China Gaming Market Size 2025-2029

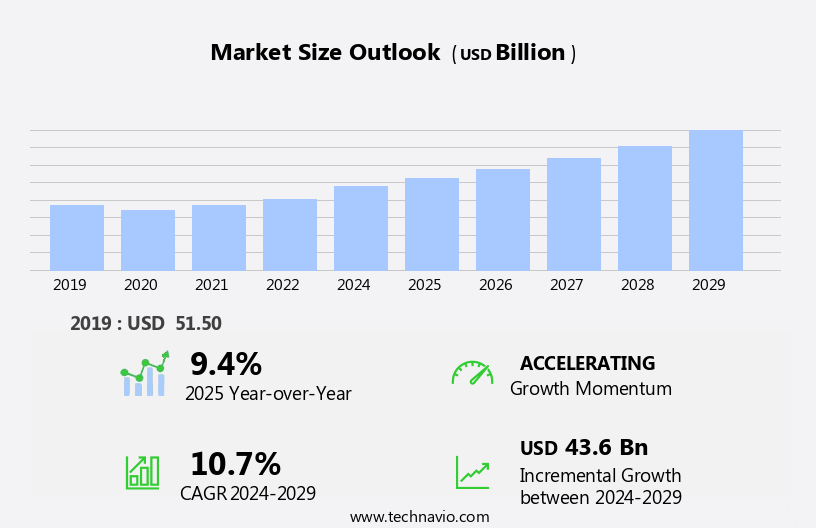

The china gaming market size is forecast to increase by USD 43.6 billion, at a CAGR of 10.7% between 2024 and 2029.

- The market is experiencing significant growth, driven by the increasing disposable income of consumers and the expansion of cloud gaming services. The rise in disposable income allows more individuals to invest in gaming devices and subscriptions, leading to a larger consumer base. Additionally, cloud gaming services are gaining popularity, offering convenience and accessibility to gamers. However, this market faces challenges, including data security and privacy issues. With the increasing amount of personal information being shared online, concerns regarding data protection are becoming more prominent.

- Companies operating in this market must prioritize robust security measures to mitigate these risks and maintain consumer trust. In summary, the market presents substantial opportunities for growth, fueled by rising disposable income and the adoption of cloud gaming services. However, companies must address data security and privacy concerns to effectively capitalize on these opportunities and navigate the market's challenges.

What will be the size of the China Gaming Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- The Chinese gaming market, a significant global force, witnesses dynamic trends and activities. Game streaming hardware and infrastructure, including cloud gaming services and platforms, shape the future of gaming accessibility. Game localization tools facilitate the expansion of game franchises into the Chinese market, ensuring player engagement. Game remakes and sequels fuel sales, while e-sports analytics and merchandise capitalize on the growing e-sports scene. Game engine optimization and QA ensure high-quality gaming experiences, mitigating issues and enhancing player satisfaction. Game licensing and player behavior analytics enable publishers to segment their audience effectively, tailoring offerings to specific demographics. Game pre-orders, expansions, and testing generate revenue and anticipation, while e-sports broadcasting and server management maintain a seamless gaming experience.

- Game copyright and piracy remain ongoing challenges, necessitating cybersecurity measures for gaming platforms. Game development software and game streaming software cater to the needs of developers and content creators, fostering innovation. Game revenue streams continue to diversify, with revenue from various sources, including advertising, subscriptions, and in-game purchases, contributing to the market's growth.

How is this market segmented?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Casual gaming

- Professional gaming

- Device

- Mobile

- Gaming console

- PC

- Platform

- Online

- Offline

- Geography

- APAC

- China

- APAC

By Type Insights

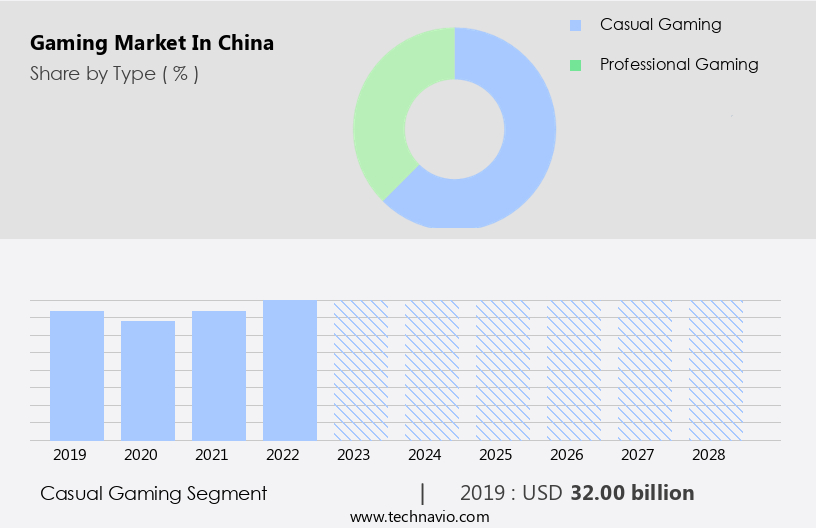

The casual gaming segment is estimated to witness significant growth during the forecast period.

In China's gaming market, various elements contribute to the dynamic and evolving landscape. Casual games, which appeal to a broad demographic due to their simplicity and accessibility, attract a vast audience. These games, often featuring easy-to-learn mechanics and short play sessions, are popular among non-core gamers, including younger and older demographics, as well as women and the elderly. Game content creation and optimization are crucial, ensuring engaging experiences for players. Console gaming and PC gaming continue to thrive, with console manufacturers and PC developers releasing new titles and updates. Security remains a priority, with game developers implementing measures to protect players from cheating and hacking.

Pay-to-win (P2W) and free-to-play (F2P) models dominate the market, with players able to purchase in-game items or subscribe to services for enhanced gameplay experiences. Game patches and updates keep titles fresh, while mobile gaming's convenience and accessibility make it a significant player in the market. E-sports sponsorships and tournaments fuel the competitive scene, with teams and influencers promoting games and driving engagement. Game mechanics, artificial intelligence, and deep learning enhance gameplay and create immersive experiences. Social media integration and influencer marketing expand reach and engagement. Game design, level design, and character design are essential elements, with user interface, user experience, and game art creating visually appealing and intuitive games.

Game analytics and machine learning help developers understand player behavior and preferences, ensuring player retention and monetization strategies. Network latency and game performance are crucial for optimal gameplay, with game engines and cloud gaming technologies addressing these challenges. Battle royale games and first-person shooters continue to dominate the market, with role-playing games, strategy games, and simulation games also popular. In-app purchases, game subscription services, and in-game advertising generate revenue, while game patches and updates keep titles fresh and engaging. E-sports teams and influencer marketing further monetize the gaming ecosystem. The market remains a vibrant and innovative space, with continuous advancements in technology and game design shaping the future of gaming.

The Casual gaming segment was valued at USD 32.00 billion in 2019 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the China Gaming Market drivers leading to the rise in adoption of the Industry?

- Disposable income plays a crucial role in driving market growth, as an increase in this financial resource enables consumers to purchase more goods and services.

- The market is experiencing significant growth due to the expanding middle class and increasing disposable income. With urbanization progressing and income levels rising, consumers are investing more in entertainment, including video games. According to the National Bureau of Statistics of China, per capita disposable income reached approximately USD5,511 in 2023, marking a 6.3% year-on-year increase. This economic growth is fueling demand for both casual and professional gaming experiences. Game content creation, optimization, and performance are crucial aspects of this market. Console gaming and mobile gaming are popular choices, with game security a top priority. Pay-to-win (p2w) models and game patches are common practices.

- Level design, game mechanics, and artificial intelligence (AI) are essential elements of game development. Moreover, e-sports sponsorships are on the rise, attracting major brands and investors. Game servers ensure smooth gameplay and maintain harmonious game environments. As the market evolves, game mechanics and AI are becoming increasingly sophisticated, offering immersive gaming experiences. Overall, the market presents significant opportunities for businesses, with a large and growing consumer base.

What are the China Gaming Market trends shaping the Industry?

- Cloud gaming services are experiencing significant expansion, representing the latest market trend. This growth is driven by advancements in technology and increasing consumer demand for on-demand, high-quality gaming experiences.

- In China, the gaming market is experiencing significant growth due to the proliferation of cloud gaming services. This innovation allows users to stream high-game quality experiences directly to various devices, including smartphones, tablets, smart TVs, and low-end PCs, using a reliable internet connection. Eliminating the need for expensive gaming hardware makes gaming more accessible to a larger demographic, breaking down barriers such as hardware limitations and geographical restrictions. Game developers are responding to this trend by increasing their focus on game localization, game reviews, and social media integration to cater to the diverse gaming community. The popularity of free-to-play (F2P) models, such as first-person shooter (FPS) games, has led to an increase in in-game advertising and game subscription services.

- Furthermore, advancements in technology, including deep learning, are enhancing the immersive nature of gaming experiences. Moreover, the rise of game streaming and e-sports teams has created a vibrant gaming ecosystem, with players from all walks of life coming together to share their experiences and compete against each other. This inclusive community is driving innovation and growth in the Chinese gaming market, making it an exciting space for businesses to explore.

How does China Gaming Market faces challenges face during its growth?

- Data security and privacy concerns represent significant challenges that can hinder industry growth. Companies must prioritize implementing robust security measures and adhere to regulatory compliance to protect sensitive information and maintain consumer trust.

- The Chinese gaming market presents unique challenges for companies in the areas of data security and privacy. With the increasing popularity of live streaming platforms and the monetization strategies such as game DLC and in-game advertising, vast amounts of user data are being collected and processed. This data includes personal information, gameplay preferences, social interactions, and financial transactions. While this data is used for game customization, targeted advertising, and user analytics, it also raises concerns about privacy protection and data security. Cybersecurity threats, including hacking, data breaches, phishing attacks, malware infections, and distributed denial-of-service (DDoS) attacks, pose significant risks to gaming companies in China.

- Cybercriminals target these companies to steal sensitive information, compromise user accounts, disrupt services, and extort ransom payments. Game design elements such as network latency and game art also require robust security measures to prevent unauthorized access and manipulation. E-sports tournaments and influencer marketing further amplify the importance of data security. Game influencers have a significant impact on player acquisition and retention, and their endorsements can influence user behavior and spending patterns. As a result, gaming companies must ensure that user data is protected from unauthorized access and misuse, particularly when it comes to sensitive information related to influencer partnerships and financial transactions.

- In conclusion, the Chinese gaming market presents both opportunities and challenges for companies. While the market is growing rapidly, with trends such as battle royale games, role-playing games (RPGs), and let's play content gaining popularity, data security and privacy remain critical concerns. Companies must prioritize data security measures to protect user information, prevent cyber attacks, and build trust with their user base.

Exclusive China Gaming Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 37 Interactive Entertainment Network Technology Group Co. Ltd.

- Bandai Namco Holdings Inc.

- Beijing Elex Technology Co. Ltd.

- Electronic Arts Inc.

- Kunlun Wanwei Technology Co. Ltd.

- Microsoft Corp.

- NetEase Inc.

- Nintendo Co. Ltd.

- Perfect World

- SEGA SAMMY CREATION INC.

- Shanda

- Sony Group Corp.

- Take Two Interactive Software Inc.

- Tencent Holdings Ltd.

- Virtuos

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Gaming Market In China

- In March 2023, Tencent Holdings Ltd., the leading gaming company in China, announced the global launch of its highly anticipated multiplayer online battle arena game, "Arena of Valor: Beyond the West" (Reuters). This expansion marks a significant geographic entry for Tencent, aiming to tap into international markets and diversify its revenue streams.

- In June 2023, Alibaba Group Holding Ltd. And NetEase, Inc. Formed a strategic partnership to jointly develop and operate mobile games (Xinhua Net). This collaboration is expected to strengthen both companies' positions in the Chinese gaming market by combining their resources, expertise, and user bases.

- In October 2024, ByteDance, the creator of TikTok, raised over USD3 billion in a funding round for its gaming subsidiary, Larksuite Technology Co. Ltd. (Bloomberg). This substantial investment will support the development of new games and expansion into the competitive gaming market.

- In December 2025, the Chinese government issued new regulations to further tighten control over online gaming for minors, limiting playtime to three hours per week (Xinhua Net). This policy change aims to address concerns regarding the potential negative impact of gaming on children's health and education. Despite the restrictions, the market continues to grow, driven by the increasing popularity of mobile games and the continuous innovation from domestic and international players.

Research Analyst Overview

The market continues to evolve, with dynamic market activities unfolding across various sectors. Game content creation and optimization remain key focus areas, as developers strive to enhance console gaming experiences and ensure game security. Free-to-play (F2P) models, first-person shooter (FPS) games, and battle royale titles dominate the landscape, with mobile gaming and PC gaming also maintaining strong presence. Social media integration, e-sports teams, and influencer marketing are shaping the industry's landscape, as streaming platforms and live events attract massive audiences. In-game advertising, deep learning, and machine learning (ML) are being employed to personalize user experiences and optimize game performance.

Game development and localization are ongoing processes, with game guides and level design essential for player acquisition and retention. Network latency, game patches, and game updates are crucial for maintaining optimal game servers and addressing performance issues. Artificial intelligence (AI) and computer vision are revolutionizing game mechanics, while game design, character design, and user interface (UI) undergo continuous refinement. Game subscription services and in-app purchases offer alternative monetization strategies, as game communities and forums foster engagement and discussion. The market remains a vibrant, ever-changing ecosystem, where innovation and adaptation are the keys to success.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Gaming Market in China insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

169 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.7% |

|

Market growth 2025-2029 |

USD 43.6 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

9.4 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across China

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -