Pet Food Market Size 2026-2030

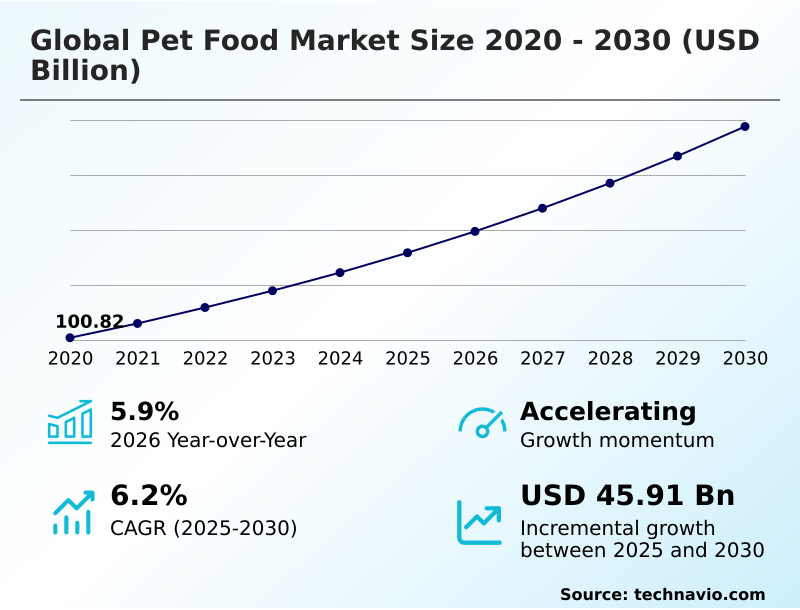

The pet food market size is valued to increase by USD 45.91 billion, at a CAGR of 6.2% from 2025 to 2030. Growing demand for organic pet food will drive the pet food market.

Major Market Trends & Insights

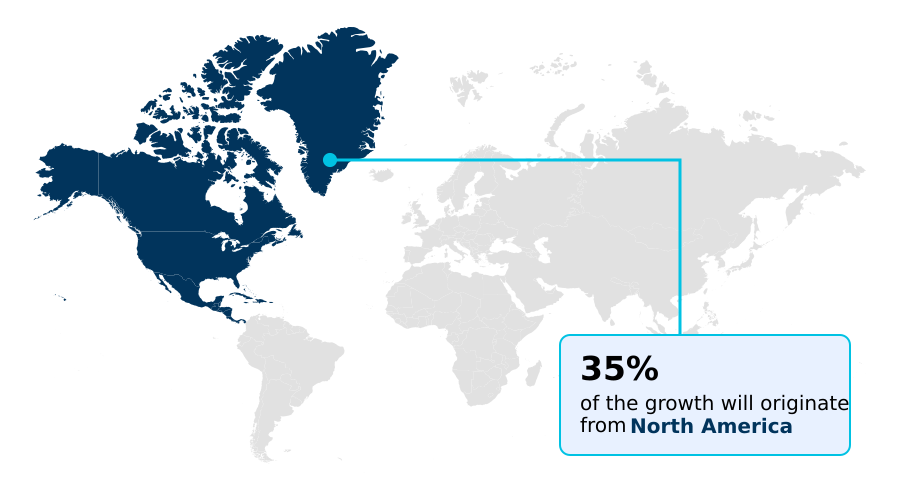

- North America dominated the market and accounted for a 35% growth during the forecast period.

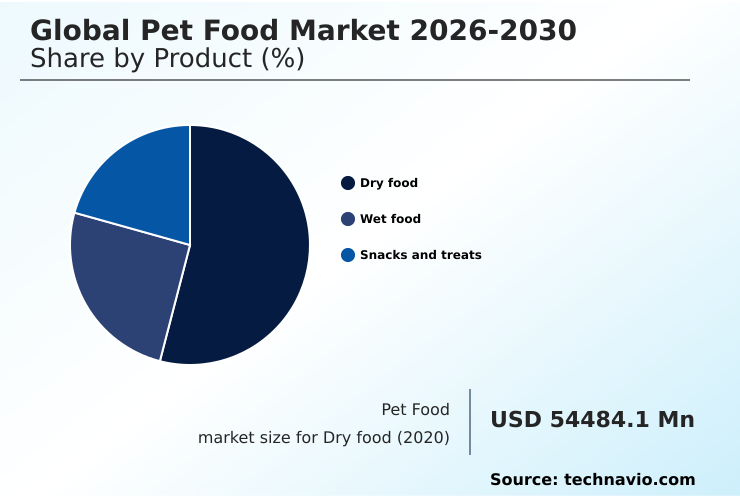

- By Product - Dry food segment was valued at USD 67.70 billion in 2024

- By Type - Dog food segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 76.82 billion

- Market Future Opportunities: USD 45.91 billion

- CAGR from 2025 to 2030 : 6.2%

Market Summary

- The pet food market is undergoing a significant transformation, driven by the deep-seated humanization trend where pets are considered integral family members. This cultural shift is fueling demand for premium nutrition, pushing the industry beyond basic sustenance toward products that offer targeted health benefits.

- As a result, the pet care landscape is increasingly focused on functional pet nutrition, with owners seeking clean label ingredients and formulations that support everything from digestive health to cognitive function. In response, manufacturers are innovating with advanced processing methods like freeze-drying to preserve nutrient integrity.

- However, this push for premiumization is met with challenges, including the need for sustainable ingredient sourcing and managing supply chain disruptions. For instance, a mid-sized company aiming to launch a new organic line must navigate volatile raw material costs and complex global logistics, all while ensuring its packaging is recyclable to meet consumer expectations.

- The evolution of the pet food market requires a delicate balance between scientific innovation, ethical production, and accessible pricing to meet the sophisticated demands of modern pet owners.

What will be the Size of the Pet Food Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Pet Food Market Segmented?

The pet food industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

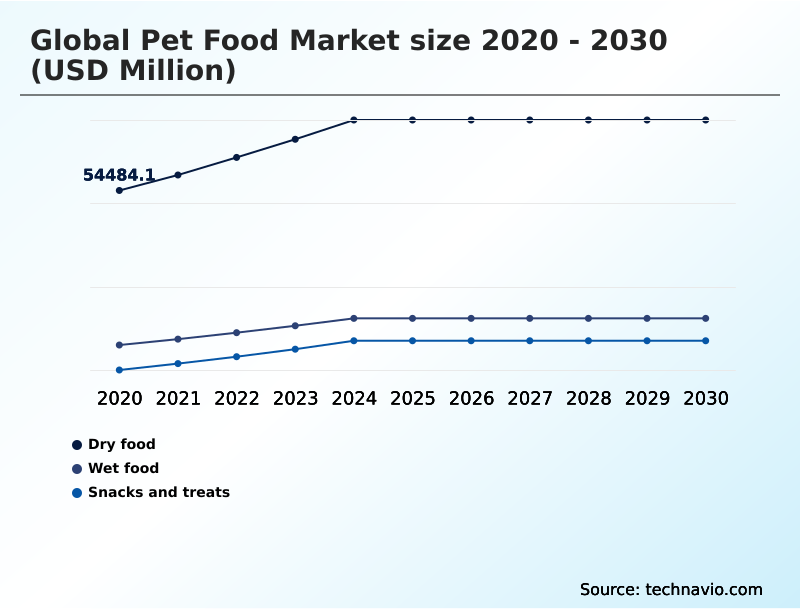

- Product

- Dry food

- Wet food

- Snacks and treats

- Type

- Dog food

- Cat food

- Others

- Distribution channel

- Supermarkets and hypermarkets

- Specialty stores

- Online

- Convenience stores

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- South Africa

- Saudi Arabia

- Rest of World (ROW)

- North America

By Product Insights

The dry food segment is estimated to witness significant growth during the forecast period.

The dry food segment remains the largest category, accounting for over 60% of market share due to its convenience and cost-effectiveness.

The market is evolving beyond basic nutrition, with a strong push toward clean label formulation and the integration of functional additives like omega-3 fatty acids and glucosamine for joint support.

Innovations in food extrusion technology allow for the creation of products that meet demands for pet food palatability while supporting therapeutic diets. As consumers seek eco-friendly pet products, manufacturers are also exploring sustainable practices even in this high-volume segment.

This includes developing veterinary nutritional formulas and hypoallergenic formulations in dry formats, shifting from niche small-batch production models to mass-market availability for specialized health needs, reflecting high animal welfare standards.

The Dry food segment was valued at USD 67.70 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Pet Food Market Demand is Rising in North America Get Free Sample

North America continues to dominate the global landscape, accounting for approximately 35% of the market opportunity, driven by high adoption of premium and specialized diets.

However, the APAC region is the fastest-growing, representing nearly 18% of the opportunity, with demand for plant-based protein sources and products with organic pet food certification surging.

Innovations in pet food manufacturing innovation, such as smart packaging integration and advanced sterilization techniques, are critical for meeting diverse regional pet food safety standards.

The rise of subscription pet food services is accelerating the adoption of limited ingredient diets and insect-based protein globally. This focus on holistic pet wellness and the use of upcycled food ingredients is reshaping supply chains across all major regions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic landscape of the pet food market is shaped by a confluence of economic pressures and technological advancements. The impact of tariffs on pet food ingredients is a primary concern, forcing companies to explore regional sourcing and cost-saving measures.

- In response, advancements in smart pet food manufacturing are becoming critical, with automated systems improving supply chain efficiency by over 15% in some facilities. This allows for better management of both costs and quality control, which is essential for addressing and preventing pet food product recalls. Consumer trends are also a powerful force.

- The demand for healthier options is driving research into the benefits of probiotics in dog food and the rise of human-grade ingredients in cat food. Concurrently, the consumer trends in fresh pet food are pushing the industry toward complex supply chain logistics for refrigerated pet food.

- Sustainability is another key pillar, influencing everything from the development of recyclable packaging for wet pet food to the exploration of sustainable alternatives to animal protein. Companies must also navigate regulatory standards for pet food labeling to communicate the benefits of grain-free dog food diets and address the challenges in sourcing organic pet food.

- This dynamic environment has opened doors for the growth of pet food subscription services and the rise of private label pet food, both of which use targeted marketing strategies for premium pet food to capture market share. The ongoing comparison of dry vs wet pet food continues, while the pet food market dynamics in APAC present significant growth opportunities.

- Finally, understanding the nutritional requirements for senior pets and creating innovations in dental care pet treats are key areas for product differentiation, showcasing the industry's response to the role of AI in personalized pet nutrition.

What are the key market drivers leading to the rise in the adoption of Pet Food Industry?

- A key market driver is the growing consumer demand for organic pet food, which reflects a broader shift toward natural, chemical-free, and transparently sourced ingredients.

- The pet humanization trend is a primary driver, fueling premiumization in pet care and the demand for functional ingredients. Innovations in aseptic processing and quality control automation allow for the production of safe, high-quality veterinary-endorsed diets and raw food diets.

- Enhanced ingredient traceability and sophisticated feed formulation software are becoming standard, with some packaging innovations reducing carbon footprints by as much as 46%. Companies are leveraging data-driven marketing and focusing on palatability enhancers to capture consumer loyalty.

- The strategic by-product utilization to create upcycled ingredients also addresses sustainability concerns, contributing to a 7-point benefit from price and mix in certain product categories.

What are the market trends shaping the Pet Food Industry?

- The profound trend of pet humanization is fundamentally reshaping the market, creating significant consumer demand for premium nutritional products that align with human dietary standards.

- The pet food market is rapidly evolving, driven by the demand for sophisticated nutritional solutions that improve nutrient bioavailability. Innovations in freeze-drying technology and extrusion processes are enabling the development of human-grade pet food with superior quality. Dog feeding represents over 60% of retail sales in mature markets, with a pronounced shift towards functional pet nutrition.

- This includes products with bioactive compounds that support microbiome science. The fresh subcategory is projected to grow significantly, indicating a strong consumer preference for minimally processed options. Companies are also exploring alternative proteins and adopting mono-material packaging to align with the demand for sustainable ingredient sourcing and grain-free formulations with clean label ingredients.

What challenges does the Pet Food Industry face during its growth?

- Trade barriers and geopolitical volatility represent a significant market challenge, affecting industry growth by disrupting supply chains and elevating the cost of essential raw materials.

- Navigating operational costs and regulatory demands presents a significant challenge. Some companies have reported net sales falling by 4% due to consumer price sensitivity, while others have seen operating profits decline by 8.4% amid rising input costs. These pressures compel investment in technologies for shelf-life extension and antioxidant preservation.

- The market's shift toward specialized life-stage nutrition and breed-specific diets requires precise nutrient fortification and rigorous raw material analysis. Furthermore, consumer demand for ethical ingredient sourcing and recyclable pet food packaging adds complexity, particularly for direct-to-consumer models that rely on efficient e-commerce pet supplies logistics. Balancing cold-pressed processing costs with affordability remains a key hurdle.

Exclusive Technavio Analysis on Customer Landscape

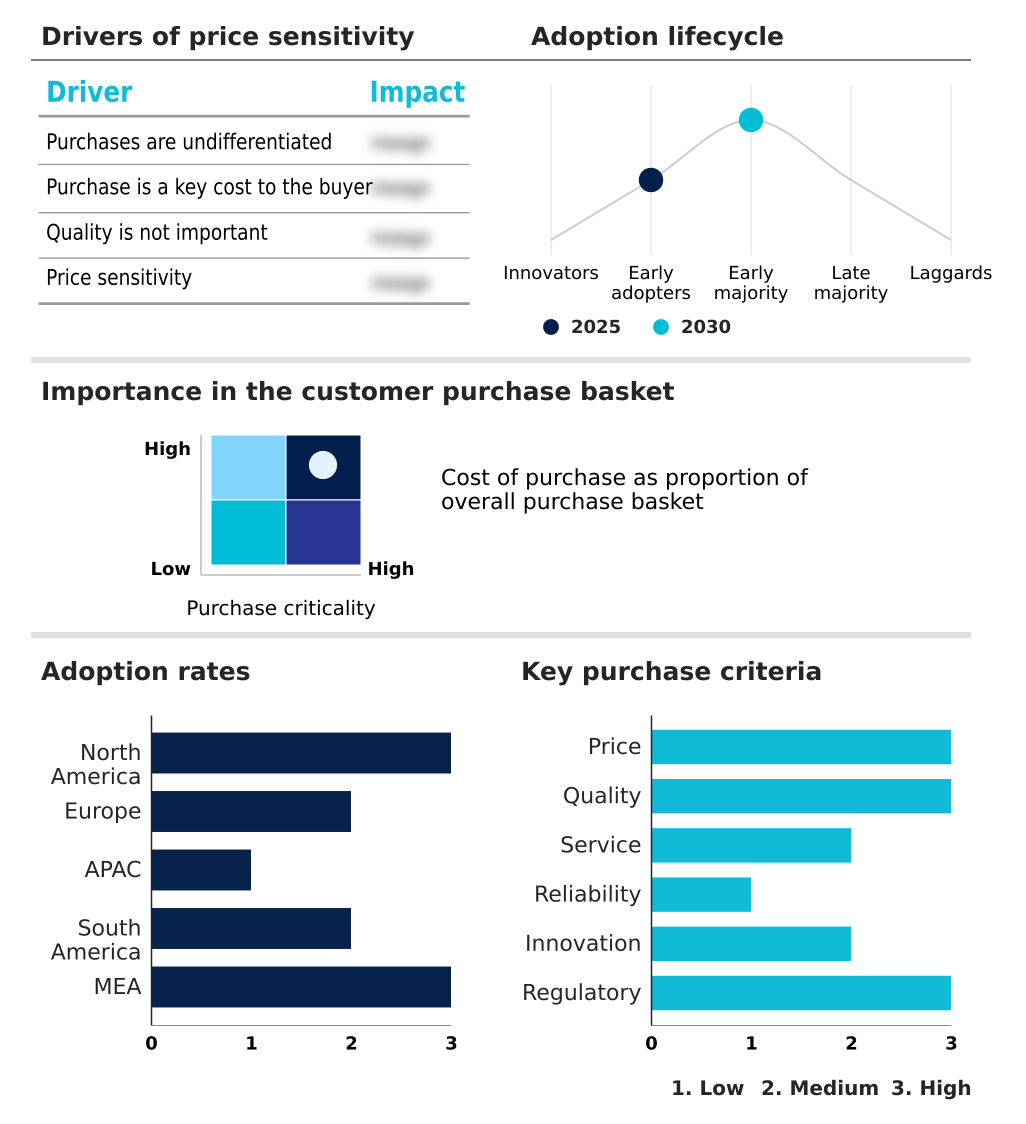

The pet food market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the pet food market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Pet Food Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, pet food market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Archer Daniels Midland Co. - Provides specialty pet nutrition ingredients and complete feed formulations, focusing on companion animal nutrition to meet diverse dietary requirements.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Archer Daniels Midland Co.

- C and D Foods Ltd.

- Colgate Palmolive Co.

- General Mills Inc.

- Global Pet Foods

- Hartz Mountain Corp.

- Himalaya Global Holdings Ltd.

- Mars Inc.

- Merrick Pet Care Inc.

- Nestle SA

- Nippon Pet Food Co. Ltd.

- NutriSource Pet Foods

- Premier Petfoods Company Pty Ltd.

- Schell and Kampeter Inc.

- Sunshine Mills Inc.

- The J.M. Smucker Co.

- Tiernahrung Deuerer GmbH

- Unicharm Corp.

- Wellness Pet Co. Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Pet food market

- In October, 2024, Hills Pet Nutrition opened a 365,000-square-foot smart manufacturing facility in Kansas, leveraging advanced automation and AI to produce over 170 wet food formulas and enhance food safety protocols.

- In February, 2025, Nestle Purina launched its innovative pyramid-shaped wet cat food, Gourmet Revelations, in fifteen European markets, a product designed with a unique texture to encourage natural feeding behaviors.

- In May, 2025, Mars, Incorporated inaugurated a new $450 million Royal Canin dry pet food manufacturing plant in Lewisburg, Ohio, focused on producing precise, science-based nutrition for cats and dogs.

- In May, 2025, the Brazilian pet food manufacturer Adimax opened a new production facility in Parana, enhancing its capacity for natural and premium lines while integrating at least 30% post-consumer recycled PET in its packaging.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Pet Food Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.2% |

| Market growth 2026-2030 | USD 45914.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.9% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, Australia, Indonesia, South Korea, Brazil, Argentina, Chile, UAE, South Africa, Saudi Arabia, Egypt and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The pet food market's technical landscape is evolving, with boardroom strategies focused on sustainable and scientific innovation. A key decision area is the adoption of alternative proteins, including insect-based protein and sustainable aquaculture feed, to ensure supply chain resilience.

- Manufacturing relies on extrusion processes, food extrusion technology, and cold-pressed processing to create therapeutic diets and hypoallergenic formulations that maximize nutrient bioavailability. The use of bioactive compounds, omega-3 fatty acids, and glucosamine for joint support in veterinary nutritional formulas is standard. Innovations like freeze-drying technology and advanced sterilization techniques using aseptic processing are vital for shelf-life extension and antioxidant preservation.

- Formulators use feed formulation software for precise nutrient fortification based on microbiome science and raw material analysis, ensuring ingredient traceability and adherence to pet food safety standards. The shift to clean label formulation promotes by-product utilization as upcycled food ingredients, while palatability enhancers and dietary fiber technology improve product performance.

- Sustainability goals are driving the adoption of mono-material packaging and active packaging systems with smart packaging integration, with some new designs achieving a 46% reduction in carbon footprint, showcasing how quality control automation links directly to corporate ESG objectives.

What are the Key Data Covered in this Pet Food Market Research and Growth Report?

-

What is the expected growth of the Pet Food Market between 2026 and 2030?

-

USD 45.91 billion, at a CAGR of 6.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Dry food, Wet food, and Snacks and treats), Type (Dog food, Cat food, and Others), Distribution Channel (Supermarkets and hypermarkets, Specialty stores, Online, Convenience stores, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing demand for organic pet food, Trade barriers and geopolitical volatility

-

-

Who are the major players in the Pet Food Market?

-

Archer Daniels Midland Co., C and D Foods Ltd., Colgate Palmolive Co., General Mills Inc., Global Pet Foods, Hartz Mountain Corp., Himalaya Global Holdings Ltd., Mars Inc., Merrick Pet Care Inc., Nestle SA, Nippon Pet Food Co. Ltd., NutriSource Pet Foods, Premier Petfoods Company Pty Ltd., Schell and Kampeter Inc., Sunshine Mills Inc., The J.M. Smucker Co., Tiernahrung Deuerer GmbH, Unicharm Corp. and Wellness Pet Co. Inc.

-

Market Research Insights

- The shift toward functional pet nutrition is reshaping product development, with a growing emphasis on clean label ingredients and sustainable ingredient sourcing. This focus has tangible impacts on business operations; for example, adopting recyclable pet food packaging has enabled a 46% reduction in carbon footprint for certain product lines.

- To engage modern consumers, companies are using data-driven marketing to create personalized pet food plans, a strategy that has contributed to a 7-point improvement from price and mix in key segments. The rising popularity of human-grade pet food and grain-free formulations highlights the premiumization in pet care trend.

- Success in this environment requires balancing raw material volatility with investments in advanced processing methods to deliver on the promise of holistic pet wellness.

We can help! Our analysts can customize this pet food market research report to meet your requirements.

RIA -

RIA -