Metal Material Based 3D Printing Market Size 2025-2029

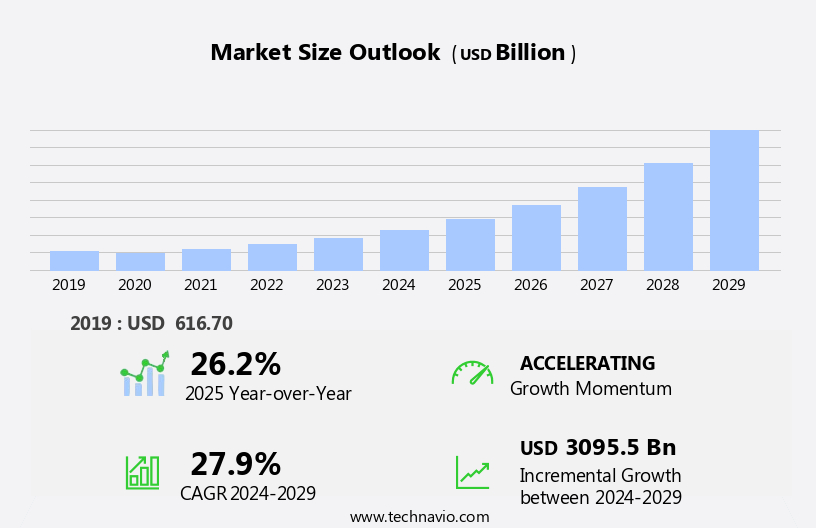

The metal material based 3D printing market size is forecast to increase by USD 3095.5 billion, at a CAGR of 27.9% between 2024 and 2029.

- The Metal Material-Based 3D Printing Market is experiencing significant growth due to the increasing demand for customized and personalized metal products. This trend is driven by advancements in 3D printing technologies that enable the production of complex metal components with high precision and accuracy. These advancements have expanded the capabilities of metal additive manufacturing in various industries, including defense and aerospace. Metal 3D printers are transforming manufacturing expenditure by providing accurate and efficient solutions for various industries, including the dental, education, food, automotive, and consumer electronics segments. However, the high initial investment costs associated with metal 3D printing systems pose a considerable challenge for market entrants.

- Despite this, the potential for producing lightweight, strong, and intricately designed metal parts on-demand offers substantial opportunities for companies in various industries, including automotive, aerospace, and healthcare. To capitalize on these opportunities, businesses must navigate the high upfront costs and continuously innovate to improve efficiency and reduce production costs.

What will be the Size of the Metal Material Based 3D Printing Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The metal material-based 3D printing market continues to evolve, driven by advancements in technology and increasing applications across various sectors. Cobalt alloys, nickel alloys, and titanium alloys are among the metals gaining popularity due to their superior mechanical properties. Binder jetting and powder recycling are transforming the manufacturing process, enabling cost savings and reduced environmental impact. Artificial intelligence (AI) and machine learning are being integrated into the workflow for quality control and process optimization. In the aerospace industry, 3D printing is revolutionizing the production of complex components, while the automotive sector is leveraging the technology for rapid prototyping and custom parts.

The medical field is benefiting from 3D printing for producing implants and dental applications. Industrial machinery, jigs, and fixtures are also being manufactured using additive manufacturing, leading to improved dimensional accuracy and reduced material cost. Print speed, generative design, surface roughness, and topology optimization are critical factors influencing the market dynamics. Support structures and supply chain management are also undergoing significant changes to accommodate the unique requirements of metal 3D printing. Energy consumption and material extrusion are areas of ongoing research to improve the sustainability and efficiency of the manufacturing process. Simulation software, process monitoring, and digital twin technology are essential tools for optimizing the manufacturing process and ensuring consistent quality.

Heat treatment, surface finishing, and non-destructive testing are crucial post-processing steps to enhance the final properties of the printed parts. The market is expected to continue unfolding with new innovations and applications, making it an exciting space to watch.

How is this Metal Material Based 3D Printing Industry segmented?

The metal material based 3d printing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Iron-based

- Titanium

- Nickel

- Aluminum

- End-user

- Healthcare

- Automotive

- Aerospace and defense

- Tool and mold making

- Others

- Technology

- PBF

- DED

- Binder jetting

- Metal extrusion

- Application

- Prototyping

- Functional Parts

- Tooling

- Repair & Overhaul

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

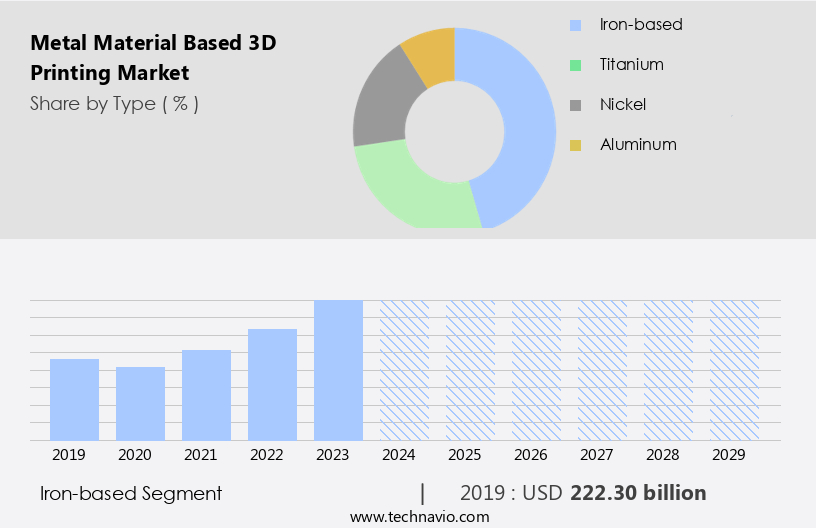

By Type Insights

The iron-based segment is estimated to witness significant growth during the forecast period.

The market encompasses various metal alloys, including nickel, titanium, stainless steel, aluminum, and iron, among others. Binder jetting and powder recycling are prominent technologies driving the market's growth. Artificial intelligence and machine learning are revolutionizing quality control, enabling real-time process monitoring and predictive maintenance. Nickel alloys, known for their high mechanical properties and corrosion resistance, are increasingly used in aerospace components and industrial machinery. Environmental concerns have led to the development of eco-friendly 3D printing resins, reducing the industry's carbon footprint. The market caters to diverse applications, from automotive parts and jigs and fixtures to medical implants and dental applications.

3D printing technologies, such as stereolithography, selective laser melting, and multi jet fusion, offer unique benefits, including high dimensional accuracy, surface finishing, and material extrusion. The market's dynamics are influenced by factors like material cost, energy consumption, build volume, and production cost. Digital twin technology and simulation software enable optimized design, reducing the need for support structures and enhancing yield strength. CAD software, heat treatment, and non-destructive testing ensure the production of high-quality components with desirable mechanical properties, such as tensile strength and fatigue resistance. The supply chain is streamlined through rapid prototyping and custom parts production, ensuring timely delivery and cost savings.

The Iron-based segment was valued at USD 222.30 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

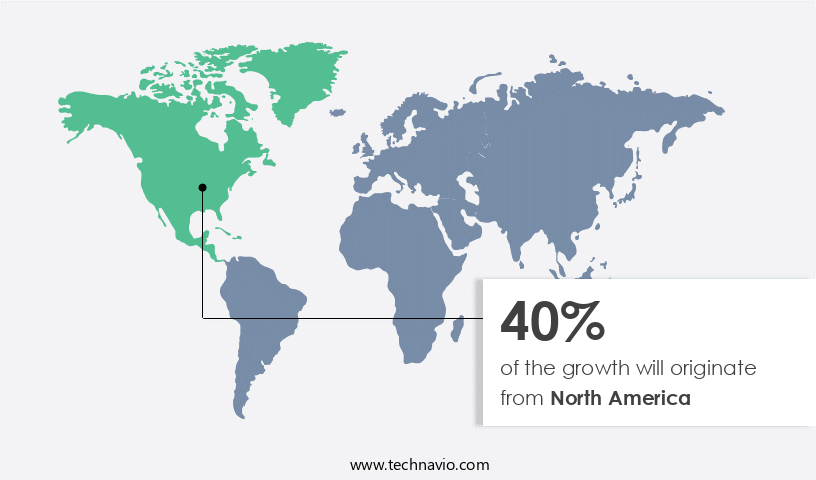

North America is estimated to contribute 40% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In 2024, the North American region significantly contributed to The market. The US government's investment in metal material production and adoption of 3D printers drove this growth. For instance, in February 2025, the University of Waterloo's Multi-Scale Additive Manufacturing (MSAM) Lab secured a USD5 million USD grant from the Federal Economic Development Agency for Southern Ontario. This initiative, aimed at strengthening Waterloo's leadership in additive manufacturing, fostered collaboration between academic institutions and industry partners. Metal alloys, including nickel, titanium, stainless steel, and aluminum, are increasingly used in 3D printing for their mechanical properties and corrosion resistance.

Binder jetting and powder recycling are popular 3D printing technologies for metal materials. Artificial intelligence and machine learning improve quality control, process monitoring, and generative design. Environmental impact is a concern, with energy consumption and material cost being key considerations. Digital twin technology and simulation software help optimize build volume and reduce waste. Aerospace components, automotive parts, industrial machinery, jigs and fixtures, and medical implants are common applications. Additive manufacturing processes, such as stereolithography and multi jet fusion, offer high dimensional accuracy and surface finishing. Heat treatment, non-destructive testing, and post-processing techniques ensure the desired material properties, such as yield strength and tensile strength.

CAD software and cam software streamline the manufacturing process, while topology optimization and support structures enable the production of complex geometries. Supply chain optimization and rapid prototyping reduce lead times and production cost. In conclusion, the market is evolving, with advancements in technology, materials, and applications. The integration of AI, machine learning, and digital twin technology is transforming the manufacturing landscape, offering improved efficiency, cost savings, and customization.

Market Dynamics

The Metal Material Based 3D Printing Market is surging, driven by demand for metal 3D printing powders, titanium alloys, and aluminum alloys in aerospace 3D printing and automotive 3D printing. Technologies like Direct Metal Laser Sintering (DMLS) and Selective Laser Melting (SLM) enable high-precision metal 3D printing for medical 3D printing applications. Sustainable metal 3D printing aligns with eco-conscious trends, while metal 3D printing powders for aerospace, titanium alloys for medical 3D printing, Direct Metal Laser Sintering for automotive parts, Selective Laser Melting for jet engine components, sustainable metal 3D printing for lightweight parts, AI-driven 3D printing optimization for tooling, high-precision metal 3D printing for dental implants, cost-effective metal AM for industrial applications, scalable metal 3D printing for defense sector, and lightweight metal AM solutions for aerospace 2025 shape the industry's innovative future.

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Metal Material Based 3D Printing Industry?

- The significant rise in the adoption of customized and personalized metal products is the primary driving force behind the market's growth.

- The market is experiencing notable growth due to the increasing demand for customized and intricately designed metal components. This trend is fueled by the advantages of additive manufacturing, which enables the production of unique metal parts with optimized design and functionality. In industries such as medical, automotive, and industrial machinery, metal additive manufacturing is revolutionizing the production of complex components, including stainless steel implants, aluminum alloy automotive parts, and industrial jigs and fixtures. Processes like stereolithography (SLA) allow for the creation of highly detailed metal structures, leading to improved functionality and performance. Moreover, digital twin technology and process monitoring with simulation software facilitate efficient design and optimization, reducing material costs and energy consumption.

- For instance, in the medical sector, customized implants can be 3D printed using metal additive manufacturing to fit perfectly with a patient's anatomy, ensuring better implant performance and patient outcomes. Similarly, in the automotive industry, metal additive manufacturing enables the production of lightweight and durable parts, reducing energy consumption and improving overall vehicle efficiency. In summary, The market is witnessing significant growth due to the advantages of additive manufacturing, including optimized design, reduced material costs, and improved performance. Industries such as medical, automotive, and industrial machinery are capitalizing on these benefits to produce customized and intricately designed metal components.

What are the market trends shaping the Metal Material Based 3D Printing Industry?

- Metal material-based 3D printing technologies are experiencing significant advancements, making them the current market trend in the additive manufacturing industry. This innovative technology offers numerous benefits, including the production of complex and lightweight components, increased design freedom, and reduced material waste.

- The market has experienced significant growth due to technological advancements in additive manufacturing techniques. Two notable advancements are the enhancement of laser-based metal 3D printing methods, specifically Laser Powder Bed Fusion (LPBF) and Directed Energy Deposition (DED). LPBF uses a high-powered laser to melt layers of metal powder, producing intricate and precise parts with excellent surface finish. DED, which involves feeding metal wire or powder into a melt pool created by a laser or electron beam, enables the deposition of material layer by layer. These improvements have expanded the capabilities and applications of metal additive manufacturing. For instance, yield strength of cobalt alloys has increased, making them suitable for producing custom parts in industries such as aerospace and automotive.

- Additionally, print speed has been enhanced, reducing production time for complex parts. Moreover, generative design and topology optimization have become more prevalent, allowing for the creation of lightweight yet strong structures. Support structures have also been optimized, reducing the need for post-processing and improving overall efficiency. The supply chain has been transformed as well, with rapid prototyping becoming a more viable option for manufacturing custom parts. Material extrusion and layer thickness have also seen advancements, broadening the range of materials that can be used in metal 3D printing. Despite these advancements, challenges remain, including the high cost of metal powders and the need for further research on material properties and post-processing techniques.

- Nevertheless, the future of metal material based 3D printing looks promising, with continued innovation and investment in research and development.

What challenges does the Metal Material Based 3D Printing Industry face during its growth?

- The high initial investment costs represent a significant challenge impeding the growth of the industry.

- The market faces a significant hurdle in the form of high initial investment costs, which have hindered widespread adoption among businesses. The expense of acquiring metal 3D printers is a major concern, as these advanced machines can cost anywhere from USD1,500 to USD1 million, depending on the intended use by the end-user. This high cost presents a challenge for small and medium-sized enterprises (SMEs), limiting their access to this innovative technology. Despite these challenges, the benefits of metal material based 3D printing are substantial. This additive manufacturing process offers dimensional accuracy, surface finishing, heat treatment, non-destructive testing, and improved material properties such as corrosion resistance, fatigue resistance, and tensile strength.

- These advantages make metal material based 3D printing an attractive option for various industries, including dental applications. To optimize the manufacturing process, users often employ Computer-Aided Design (CAD) software to create digital models for 3D printing. Post-production processes, such as heat treatment and surface finishing, further enhance the final product's quality and durability. By investing in these advanced technologies, businesses can create complex geometries and intricate designs that would be difficult or impossible to achieve using traditional manufacturing methods. In conclusion, while the high cost of metal material based 3D printers presents a significant barrier to entry, the benefits of this manufacturing process, such as dimensional accuracy, improved material properties, and design flexibility, make it a valuable investment for businesses seeking to innovate and stay competitive in their industries.

Exclusive Customer Landscape

The metal material based 3d printing market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the metal material based 3d printing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, metal material based 3d printing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3D Systems Corp. - This company specializes in advanced 3D printing technology, focusing on direct metal printing with titanium alloys, stainless steel alloys, and maraging steel alloys. Their innovative solution revolutionizes the manufacturing industry by enabling the production of complex metal components with unparalleled precision and efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3D Systems Corp.

- BASF SE

- Carpenter Technology Corp.

- Desktop Metal Inc.

- EOS GmbH

- Equispheres Inc.

- General Electric Co.

- Markforged Holding Corp.

- MATERIALISE NV

- Ponoko Inc.

- Proto Labs Inc.

- Renishaw Plc

- Sandvik AB

- SHAPEWAYS HOLDINGS INC.

- Sisma SpA

- SLM Solutions Group AG

- Stratasys Ltd.

- Titomic Ltd.

- TRUMPF SE Co. KG

- Velo3D Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Metal Material Based 3D Printing Market

- In January 2024, GE Additive, a leading provider of metal 3D printing solutions, announced the launch of its new Arcam EBM System, the EBM Q10plus, which offers increased build volume and improved productivity for the aerospace and automotive industries (GE Additive Press Release).

- In March 2024, 3D Systems and Desktop Metal entered into a strategic partnership to expand their metal 3D printing offerings, combining Desktop Metal's innovative metal binder jetting technology with 3D Systems' expertise in production-grade 3D printing solutions (3D Systems Press Release).

- In May 2024, HP Inc. Raised the bar in metal 3D printing with the introduction of their new Multi Jet Fusion 3D Metal Jet platform, capable of producing high-quality, mass-produced metal parts at an unprecedented speed and scale (HP Inc. Press Release).

- In April 2025, SLM Solutions, a global leader in selective laser melting technology, secured a significant investment of â¬20 million from Siemens AG to strengthen their market position and accelerate the development of new metal 3D printing applications (Reuters).

Research Analyst Overview

- The 3D printing market for metal materials is experiencing significant advancements, with various technologies gaining traction. Precision machining and CNC machining continue to dominate traditional manufacturing processes, but ultrasonic welding, VAT polymerization, electron beam, and direct energy deposition are disrupting the industry. Quality assurance is a critical concern, with design validation, sand casting, and investment casting undergoing innovation through software simulation and 3D scanning. Production planning and inventory management are essential elements in metal 3D printing, with build plates, part orientation, print heads, and production planning software optimizing the manufacturing process. Powder bed fusion, powder bed, and sheet lamination are popular techniques, while reverse engineering, laser cladding, high-pressure die casting, and support structures offer unique advantages.

- Design software, file formats, and design for manufacturing are crucial aspects of the metal 3D printing value chain. Laser cutting, waterjet cutting, material jetting, cold spray, and electrochemical machining (ECM) are additional techniques expanding the market's scope. Overall, the metal 3D printing market is dynamic, with continuous innovation in technology and processes shaping its future.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Metal Material Based 3D Printing Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

219 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 27.9% |

|

Market growth 2025-2029 |

USD 3095.5 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

26.2 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Metal Material Based 3D Printing Market Research and Growth Report?

- CAGR of the Metal Material Based 3D Printing industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the metal material based 3d printing market growth of industry companies

We can help! Our analysts can customize this metal material based 3d printing market research report to meet your requirements.

RIA -

RIA -