Artificial Intelligence (AI) Chips Market Size 2026-2030

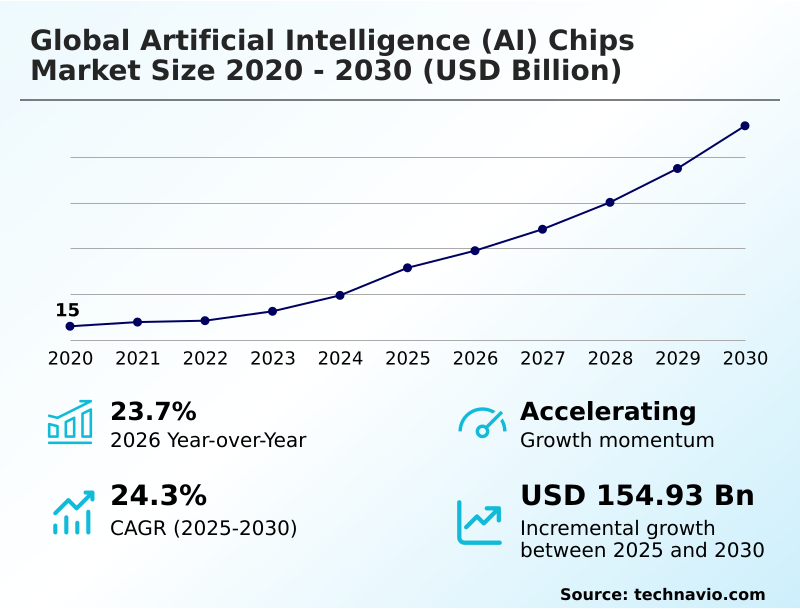

The artificial intelligence (ai) chips market size is valued to increase by USD 154.93 billion, at a CAGR of 24.3% from 2025 to 2030. Proliferation of big data and imperative for advanced data processing will drive the artificial intelligence (ai) chips market.

Major Market Trends & Insights

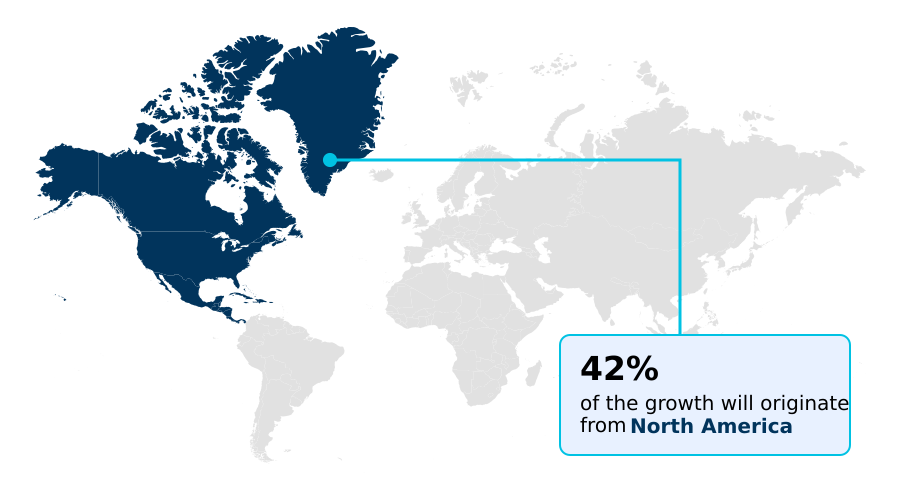

- North America dominated the market and accounted for a 41.7% growth during the forecast period.

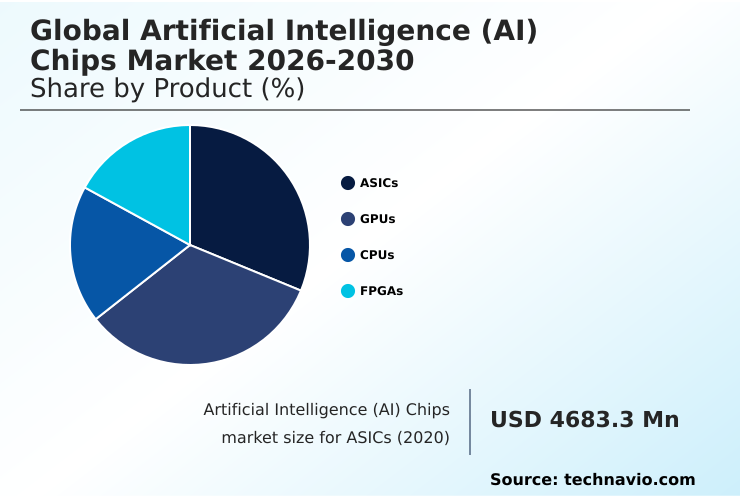

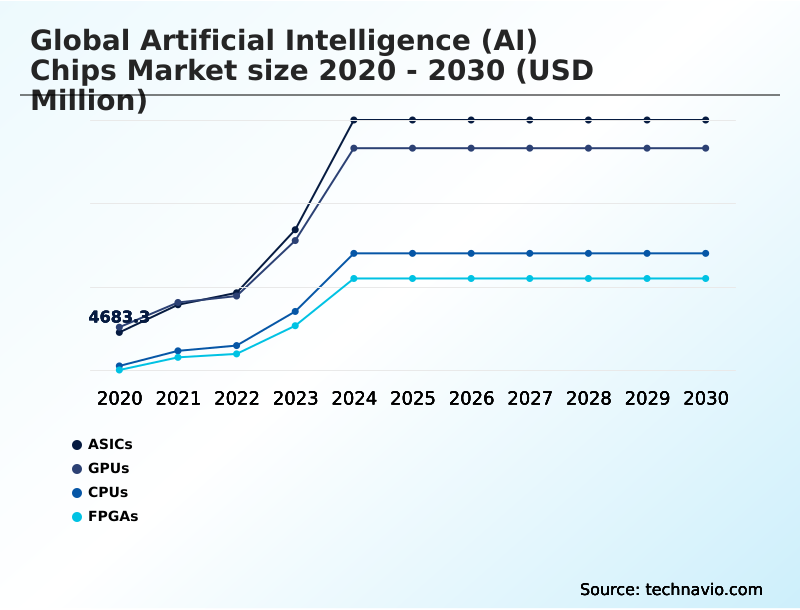

- By Product - ASICs segment was valued at USD 16.70 billion in 2024

- By End-user - Media and advertising segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 218.67 billion

- Market Future Opportunities: USD 154.93 billion

- CAGR from 2025 to 2030 : 24.3%

Market Summary

- The Artificial Intelligence (AI) Chips Market is undergoing a fundamental transformation, driven by the escalating complexity of AI workloads and the demand for specialized hardware. This evolution is fostering a highly competitive environment where innovation in custom silicon and parallel processing architecture is paramount.

- The proliferation of big data from sources like IoT devices and social media creates a perpetual need for more powerful computational hardware to extract actionable insights. For example, in retail, AI-driven supply chain optimization relies on chips that can process vast datasets in real-time to forecast demand, reducing inventory costs and improving efficiency.

- However, the industry grapples with challenges such as the extreme technical complexity of hardware-software co-design and the high capital investment required for semiconductor fabrication.

- Architectural diversification toward solutions like the field programmable gate array and application specific integrated circuit is a key trend, moving the market away from general-purpose processors to purpose-built silicon for specific tasks from the cloud to the intelligent edge.

What will be the Size of the Artificial Intelligence (AI) Chips Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Artificial Intelligence (AI) Chips Market Segmented?

The artificial intelligence (ai) chips industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- ASICs

- GPUs

- CPUs

- FPGAs

- End-user

- Media and advertising

- BFSI

- IT and telecommunication

- Others

- Type

- Cloud

- Edge

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- APAC

- China

- Japan

- South Korea

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By Product Insights

The asics segment is estimated to witness significant growth during the forecast period.

The application specific integrated circuit segment is defined by bespoke design, where custom silicon is engineered to perform a singular function with maximum efficiency.

This approach to hardware acceleration is ideal for mature, high-volume AI workload optimization where the underlying algorithms are stable. By hardwiring computational flows, these chips deliver unparalleled performance-per-watt metric, a critical advantage for large-scale data center deployments.

Unlike a wafer-scale engine, an ASIC trades flexibility for peak operational excellence, drastically reducing inference latency for its designated task.

This specialization makes the deep learning accelerator the ultimate solution for power-efficient processing in environments where cost and energy consumption are paramount, improving performance-per-watt by over 50% compared to general-purpose hardware.

The ASICs segment was valued at USD 16.70 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Artificial Intelligence (AI) Chips Market Demand is Rising in North America Get Free Sample

The geographic landscape is led by North America, which accounts for 41.7% of the market's incremental growth, fueled by intense data center acceleration and innovation.

Meanwhile, APAC is the fastest-growing region, with a projected CAGR of 25.1%, driven by expanding digital economies and government-led initiatives.

In this competitive environment, the adoption of the field programmable gate array and the reconfigurable dataflow unit is increasing for applications requiring real-time inference. Advanced interconnect technology is critical for linking thousands of AI superchips into cohesive systems.

These systems are designed for low-latency processing, a key requirement for both cloud services and emerging edge applications that utilize digital signal processors and in-memory computing to handle complex workloads efficiently.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- A comprehensive review of the Global Artificial Intelligence (AI) Chips Market 2026-2030 requires analyzing several key facets. The Global Artificial Intelligence (AI) Chips Market 2026-2030 segmentation reveals distinct categories, with ASICs in artificial intelligence applications providing peak efficiency, while GPUs for deep learning training offer programmability, and FPGAs for low-latency inference address real-time needs.

- The core Global Artificial Intelligence (AI) Chips Market 2026-2030 drivers include the relentless growth of data and the expanding adoption of AI. Key Global Artificial Intelligence (AI) Chips Market 2026-2030 trends point toward specialization, including the rise of energy efficient AI hardware solutions and specific edge computing AI processor trends.

- Examining the Global Artificial Intelligence (AI) Chips Market 2026-2030 regional outlook shows varied adoption rates and strategic priorities across geographies. However, significant Global Artificial Intelligence (AI) Chips Market 2026-2030 challenges persist, such as high AI chip manufacturing cost analysis and persistent AI chip software ecosystem challenges.

- The semiconductor technology impact on AI is profound, enabling innovations like chiplet technology for AI processors and the use of high bandwidth memory in AI accelerators. Advanced concepts such as in-memory computing for AI and explorations into neuromorphic chip architecture benefits are pushing boundaries.

- The Global Artificial Intelligence (AI) Chips Market 2026-2030 vendor analysis highlights the race to develop custom silicon for cloud AI and specialized AI hardware for generative models. In business operations, such as supply chain management, deploying these technologies has improved forecast accuracy by more than double compared to legacy systems.

What are the key market drivers leading to the rise in the adoption of Artificial Intelligence (AI) Chips Industry?

- The proliferation of big data and the corresponding imperative for advanced data processing capabilities are key drivers for the market.

- The market is fundamentally driven by the need to process vast parallel data streams for computational-intensive tasks. The established parallel processing architecture of the graphics processing unit remains a cornerstone for achieving high model training performance.

- However, demand is growing for specialized hardware like the tensor processing unit and the neural processing unit, which are purpose-built for AI workloads.

- Organizations are building out massive cloud AI infrastructure, with some hyperscalers increasing their AI compute capacity by over 60% annually.

- This infrastructure relies on processors equipped with high bandwidth memory to feed data to the cores efficiently, ensuring that the hardware can handle the scale of today's foundation models and deliver actionable insights from big data.

What are the market trends shaping the Artificial Intelligence (AI) Chips Industry?

- A defining market trend is the move toward architectural diversification. This involves a proliferation of specialized processors designed to meet specific AI workload demands.

- A primary trend is the diversification toward specialized hardware, including advancements in neuromorphic computing and heterogeneous computing systems. This shift enables more efficient on-device machine learning and supports increasing algorithmic complexity scaling without relying solely on cloud resources. The use of advanced packaging and chiplet design is becoming mainstream, allowing for more powerful and modular processors.

- For instance, these designs have enabled a 25% increase in computational density on a single package. Furthermore, the focus on adaptive computing is crucial for inference at the edge, where reconfigurable hardware can adapt to new models.

- The adoption of low-precision computing is another key trend, reducing memory bandwidth requirements by up to 50% in certain applications, which is critical for power-constrained edge devices.

What challenges does the Artificial Intelligence (AI) Chips Industry face during its growth?

- Prohibitive development costs, combined with complex manufacturing economics, present a key challenge affecting industry growth.

- Significant challenges persist, rooted in the extreme complexity of semiconductor fabrication and the high cost of electronic design automation software. Managing the thermal design power of high-performance chips remains a critical issue, with cooling systems now accounting for up to 40% of data center energy consumption.

- The von neumann bottleneck continues to limit performance, driving innovation in hardware-software co-design to bring processing closer to data. The design of a modern system on chip involves intricate computational lithography and verification processes.

- Furthermore, optimizing the matrix multiplication engine and vector processing units within these chips requires a deep talent pool, but there is a persistent industry shortage, with open roles for skilled engineers increasing by 25% year-over-year.

Exclusive Technavio Analysis on Customer Landscape

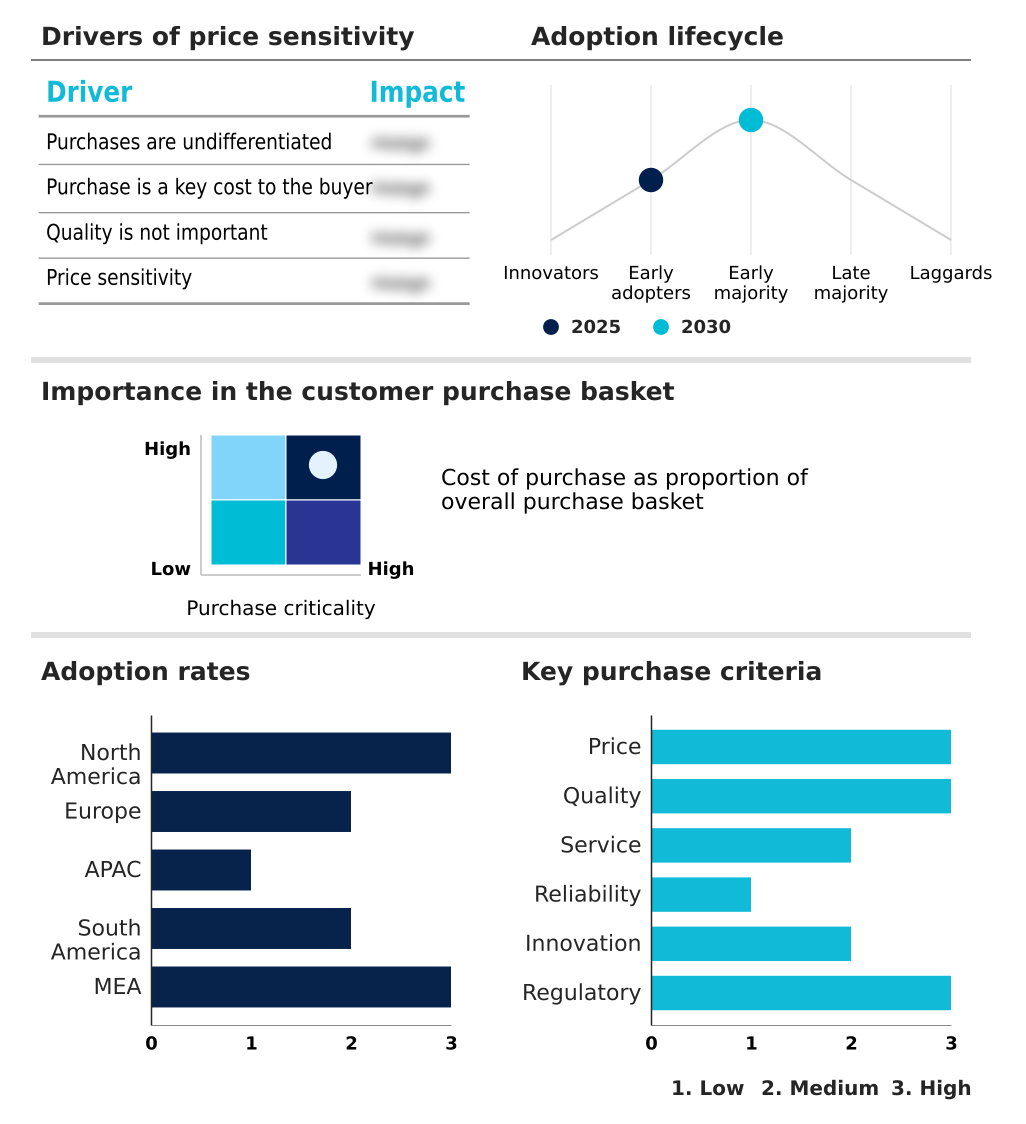

The artificial intelligence (ai) chips market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the artificial intelligence (ai) chips market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Artificial Intelligence (AI) Chips Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, artificial intelligence (ai) chips market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Micro Devices Inc. - Specialized silicon for high-performance data center training and inference workloads addresses critical computational demands in enterprise AI.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Amazon.com Inc.

- Apple Inc.

- Arm Ltd.

- Baidu Inc.

- Cerebras Systems Inc.

- Fujitsu Ltd.

- Graphcore Ltd.

- Hailo Technologies Ltd.

- Huawei Technologies Co. Ltd.

- IBM Corp.

- Intel Corp.

- MediaTek Inc.

- Microsoft Corp.

- NVIDIA Corp.

- NXP Semiconductors NV

- Qualcomm Inc.

- Rebellions Inc.

- SambaNova Systems Inc.

- Samsung Electronics Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Artificial intelligence (ai) chips market

- In March 2025, SoftBank acquired U.S. chip startup Ampere Computing in a strategic move to fortify its own AI infrastructure and capabilities.

- In August 2025, Saudi Arabia's Humain announced plans for new data centers in Riyadh and Dammam, which are set to be powered by advanced AI chips from U.S. companies Nvidia and AMD.

- In September 2025, Nvidia announced a substantial investment in OpenAI, a move aimed at deepening the collaboration between the world-leading AI chip designer and a premier AI research and deployment company.

- In October 2025, Nvidia secured an agreement to supply over 260,000 of its next-generation Blackwell AI chips to South Korea to support the build-out of the country's national AI infrastructure.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Artificial Intelligence (AI) Chips Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 316 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 24.3% |

| Market growth 2026-2030 | USD 154928.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 23.7% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, China, Japan, South Korea, India, Australia, Indonesia, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is driven by the need for dedicated hardware acceleration. The landscape is moving beyond the general-purpose graphics processing unit to embrace the application specific integrated circuit and the field programmable gate array. This push for custom silicon, often arranged in a chiplet design with advanced packaging, is essential for creating a powerful deep learning accelerator.

- Architects are developing heterogeneous computing systems featuring the tensor processing unit and neural processing unit to tackle the von neumann bottleneck. Innovations like the wafer-scale engine and reconfigurable dataflow unit showcase the focus on parallel processing architecture. These complex designs rely on sophisticated electronic design automation tools for computational lithography and semiconductor fabrication.

- Emerging technologies like in-memory computing and neuromorphic computing promise further gains. For boardroom strategy, adopting low-precision computing is key, as it can reduce data center power usage by 30%. This, combined with advanced interconnect technology and high bandwidth memory on each system on chip, defines the next generation of AI hardware.

What are the Key Data Covered in this Artificial Intelligence (AI) Chips Market Research and Growth Report?

-

What is the expected growth of the Artificial Intelligence (AI) Chips Market between 2026 and 2030?

-

USD 154.93 billion, at a CAGR of 24.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (ASICs, GPUs, CPUs, and FPGAs), End-user (Media and advertising, BFSI, IT and telecommunication, and Others), Type (Cloud, and Edge) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Proliferation of big data and imperative for advanced data processing, Prohibitive development costs and complex manufacturing economics

-

-

Who are the major players in the Artificial Intelligence (AI) Chips Market?

-

Advanced Micro Devices Inc., Amazon.com Inc., Apple Inc., Arm Ltd., Baidu Inc., Cerebras Systems Inc., Fujitsu Ltd., Graphcore Ltd., Hailo Technologies Ltd., Huawei Technologies Co. Ltd., IBM Corp., Intel Corp., MediaTek Inc., Microsoft Corp., NVIDIA Corp., NXP Semiconductors NV, Qualcomm Inc., Rebellions Inc., SambaNova Systems Inc. and Samsung Electronics Co. Ltd.

-

Market Research Insights

- The market is characterized by a dynamic shift toward purpose-built silicon to manage increasingly computational-intensive tasks. This move away from general-purpose hardware is driven by the need for superior model training performance and AI workload optimization. As a result, designs focusing on an improved performance-per-watt metric are becoming standard, with some specialized chips achieving a 40% reduction in inference latency.

- This focus on efficiency and speed is critical for both large-scale cloud AI infrastructure and power-constrained on-device machine learning applications. The strategic adoption of hardware-software co-design is further enabling these gains, with certain architectures lowering power consumption by over 25% for targeted AI functions, directly impacting the total cost of ownership for enterprises.

We can help! Our analysts can customize this artificial intelligence (ai) chips market research report to meet your requirements.

RIA -

RIA -