North America Bagged Industrial Salt Market Size 2025-2029

The North America bagged industrial salt market size is forecast to increase by USD 78.3 million at a CAGR of 1.2% between 2024 and 2029.

- The market is experiencing significant growth due to several key factors. Severe winter weather conditions continue to drive demand for salt as de-icing agent in various industries, particularly transportation and construction. Additionally, the increasing focus on water treatment and wastewater management is leading to increased usage of bagged industrial salt in this application. Furthermore, accidents at salt mines and supply chain disruptions have highlighted the importance of having a reliable and consistent supply of salt, further boosting market growth. These trends are expected to continue shaping the market dynamics in the coming years.

What will be the Size of the Market During the Forecast Period?

- The market is a significant sector within the broader industrial salt industry. This market caters to various industries, including pharmaceuticals, food processing, agriculture, and cleaning, among others. The demand for bagged industrial salt is driven by its diverse applications, which range from disinfection and sanitation to food additives and livestock supplements. The industrial automation sector plays a crucial role in the production and distribution of bagged industrial salt. Process engineering and quality control are essential elements of this process, ensuring the consistent delivery of high-quality salt products. The integration of advanced technologies, such as material science and nanotechnology, enhances the efficiency and sustainability of salt production methods. The hygiene industry is another major consumer of bagged industrial salt. The demand for salt in this sector is driven by its role in disinfection and sanitation processes. Salt's ability to absorb moisture and lower the freezing point of water makes it an essential component in various cleaning products. The pharmaceutical industry relies on bagged industrial salt as a critical raw material for producing various medications. Salt is used as a preservative, a bulking agent, and a flavoring agent in pharmaceutical formulations.

- The production of salt for pharmaceutical applications requires stringent regulatory compliance and adherence to safety regulations. The agricultural sector utilizes bagged industrial salt for various purposes, including animal feed and agricultural chemicals. Salt is used as a livestock supplement to maintain animal health and productivity. In the agricultural sector, salt is also used as a raw material for producing various chemicals, such as fertilizers and pesticides. The food industry uses bagged industrial salt for food additives, food preservation, and de-icing applications. Salt's role in food additives includes its use as a flavor enhancer and a preservative. In food preservation, salt is used to prevent bacterial growth and enhance the shelf life of various food products. The market research reports indicate a growing trend towards sustainable practices in the bagged industrial salt industry. Companies are focusing on reducing their carbon footprint by adopting evaporative salt production methods and solar salt production. These methods reduce the energy consumption and water usage associated with traditional salt mining and brine extraction methods.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

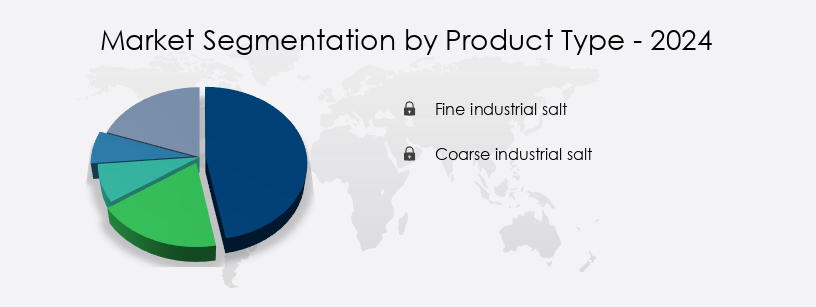

- Product Type

- Fine industrial salt

- Coarse industrial salt

- Application

- Chemical industry

- De-icing

- Food processing industry

- Agriculture

- Others

- Geography

- North America

- Canada

- Mexico

- US

- North America

By Product Type Insights

- The fine industrial salt segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant growth due to its increasing utilization in various industries and advanced manufacturing processes. This segment's expansion is fueled by the demand for finer salt grades, which offer distinct advantages in different industrial applications. In the realm of chemical processing, the necessity for fine industrial salt is particularly prominent. Its precise particle size distribution is essential for ensuring optimal reaction efficiency and superior product quality. The fine granules of this salt create a consistent and controlled environment for chemical reactions, resulting in enhanced yields and superior end products. Moreover, the fine industrial salt market is influenced by the mining techniques used, including vacuum pan technology and solution mining.

Further, logistical services play a crucial role in ensuring the timely delivery of this essential commodity to various end-users, including energy generation, hospitals, and water treatment facilities. The demand for clean drinking water and the growing adoption of solar evaporation for water treatment are also driving the market's growth. The fine industrial salt is a vital component in the production of chlorine, which is used extensively in water treatment processes. Furthermore, its application in energy generation, particularly in the form of brine, is gaining momentum due to the increasing focus on renewable energy sources.

Get a glance at the market report of share of various segments Request Free Sample

Market Dynamics

Our market researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of the market?

Severe winter weather is the key driver of the market.

- The market experiences significant growth due to the harsh winter conditions in the United States and Canada. Municipalities and state governments actively utilize high-grade salts, such as magnesium chloride, sodium chloride, and sodium fluorosilicate, for de-icing and snow removal during the winter months. These salts are essential for maintaining traffic safety and preventing accidents caused by icy roads and highways. In the chemical processing industry, industrial salt is used in various applications, including the production of chlorine, sulfates, and sodium hypochlorite for water treatment. Additionally, it is employed in the manufacturing processes of PVC, plastics, and pharmaceuticals. Sodium chlorate, a byproduct of the chlor-alkali process, is another industrial salt application.

Furthermore, industrial salt is used in various industries such as agriculture, food processing, and mining activities. In agriculture, it is used as a fertilizer and for livestock feed. In food processing, it is used as a preservative and in the production of laundry care products, cosmetics, and meat processing. In mining activities, it is used as a drilling fluid and in solution mining. Environmental compliance plays a crucial role in the industrial salt market. The chemical industry adheres to strict environmental regulations to minimize CO2 emissions and ensure clean drinking water. Vacuum pan technology and solar evaporation are used to produce high-purity salts, reducing the environmental impact of traditional mining practices.

What are the market trends shaping the market?

Growing water treatment needs is the upcoming trend in the market.

- The market is witnessing notable expansion due to the escalating demand for water treatment solutions. With urbanization and industrialization progressing at an unprecedented pace, there is a growing necessity for water softening processes that are essential for both residential water systems and large-scale municipal treatment plants. These processes eliminate minerals, such as calcium and magnesium, which contribute to water hardness. Strict regulations governing water quality and treatment in North America, particularly in the U.S. And Canada, necessitate continuous investments in enhancing water systems. Consequently, the demand for bagged industrial salt is fueled by these regulatory mandates, as it is an indispensable component in the regeneration of water softening systems.

- Moreover, the chemical processing industry also relies heavily on high-purity salts, including sodium chloride, magnesium chloride, and sodium fluorosilicate, for various applications. These salts are utilized in the production of chlorine, which is employed in water treatment, disinfection, and bleaching processes. In addition, they are integral to the manufacturing of PVC, a widely used plastic in various industries, including healthcare, food processing, and agriculture. The healthcare sector employs bagged industrial salt in the production of high-purity salts, such as sodium chloride, which is used as an essential electrolyte in intravenous formulas and as a critical component in the production of chlorides for various medical applications.

- Furthermore, the salt is also used in the pharmaceutical industry for the production of therapeutic drugs and in the manufacturing of soaps and detergents. The food processing industry utilizes industrial salt for various applications, including food preservation, seasoning, and as a raw material in the production of soda ash, which is employed in the manufacturing of glass, paper, and other industrial products. In the agricultural sector, salt is used as a fertilizer and in the production of animal feed. The solar energy industry also employs industrial salt in the production of solar evaporation ponds, which are used for energy generation.

What challenges does the market face during the growth?

Accidents at salt mines is a key challenge affecting the market growth.

- The market faces challenges due to accidents in salt mines, which impact both supply and financial stability. These incidents can result in temporary mine shutdowns or sections, causing significant disruptions during high-demand periods, such as winter months, for road de-icing salt. The financial consequences of these accidents are substantial, with mining companies incurring losses from recovery efforts and investigations. Furthermore, these interruptions can create market instability, leading to supply shortages and price increases. Magnesium, sodium fluorosilicate, and sulfates are essential chemicals used in the production of industrial salt. In the chemical processing industry, high-grade salts are produced using techniques like vacuum pan technology and solution mining.

- These salts find applications in various sectors, including laundry care products, water treatment, food processing, agriculture, and energy production. Magnesium chloride, a high-purity salt, is used in PVC production, while sodium chloride is essential for chlorine production in the chemical industry. Sodium chlorate is used in mining activities, while potassium chloride is used in meat processing and cosmetics. Calcium hypochlorite, chlorine dioxide, and sodium hypochlorite are used in water treatment, ensuring clean drinking water and maintaining water quality in waterways. In the healthcare sector, high-purity salts are used in pharmaceuticals and intravenous formulas. In food and beverage applications, salts like sodium chloride, sodium fluorosilicate, and sulfates are used as preservatives and additives.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast , partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Cargill Inc. - This company offers bagged industrial salt used in a wide range of industrial applications such as chemical manufacturing, textile processing, and metallurgical smelting.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Cargill Inc.

- Delmon Group

- Dominion Salt Ltd.

- Donald Brown Group

- INEOS Group Holdings S.A.

- KS Aktiengesellschaft

- Mitsui and Co. Ltd.

- Namco Pools

- Rio Tinto Ltd.

- Tata Chemicals Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is driven by several factors, which are discussed below. Magnesium and other essential minerals are vital components of bagged industrial salt. These minerals find extensive applications in the manufacturing processes of various industries. For instance, magnesium is used in the production of high-purity salts, which are essential in the chemical industry. Magnesium is also used in the production of chlorine, a critical disinfectant in water treatment and various other applications. Polyvinyl chloride (PVC) is another significant application area for bagged industrial salt. The vacuum pan technique is commonly used to produce high-grade chemicals, including PVC, which requires the use of bagged industrial salt. In the production of PVC, sodium fluorosilicate is used as a catalyst, which is derived from bagged industrial salt. Laundry care products and detergents are other major consumers of bagged industrial salt. Sodium chloride, a primary component of bagged industrial salt, is used in the production of laundry care products and detergents. Sodium chloride is also used in the production of chlorine, which is used as a bleaching agent in laundry care products.

Perishable products, such as meat, require preservation to maintain their quality during transportation and storage. Bagged industrial salt is used as a preservative in the transportation and storage of such products. Chlorides, a component of bagged industrial salt, are used as preservatives in the meat industry. The chemical processing industry is a significant consumer of bagged industrial salt. Sodium chlorate, a chlorate salt, is produced from bagged industrial salt and is used as a bleaching agent in the chemical industry. Sodium chlorate also finds applications in mining activities, such as in the production of chlorine dioxide, which is used for water treatment and bleaching. The healthcare industry is another major consumer of bagged industrial salt. Sodium chloride is used in the production of intravenous formulas and contact solutions. Sodium chloride is also used in the production of pharmaceuticals, such as capsules and tablets. The food processing industry uses bagged industrial salt extensively. It is used as a seasoning agent, a preservative, and a raw material in the production of various food items. Rock salt, a type of bagged industrial salt, is used in food processing due to its high purity and unique taste. The solar energy industry uses bagged industrial salt in the production of solar evaporation systems.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

164 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 1.2% |

|

Market Growth 2025-2029 |

USD 78.3 million |

|

Market structure |

Concentrated |

|

YoY growth 2024-2025(%) |

-0.1 |

|

Key countries |

US, Canada, and Mexico |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -