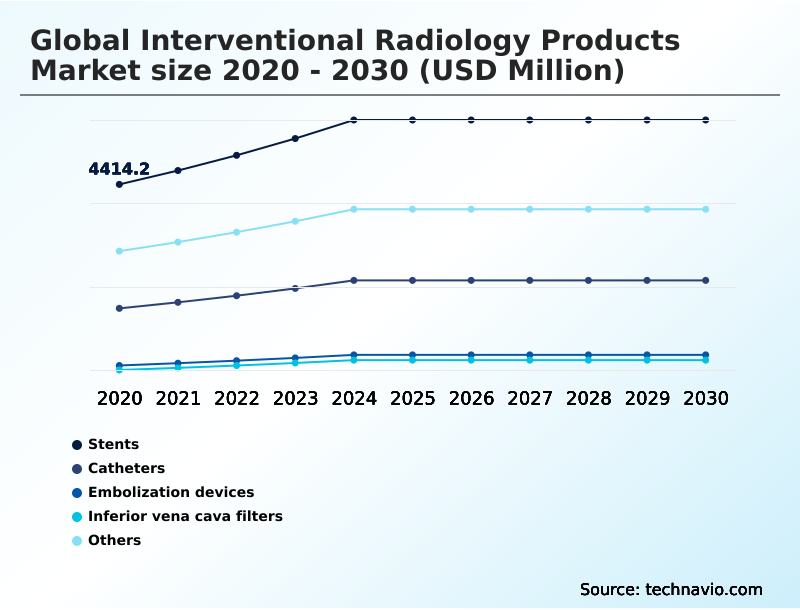

- By Type - Stents segment was valued at USD 5.68 billion in 2024

- By Application - Cardiology segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 10.73 billion

- Market Future Opportunities: USD 6.72 billion

- CAGR from 2025 to 2030 : 7.6%

Market Summary

- The interventional radiology products market is undergoing substantial expansion, driven by a clinical paradigm shift toward minimally invasive, image-guided procedures. This growth is fundamentally supported by the rising global incidence of chronic diseases and an aging population, creating a sustained demand for advanced diagnostic and therapeutic tools.

- Technologies such as drug-eluting stents and mechanical thrombectomy devices have revolutionized treatment for cardiovascular and neurological conditions. Simultaneously, the ascendancy of interventional oncology, utilizing techniques like transarterial chemoembolization and percutaneous tumor ablation, has established a new pillar in cancer care. A key business scenario involves optimizing hospital supply chains for high-volume procedures.

- By implementing just-in-time inventory systems for catheter-based systems and steerable guiding sheaths, facilities can reduce holding costs by over 20% while ensuring critical device availability. However, the market is constrained by high product costs, stringent regulatory pathways, and a scarcity of trained interventionalists.

- The integration of robotics and AI-powered imaging promises to enhance precision and efficiency, but navigating intense pricing pressures from group purchasing organizations remains a critical strategic focus for manufacturers aiming for sustainable operations.

What will be the Size of the Interventional Radiology Products Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Interventional Radiology Products Market Segmented?

The interventional radiology products industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Stents

- Catheters

- Embolization devices

- Inferior vena cava filters

- Others

- Application

- Cardiology

- Urology and nephrology

- Oncology

- Gastroenterology

- Others

- End-user

- Hospitals

- ASCs

- Diagnostic imaging centers

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Type Insights

The stents segment is estimated to witness significant growth during the forecast period.

Stents are a cornerstone of modern practice, indispensable for maintaining patency in various anatomical structures, most notably blood vessels.

This segment includes a wide array of products tailored for specific clinical scenarios in cardiovascular disease treatment and peripheral artery disease interventions. The evolution from bare-metal devices to advanced drug-eluting stents and bioresorbable vascular scaffolds has significantly improved long-term outcomes.

Innovation continues with the development of specialized products such as flow-diverting stents for complex neurovascular intervention and the peripheral self-expanding stent.

Expanding applications now include ureteral stents and devices for endovascular aneurysm repair, driven by a clinical focus on enhancing patient quality of life.

This alignment with value-based healthcare models, where procedures using atherectomy devices improve efficiency by 15%, solidifies their role in both hospital and outpatient procedure settings.

The Stents segment was valued at USD 5.68 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 32.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Interventional Radiology Products Market Demand is Rising in North America Request Free Sample

North America is the largest regional market, distinguished by high healthcare expenditure and rapid adoption of advanced technologies like mechanical thrombectomy devices and catheter-based systems.

The region's sophisticated infrastructure supports a high volume of procedures in hospitals and a growing number of ambulatory surgical centers. In contrast, Asia is the fastest-growing market, led by expanding healthcare access in China and India.

This growth is fueling demand for interventional oncology therapies, including transarterial chemoembolization and radioembolization microspheres for locoregional tumor treatment. Europe represents a mature market, with strong demand for cryoablation systems and hemostatic devices.

However, it faces stringent regulations and pricing pressures that influence technology adoption. Implementing centralized inventory management across multiple office-based labs can decrease supply waste by 18%.

The Rest of World (ROW) region, encompassing South America and the Middle East, shows significant potential for trauma care embolization but is constrained by infrastructure gaps and complex volume-based procurement policies.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic focus for manufacturers in the interventional radiology products market is increasingly on demonstrating clear clinical differentiation and economic value. For instance, the debate over drug-eluting stents vs bioresorbable scaffolds continues, with decisions often hinging on long-term patient outcomes and cost-effectiveness analyses. Similarly, data on microwave vs radiofrequency ablation efficacy is critical for oncology departments making capital investment decisions.

- In neurology, the use of liquid embolic agents in neurovascular procedures is expanding, but it requires extensive physician training, impacting adoption rates. The specific catheter design for chronic total occlusions is a key competitive advantage, as it directly relates to procedural success rates.

- In stroke care, stent retriever thrombectomy success rates are a primary metric, influencing hospital purchasing protocols for advanced thrombectomy systems. The development of a drug-coated balloon for in-stent restenosis addresses a significant unmet clinical need. In oncology, the choice of embolic microspheres for liver tumors depends on precise calibration and delivery.

- The growth of robotic catheter systems for peripheral intervention is tied to demonstrating improved navigability, while fusion imaging for complex aortic repair must prove it reduces procedure time and radiation exposure. Compliance teams closely monitor vena cava filter retrieval complication rates, which have become a focus of regulatory scrutiny.

- The hemostatic device access site closure time is a key efficiency metric in high-volume catheterization labs. Finally, analyzing the regulatory pathways for novel embolization devices is a critical business function, with proactive planning reducing approval timelines by several months compared to reactive strategies.

What are the key market drivers leading to the rise in the adoption of Interventional Radiology Products Industry?

- The increasing global burden of chronic diseases, coupled with aging demographics, is a fundamental driver creating an expanding patient base for minimally invasive procedures.

- The overwhelming preference for minimally invasive procedures is a primary market driver, embraced by clinicians and healthcare systems for its clinical and economic benefits.

- This shift fuels continuous innovation in device engineering, evident in technologies like the steerable guiding sheath and radiopaque liquid embolic agent, which enhance safety in complex endovascular therapy.

- Advances in microcatheter technology and hydrophilic guidewires enable physicians to perform intricate neurovascular intervention and prostate artery embolization with greater precision. For example, the latest aspiration catheters have improved first-pass clot removal rates by up to 15%.

- This preference extends to routine procedures such as percutaneous nephrostomy and the placement of tunneled central venous catheters for vascular access management, driving procedural volumes and incentivizing investment in efficient, high-performance tools, despite pricing pressures from group purchasing organizations.

What are the market trends shaping the Interventional Radiology Products Industry?

- A procedural shift toward outpatient settings, including ambulatory surgical centers, represents a significant market trend. This migration is driven by economic, clinical, and patient-centric incentives.

- The market is being reshaped by the convergence of devices with digital technologies. The integration of AI-powered imaging and fusion imaging software into image-guided therapy systems is enhancing precision and enabling clinical decision support, with some platforms improving lesion targeting accuracy by over 20%.

- A key trend is the development of robotics-ready devices and robotic-assisted catheters, which promise to improve procedural stability and reduce operator radiation exposure. Innovations like interventional MRI technologies are opening new frontiers for real-time guidance. This digital shift influences device design for technologies like microwave ablation systems and stent retrievers.

- The trend is also impacted by evolving medical device regulation, which now requires more rigorous post-market surveillance for both novel and established products, including simple biopsy needles, adding a layer of complexity to innovation.

What challenges does the Interventional Radiology Products Industry face during its growth?

- Stringent regulatory frameworks and prolonged product approval cycles present a significant challenge, creating high barriers to entry and potentially slowing the pace of innovation.

- High product costs and intensifying pricing pressures present significant market challenges. The sophisticated engineering behind devices for structural heart disease repair, such as those for transcatheter aortic valve replacement, results in high prices that can be a barrier to adoption, particularly in systems with tight budgets.

- Healthcare systems increasingly use health technology assessment and volume-based procurement to negotiate lower prices, impacting margins on products like atherectomy balloons and inferior vena cava filters. This pressure is also felt in ambulatory surgical centers, where procedures like vertebroplasty and kyphoplasty must demonstrate clear cost-effectiveness.

- In some value-based healthcare models, bundled payments for procedures using drainage catheters or embolic plug systems have led to a 10% reduction in overall reimbursement, forcing providers to scrutinize device costs more closely.

Exclusive Technavio Analysis on Customer Landscape

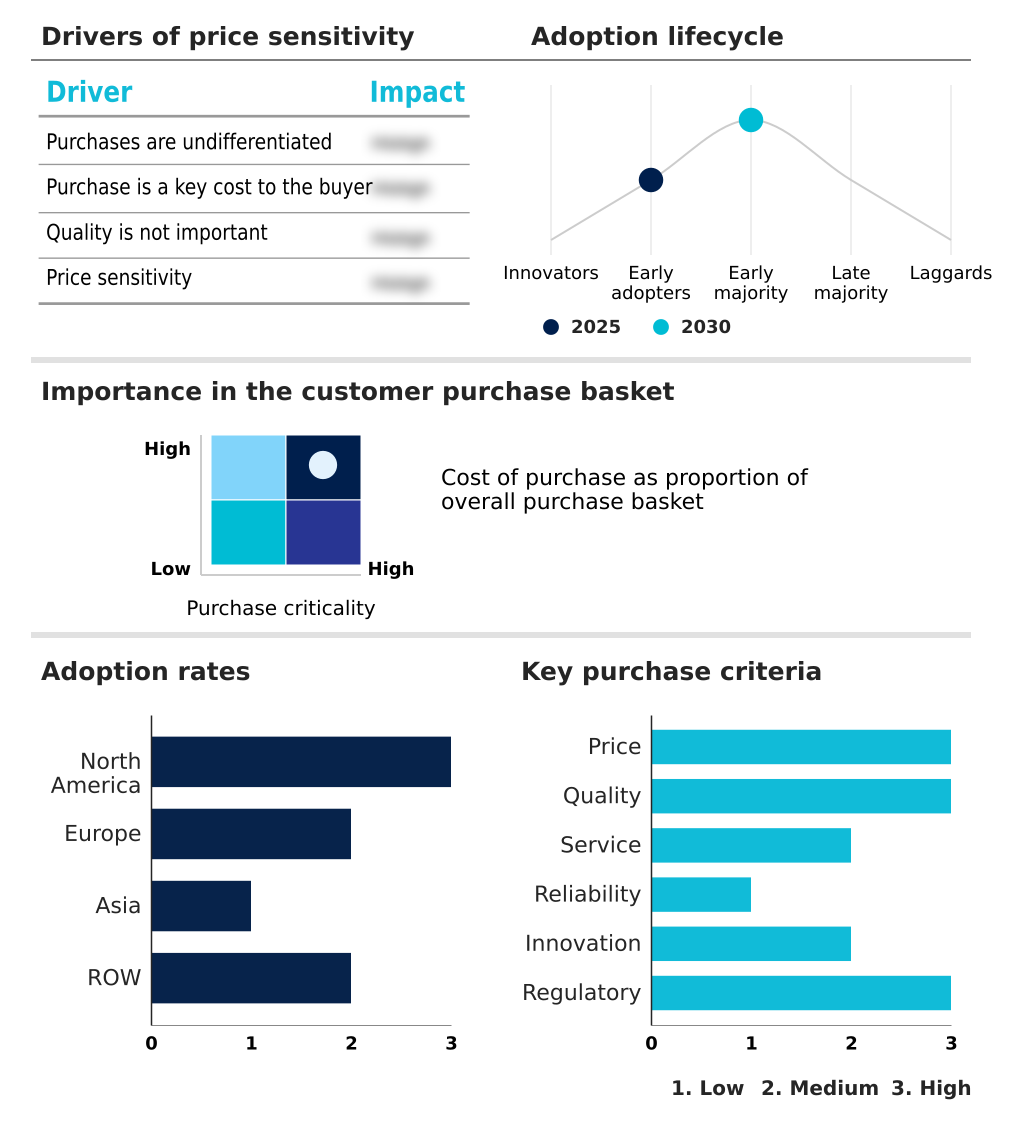

The interventional radiology products market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the interventional radiology products market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Interventional Radiology Products Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, interventional radiology products market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - A research analyst viewpoint indicates the offerings include advanced vascular closure devices, flexible stent systems with chronic outward force, and catheters designed for superior procedural visualization.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Adept Medical Ltd.

- ASAHI INTECC CO. LTD.

- Blueneem Medical Devices

- Boston Scientific Corp.

- Cardinal Health Inc.

- Cook Group Inc.

- GE Healthcare Technologies

- Guerbet

- ILUMARK GmbH

- INRAD Inc.

- Koninklijke Philips NV

- Merit Medical Systems Inc.

- Seda SpA

- Siemens Healthineers AG

- Teleflex Inc.

- Terumo Corp.

- Tokai Medical Products Inc.

- Uresil LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Interventional radiology products market

- In November 2024, CILBA announced it received ANVISA regulatory approval to market its DIALEV-247 long-term hemodialysis catheter in Brazil, marking a strategic entry into the South American market.

- In January 2025, Argon Medical expanded its interventional oncology portfolio through the acquisition of the SeQure and DraKon microcatheters from Accurate Medical Therapeutics, enhancing its capabilities in targeted therapeutic delivery.

- In January 2025, Siemens Healthineers unveiled its Optiq AI, an AI-powered imaging pipeline integrated into its advanced systems to deliver real-time noise reduction and automated exposure optimization for complex procedures.

- In May 2025, Merit Medical Systems acquired Biolife Delaware, LLC for approximately $120 million, gaining access to specialized hemostatic devices like StatSeal and WoundSeal to strengthen its access site closure offerings.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Interventional Radiology Products Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 329 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.6% |

| Market growth 2026-2030 | USD 6717.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.1% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Indonesia, Thailand, Brazil, Saudi Arabia, UAE, Turkey, Argentina, Colombia, South Africa and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The interventional radiology products market is characterized by relentless technological advancement, fundamentally expanding the scope of minimally invasive care. The continuous evolution from basic instruments to sophisticated catheter-based systems, including drug-eluting stents and bioresorbable vascular scaffolds, addresses complex clinical needs.

- Key sub-fields like interventional oncology are propelled by innovations in transarterial chemoembolization and percutaneous tumor ablation, while neurology benefits from advanced mechanical thrombectomy devices and flow-diverting stents. A critical boardroom consideration is aligning R&D investment with evolving regulatory landscapes.

- For example, developing a new radiopaque liquid embolic agent or steerable guiding sheath now requires navigating stricter post-market surveillance protocols, impacting long-term compliance budgets. The integration of fusion imaging software and AI-powered imaging into image-guided therapy systems is enhancing procedural precision, with some centers reporting a 25% reduction in radiation exposure.

- The development of atherectomy balloons, drug-coated balloons, and robotic-assisted catheters further underscores the industry's focus on improving outcomes in endovascular aneurysm repair and beyond.

What are the Key Data Covered in this Interventional Radiology Products Market Research and Growth Report?

-

What is the expected growth of the Interventional Radiology Products Market between 2026 and 2030?

-

USD 6.72 billion, at a CAGR of 7.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Stents, Catheters, Embolization devices, Inferior vena cava filters, and Others), Application (Cardiology, Urology and nephrology, Oncology, Gastroenterology, and Others), End-user (Hospitals, ASCs, and Diagnostic imaging centers) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing global burden of chronic diseases and aging demographics, Stringent regulatory frameworks and prolonged product approval cycles

-

-

Who are the major players in the Interventional Radiology Products Market?

-

Abbott Laboratories, Adept Medical Ltd., ASAHI INTECC CO. LTD., Blueneem Medical Devices, Boston Scientific Corp., Cardinal Health Inc., Cook Group Inc., GE Healthcare Technologies, Guerbet, ILUMARK GmbH, INRAD Inc., Koninklijke Philips NV, Merit Medical Systems Inc., Seda SpA, Siemens Healthineers AG, Teleflex Inc., Terumo Corp., Tokai Medical Products Inc. and Uresil LLC

-

Market Research Insights

- The market is shaped by a confluence of clinical and economic dynamics driving a preference for minimally invasive procedures. The migration of care to outpatient procedure settings and office-based labs is a key structural change, with facilities reporting a 15% improvement in patient throughput for routine vascular access management.

- This shift is reinforced by value-based healthcare models that prioritize cost-effective outcomes. The growth of specialized fields like interventional oncology therapies and neurovascular intervention is creating demand for premium technologies. At the same time, health technology assessment bodies and group purchasing organizations exert significant pricing pressure, forcing manufacturers to demonstrate clear economic benefits.

- Aligning product innovation with these cost-containment goals is critical, as integrated AI-powered imaging platforms have demonstrated the ability to reduce procedural times by up to 12%, directly addressing efficiency demands.

We can help! Our analysts can customize this interventional radiology products market research report to meet your requirements.