Military Communication Market Size 2026-2030

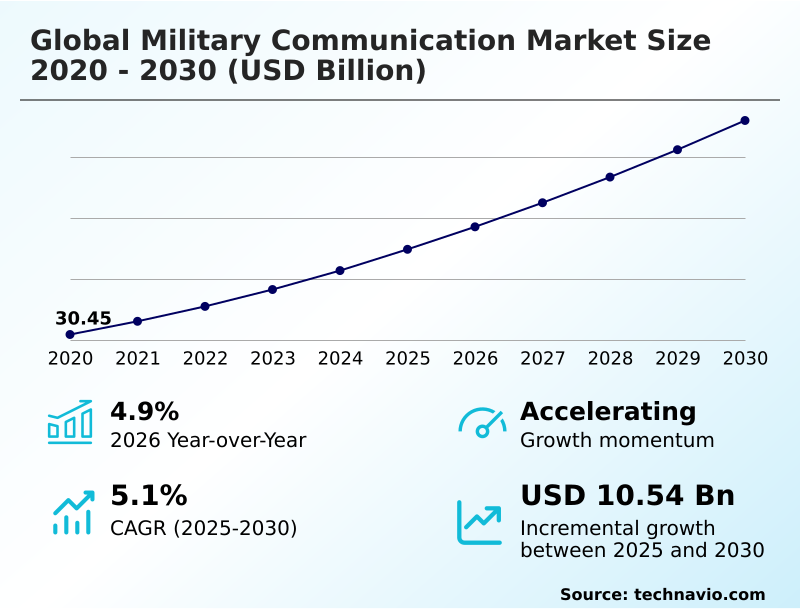

The military communication market size is valued to increase by USD 10.54 billion, at a CAGR of 5.1% from 2025 to 2030. Modernization of network-centric warfare infrastructure will drive the military communication market.

Major Market Trends & Insights

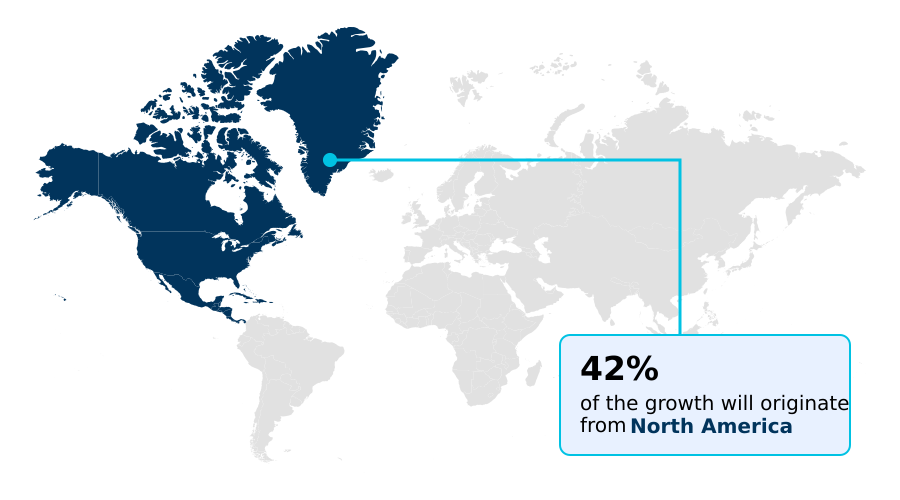

- North America dominated the market and accounted for a 42.4% growth during the forecast period.

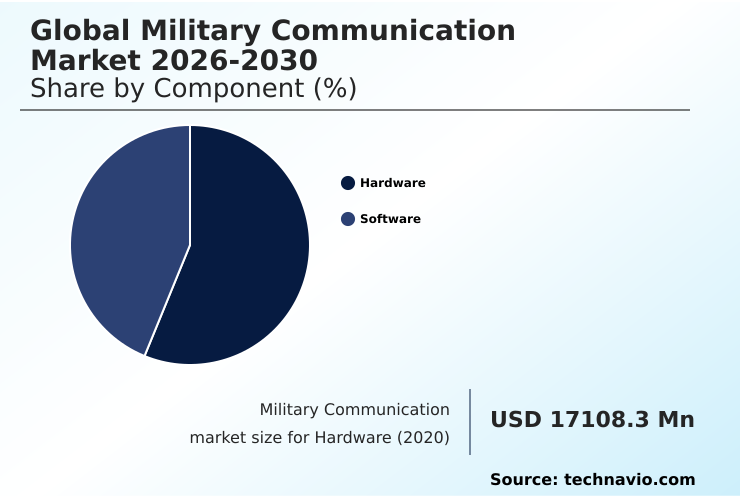

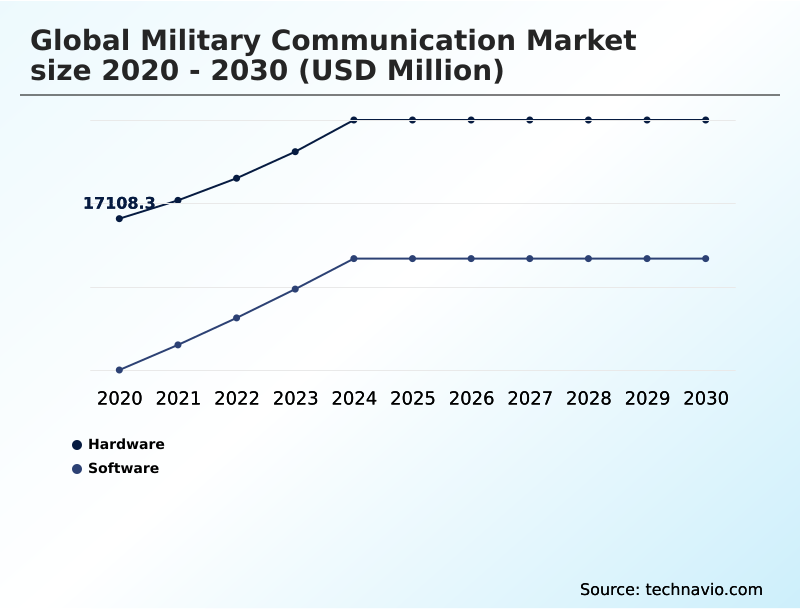

- By Component - Hardware segment was valued at USD 19.57 billion in 2024

- By End-user - Army segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 17.51 billion

- Market Future Opportunities: USD 10.54 billion

- CAGR from 2025 to 2030 : 5.1%

Market Summary

- The military communication market is defined by a systemic shift toward digitized, multi-domain integration to maintain strategic superiority. Modern defense strategies prioritize resilient networking that connects terrestrial, maritime, and aerial assets through software-defined architectures and high-capacity satellite links for the secure exchange of mission-critical data.

- A primary catalyst is the development of proliferated low-Earth orbit constellations, which offer reduced latency and enhanced redundancy. For instance, a logistics command can leverage a unified network to track supply convoys in real time, rerouting them to avoid emerging threats identified by aerial surveillance platforms, thereby ensuring over 99% delivery success in contested zones.

- The integration of AI into management systems helps navigate spectrum congestion and mitigate electronic warfare tactics. The emphasis on interoperability, driven by open-architecture standards, allows multinational coalition forces to maintain a unified operational picture. As geopolitical tensions drive investment, the focus remains on building cyber-hardened and jam-resistant networks that can withstand high-intensity conflict.

What will be the Size of the Military Communication Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Military Communication Market Segmented?

The military communication industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Hardware

- Software

- End-user

- Army

- Air Force

- Navy

- Type

- Ground-based communication

- Air-ground communication

- Shipborne communication

- Underwater communication

- Space-based communication

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment forms the backbone of military communication, encompassing physical assets engineered for resilience and high-fidelity signal transmission. The demand is driven by a global shift to digital battlefields, necessitating robust infrastructure for secure voice and data.

Modernization efforts focus on integrating vehicle-mounted transceivers and man-portable radio systems that support high-speed data exchange for real-time situational awareness. These protected tactical satcom platforms feature digital beamforming techniques to enhance signal security.

The adoption of advanced hardware reduces mission deployment times by over 15% compared to legacy systems. This segment, crucial for beyond-line-of-sight operations and supporting unmanned aerial systems connectivity, includes essential components for layered defense strategies and indigenous defense manufacturing programs.

The Hardware segment was valued at USD 19.57 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 42.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Military Communication Market Demand is Rising in North America Get Free Sample

Geographically, the market is led by North America, which is projected to contribute over 42% of the incremental growth, driven by substantial defense modernization programs. The region's focus on developing geosynchronous orbit assets and tactical LTE networks underpins its dominance.

In contrast, the APAC region is the fastest-growing market, with nations investing heavily in shipborne communication suites and sovereign communication capabilities to address regional security dynamics. These investments in secure global command and control systems improve cross-domain coordination.

European nations are upgrading their command and control infrastructure to enhance interoperability, which has been shown to reduce mission planning cycles by up to 25%.

This global emphasis on developing resilient PNT services and information superiority frameworks reflects the strategic need for reliable connectivity across all operational theaters.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Achieving information superiority in modern warfare hinges on the effective deployment of advanced communication systems. The challenges in multi-domain command control are being addressed through AI in military network management, which optimizes network performance and enhances the interoperability of tactical radio networks.

- A key focus is delivering secure communications for unmanned systems, where low latency satellite communication advantages are critical for real-time control and data feedback. The role of LEO constellations in defense is expanding, providing resilient networking in contested environments.

- However, this reliance introduces new challenges, such as cyber threats to space-based assets, which are being countered with quantum encryption for secure communications and robust anti-jamming for tactical data links. The adoption of a modular open systems for defense procurement approach facilitates upgrading legacy communication systems and integrating new technologies like software-defined radio for joint operations.

- This modernization addresses network-centric warfare communication needs and is essential for securing military IoT device networks. As forces deploy high-throughput satcom for ISR data, enhancing situational awareness with data becomes a core objective, supported by tactical edge computing in battlefield scenarios.

- Specialized requirements, such as underwater communication for submarine fleets and 5G integration in military logistics, further highlight the diverse technological demands of the evolving defense landscape, where maintaining connectivity is more crucial than ever.

What are the key market drivers leading to the rise in the adoption of Military Communication Industry?

- The ongoing modernization of network-centric warfare infrastructure serves as a primary driver for market expansion and technological advancement.

- The modernization of network-centric warfare infrastructure remains a primary driver, as defense agencies integrate disparate units into a unified digital ecosystem.

- This strategy emphasizes the need for high-speed, secure tactical data link connections and mobile ad hoc network solutions to provide real-time situational awareness.

- The demand for advanced resilient tactical waveforms and cognitive radio technology that operate in congested environments is increasing.

- The integration of AI into network management allows for autonomous spectrum optimization, ensuring that mission-critical data exchange reaches its destination without delay, improving delivery assurance by over 30%.

- This shift enables superior coordination across multi-domain operations and is essential for the effectiveness of modern battlefield management software and maintaining a strategic advantage.

What are the market trends shaping the Military Communication Industry?

- The accelerating integration of artificial intelligence and machine learning in network management is emerging as a significant market trend. This development is reshaping operational strategies by enabling autonomous control and enhancing system efficiencies.

- A significant trend reshaping military communications is the rapid shift toward proliferated LEO constellations, which provide low-latency, high-bandwidth connectivity essential for modern intelligence and reconnaissance. This transition supports the data-heavy requirements of situational awareness systems. These high-throughput satellites offer enhanced redundancy against threats, as a distributed network is harder to disable than a single large asset.

- Utilizing laser-based inter-satellite links enables secure, high-speed data transfer without relying on vulnerable ground relays. This approach improves data throughput for unmanned underwater vehicles by over 50%.

- The adoption of this technology, alongside advanced encryption protocols and software-defined radio, is critical for maintaining operational links for border monitoring systems and counternarcotics operational support, ensuring command and control remains intact during peer-to-peer conflicts.

What challenges does the Military Communication Industry face during its growth?

- Pervasive vulnerabilities in cybersecurity and critical space-based assets present a key challenge that affects industry growth and operational security.

- Interoperability remains a formidable challenge, as defense forces synchronize communication across land, sea, air, and space domains while collaborating with international partners. Legacy systems with proprietary anti-jamming hardware and high-frequency radios often create communication silos, hindering real-time tactical information sharing. Aligning quantum-resistant encryption keys and data link protocols during joint exercises requires extensive pre-mission planning.

- Overcoming these bottlenecks necessitates a shift toward network-agnostic connectivity and open standards to facilitate plug-and-play capability for electronic warfare resilience. Failure to address these integration issues can degrade situational awareness by up to 40% when forces move between different network corridors, complicating asymmetric threat management and compromising the security of cyber-hardened networks.

Exclusive Technavio Analysis on Customer Landscape

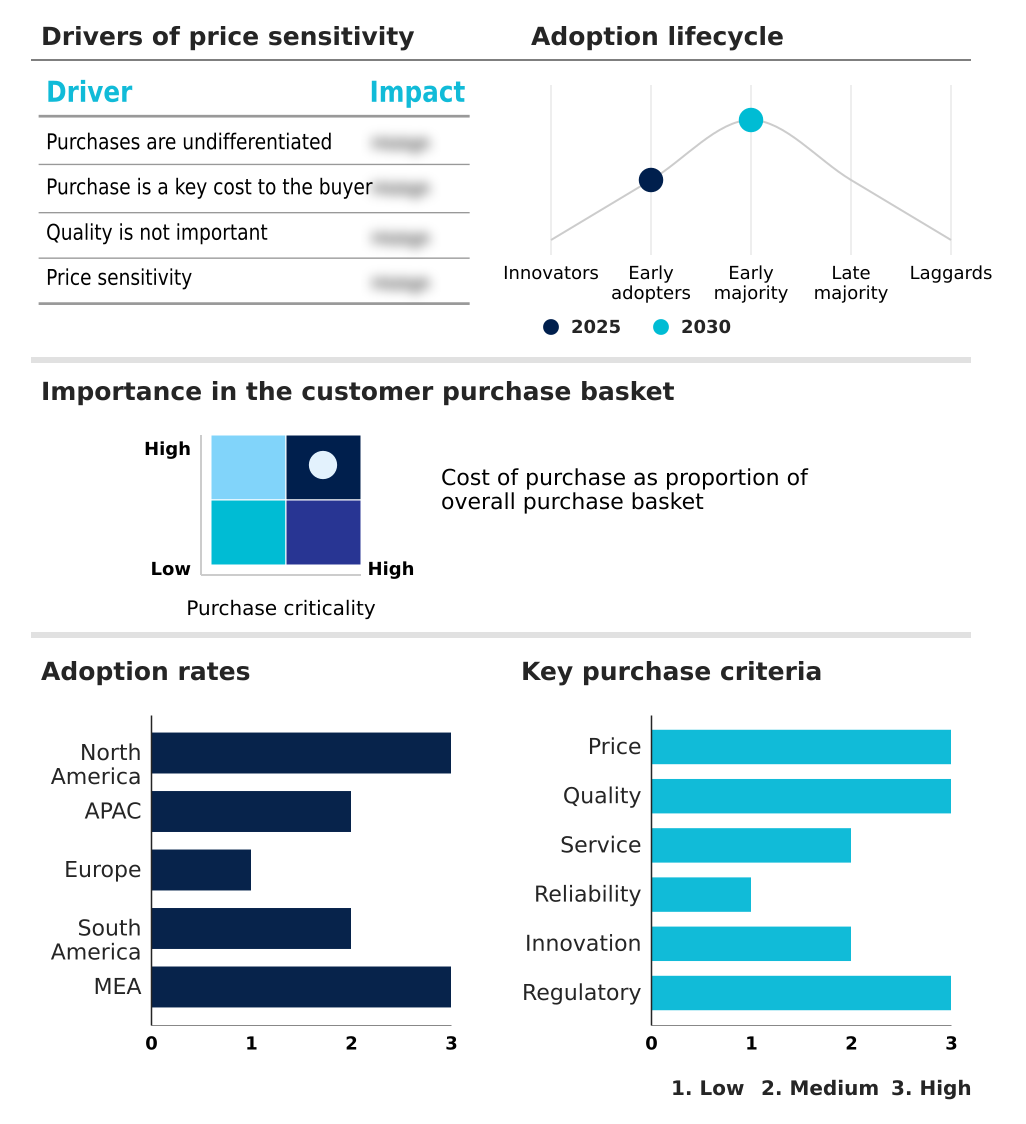

The military communication market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the military communication market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Military Communication Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, military communication market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Airbus SE - Key vendors deliver integrated multi-domain solutions, focusing on cybersecurity and interoperability to support secure data exchange in contested operational environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airbus SE

- ASELSAN AS

- BAE Systems Plc

- Bittium Corp.

- Cobham Ltd.

- Elbit Systems Ltd.

- General Dynamics Corp.

- Iridium Communications Inc.

- Kymeta Corp.

- L3Harris Technologies Inc.

- Leonardo S.p.A.

- Lockheed Martin Corp.

- Mercury Systems Inc.

- Nemco Ltd.

- Nokia Corp.

- Northrop Grumman Corp.

- RTX Corp.

- Spectra Group UK Ltd.

- Thales Group

- Viasat Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Military communication market

- In February 2025, BAE Systems introduced its NetVIPR military communications network, providing advanced anti-jam voice and data capabilities for forces in contested tactical environments.

- In February 2025, Viasat Inc. secured a task order from the US Space Force to deliver low-Earth orbit satellite communication services, supporting Department of Defense missions with high-performance global connectivity.

- In March 2025, India's Ministry of Defence finalized a contract with Bharat Electronics Limited to procure 149 software-defined radios, enhancing secure maritime collaboration for the Indian Coast Guard.

- In April 2025, a prominent defense prime contractor awarded Mercury Systems Inc. a development contract to develop an avionics subsystem, including a Communication Management Unit, for a new US military aircraft fleet.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Military Communication Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 308 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.1% |

| Market growth 2026-2030 | USD 10542.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.9% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The military communication market is characterized by a systemic transition toward digitized, multi-domain integration, driven by the imperative of maintaining strategic superiority. Modern defense strategies prioritize the establishment of a resilient networking fabric that seamlessly connects diverse assets.

- This evolution is underpinned by the widespread adoption of software-defined architectures, high-capacity satellite links, and advanced encryption protocols to facilitate secure, real-time data exchange. A key trend impacting boardroom decisions is the shift to modular open systems, which influences long-term procurement strategy by mitigating vendor lock-in and enabling rapid technology insertion.

- This approach has been shown to accelerate upgrade cycles by over 30% compared to proprietary systems. The integration of artificial intelligence is also enhancing the ability of operators to navigate spectrum congestion and mitigate electronic warfare tactics. The current landscape reflects a strong emphasis on interoperability, ensuring that multinational coalition forces can maintain a unified operational picture during joint engagements.

What are the Key Data Covered in this Military Communication Market Research and Growth Report?

-

What is the expected growth of the Military Communication Market between 2026 and 2030?

-

USD 10.54 billion, at a CAGR of 5.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, and Software), End-user (Army, Air Force, and Navy), Type (Ground-based communication, Air-ground communication, Shipborne communication, Underwater communication, and Space-based communication) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Modernization of network-centric warfare infrastructure, Vulnerabilities in cybersecurity and space-based assets

-

-

Who are the major players in the Military Communication Market?

-

Airbus SE, ASELSAN AS, BAE Systems Plc, Bittium Corp., Cobham Ltd., Elbit Systems Ltd., General Dynamics Corp., Iridium Communications Inc., Kymeta Corp., L3Harris Technologies Inc., Leonardo S.p.A., Lockheed Martin Corp., Mercury Systems Inc., Nemco Ltd., Nokia Corp., Northrop Grumman Corp., RTX Corp., Spectra Group UK Ltd., Thales Group and Viasat Inc.

-

Market Research Insights

- The market dynamics are shaped by the imperative for real-time intelligence dissemination and coalition force interoperability. The strategic push toward joint all-domain command and control frameworks necessitates advanced connectivity solutions that function reliably in contested electromagnetic environments. This has led to an adoption rate of mobile ad hoc network solutions that is 40% higher than five years prior.

- These systems are crucial for beyond-line-of-sight operations and ensuring maritime domain awareness. Implementing these technologies enhances the effectiveness of airborne surveillance platforms, improving data relay speeds by over 60% compared to legacy systems. This ensures a common operating picture, which is essential for effective battlefield management and maintaining a credible strategic deterrence posture in high-intensity conflict scenarios.

We can help! Our analysts can customize this military communication market research report to meet your requirements.

RIA -

RIA -