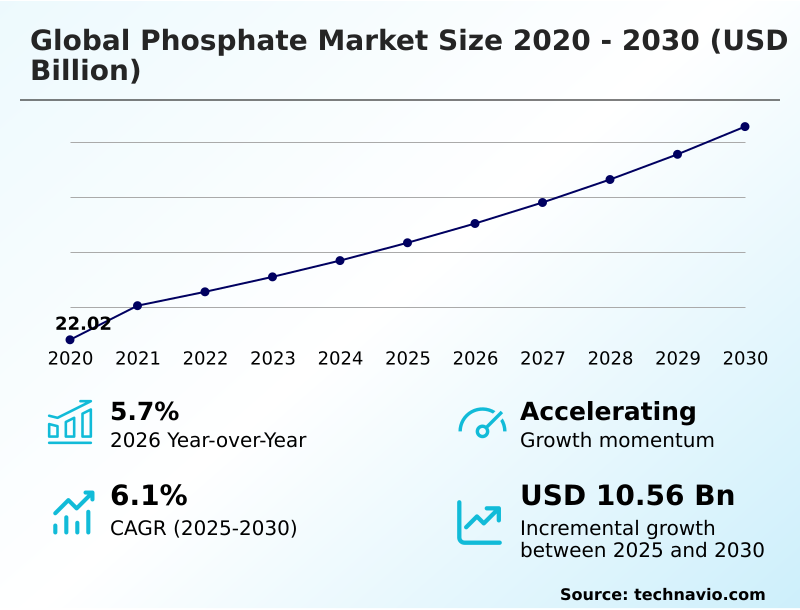

Phosphate Market Size 2026-2030

The phosphate market size is valued to increase by USD 10.56 billion, at a CAGR of 6.1% from 2025 to 2030. Growing demand for phosphate fertilizers will drive the phosphate market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 57.6% growth during the forecast period.

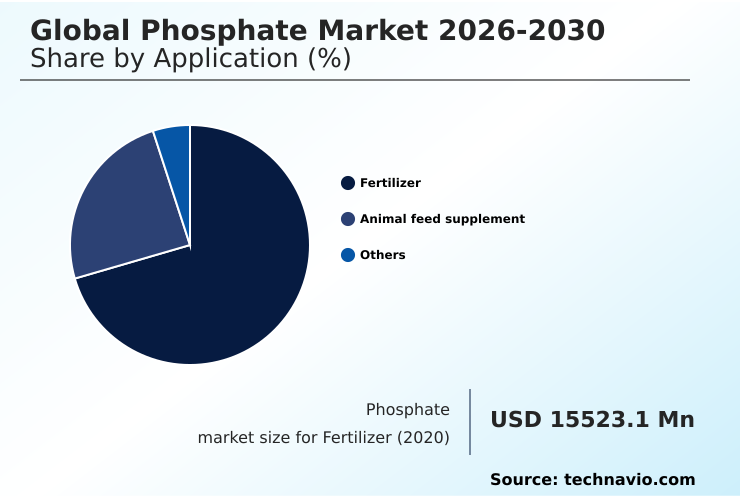

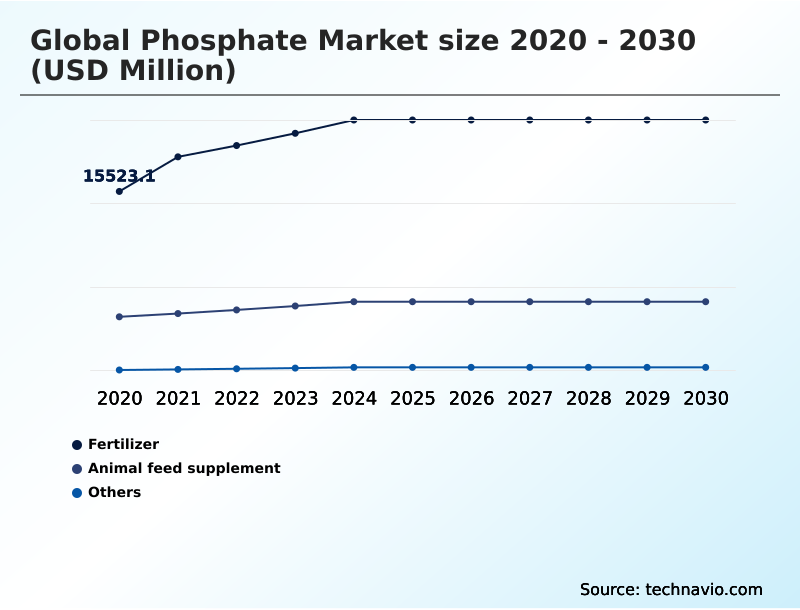

- By Application - Fertilizer segment was valued at USD 21.29 billion in 2024

- By Source - Sedimentary deposits segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 19.38 billion

- Market Future Opportunities: USD 10.56 billion

- CAGR from 2025 to 2030 : 6.1%

Market Summary

- The phosphate market is fundamental to global agriculture and increasingly vital for industrial sectors. Its core function remains supporting food production through fertilizers, but its scope is expanding. The industry is navigating complex phosphate market dynamics, influenced by geopolitical factors and the push for sustainable phosphate mining practices. In industrial phosphate applications, the focus is shifting toward high-value products.

- For instance, a key business scenario involves optimizing the phosphoric acid purification process to meet stringent specifications for electronics or food-grade materials, a far more complex challenge than standard phosphate ore beneficiation for bulk fertilizers. This requires significant capital investment in advanced filtration and treatment technologies.

- Concurrently, the demand for animal feed supplementation continues to grow with the global livestock industry, requiring feed-grade phosphates free from contaminants. Navigating these divergent demand signals—from bulk agriculture to high-purity industrial use—while addressing environmental concerns and supply chain vulnerabilities defines the strategic landscape for market participants.

- The ability to pivot between different grades and applications is becoming a critical competitive advantage.

What will be the Size of the Phosphate Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Phosphate Market Segmented?

The phosphate industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Fertilizer

- Animal feed supplement

- Others

- Source

- Sedimentary deposits

- Igneous deposits

- Marine deposits

- Product type

- Diammonium phosphate

- Monoammonium phosphate

- Triple superphosphate

- Single superphosphate

- Others

- Geography

- APAC

- China

- India

- Indonesia

- North America

- US

- Canada

- Mexico

- Europe

- Spain

- Germany

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- Rest of World (ROW)

- APAC

By Application Insights

The fertilizer segment is estimated to witness significant growth during the forecast period.

The fertilizer segment is foundational to the phosphate market, driven by the non-negotiable need for agricultural nutrient management to ensure global food security.

Demand for products like diammonium phosphate and monoammonium phosphate is tied directly to crop cycles and the continuous effort for soil fertility enhancement to achieve crop yield improvement.

Phosphate fertilizer production is a complex process, influenced by raw material access and logistics. The market's growth is geographically concentrated, with the APAC region alone representing 57.6% of the incremental growth, underscoring its pivotal role in global agricultural output.

This highlights the segment's deep integration with regional food policies and large-scale farming operations that depend on consistent phosphate supply for sustained productivity.

The Fertilizer segment was valued at USD 21.29 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 57.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Phosphate Market Demand is Rising in APAC Get Free Sample

The geographic landscape is defined by a concentration of phosphate rock reserves in a few key regions, which creates vulnerabilities within the global phosphate supply chain and contributes to fertilizer price fluctuation.

APAC is the dominant growth engine, expanding at a rate of 7.3% and accounting for approximately 57.6% of the market's incremental growth, driven by massive agricultural demand.

North America follows with a more moderate 5.0% growth rate, focusing on high-efficiency agriculture and domestic supply security.

In Europe, the import-dependent market is shaped by regulations like the Critical Raw Materials Act, which prioritizes supply chain diversification and recycling to mitigate geopolitical risks.

This regional disparity in production and consumption underpins global trade flows and strategic investment decisions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The market is undergoing a structural shift, driven by the significant impact of lfp battery demand on phosphate, which pulls high-purity material away from traditional agriculture. This trend is particularly relevant for meeting the needs of low-cadmium phosphate for european markets, where environmental standards are stringent.

- Simultaneously, the established role of phosphate in animal nutrition continues to grow, although industry faces challenges in managing heavy metal in feed phosphates. The expanding industrial use of phosphate in water treatment corrosion prevention highlights its versatility. Strategic sourcing decisions increasingly weigh sedimentary vs igneous phosphate sourcing, as igneous deposits often offer higher purity.

- A key trend is converting green phosphoric acid to fertilizer, which supports circular economy goals. In India, nutrient based subsidy effects on ssp use are reshaping domestic demand patterns. Globally, the challenges of marine phosphate deposit mining remain largely unresolved due to ecological concerns, while land-based operations face tightening environmental regulations on phosphogypsum stacks.

- In response, technology for enhancing nutrient uptake and innovations in phosphate recovery from municipal wastewater are gaining traction. This is partly driven by market impact of phosphate export quotas from major producers. The choice between dap vs map in alkaline soils remains a key agronomic decision, while the specific use of tsp for nitrogen-fixing legume crops demonstrates niche demand.

- Circular economy models for phosphorus are becoming central to long-term strategy. The phosphate sourcing for industrial chemicals and the role of phosphates in processed foods represent stable, value-added segments, while producers grapple with how to reduce raw material price volatility through strategic hedging and vertical integration.

- Overall, sustainable practices in phosphate mining are now a non-negotiable aspect of operational planning, with companies investing in cleaner technologies seeing a 15% improvement in their ESG ratings compared to laggards.

What are the key market drivers leading to the rise in the adoption of Phosphate Industry?

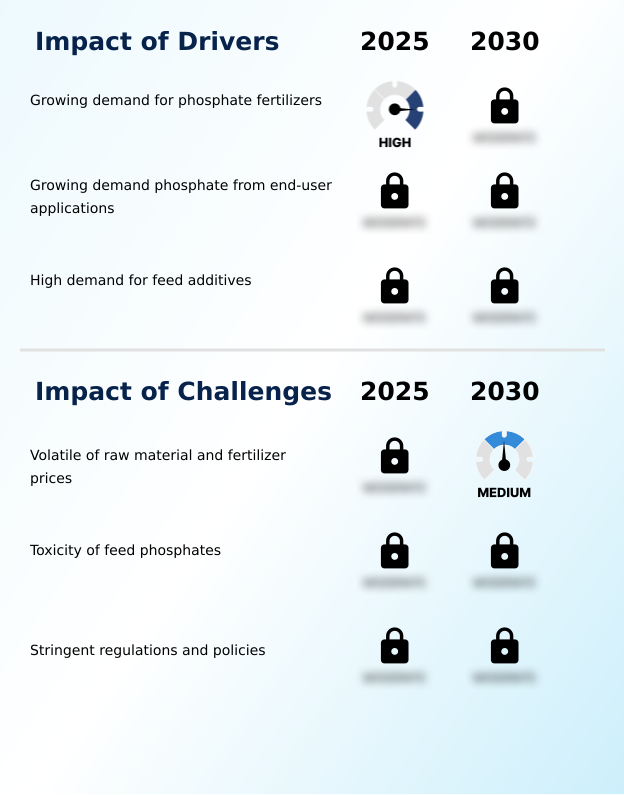

- The escalating global demand for phosphate fertilizers to enhance agricultural productivity serves as the primary market driver.

- Market growth is driven by the dual needs of agricultural intensification and industrial diversification. The primary driver remains the need for soil health improvement through effective fertilization, supported by efficient mineral deposit extraction to ensure supply.

- However, there is a clear shift toward specialty phosphate products designed for high-value crops, which have demonstrated yield increases of 10-15% over conventional fertilizers.

- Concurrently, environmental regulations are fueling demand for better nutrient runoff management, leading to innovations in liquid fertilizer formulation. These advanced formulations offer up to 95% application uniformity, ensuring precise nutrient delivery while minimizing waste.

- This drive for efficiency and sustainability is expanding the market beyond traditional applications.

What are the market trends shaping the Phosphate Industry?

- The increasing production of ammonium phosphate utilizing green phosphoric acid is a notable market trend. This development is creating new opportunities across various end-user applications.

- Key trends are reshaping product development, moving beyond bulk commodities toward high-efficiency solutions. The focus is on maximizing plant energy transfer and root development stimulation through specialized formulations. The rise of organic farming inputs has spurred innovation in bio-based phosphate fertilizer products, which are shown to improve soil microbial activity by over 25%. These sustainable alternatives address soil degradation concerns.

- Furthermore, the adoption of precision agriculture nutrients is a major trend, where variable-rate application technologies can reduce phosphate overuse by up to 40%, optimizing farm economics and minimizing environmental runoff. This shift reflects a move from volume to value, where performance and sustainability dictate market preference, especially in regulated agricultural economies.

What challenges does the Phosphate Industry face during its growth?

- The inherent volatility of raw material and fertilizer prices presents a significant challenge to sustained industry growth.

- The industry confronts significant hurdles related to supply chain stability and regulatory compliance. Volatile phosphate market dynamics, where geopolitical events can trigger price spikes of over 50% in a quarter, create profound uncertainty for both producers and consumers. The push for sustainable phosphate mining and reducing the environmental impact of mining is adding operational complexity and cost.

- For example, compliance with stringent heavy metal regulations, such as new cadmium limits in fertilizers, can increase processing costs by as much as 20%. Furthermore, legislative frameworks like the Critical Raw Materials Act are reshaping global trade flows by encouraging regional sourcing and recycling, challenging the business models of traditional, large-scale exporters.

Exclusive Technavio Analysis on Customer Landscape

The phosphate market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the phosphate market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Phosphate Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, phosphate market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AquaPhoenix Scientific Inc. - Provides a specialized portfolio of phosphate compounds, such as orthophosphate and metaphosphate, in addition to vital laboratory reagents and high-purity analytical standards.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AquaPhoenix Scientific Inc.

- Avantor Inc.

- CMOC Group Limited

- EuroChem Group AG

- Fertoz Ltd.

- Innophos Holdings Inc.

- Israel Chemicals Ltd.

- Jordan Phosphate Mines Co. PLC

- Koch Fertilizer LLC

- Misr Phosphate Co.

- Nutrien Ltd.

- OCP Group

- PhosAgro Group of Companies

- Saudi Arabian Mining Co.

- Solvay SA

- The Mosaic Co.

- Yunnan Phosphate Haikou Co.

- Yuntianhua Group Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Phosphate market

- In December 2024, the Saudi Arabian Mining Company (Maaden) finalized the acquisition of the entire stake of the Mosaic Company in the Waad Al Shamal Phosphate Company, strengthening its global leadership in phosphate fertilizer production.

- In February 2025, the European Commission introduced a directive requiring member states to increase phosphorus recovery from municipal wastewater sludge by 20%, aiming to advance the circular economy.

- In June 2025, a leading fertilizer company in Tampa unveiled a new facility for producing high-purity monoammonium phosphate, specifically targeting the growing battery materials supply chain.

- In July 2025, OCP Group in Morocco commissioned a major industrial desalination facility at its Jorf Lasfar hub, securing water supply for phosphoric acid production amid climatic volatility.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Phosphate Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 304 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.1% |

| Market growth 2026-2030 | USD 10561.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.7% |

| Key countries | China, India, Vietnam, Thailand, Indonesia, Australia, US, Canada, Mexico, Russia, Spain, Germany, France, Poland, The Netherlands, Brazil, Argentina, Chile, Morocco, Saudi Arabia, Egypt, Algeria and Tunisia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The phosphate market is evolving beyond its agricultural foundations, now defined by raw material volatility and a strategic pivot towards a circular nutrient economy.

- While demand for fertilizers like diammonium phosphate (dap), monoammonium phosphate (map), triple superphosphate (tsp), and single superphosphate (ssp) remains strong, influenced by policies like the nutrient based subsidy (nbs), a significant boardroom decision involves allocating resources to produce high-purity phosphoric acid for the lithium iron phosphate (lfp) battery sector.

- This requires a sophisticated beneficiation process and granulation technology to create superior phosphate rock concentrate. Producers are diversifying from sedimentary phosphate deposits to explore igneous phosphate deposits and even nascent marine phosphate deposits. The industry faces pressures from phosphogypsum waste management and stringent cadmium content regulation.

- Investment in apatite rock processing now includes advanced fluorine removal process technology to mitigate heavy metal contamination and lower the arsenic impurity level, especially for food-grade phosphoric acid and feed grade phosphate products like monocalcium phosphate and dicalcium phosphate. The focus on sustainability is driving innovation in phosphate recovery technology, including struvite precipitation, to reduce eutrophication risk.

- This push creates demand for enhanced efficiency fertilizer and slow-release fertilizer products that improve crop nutrient uptake and act as a soil ph amendment, with some solutions improving uptake efficiency by 20%. Simultaneously, phosphate’s role as a corrosion inhibitor and water treatment chemical continues to expand.

What are the Key Data Covered in this Phosphate Market Research and Growth Report?

-

What is the expected growth of the Phosphate Market between 2026 and 2030?

-

USD 10.56 billion, at a CAGR of 6.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Fertilizer, Animal feed supplement, and Others), Source (Sedimentary deposits, Igneous deposits, and Marine deposits), Product Type (Diammonium phosphate, Monoammonium phosphate, Triple superphosphate, Single superphosphate, and Others) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing demand for phosphate fertilizers, Volatile of raw material and fertilizer prices

-

-

Who are the major players in the Phosphate Market?

-

AquaPhoenix Scientific Inc., Avantor Inc., CMOC Group Limited, EuroChem Group AG, Fertoz Ltd., Innophos Holdings Inc., Israel Chemicals Ltd., Jordan Phosphate Mines Co. PLC, Koch Fertilizer LLC, Misr Phosphate Co., Nutrien Ltd., OCP Group, PhosAgro Group of Companies, Saudi Arabian Mining Co., Solvay SA, The Mosaic Co., Yunnan Phosphate Haikou Co. and Yuntianhua Group Co. Ltd.

-

Market Research Insights

- Market dynamics are shaped by demand diversification beyond agriculture. While essential for livestock bone development in animal feed, phosphates are critical as food and beverage additives, enhancing product stability. In industrial use cases, phosphates function as a key metal finishing agent, where process efficiency has improved coating adhesion by 10%. Concurrently, stringent environmental regulations are driving innovation.

- Advanced wastewater treatment solutions now achieve up to a 30% greater phosphorus recovery rate, turning a waste stream into a valuable resource. Furthermore, new methods are reducing the environmental impact of mining, with some operations cutting water consumption by over 15%. This shift toward value-added applications and sustainable practices defines the market's trajectory, balancing industrial need with ecological responsibility.

We can help! Our analysts can customize this phosphate market research report to meet your requirements.

RIA -

RIA -