Self-driving Truck Market Size 2025-2029

The self-driving truck market size is valued to increase by USD 52.34 billion, at a CAGR of 19.3% from 2024 to 2029. Advancements in technology propelling market growth will drive the self-driving truck market.

Major Market Trends & Insights

- North America dominated the market and accounted for a 49% growth during the forecast period.

- By End-user - Logistics segment was valued at USD 16.11 billion in 2023

- By Technology - Level 1 segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 60.08 billion

- Market Future Opportunities: USD 52.34 billion

- CAGR from 2024 to 2029 : 19.3%

Market Summary

What will be the Size of the Self-driving Truck Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Self-driving Truck Market Segmented?

The self-driving truck industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

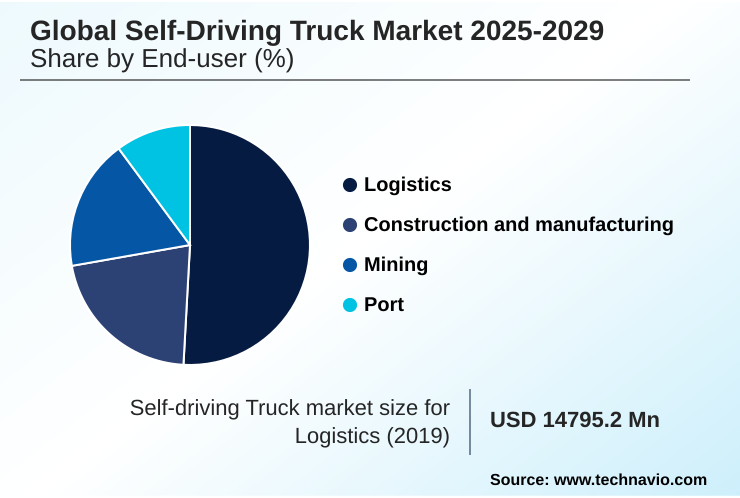

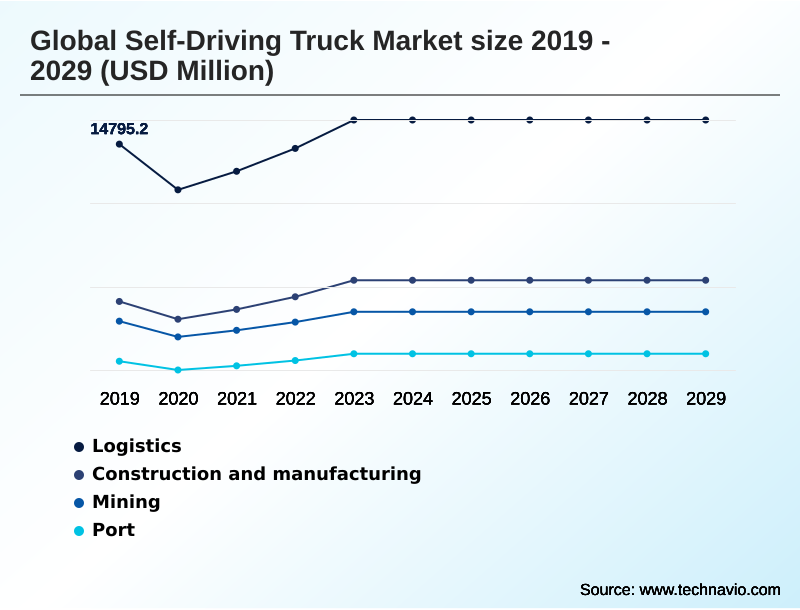

- End-user

- Logistics

- Construction and manufacturing

- Mining

- Port

- Technology

- Level 1

- Level 3

- Level 4

- Level 5

- Propulsion

- Internal combustion

- Hybrid transmission

- Electric transmission

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By End-user Insights

The logistics segment is estimated to witness significant growth during the forecast period.

The Logistics segment was valued at USD 16.11 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 49% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Self-driving Truck Market Demand is Rising in North America Get Free Sample

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Self-driving Truck Industry?

What are the market trends shaping the Self-driving Truck Industry?

What challenges does the Self-driving Truck Industry face during its growth?

Exclusive Technavio Analysis on Customer Landscape

The self-driving truck market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the self-driving truck market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Self-driving Truck Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, self-driving truck market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AB Volvo -

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AB Volvo

- Caterpillar Inc.

- Continental AG

- Daimler Truck AG

- Einride AB

- Ford Motor Co.

- Inceptio Technology

- Isuzu Motors Ltd.

- Iveco Group N.V

- Kodiak Robotics Inc.

- PACCAR Inc.

- PlusAI Inc.

- Tesla Inc.

- Torc Robotics Inc.

- Traton SE

- Volkswagen AG

- Waymo LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Self-driving truck market

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Self-driving Truck Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 305 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 19.3% |

| Market growth 2025-2029 | USD 52344.2 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 14.8% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, The Netherlands, Spain, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

What are the Key Data Covered in this Self-driving Truck Market Research and Growth Report?

-

What is the expected growth of the Self-driving Truck Market between 2025 and 2029?

-

USD 52.34 billion, at a CAGR of 19.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Logistics, Construction and manufacturing, Mining, and Port), Technology (Level 1, Level 3, Level 4, and Level 5), Propulsion (Internal combustion, Hybrid transmission, and Electric transmission) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Advancements in technology propelling market growth, Regulatory and legal uncertainty

-

-

Who are the major players in the Self-driving Truck Market?

-

AB Volvo, Caterpillar Inc., Continental AG, Daimler Truck AG, Einride AB, Ford Motor Co., Inceptio Technology, Isuzu Motors Ltd., Iveco Group N.V, Kodiak Robotics Inc., PACCAR Inc., PlusAI Inc., Tesla Inc., Torc Robotics Inc., Traton SE, Volkswagen AG and Waymo LLC

-

Market Research Insights

We can help! Our analysts can customize this self-driving truck market research report to meet your requirements.

RIA -

RIA -