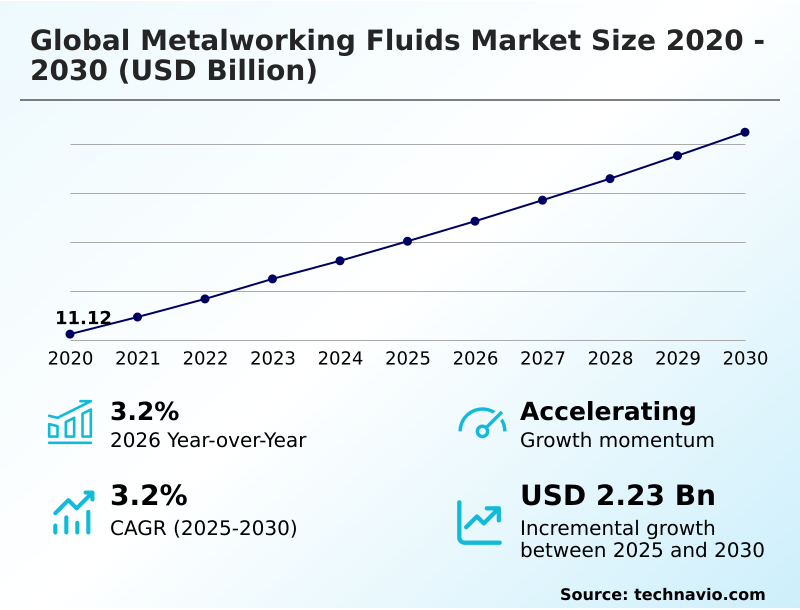

Metalworking Fluids Market Size 2026-2030

The metalworking fluids market size is valued to increase by USD 2.23 billion, at a CAGR of 3.2% from 2025 to 2030. Increasing industrialization in emerging economies will drive the metalworking fluids market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 49.2% growth during the forecast period.

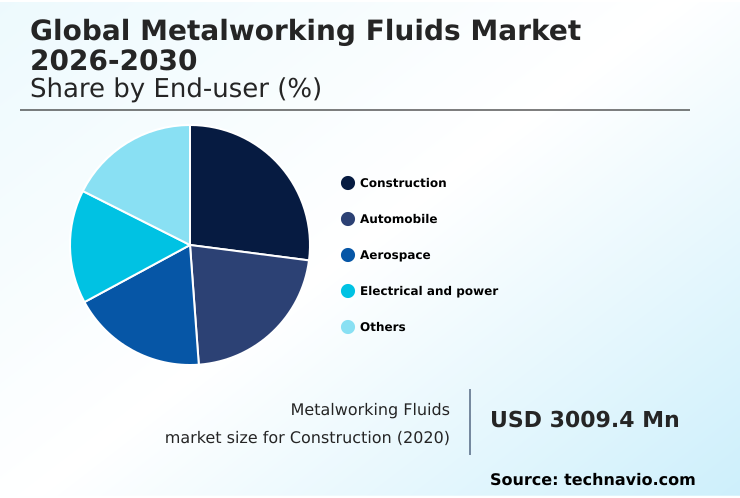

- By End-user - Construction segment was valued at USD 3.41 billion in 2024

- By Product - Mineral segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 4.13 billion

- Market Future Opportunities: USD 2.23 billion

- CAGR from 2025 to 2030 : 3.2%

Market Summary

- The metalworking fluids market is integral to global manufacturing, providing essential lubrication and cooling for precision machining operations. Its trajectory is shaped by increasing industrialization, particularly in emerging economies, which drives demand for high-performance fluids to support automotive, aerospace, and heavy machinery production.

- A key trend is the shift toward sustainability, with a growing emphasis on bio-based and synthetic formulations that minimize environmental impact and enhance worker safety. For instance, a Tier 1 automotive supplier might transition its production line from a conventional mineral oil-based fluid to a biodegradable, high-lubricity synthetic to meet stringent new environmental regulations.

- This move not only ensures compliance but also reduces tool wear and improves surface finish, leading to lower operational costs and higher-quality components. However, the industry grapples with challenges such as the disposal of used fluids and fluctuating raw material prices.

- Innovations in fluid chemistry, including advanced corrosion inhibitors and biocides, along with the adoption of Industry 4.0 technologies for real-time monitoring, are crucial for optimizing fluid performance and addressing these complexities.

What will be the Size of the Metalworking Fluids Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Metalworking Fluids Market Segmented?

The metalworking fluids industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

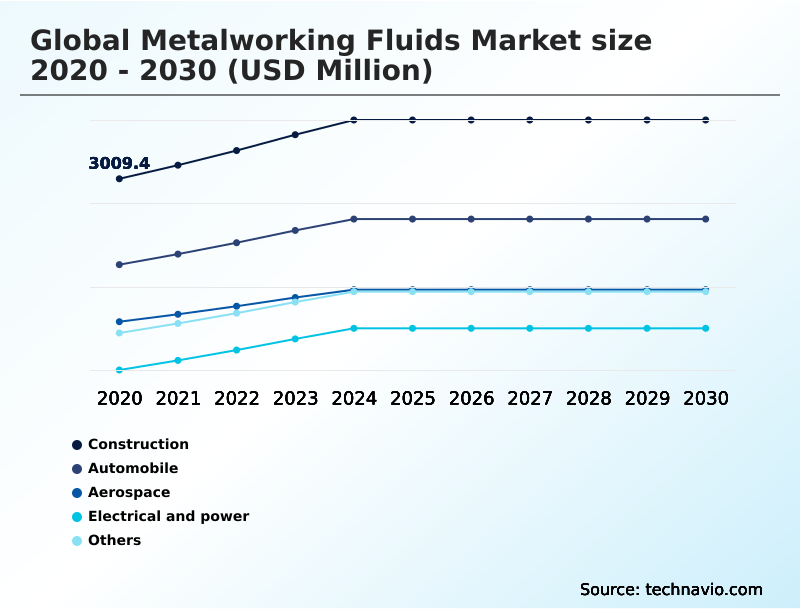

- End-user

- Construction

- Automobile

- Aerospace

- Electrical and power

- Others

- Product

- Mineral

- Synthetic

- Bio-based

- Application

- Water-soluble fluids

- Neat cutting oils

- Corrosion preventives

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- Italy

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By End-user Insights

The construction segment is estimated to witness significant growth during the forecast period.

The construction segment’s demand for metalworking fluids is driven by the need for precision in fabricating metal components for machinery and structural frameworks. These operations necessitate effective workpiece cooling efficiency and robust corrosion inhibitor additive packages.

Advanced forming lubricant and rust preventative coating technologies are critical as automated fabrication processes become standard. The adoption of high-performance fluids directly impacts operational outcomes, with some applications achieving up to a 15% improvement in tool life.

This reliance on specialized synthetic cutting fluid formulations for enhanced machining performance underscores the segment’s focus on productivity and quality, especially in large-scale infrastructure projects where consistent results are paramount.

The use of a specific grinding fluid filtration also plays a key role.

The Construction segment was valued at USD 3.41 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 49.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Metalworking Fluids Market Demand is Rising in APAC Request Free Sample

The geographic landscape of the metalworking fluids market is led by APAC, which accounts for approximately 49% of the market's incremental growth.

This dominance is fueled by robust industrialization and a massive manufacturing base in countries like China and India, where demand for everything from automotive engine component coolant to general machining lubricants is high.

North America and Europe remain significant markets, driven by advanced manufacturing sectors such as aerospace, where specialized aerospace machining lubricant and heavy-duty machining fluid are critical.

In these mature regions, the focus is on high-performance, sustainable solutions that comply with strict environmental standards.

The adoption of advanced fluid management techniques in these markets has been shown to improve workpiece cooling efficiency by over 15%, directly impacting productivity and component quality across various end-user industries.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the metalworking fluids market increasingly hinge on a nuanced understanding of specific application needs and total cost of ownership. For manufacturers, determining the best coolant for cnc milling aluminum involves balancing performance with environmental impact, often leading to an evaluation of the cost-benefit of synthetic metalworking fluids versus traditional options.

- The selection of a metalworking fluid for titanium alloys in the aerospace sector, for example, requires lubricants that can withstand extreme pressures and temperatures. Across all industries, the question of how to extend coolant sump life is a primary operational concern. Effective strategies for managing bacterial growth in coolants and reducing tramp oil in machine coolant are essential.

- This often involves a comprehensive fluid management program for manufacturing, which can reduce fluid consumption by up to 20% compared to unmanaged systems. Furthermore, learning how to prevent rust with water-soluble fluids is crucial for protecting finished parts. The rise of sustainable manufacturing is also pushing the adoption of bio-based cutting oil for medical devices and other precision applications.

- As companies weigh the metalworking fluid recycling system cost, the overall goal remains consistent: to enhance efficiency, ensure quality, and maintain compliance in a competitive industrial landscape, whether through choosing a fluid for grinding steel or a lubricant for heavy-duty metal forming.

What are the key market drivers leading to the rise in the adoption of Metalworking Fluids Industry?

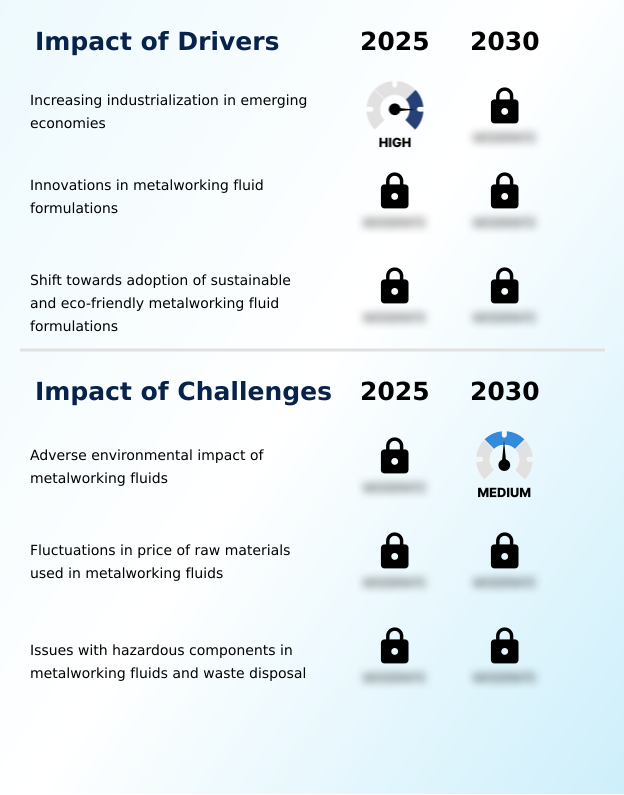

- Increasing industrialization in emerging economies is a key driver, fueling demand for metalworking fluids as manufacturing capabilities expand globally.

- Increasing industrialization and the continuous pursuit of manufacturing efficiency are primary drivers for the metalworking fluids market. As emerging economies expand their industrial capacity, the demand for high-performance fluids that support complex machining operations grows.

- Innovations in fluid formulations, such as advanced synthetic and semi-synthetic fluid types, are enabling significant gains in productivity. For example, a new synthetic cutting fluid can increase tool life by up to 25%, directly reducing operational costs.

- Moreover, optimized fluids enhance machining performance, allowing for higher speeds and feeds, which can shorten cycle times by as much as 10% in high-volume production environments.

- This drive for efficiency is pushing the development of specialized solutions, including those with superior lubricity agent and antifoam additive packages, to meet the demands of modern manufacturing.

What are the market trends shaping the Metalworking Fluids Industry?

- The emergence of bio-based metalworking fluids is a notable trend, reflecting a wider industry shift toward sustainability and reduced environmental impact.

- Key trends in the metalworking fluids market are centered on sustainability and digitalization. The emergence of bio-based and biodegradable lubricant options is reshaping product portfolios, with newer formulations demonstrating a 50% improvement in biodegradability over conventional mineral oils. This shift addresses environmental regulations and corporate sustainability goals, pushing innovation in fluid chemistry, including advanced emulsifier package designs.

- Concurrently, the integration of Industry 4.0 technologies for monitoring fluid condition in real-time is gaining traction. This allows for predictive maintenance and optimized fluid usage, with early adopters reporting a 20% reduction in fluid-related production stoppages.

- This trend toward 'smart fluids' and greener formulations, such as those with improved hard water stability and low-foaming coolant properties, is setting a new standard for performance and efficiency.

What challenges does the Metalworking Fluids Industry face during its growth?

- The adverse environmental impact associated with metalworking fluids poses a significant challenge, driving regulatory changes and the adoption of sustainable alternatives.

- The primary challenges facing the metalworking fluids market are environmental regulations and raw material price volatility. The adverse environmental impact of traditional fluids has led to stringent regulations on disposal and worker exposure, driving up compliance costs. For instance, the cost of managing and disposing of used fluids can constitute a significant portion of a facility's maintenance budget.

- In response, the industry is shifting toward solutions like advanced fluid recycling systems, which can recover up to 90% of used coolants, drastically reducing waste volumes and disposal expenses. Additionally, fluctuations in the price of petroleum and other raw materials create financial uncertainty for both fluid manufacturers and end-users.

- This has increased interest in bio-based and other alternative formulations with more stable input costs, with some manufacturers reducing cost volatility by 15% through strategic reformulation, including the use of boron-free coolant and chlorine-free cutting oil.

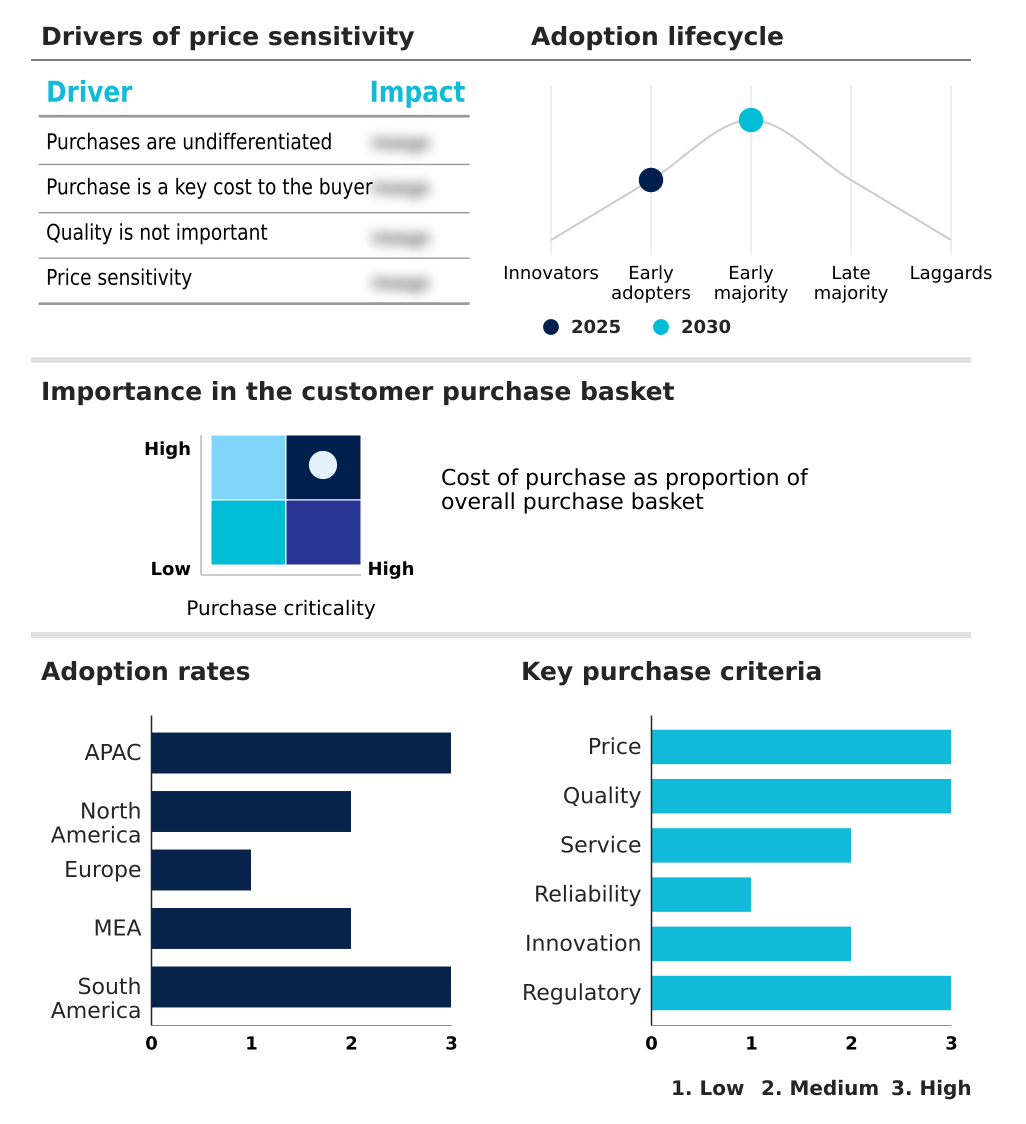

Exclusive Technavio Analysis on Customer Landscape

The metalworking fluids market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the metalworking fluids market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Metalworking Fluids Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, metalworking fluids market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Blaser Swisslube - Offerings center on advanced formulations designed to enhance machining efficiency, improve surface finish quality, and extend tool life across diverse industrial metalworking applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Blaser Swisslube

- BP Plc

- Chevron Corp.

- China Petrochemical Corp.

- CONDAT

- ENEOS Corp.

- Exxon Mobil Corp.

- FUCHS SE

- Henkel AG and Co. KGaA

- Idemitsu Kosan Co. Ltd.

- Italmatch Chemicals Spa

- Master Fluid Solutions

- Motul group

- PETROFER

- PJSC LUKOIL

- Quaker Houghton

- TotalEnergies SE

- YUSHIRO Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Metalworking fluids market

- In November 2025, Americo Chemical Products completed its acquisition of Fusion Chemical, a move designed to broaden its portfolio of metalworking fluids, hybrid cooling products, and high-performance lubricants for various machining applications.

- In October 2025, FUCHS finalized the acquisition of its Swiss partner, ASEOL SUISSE, significantly strengthening its strategic position and footprint in the metalworking fluids and lubrication technology sector across European industries.

- In May 2025, Clariant introduced new synthetic metalworking fluids at Inter Lubric 2025 in Shanghai, showcasing an expanded Hostagliss portfolio designed to meet modern performance, environmental, and efficiency requirements.

- In April 2025, PETRONAS Lubricants International and Quaker Houghton announced a strategic partnership to combine advanced fluid technologies with broad regional distribution, aiming to deliver enhanced industrial metalworking solutions in key Asian markets.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Metalworking Fluids Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3.2% |

| Market growth 2026-2030 | USD 2234.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.2% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, France, Italy, UK, Spain, The Netherlands, South Africa, Saudi Arabia, UAE, Egypt, Turkey, Brazil, Chile and Argentina |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The metalworking fluids market remains a critical enabler of modern manufacturing, where the selection of a fluid—from a basic neat cutting oil to an advanced micro-emulsion technology—directly impacts operational efficiency. The industry is characterized by a continuous drive for innovation in machining performance, focusing on enhancing surface finish quality and achieving significant tool life extension.

- A key boardroom consideration is the investment in a comprehensive coolant management program, which addresses both cost and sustainability. Adopting a modern fluid recycling system can reduce fluid-related downtime by over 30%. This shift is propelled by the need for better tramp oil rejection and bacterial growth control to extend sump life.

- Formulations are evolving with advanced corrosion inhibitor additive packages and more effective biocide formulation, balancing high performance with environmental responsibility. The emphasis is on delivering value through solutions like specialized aluminum machining fluid and high-speed machining coolant that optimize the entire production process, ensuring both quality and cost-effectiveness.

What are the Key Data Covered in this Metalworking Fluids Market Research and Growth Report?

-

What is the expected growth of the Metalworking Fluids Market between 2026 and 2030?

-

USD 2.23 billion, at a CAGR of 3.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Construction, Automobile, Aerospace, Electrical and power, and Others), Product (Mineral, Synthetic, and Bio-based), Application (Water-soluble fluids, Neat cutting oils, and Corrosion preventives) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing industrialization in emerging economies, Adverse environmental impact of metalworking fluids

-

-

Who are the major players in the Metalworking Fluids Market?

-

Blaser Swisslube, BP Plc, Chevron Corp., China Petrochemical Corp., CONDAT, ENEOS Corp., Exxon Mobil Corp., FUCHS SE, Henkel AG and Co. KGaA, Idemitsu Kosan Co. Ltd., Italmatch Chemicals Spa, Master Fluid Solutions, Motul group, PETROFER, PJSC LUKOIL, Quaker Houghton, TotalEnergies SE and YUSHIRO Inc.

-

Market Research Insights

- The metalworking fluids market is shaped by a dynamic interplay between performance demands and regulatory pressures. The push for worker safety improvements and VOC-compliant formulation is accelerating the adoption of ester-based synthetic and other advanced fluids.

- Manufacturers using a central system coolant are achieving significant fluid disposal cost reduction, with some reporting savings of over 30% through enhanced filtration media compatibility. Simultaneously, the demand for multi-metal compatibility drives innovation, as a single fluid that prevents staining on aluminum while protecting ferrous metals can streamline operations.

- This has led to formulations demonstrating a 25% longer sump life, reducing both consumption and maintenance needs, showcasing how technical advancements directly translate to measurable operational and financial benefits for end-users.

We can help! Our analysts can customize this metalworking fluids market research report to meet your requirements.