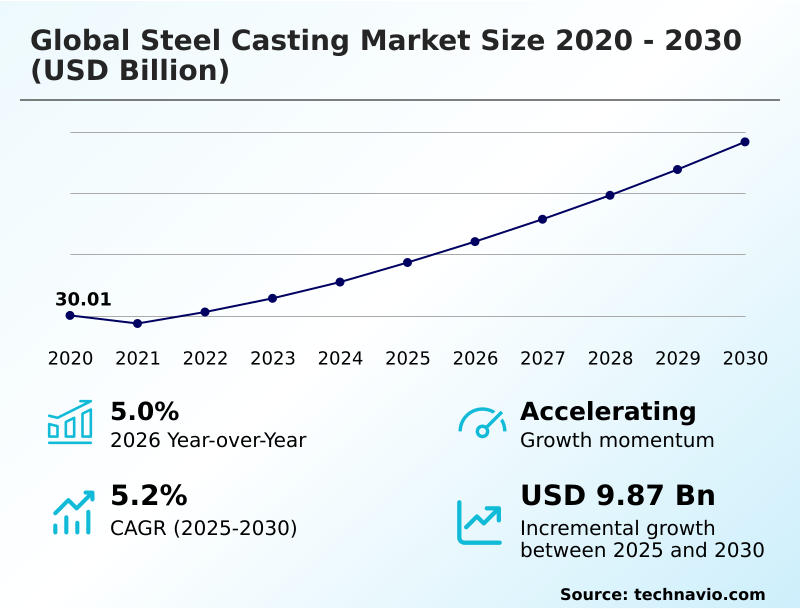

Steel Casting Market Size 2026-2030

The steel casting market size is valued to increase by USD 9.87 billion, at a CAGR of 5.2% from 2025 to 2030. Accelerated global energy transition and shift toward renewable energy infrastructure will drive the steel casting market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 55.4% growth during the forecast period.

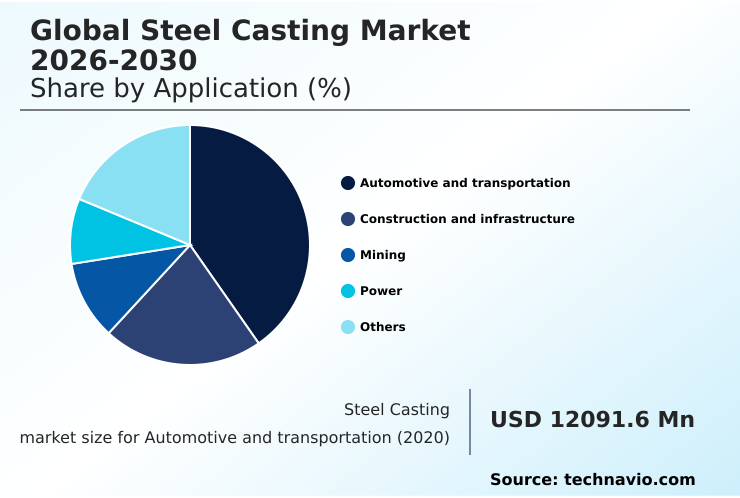

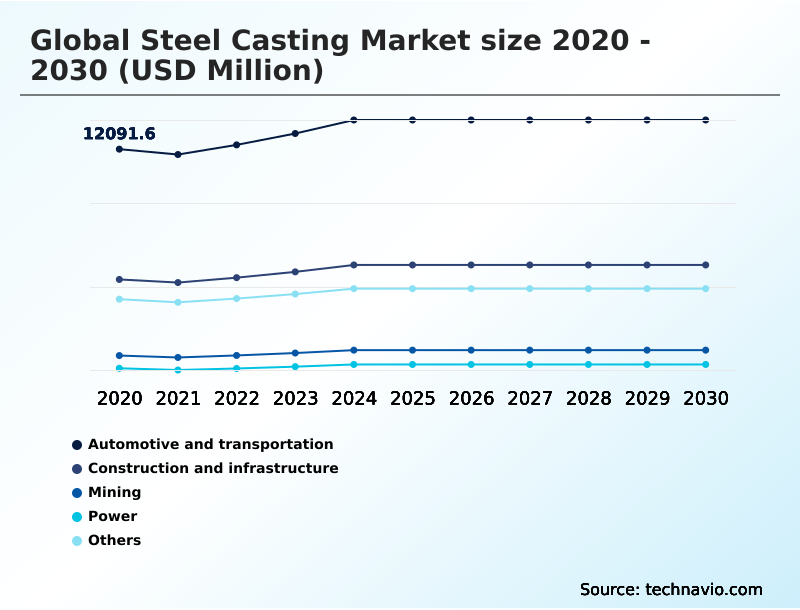

- By Application - Automotive and transportation segment was valued at USD 13.35 billion in 2024

- By Product - Sand casting segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 14.20 billion

- Market Future Opportunities: USD 9.87 billion

- CAGR from 2025 to 2030 : 5.2%

Market Summary

- The steel casting market is advancing beyond traditional manufacturing, driven by the need for high-performance materials in critical sectors. This evolution is marked by a focus on specialty alloy development and the adoption of advanced foundry automation to produce complex components with enhanced mechanical properties.

- For instance, a firm specializing in parts for renewable energy infrastructure can leverage AI-driven casting simulation and foundry digital twin integration to optimize the production of wind turbine rotor hubs, reducing material waste and ensuring structural integrity. This approach addresses challenges in metal solidification analysis and improves casting defect reduction.

- The industry is also pivoting toward carbon-neutral steel production, integrating electric arc furnace technology and scrap-based decarbonization to meet stringent environmental standards. The ability to deliver born-qualified cast parts with documented performance, from high-pressure environment casting to large-scale structural castings, is becoming a key differentiator.

- This shift requires not only technological investment but also a resilient supply chain for high-purity iron ore and ferroalloys, ensuring consistent quality across all production cycles.

What will be the Size of the Steel Casting Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Steel Casting Market Segmented?

The steel casting industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Automotive and transportation

- Construction and infrastructure

- Mining

- Power

- Others

- Product

- Sand casting

- Investment casting

- Die casting

- Centrifugal casting

- Type

- Carbon steel

- Low-alloy steel

- High-alloy steel

- Others

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- Italy

- France

- Middle East and Africa

- South Africa

- Saudi Arabia

- Turkey

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Application Insights

The automotive and transportation segment is estimated to witness significant growth during the forecast period.

The automotive and transportation segment is undergoing a significant transformation, driven by the shift to electric platforms and lightweighting imperatives. Demand for traditional powertrain components is evolving, while the adoption of the giga-casting manufacturing process for structural parts is accelerating.

This method, often utilizing advanced die casting and high-strength low-alloy steel, enables the production of large, near-net-shape casting components, which has been shown to reduce part counts by over 20%.

Foundries are leveraging advanced foundry automation and specializing in precision-engineered components to meet stringent OEM requirements.

The focus on scrap-based decarbonization and sustainable smelting processes is also influencing material selection, with an emphasis on carbon steel casting grades and low-alloy steel properties for applications from passenger vehicles to heavy-duty cast bogie frames.

The Automotive and transportation segment was valued at USD 13.35 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 55.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Steel Casting Market Demand is Rising in APAC Get Free Sample

The geographic landscape is characterized by distinct regional specializations and intense competition. APAC continues to lead in production volume, focusing on heavy machinery components and large-scale structural castings for infrastructure projects.

In this region, modern foundries have improved casting defect reduction by over 25% by implementing metal solidification analysis tools.

North America and Europe are distinguished by their focus on high-value applications, such as precision-engineered components and high-integrity castings for the aerospace and energy sectors.

European firms, in particular, are pioneering carbon-neutral steel production and sustainable smelting processes, driven by stringent regulations.

These regions leverage advanced heat treatment process technologies and 3D-printed sand molds to produce components from duplex stainless steel and super-duplex stainless steel, meeting high surface finish standards.

The strategic management of the ferroalloy supply chain remains a critical factor for competitiveness across all geographies.

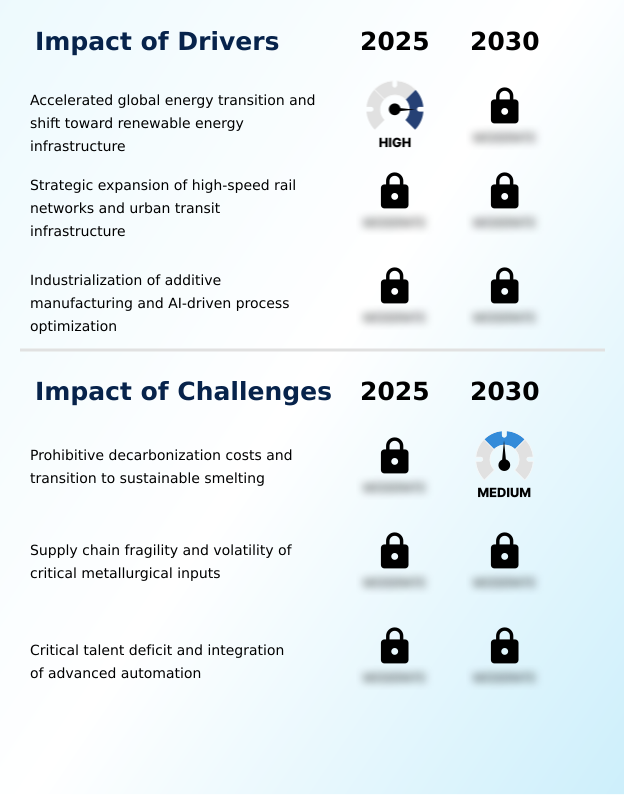

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic focus of the steel casting market is diversifying across high-value applications, directly impacting operational planning and supply chain configurations. The demand for steel casting for wind turbine hubs and broader steel casting for renewable energy infrastructure is compelling foundries to master large-scale, high-integrity production.

- In parallel, the transportation sector's requirements for high-strength steel for high-speed rail and low-carbon steel castings for automotive applications are driving innovations in lightweighting and material science.

- The use of additive manufacturing in steel casting is accelerating prototyping for precision steel casting for aerospace components and investment casting for medical implants, with some firms reporting a 40% reduction in development lead times compared to traditional tooling methods. For heavy-duty sectors, producing wear-resistant castings for mining equipment and casting solutions for subsea applications remains a core business.

- Foundries are increasingly using AI simulation for casting defect prediction to enhance quality control in steel casting, which is critical for high-alloy steel casting for nuclear reactors and centrifugal casting for petrochemical pipes.

- These specialized demands are pushing the industry to refine processes for optimizing steel casting cycle times and implementing sustainable practices in steel foundries, ultimately enabling cost reduction in the steel casting process and clarifying decisions on steel casting vs forging applications.

What are the key market drivers leading to the rise in the adoption of Steel Casting Industry?

- The accelerated global energy transition and a pronounced shift toward renewable energy infrastructure are key drivers propelling market growth.

- Market growth is significantly propelled by industrial modernization and the adoption of advanced manufacturing technologies.

- Casting 4.0 implementation, which includes robotic casting cell systems and smart castings with IoT sensors, is a key driver, with some operators reporting a 20% increase in production uptime.

- This digital transformation facilitates the creation of high-integrity castings and modular casting designs. The demand for specialty alloy development is surging, driven by the need for materials that can perform in high-pressure environment casting scenarios.

- The industrialization of the Giga-casting manufacturing process in the automotive sector is another powerful driver, enabling vehicle light-weighting and simplifying assembly.

- These technological advancements, combined with a focus on non-destructive testing of castings and lean manufacturing in foundries, are enhancing overall competitiveness and operational excellence.

What are the market trends shaping the Steel Casting Industry?

- The market is experiencing a structural transition toward green steel casting, driven by the increasing importance of achieving carbon neutrality in production processes.

- A primary trend reshaping the market is the structural move toward sustainability, driven by circular economy in foundries and the need for carbon-neutral steel production. This shift is materializing through the adoption of green hydrogen-based reduction and sustainable smelting processes, which have been shown to lower emissions by over 30% in pilot facilities compared to conventional methods.

- The emphasis on low-carbon casting process technologies is creating new opportunities for high-chromium steel alloys and manganese steel components, particularly in green infrastructure. Furthermore, the use of powder metallurgy for casting and investment casting applications is expanding, allowing for more intricate designs.

- The development of advanced alloys with superior passive film formation and sour gas resistant steel properties is critical for extreme environments, reflecting a broader industry push toward high-performance materials.

What challenges does the Steel Casting Industry face during its growth?

- Prohibitive decarbonization costs associated with the transition to sustainable smelting present a key challenge affecting industry growth.

- The market faces significant challenges related to supply chain volatility and operational costs. Securing a stable supply of high-purity iron ore sourcing and managing metallurgical coal logistics are persistent hurdles, with price fluctuations impacting profit margins by as much as 10-15% quarter-over-quarter for some foundries.

- The high capital investment required for a high-tonnage forge press and advanced automation presents a barrier to entry for smaller players. Furthermore, achieving consistent quality in thin-wall investment casting and large-scale forging and casting remains a technical challenge. Foundries are working to improve metal solidification analysis and casting surface finish standards to address these issues.

- Ensuring supply chain resilience for foundries is now a top priority, compelling firms to diversify suppliers and invest in better inventory management systems to mitigate disruptions.

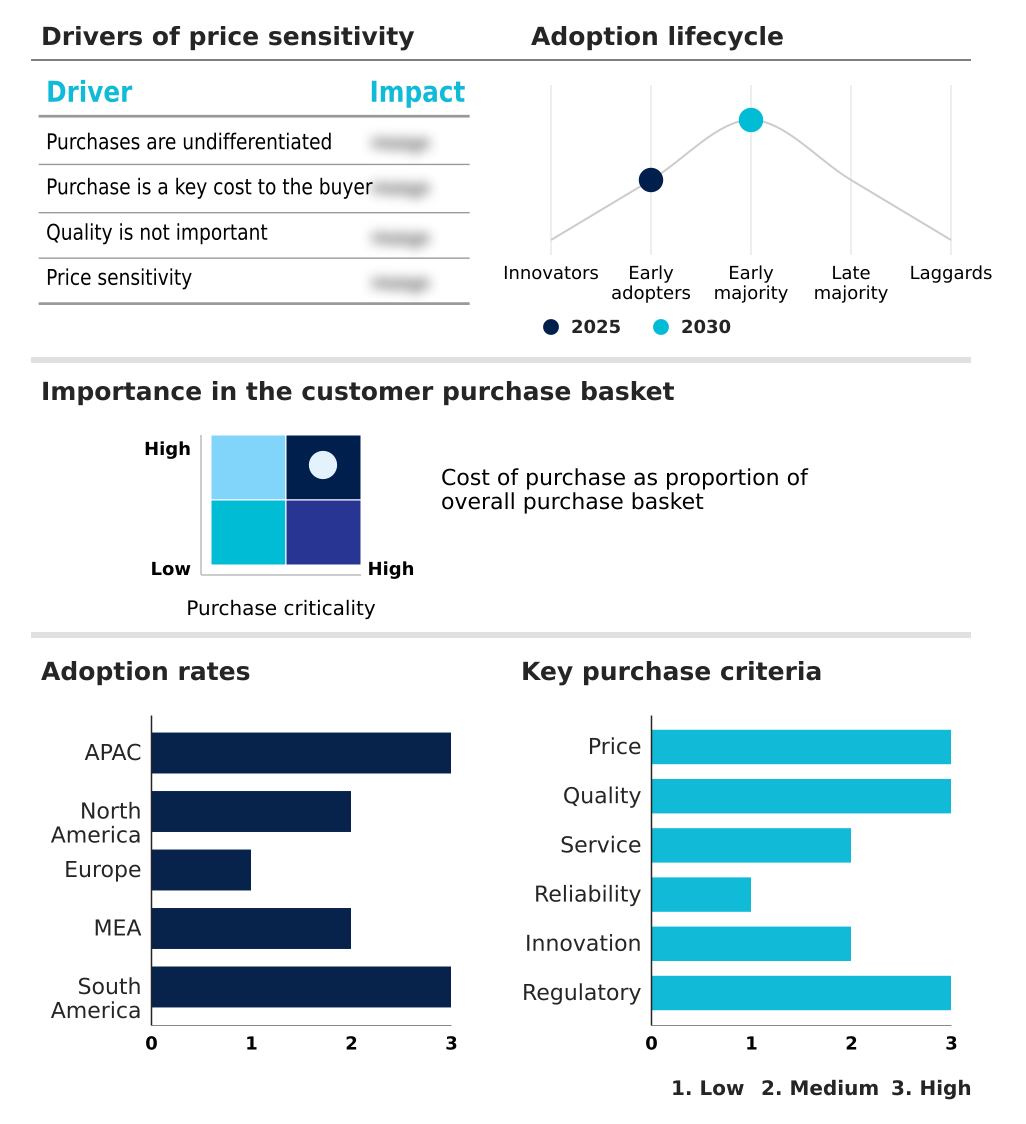

Exclusive Technavio Analysis on Customer Landscape

The steel casting market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the steel casting market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Steel Casting Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, steel casting market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ArcelorMittal - Specializing in advanced steel casting, the firm provides custom tool steels and die blocks engineered for high-performance forging and stamping applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ArcelorMittal

- Aubert and Duval

- Bradken Ltd

- Columbia Steel Casting Co Inc.

- Doosan Corp.

- Eagle Alloy Inc

- Harrison Steel Castings Co.

- HITCHINER Manufacturing Co.

- Impro Precision Industries Ltd.

- Kubota Corp.

- Magotteaux

- MetalTek International

- Nippon Steel Corp.

- Peekay Steel Castings Pvt. Ltd.

- Proterial Ltd.

- Scaw Metals Group

- Sheffield Forgemasters

- Stainless Foundry and Engineering

- The Japan Steel Works Ltd.

- voestalpine AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Steel casting market

- In January 2025, Nippon Steel announced a major strategic expansion in the APAC region through its joint venture, ArcelorMittal Nippon Steel, which involves activating new production lines in India to support the local automotive sector with high-grade steel components.

- In May 2025, Auxo Investment Partners announced the acquisition of Bay Cast Incorporated, a strategic move highlighting the ongoing consolidation within the high-precision casting market to better serve the space and defense sectors.

- In February 2025, Dillinger Hutte and the SMS Group entered into a strategic partnership focused on precision blast furnace optimization and the adoption of greener production technologies, reflecting a broader regional trend toward industrial decarbonization.

- In October 2024, voestalpine AG announced an investment exceeding two hundred million euros in its steel division to transition from traditional blast furnaces to electric arc furnace technology, aligning with its decarbonization goals.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Steel Casting Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 312 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.2% |

| Market growth 2026-2030 | USD 9867.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.0% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, Italy, France, UK, Spain, The Netherlands, South Africa, Saudi Arabia, Turkey, Egypt, Iran, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The steel casting market is defined by a significant technological shift toward precision and sustainability, where metallurgical process control is paramount for boardroom strategy. The integration of advanced manufacturing, from the sand casting process to high-pressure die casting, is enabling the creation of complex components.

- Key technologies such as AI-driven casting simulation and foundry digital twin integration are now standard for optimizing the production of carbon steel casting grades and high-alloy steel metallurgy. Firms are achieving superior material properties through vacuum induction melting and advanced heat treatment process methods, especially for low-alloy steel properties and duplex stainless steel casting.

- The use of 3D-printed sand molds allows for the rapid production of near-net-shape casting parts like cast nacelle frames and heavy machinery components. One verifiable trend is the adoption of electric arc furnace technology, which has enabled leading foundries to reduce energy consumption per ton of molten steel handling by up to 15%.

- This focus on efficiency and quality is critical for manufacturing everything from austenitic stainless steel parts to wear-resistant steel castings.

What are the Key Data Covered in this Steel Casting Market Research and Growth Report?

-

What is the expected growth of the Steel Casting Market between 2026 and 2030?

-

USD 9.87 billion, at a CAGR of 5.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Automotive and transportation, Construction and infrastructure, Mining, Power, and Others), Product (Sand casting, Investment casting, Die casting, and Centrifugal casting), Type (Carbon steel, Low-alloy steel, High-alloy steel, and Others) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Accelerated global energy transition and shift toward renewable energy infrastructure, Prohibitive decarbonization costs and transition to sustainable smelting

-

-

Who are the major players in the Steel Casting Market?

-

ArcelorMittal, Aubert and Duval, Bradken Ltd, Columbia Steel Casting Co Inc., Doosan Corp., Eagle Alloy Inc, Harrison Steel Castings Co., HITCHINER Manufacturing Co., Impro Precision Industries Ltd., Kubota Corp., Magotteaux, MetalTek International, Nippon Steel Corp., Peekay Steel Castings Pvt. Ltd., Proterial Ltd., Scaw Metals Group, Sheffield Forgemasters, Stainless Foundry and Engineering, The Japan Steel Works Ltd. and voestalpine AG

-

Market Research Insights

- The market is shaped by a focus on foundry operational efficiency and supply chain resilience for foundries. The implementation of Casting 4.0, integrating advanced foundry automation and robotic casting cell systems, has demonstrated a capacity to reduce casting defect rates by up to 15%. This pivot to smart manufacturing supports the delivery of high-integrity castings and born-qualified cast parts.

- Concurrently, circular economy in foundries and scrap-based decarbonization are central strategies, with firms reporting a 10% improvement in resource utilization through lean manufacturing in foundries and foundry waste heat recovery. The Giga-casting manufacturing process is transforming automotive applications, while specialty alloy development addresses demand for corrosion-resistant steel grades in high-pressure environments.

- These dynamics underscore a market where technological adoption and sustainability are directly tied to competitive advantage and profitability.

We can help! Our analysts can customize this steel casting market research report to meet your requirements.

RIA -

RIA -