Cloud Infrastructure Services Market Size 2026-2030

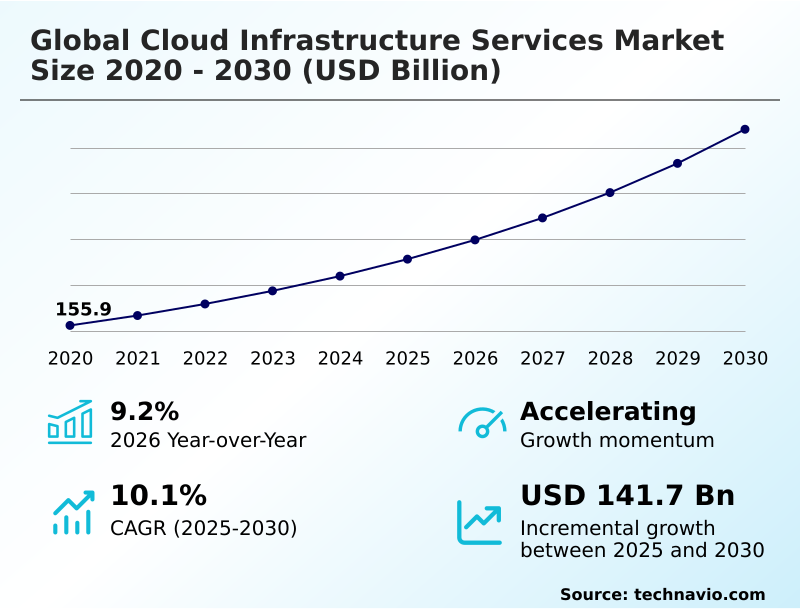

The cloud infrastructure services market size is valued to increase by USD 141.7 billion, at a CAGR of 10.1% from 2025 to 2030. Pervasive imperative of digital transformation will drive the cloud infrastructure services market.

Major Market Trends & Insights

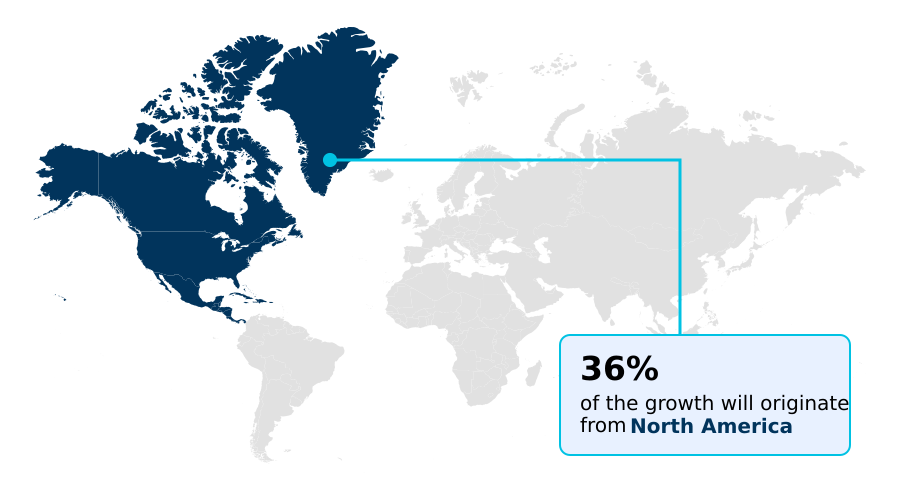

- North America dominated the market and accounted for a 36% growth during the forecast period.

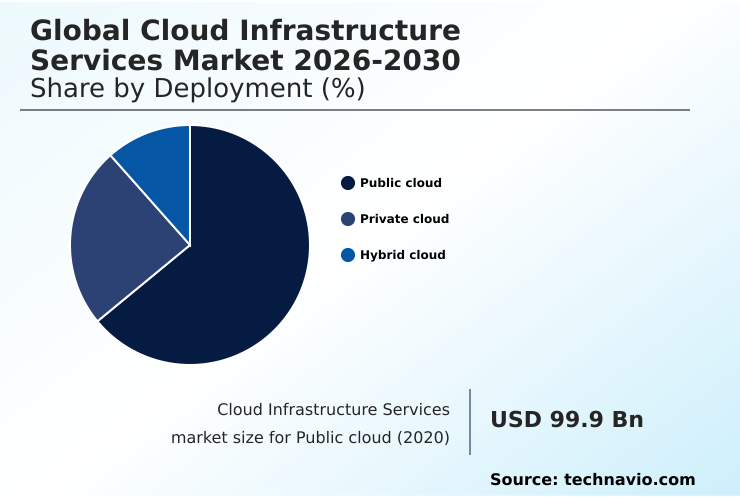

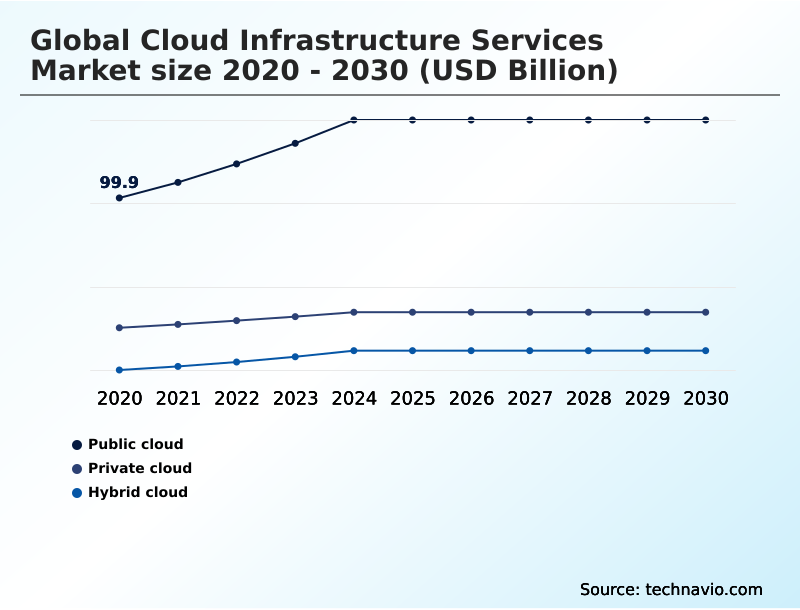

- By Deployment - Public cloud segment was valued at USD 137 billion in 2024

- By Service Type - Compute as a service segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 214 billion

- Market Future Opportunities: USD 141.7 billion

- CAGR from 2025 to 2030 : 10.1%

Market Summary

- The Cloud Infrastructure Services Market is fundamentally driven by the enterprise-wide mandate for digital transformation. Organizations are moving beyond legacy on-premises systems, leveraging on-demand resource scaling and consumption-based pricing models to gain agility and competitive advantage. This transition enables rapid development and deployment of cloud-native applications through robust CI/CD pipeline integration.

- Key trends include the adoption of hybrid cloud management and multi-cloud governance to mitigate vendor lock-in and optimize workload placement. For instance, a global manufacturer can use a hybrid model to run latency-sensitive robotics controls on a private edge computing platform while using a public cloud's powerful data analytics platforms for predictive maintenance across its supply chain.

- The pervasive integration of AI/ML workload optimization and IoT data ingestion platforms is also crucial. However, the market is not without its hurdles. Cloud billing complexity, data egress cost management, and a persistent shortage of skilled professionals create significant operational challenges.

- Navigating data sovereignty laws and implementing effective cloud compliance frameworks remain top priorities for enterprises operating on a global scale, shaping their cloud infrastructure automation and enterprise cloud strategy.

What will be the Size of the Cloud Infrastructure Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Cloud Infrastructure Services Market Segmented?

The cloud infrastructure services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- Public cloud

- Private cloud

- Hybrid cloud

- Service type

- Compute as a service

- Storage as a service

- Network as a service

- Others

- End-user

- Large enterprises

- SMEs

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Deployment Insights

The public cloud segment is estimated to witness significant growth during the forecast period.

The public cloud segment is defined by multi-tenant infrastructure delivering extensive economies of scale and a consumption-based pricing model. This approach facilitates a critical shift from capital to operational expenditure, enabling on-demand resource scaling for enterprises.

The model is central to application modernization, supporting cloud-native applications and microservices architecture. Providers are integrating post-quantum cryptography to secure data against future threats, a move that enhances the value proposition for mission-critical workloads.

This ongoing innovation in areas like managed Kubernetes and software-defined networking provides access to cutting-edge technology. Businesses leveraging the public cloud often see improvements in deployment speeds of over 40%, directly impacting their time to market.

This agility, combined with CI/CD pipeline integration and cloud compliance frameworks, is essential for digital transformation enablers and maintaining a competitive edge in the Cloud Infrastructure Services Market.

The Public cloud segment was valued at USD 137 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cloud Infrastructure Services Market Demand is Rising in North America Get Free Sample

The geographic landscape of the Cloud Infrastructure Services Market is led by North America, which accounts for over 35% of the market, driven by its advanced technological adoption and the presence of major providers.

This region sees extensive use of disaster recovery solutions and high-performance computing. However, the APAC region is the fastest-growing, with a projected growth rate exceeding 10%, fueled by widespread digital transformation and a massive internet user base.

Data sovereignty and data residency requirements are shaping investment globally, compelling providers to build in-country data centers. For instance, compliance with data protection laws in Europe necessitates local infrastructure.

This geographic expansion supports real-time data processing and reduces latency, with deployments of virtual private clouds and network as a service improving application performance for users worldwide, a key tenet of cloud performance monitoring.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Successfully navigating the Cloud Infrastructure Services Market requires a focus on advanced operational strategies. When managing costs in multi-cloud environments, organizations must implement robust finops practices and cloud cost optimization techniques. Implementing infrastructure as code with Terraform is a key component of cloud infrastructure automation, allowing for repeatable and scalable deployments.

- For security, implementing a zero-trust security model and securing serverless computing functions are no longer optional. Organizations must also consider the benefits of using ARM-based VMs for cloud-native applications, which can offer significant performance-per-watt advantages. Hybrid cloud orchestration tools comparison becomes critical for enterprises seeking to balance on-premises investments with public cloud agility.

- Furthermore, achieving GDPR compliance in public cloud environments and understanding the impact of data sovereignty laws are board-level concerns, directly influencing architecture and data placement. For specialized workloads, high-performance computing on cloud infrastructure and optimizing database performance in cloud are essential for innovation.

- Businesses see that cost-effective object storage tiering strategies reduce long-term data retention costs by more than half compared to traditional archiving. The benefits of managed Kubernetes services and the use of serverless computing for IoT backends accelerate development, but the challenges of the cloud infrastructure skills gap remain.

- Finally, reducing latency with edge computing and adopting cloud infrastructure sustainability practices are becoming key differentiators.

What are the key market drivers leading to the rise in the adoption of Cloud Infrastructure Services Industry?

- The pervasive imperative for digital transformation across all industries is the primary driver propelling demand for agile and scalable cloud infrastructure services.

- The market's expansion is fundamentally propelled by the pervasive need for digital transformation and the compelling economic shift from CapEx to OpEx.

- By leveraging consumption-based pricing models, organizations report TCO reductions of up to 30% compared to managing private data centers. This financial agility, coupled with the on-demand resource scaling of cloud infrastructure, underpins modern enterprise cloud strategy.

- Furthermore, the proliferation of data-intensive technologies is a major catalyst. The demand for scalable infrastructure to support real-time data processing and data analytics platforms is immense.

- Cloud providers guarantee exceptional data durability, often exceeding 99.999%, which is critical for these workloads. This reliability, combined with robust data center virtualization and cloud access security broker solutions, makes cloud adoption a strategic necessity.

What are the market trends shaping the Cloud Infrastructure Services Industry?

- A dominant trend is the strategic enterprise embrace of hybrid and multi-cloud architectures. This reflects a sophisticated approach to infrastructure deployment that balances control with scalability.

- A defining trend is the strategic pivot towards higher levels of abstraction, specifically container orchestration and serverless computing. This shift is reshaping consumption patterns, as enterprises increasingly favor platform services that accelerate the deployment of cloud-native applications.

- This move away from managing virtual machines simplifies CI/CD pipeline integration and fosters greater developer agility, leading to a 40% reduction in time-to-market for new digital services. Concurrently, the pervasive integration of AI/ML workload optimization and API gateway management is transforming cloud platforms into intelligent systems.

- This democratization of advanced analytics enables broader innovation, with some firms reporting a 25% improvement in data model accuracy using managed services. These trends are supported by advancements in zero trust security architecture and cloud performance monitoring.

What challenges does the Cloud Infrastructure Services Industry face during its growth?

- Pervasive security, governance, and data privacy concerns represent the most significant challenge affecting broader industry growth and adoption.

- Key challenges revolve around financial governance and the pervasive skills gap. The complexity of cloud billing can lead to budget overruns, with some organizations reporting unmanaged cloud spend can escalate costs by over 20%. This necessitates disciplined finops practices and effective cloud cost optimization to prevent waste. Concurrently, the strategic risk of cloud vendor lock-in from proprietary services constrains flexibility.

- Another significant hurdle is the critical shortage of skilled professionals; critical roles in cloud security and architecture remain unfilled 15% longer than other IT positions. This talent deficit, coupled with the intricacies of managing a shared responsibility model and navigating the IaaS vs PaaS comparison for application modernization, slows the pace of cloud migration and adoption for many enterprises.

Exclusive Technavio Analysis on Customer Landscape

The cloud infrastructure services market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cloud infrastructure services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cloud Infrastructure Services Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cloud infrastructure services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Akamai Technologies Inc. - Providers deliver distributed cloud platforms, encompassing edge computing and web application protection, engineered for high performance and security at a global scale.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Akamai Technologies Inc.

- Alibaba Cloud

- Amazon Web Services Inc.

- Baidu Inc.

- Dell Technologies Inc.

- DigitalOcean Holdings Inc.

- Fujitsu Ltd.

- Google Cloud

- Hewlett Packard

- Huawei Cloud Computing Co Ltd

- IBM Corp.

- Microsoft Corp.

- NTT DATA Corp.

- Oracle Corp.

- OVH Groupe SA

- Rackspace Technology Inc.

- VMware Inc.

- VULTR

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cloud infrastructure services market

- In August 2025, Amazon Web Services launched a new, fully managed hybrid cloud platform designed to provide a consistent operational experience across on-premises data centers and the AWS cloud, addressing the complexity of hybrid environments.

- In May 2025, Microsoft Azure announced a significant global expansion of its purpose-built infrastructure for high-performance computing and AI, rolling out next-generation virtual machines with advanced GPUs and high-throughput networking.

- In April 2025, Google announced its first custom Arm-based CPU for data centers, named Axion, designed to deliver leading performance and energy efficiency, intensifying competition through specialized hardware development for AI workloads.

- In February 2025, Alibaba Cloud inaugurated its first data center in Mexico, expanding its footprint in Latin America to provide cloud computing services specifically tailored for local enterprises and their digital transformation needs.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cloud Infrastructure Services Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 303 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10.1% |

| Market growth 2026-2030 | USD 141.7 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.2% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Cloud Infrastructure Services Market is defined by the enterprise shift from capital-intensive on-premises models to agile, scalable solutions. This evolution is centered on core technologies like virtual machines and object storage, but the real value is moving up the stack to managed Kubernetes, serverless computing, and high-performance computing.

- A defining trend is the adoption of multi-cloud governance, where boardroom decisions now weigh the strategic benefit of avoiding vendor lock-in against the operational complexity of managing disparate environments. This strategy demands robust infrastructure as code practices and software-defined networking for consistent policy enforcement.

- Enterprises leveraging these advanced platforms for their microservices architecture are achieving significant performance gains; for example, some have reported a 30% reduction in data processing times for critical analytics workloads.

- However, realizing these benefits is contingent on addressing challenges like data sovereignty, data residency, and implementing effective cloud security posture management across all platforms, from virtual private clouds to the network edge.

What are the Key Data Covered in this Cloud Infrastructure Services Market Research and Growth Report?

-

What is the expected growth of the Cloud Infrastructure Services Market between 2026 and 2030?

-

USD 141.7 billion, at a CAGR of 10.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Public cloud, Private cloud, and Hybrid cloud), Service Type (Compute as a service, Storage as a service, Network as a service, and Others), End-user (Large enterprises, and SMEs) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Pervasive imperative of digital transformation, Pervasive security, governance, and data privacy concerns

-

-

Who are the major players in the Cloud Infrastructure Services Market?

-

Akamai Technologies Inc., Alibaba Cloud, Amazon Web Services Inc., Baidu Inc., Dell Technologies Inc., DigitalOcean Holdings Inc., Fujitsu Ltd., Google Cloud, Hewlett Packard, Huawei Cloud Computing Co Ltd, IBM Corp., Microsoft Corp., NTT DATA Corp., Oracle Corp., OVH Groupe SA, Rackspace Technology Inc., VMware Inc. and VULTR

-

Market Research Insights

- The market's momentum is driven by compelling operational efficiencies and economic benefits. Organizations report infrastructure TCO reductions of up to 40% by adopting consumption-based pricing models and eliminating resource over-provisioning. This shift facilitates digital transformation enablers, with firms accelerating product deployment cycles by over 50% through cloud infrastructure automation and CI/CD pipeline integration.

- The enterprise cloud strategy is evolving, with a clear focus on data analytics platforms and AI/ML workload optimization to extract business value. However, complexities in cloud billing and the challenges of cloud migration persist. Managing data egress costs and mitigating vendor lock-in are critical concerns, prompting more sophisticated multi-cloud governance and finops practices to ensure financial control and strategic flexibility.

We can help! Our analysts can customize this cloud infrastructure services market research report to meet your requirements.

RIA -

RIA -