Optometry Equipment Market Size 2024-2028

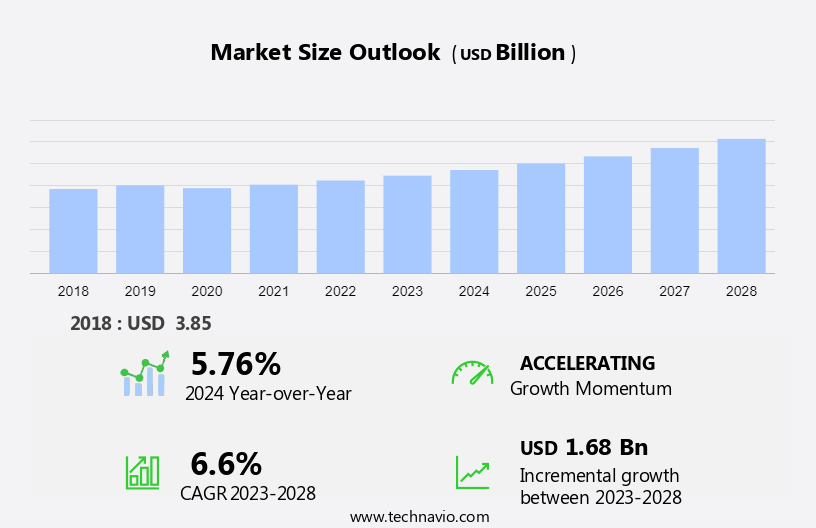

The optometry equipment market size is forecast to increase by USD 1.68 billion at a CAGR of 6.6% between 2023 and 2028.

- The market is experiencing significant growth due to several key factors. The increasing prevalence of ophthalmic diseases, such as cataracts, glaucoma, and diabetic retinopathy, is driving market demand. Furthermore, companies are focusing on expanding their presence in emerging markets to capitalize on untapped opportunities. However, the shortage of skilled ophthalmologists poses a challenge to market growth. To address this issue, there is a growing trend toward the use of advanced optometry equipment that can diagnose and treat various eye conditions with minimal intervention from medical professionals. This not only improves patient outcomes but also increases access to eye care services in regions with a shortage of ophthalmologists. Overall, the market is expected to witness strong growth in the coming years due to these factors and the continued innovation in eye care technology.

What will be the Size of the Optometry Equipment Market During the Forecast Period?

- The market is experiencing significant growth due to the increasing prevalence of eye illnesses and disorders among the aging population. With an estimated 285 million people worldwide living with vision loss, eye diseases such as cataracts, glaucoma, age-related macular degeneration, and open-angle glaucoma have become major public health issues. Diagnostic tests and ophthalmic diagnostic technologies play a crucial role in detecting and managing these conditions, enabling early intervention and prevention of further vision loss.

- Furthermore, the visual system, including the retina, cornea, and scotoma, are key areas of focus for optometrists and eye clinics. As healthcare expenses continue to rise, there is a growing demand for advanced and cost-effective solutions to address the needs of patients with various eye deformities and visual impairments. The market is expected to continue its growth trajectory, driven by technological advancements and increasing awareness of the importance of early detection and treatment of eye diseases.

How is this Optometry Equipment Industry segmented and which is the largest segment?

The optometry equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Clinics

- Hospitals

- Type

- Retina and glaucoma examination products

- General examination

- Cornea and cataract examination products

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- Asia

- China

- Rest of World (ROW)

- North America

By End-user Insights

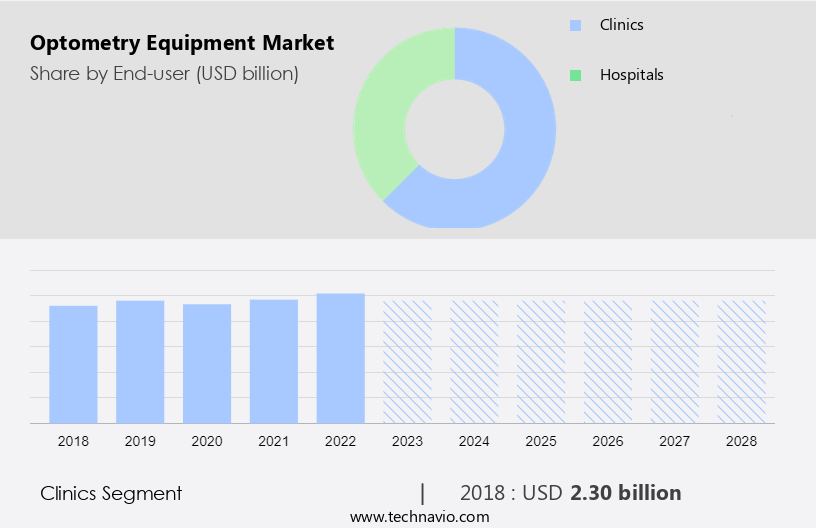

- The clinics segment is estimated to witness significant growth during the forecast period.

The market is primarily driven by the increasing prevalence of eye illnesses and disorders among the aging population, leading to vision loss. This public health issue necessitates regular eye examinations to diagnose and treat conditions such as cataracts, glaucoma, age-related macular degeneration, and diabetic retinopathy, which are common in this demographic. Eye clinics and hospitals are the major end-users of optometry equipment due to the high volume of diagnostic tests and ophthalmology procedures performed. Commonly used equipment includes autorefractors/retinoscopes, ophthalmoscopes, tonometry devices, operating microscopes, and phaco machines.

Additionally, these tools enable ophthalmologists to evaluate visual acuity, screen for ocular diseases, and provide necessary therapies and surgeries. Conditions like open-angle glaucoma, retina disorders, scotoma, and visual system deformities are frequently diagnosed and treated using advanced diagnostic technologies. Virtual care practices are also gaining popularity, offering remote consultations and examinations to enhance accessibility and reduce healthcare expenses.

Get a glance at the Optometry Equipment Industry report of share of various segments Request Free Sample

The clinics segment was valued at USD 2.30 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

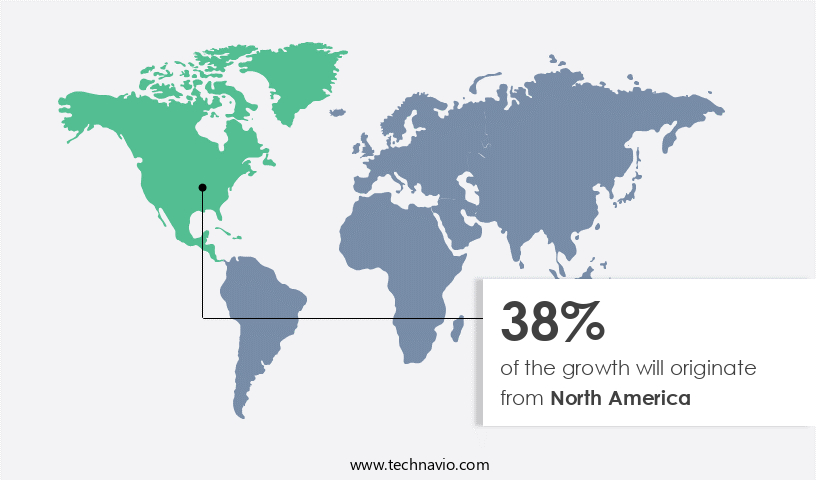

- North America is estimated to contribute 38% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market in North America is experiencing significant growth due to increasing healthcare expenditures on eye diseases, product approvals, and advanced technology adoption. The region's major contributors to market revenue are the US and Canada. The prevalence of eye diseases, including cataracts, glaucoma, diabetic retinopathy, and refractive disorders, is increasing due to the aging population and chronic conditions like diabetes. This, in turn, is driving the demand for optometry equipment.

Additionally, the number of ophthalmology surgeries and diagnostic tests, such as those for open-angle glaucoma, scotoma, and visual system deformities, is rising. Eye clinics and hospitals are investing in ophthalmic diagnostic technologies for cataract surgery, general exams, and therapies. Virtual care practices are also gaining popularity for diagnosing and managing eye diseases. Overall, the market in North America is poised for continued growth due to the aging population, increasing prevalence of eye illnesses, and advancements in ophthalmology procedures.

Market Dynamics

Our optometry equipment market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Optometry Equipment Industry?

Increasing prevalence of ophthalmic diseases is the key driver of the market.

- The market In the US is witnessing significant growth due to the increasing prevalence of eye illnesses and disorders among the elderly population. According to the World Health Organization, approximately 2.2 billion people worldwide had a near or distant vision impairment as of August 2023. Major causes of vision loss include uncorrected refractive errors, cataracts, and eye diseases such as glaucoma, age-related macular degeneration, and diabetic retinopathy. Diabetes and its complications, including hypertension, are major risk factors for eye health issues. Diabetes can lead to conditions such as diabetic retinopathy, diabetic macular edema, and retinal vein occlusion, which can cause blindness. Glaucoma, another leading cause of blindness, is a group of eye diseases that damage the optic nerve and can lead to vision loss. The aging population is particularly vulnerable to eye diseases, as the prevalence of ocular illnesses increases with age.

- Additionally, regular eye examinations are crucial for early detection and treatment of eye diseases. Eye clinics and hospitals offer diagnostic tests and ophthalmology procedures, including cataract surgery, to diagnose and treat various eye conditions. Virtual care practices are also gaining popularity, providing patients with convenient access to eye health services. Ophthalmic diagnostic technologies, such as optical coherence tomography and fundus photography, enable early detection and diagnosis of eye diseases, reducing healthcare expenses In the long run. In summary, the market In the US is driven by the increasing prevalence of eye diseases and disorders, particularly among the elderly population. Diabetes, hypertension, and aging are major risk factors for eye health issues, making regular eye examinations essential for early detection and treatment. Virtual care practices and advanced diagnostic technologies are also contributing to the growth of the market.

What are the market trends shaping the Optometry Equipment Industry?

The rising focus of the market players to strengthen their presence in emerging markets is the upcoming market trend.

- The aging population In the US and the increasing prevalence of eye illnesses and disorders among elderly individuals have made eye health a significant public health issue. According to the National Eye Institute, common age-related eye conditions include cataracts, glaucoma, and age-related macular degeneration, which can lead to vision loss and even blindness if left untreated. Regular eye examinations are crucial for early detection and prevention of these ocular diseases. Ophthalmologists and eye clinics play a vital role in diagnosing and treating various eye conditions. Diagnostic tests, such as visual acuity tests, tonometry, and retinal imaging, are essential in identifying eye diseases like open-angle glaucoma, diabetic retinopathy, and scotoma.

- Moreover, therapies and ophthalmology procedures, including cataract surgery and glaucoma treatments, are crucial for managing these conditions. The increasing prevalence of chronic conditions like diabetes and hypertension, which are risk factors for eye diseases, further highlights the importance of eye health. Healthcare expenses related to eye diseases are significant, making it essential to invest in ophthalmic diagnostic technologies and treatments. Virtual care practices are gaining popularity, offering convenience and accessibility to patients, particularly in rural areas or for those with mobility issues. The market for optometry or eye exam equipment is expected to grow as the demand for advanced diagnostic technologies and treatments increases.

- In summary, the aging population, increasing prevalence of eye diseases, and growing healthcare expenditure are driving the demand for optometry or eye exam equipment In the US. The market for these technologies is poised for growth, with opportunities in both advanced diagnostic tools and treatments for various ocular diseases.

What challenges does the Optometry Equipment Industry face during its growth?

A shortage of skilled ophthalmologists is a key challenge affecting the industry's growth.

- The market plays a crucial role In the early diagnosis and treatment of various eye diseases, including eye illnesses and disorders that lead to vision loss. As the elderly population continues to grow, the prevalence of age-related conditions such as cataracts, glaucoma, and age-related macular degeneration increases, making eye health a significant public health issue. Ophthalmologists rely on diagnostic tests and ophthalmic diagnostic technologies to identify and manage these conditions, which can result in serious consequences if misdiagnosed or treated improperly. However, the clinical practice of ophthalmology is facing challenges due to insufficient human resources and lack of funding from governments.

- The shortage of ophthalmologists is exacerbated by the increasing demand for eye care services, particularly among the baby boomer generation, and the long duration of training required to become an ophthalmologist. Furthermore, the aging of current ophthalmologists and the inadequate number of ophthalmology graduates add to the shortage. Virtual care practices and telemedicine are emerging as potential solutions to address the shortage of ophthalmologists. These technologies enable remote consultations, diagnoses, and therapies, making eye care more accessible to patients, especially those in rural areas or with mobility issues. However, the implementation of these technologies requires significant investment and expertise.

- Thus, the high patient demand, increasing prevalence of ophthalmology diseases, and the shortage of ophthalmologists drive up healthcare expenses. Regular eye exams and ophthalmology procedures, such as cataract surgery, are essential for maintaining eye health and preventing vision impairment. The market for optometry equipment is expected to grow as the need for advanced diagnostic and therapeutic tools increases to meet the demands of an aging population and the growing prevalence of ocular diseases.

Exclusive Customer Landscape

The optometry equipment market forecasting report includes the adoption lifecycle of the market, market growth and forecasting, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the optometry equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, optometry equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry. The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alcon Inc.

- Appasamy Associates Pvt. Ltd.

- Bausch Lomb Corp.

- Canon Inc.

- Carl Zeiss AG

- Devine Meditech

- Essilor Instruments

- HAAG-STREIT DEUTSCHLAND GmbH

- Halma Plc

- Heidelberg Engineering GmbH

- HEINE Optotechnik GmbH and Co. KG

- Johnson and Johnson Services Inc.

- NIDEK Co. Ltd.

- OCULUS Optikgerate GmbH

- Reichert Inc.

- Revenio Group Corp.

- Topcon America Corp.

- Unitech Vision

- Zimmer Biomet Holdings Inc.

- Visionix

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a range of diagnostic and therapeutic tools utilized by eye care professionals to assess, diagnose, and treat various eye conditions. This market caters to the growing demand for effective and efficient eye care solutions, driven by an increasing elderly population and the prevalence of eye illnesses and disorders. Eye health is a significant public health issue, with age-related macular degeneration, cataracts, glaucoma, and diabetic retinopathy being among the most common eye diseases. These conditions can lead to vision loss and impairment, necessitating regular eye examinations and specialized treatments. Ophthalmic diagnostic technologies play a crucial role In the early detection and management of these conditions. These technologies include various imaging modalities, such as optical coherence tomography (OCT), fundus photography, and retinal scanning. These tools enable eye care professionals to visualize the internal structures of the eye, identify abnormalities, and monitor disease progression.

Moreover, the advent of virtual care practices and telemedicine has expanded the accessibility of eye care services, particularly for individuals in remote areas or those with mobility issues. Further, these technologies enable remote consultations, virtual examinations, and remote monitoring, reducing the need for in-person visits to eye clinics or hospitals. The aging population, with its increased susceptibility to eye diseases, is a significant driver of demand for optometry equipment. Additionally, the rising prevalence of chronic conditions such as diabetes and hypertension, which are associated with eye health complications, further fuels market growth. The market for optometry equipment is highly competitive, with numerous players offering a range of products and services. Ophthalmic diagnostic technologies, cataract surgery equipment, and general exam equipment are among the most in-demand product categories. Therapies and therapies for various eye conditions, such as glaucoma and age-related macular degeneration, are also significant market segments. Healthcare expenses, particularly those related to eye care, continue to rise, making cost-effective and efficient solutions a priority for both providers and patients.

As a result, there is a growing focus on developing advanced, user-friendly, and cost-effective optometry equipment to meet the evolving needs of the market. In summary, the market is a dynamic and growing industry, driven by an aging population, the prevalence of eye diseases, and the increasing demand for cost-effective and efficient eye care solutions. The market offers a range of diagnostic and therapeutic tools, from advanced imaging modalities to virtual care practices, catering to the diverse needs of eye care professionals and patients.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

151 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.6% |

|

Market growth 2024-2028 |

USD 1.68 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.76 |

|

Key countries |

US, Canada, UK, Germany, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Optometry Equipment Market Research and Growth Report?

- CAGR of the Optometry Equipment industry during the forecast period

- Detailed information on factors that will drive the Optometry Equipment growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the optometry equipment market growth of industry companies

We can help! Our analysts can customize this optometry equipment market research report to meet your requirements.

RIA -

RIA -