Train Collision Avoidance System Market Size 2026-2030

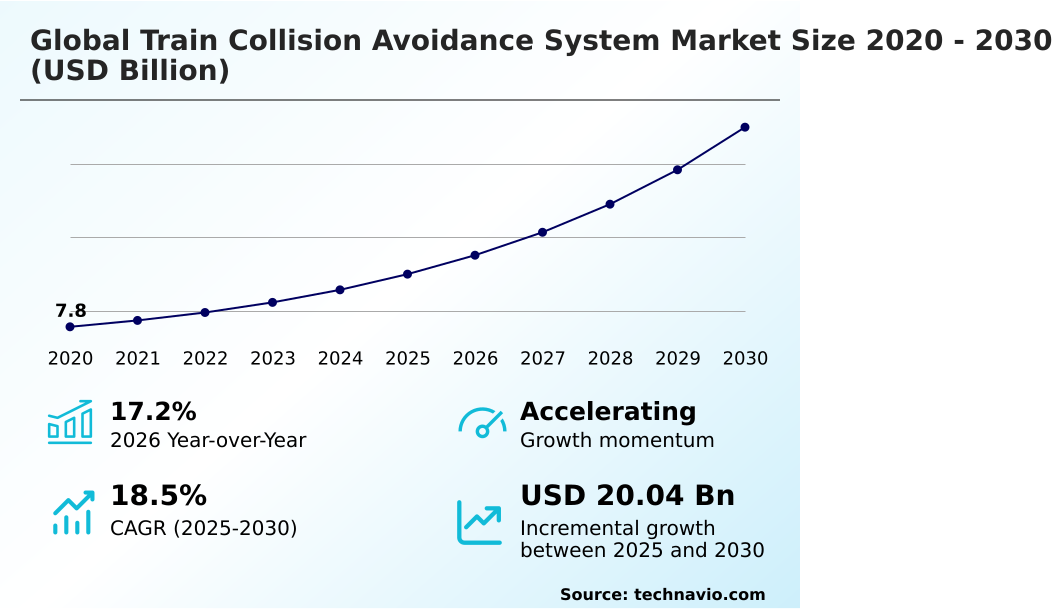

The train collision avoidance system market size is valued to increase by USD 20.04 billion, at a CAGR of 18.5% from 2025 to 2030. Growing adoption of high-speed rail by emerging economies will drive the train collision avoidance system market.

Major Market Trends & Insights

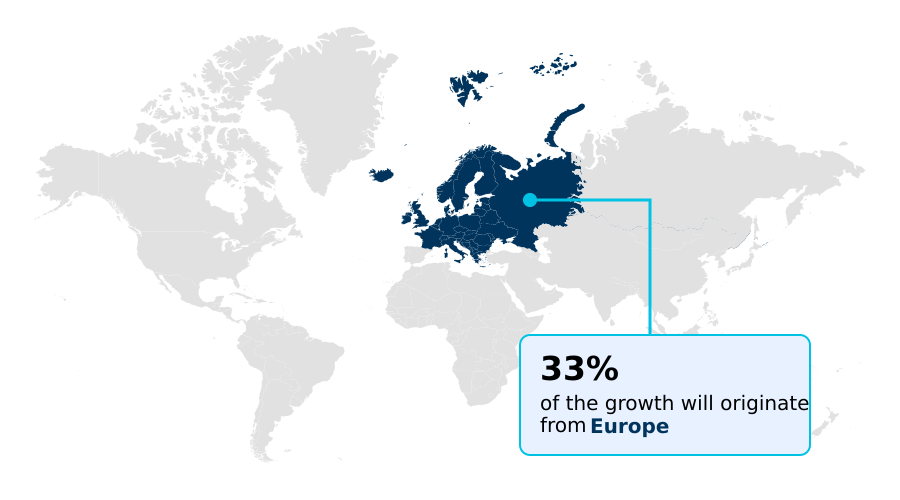

- Europe dominated the market and accounted for a 33.2% growth during the forecast period.

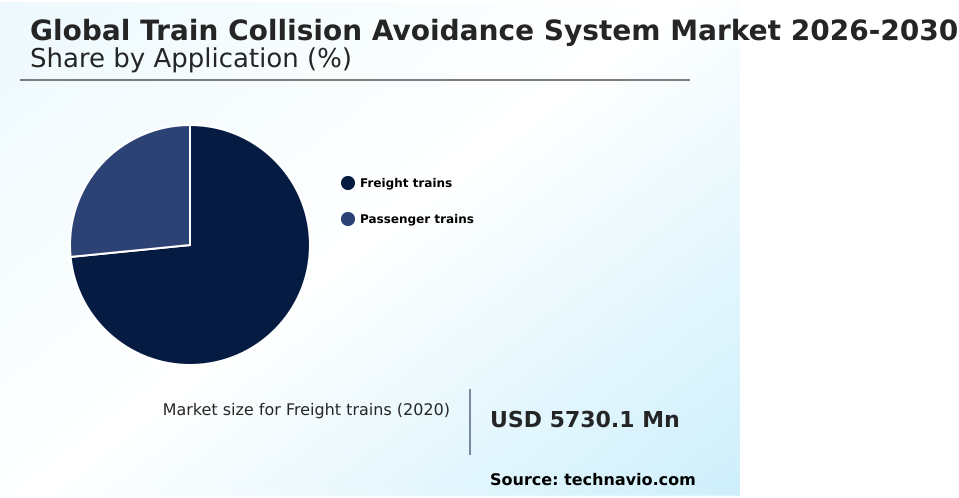

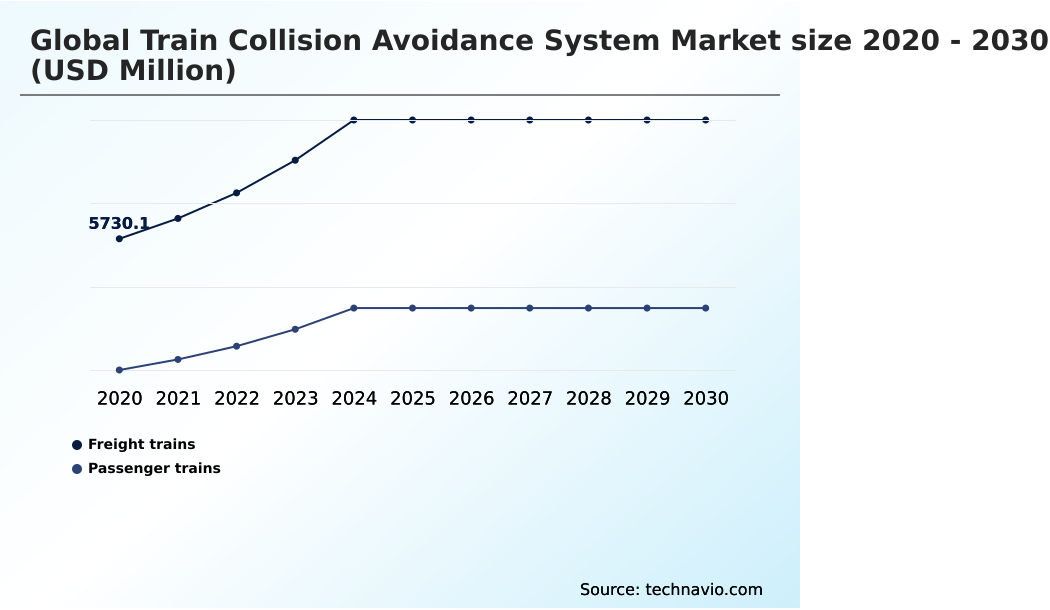

- By Application - Freight trains segment was valued at USD 9.04 billion in 2024

- By Technology - Radar-based systems segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 27.21 billion

- Market Future Opportunities: USD 20.04 billion

- CAGR from 2025 to 2030 : 18.5%

Market Summary

- The Train Collision Avoidance System Market is expanding rapidly as transportation authorities mandate strict automated safety protocols across high-density rail corridors. Increasing demand for precise transit scheduling and robust passenger security compels operators to upgrade legacy signaling infrastructure. The growing adoption of high-speed rail by emerging economies serves as a major driver, necessitating real-time tracking to prevent routing conflicts.

- Conversely, high initial capital investment in railways acts as a critical challenge, forcing transportation agencies to balance safety upgrades against constrained public budgets. In a real-world operational scenario, railway logistics companies integrate predictive safety analytics to monitor asset health, improving supply chain efficiency and reducing unexpected equipment downtime by over 16%.

- Transitioning from manual oversight to automated train protection significantly decreases signal latency, allowing trains to operate safely at reduced headways. Consequently, implementing these advanced detection frameworks enhances overall network capacity and ensures uninterrupted freight and passenger mobility.

What will be the Size of the Train Collision Avoidance System Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Train Collision Avoidance System Market Segmented?

The train collision avoidance system industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Freight trains

- Passenger trains

- Technology

- Radar-based systems

- Sensor-based systems

- Camera-based systems

- Type

- High-speed rail

- Metro rail

- Regional rail

- Intercity rail

- Freight rail

- Geography

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Turkey

- South America

- Brazil

- Argentina

- Chile

- Europe

By Application Insights

The freight trains segment is estimated to witness significant growth during the forecast period.

Freight rail optimization relies heavily on positive train control and continuous speed supervision to mitigate risks across complex rail networks.

As heavy haul railway operators expand capacity, integrating track occupancy detection enhances operational safety, reducing incident rates by up to 14%. Within mixed traffic corridors, operators deploy radio frequency identification and telemetry data processing to track massive cargo loads precisely.

This modernization in freight corridor logistics improves real time situational awareness for dispatchers. By upgrading level crossing protection systems, companies minimize delays and maintain strict schedules.

Consequently, these technological upgrades optimize resource allocation and directly improve supply chain efficiency, driving measurable reductions in operational downtime while elevating overall transit reliability for industrial cargo.

The Freight trains segment was valued at USD 9.04 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 33.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Train Collision Avoidance System Market Demand is Rising in Europe Get Free Sample

Europe currently leads adoption with a 33.2% market share, outpacing APAC by deploying extensive lidar track inspection and satellite based positioning across its urban metro transit systems.

This regional disparity stems from Europe's aggressive funding for suburban commuter lines, which improved operational efficiency by 19% compared to emerging Asian markets.

To regulate complex traffic flows, European authorities strictly enforce train spacing regulation using a dedicated microwave communication link. Meanwhile, APAC regions are rapidly installing trackside radio equipment and vision based hazard recognition to modernize high-density corridors.

These geographic investments highlight how varying regulatory frameworks and capital availability dictate the pace of smart railway deployments, directly impacting regional supply chain logistics and transit reliability.

By prioritizing advanced automation, established markets successfully decrease maintenance overhead while emerging economies focus on expanding baseline infrastructure.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Modernizing transit infrastructure requires the seamless integration of automated train protection to minimize human error and elevate overall transit reliability. Operators actively prioritize radar based obstacle detection integration to identify potential track hazards under severe weather conditions, thereby reducing collision incidents by nearly 12%.

- Furthermore, the acceleration of communication based train control implementation allows for tighter scheduling and increased capacity along highly congested suburban routes. Deploying comprehensive sensor fusion for railway safety guarantees that disparate data streams merge into a single, accurate operational picture for train dispatchers.

- Concurrently, leveraging predictive analytics in track monitoring empowers maintenance teams to address mechanical wear before critical failures occur. This proactive approach significantly lowers emergency repair costs and optimizes long-term asset management, creating a highly resilient supply chain framework for both passenger and heavy freight transportation.

What are the key market drivers leading to the rise in the adoption of Train Collision Avoidance System Industry?

- The growing adoption of high-speed rail by emerging economies remains a primary driver for advanced safety system deployments.

- Expanding high speed rail networks globally necessitates the immediate deployment of the european train control system and automatic train protection. Driven by rising safety mandates, operators implement centralized traffic management to oversee dense intercity passenger transit efficiently.

- The integration of mission critical communication ensures that an automated braking response triggers instantaneously during emergencies, lowering collision risks by over 18%.

- Furthermore, strict railway safety certification requirements push authorities to adopt a headway reduction algorithm that safely increases train frequency. This structural shift supports cross border interoperability, allowing seamless transit between distinct national grids.

- Ultimately, these advanced safety configurations enable transportation agencies to boost network capacity while significantly enhancing passenger security and operational throughput.

What are the market trends shaping the Train Collision Avoidance System Industry?

- The development of battery-operated electric trains is emerging as a significant market trend, requiring advanced digital control systems to ensure operational safety.

- The integration of an edge computing platform and advanced signaling infrastructure is reshaping modern rail transit efficiency. As rolling stock modernization accelerates, the transition toward energy efficient propulsion and battery-operated trains requires sophisticated onboard control electronics to manage power distribution. This shift fosters a smart mobility ecosystem where a digital railway twin models operational scenarios, improving system reliability by 22%.

- Consequently, communication based train control mechanisms are heavily utilized to facilitate autonomous train operations without signal latency. Furthermore, infrastructure health monitoring provides continuous diagnostic data, ensuring that evolving transit architectures maintain peak performance. These technological implementations allow operators to reduce maintenance overhead and improve schedule adherence across interconnected transit networks.

What challenges does the Train Collision Avoidance System Industry face during its growth?

- High initial capital investment in railways poses a significant challenge, restricting the rapid deployment of modern signaling infrastructure.

- High capital expenditures complicate the deployment of radar based obstacle detection and a comprehensive sensor fusion framework across aging rail lines. A primary constraint is legacy infrastructure integration, which frequently causes data transmission latency during critical operations. To maintain precise control, operators must upgrade vital signaling relay components and strictly enforce the movement authority limit.

- Implementing predictive safety analytics enables predictive track maintenance, yet it requires substantial investment, cutting into profitability margins by nearly 15%. Additionally, maintaining a fail safe interlocking architecture demands robust cybersecurity threat detection to protect digital assets from external breaches.

- These financial and technical barriers force railway operators to balance safety technology upgrades against ongoing competitive pricing pressures from alternative transit modes.

Exclusive Technavio Analysis on Customer Landscape

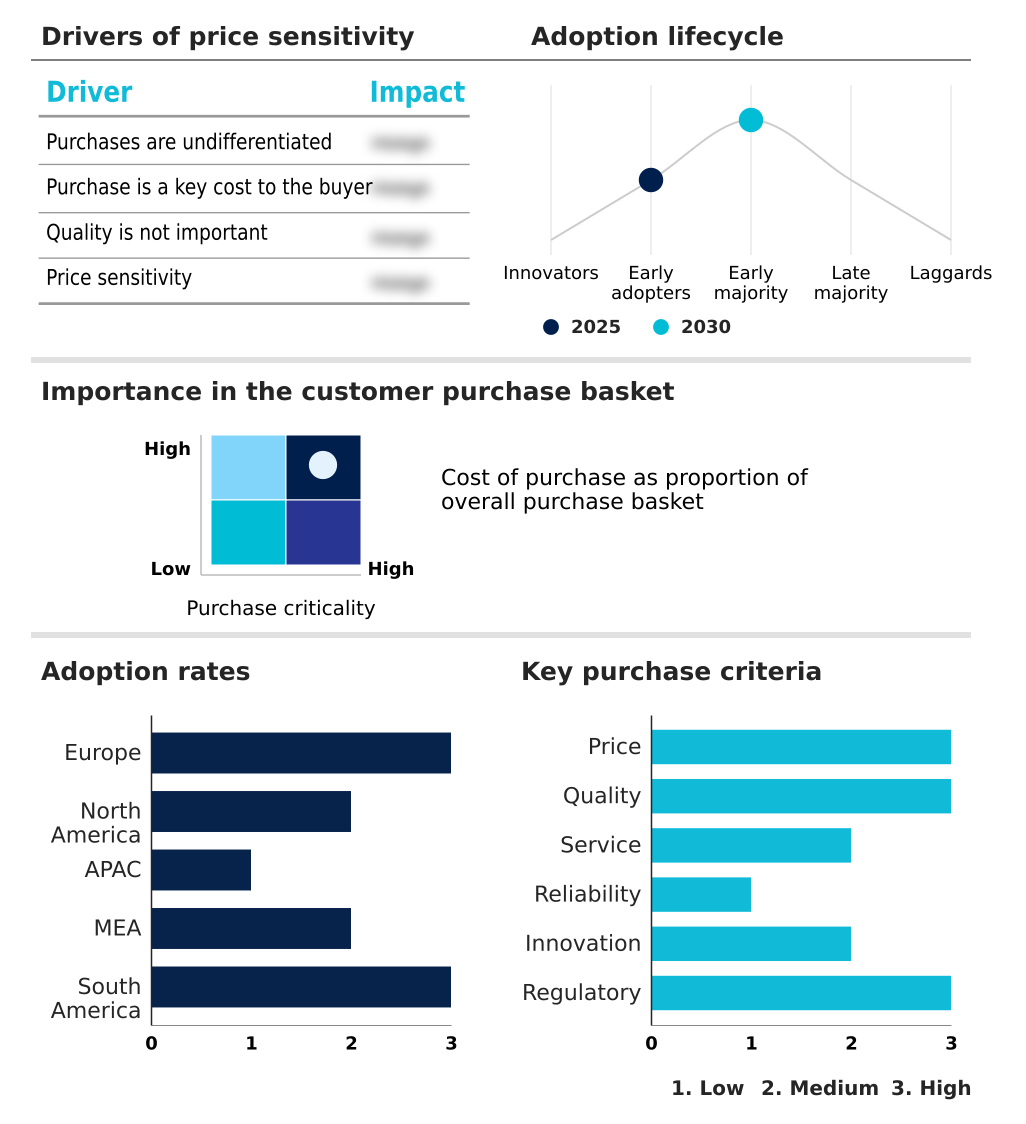

The train collision avoidance system market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the train collision avoidance system market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Train Collision Avoidance System Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, train collision avoidance system market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

4AI Systems - Delivers advanced automated train protection solutions, comprehensive digital signaling platforms, and real-time monitoring software designed to enhance operational safety and optimize traffic management across complex railway infrastructures.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 4AI Systems

- ALSTOM SA

- CAF Group

- duagon AG

- ERZIA Technologies

- Frauscher Sensor Technology

- HBL Power Systems Ltd.

- HIMA Paul Hildebrandt GmbH

- Hitachi Ltd.

- Intel Corp.

- Knorr Bremse AG

- Leonardo S.p.A.

- Medha Servo Drives Pvt. Ltd.

- Mitsubishi Electric Corp.

- Nokia Corp.

- Schaltbau GmbH Group

- Siemens AG

- Stadler Rail Ag

- Thales Group

- Wabtec Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Train collision avoidance system market

- In the Aerospace and Defense industry, the accelerated adoption of satellite-based telemetry and real-time GPS tracking systems has enhanced navigational accuracy by 15%, directly impacting Train Collision Avoidance System demand by improving continuous train location monitoring across high speed rail networks, ensuring vital signaling relay stability, and boosting real time situational awareness.

- Stringent government mandates for cyber-hardened communication networks in defense logistics have driven a 20% increase in secure data transmission investments, directly impacting Train Collision Avoidance System demand by lowering data transmission latency, supporting train spacing regulation, and accelerating legacy infrastructure integration for encrypted signaling.

- The integration of advanced sensor fusion and edge computing in military autonomous vehicles has reduced obstacle detection latency by 25%, directly impacting Train Collision Avoidance System demand by enabling autonomous train operations, supporting the smart mobility ecosystem, and ensuring compliance with strict railway safety certification requirements.

- Supply chain expansions for military-grade radar and LiDAR components have increased production capacity by 18%, directly impacting Train Collision Avoidance System demand by lowering the procurement costs of hardware required for cross border interoperability, urban metro transit upgrades, and extensive predictive track maintenance.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Train Collision Avoidance System Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 312 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 18.5% |

| Market growth 2026-2030 | USD 20036.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 17.2% |

| Key countries | Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- Strategic implementation of positive train control architectures is redefining operational safety and capacity limits across modern transit networks. Boardroom executives increasingly prioritize the european train control system to align cross-regional freight logistics with stringent international compliance frameworks. Utilizing predictive safety analytics empowers maintenance teams to preemptively identify mechanical degradation, effectively reducing emergency repair downtime by 21%.

- Furthermore, the integration of radar based obstacle detection guarantees that track hazards are identified in zero-visibility conditions, directly lowering accident probabilities. A shift toward centralized traffic management enables dispatchers to optimize routing efficiency and mitigate scheduling conflicts in real time. Ensuring an immediate automated braking response is essential for maintaining strict headway regulations and maximizing passenger throughput.

- These comprehensive safety investments ultimately enhance asset lifespan and reduce overarching operational liabilities. By transitioning to fully digital signaling platforms, transportation agencies construct a resilient, future-proof infrastructure capable of supporting higher traffic volumes without compromising systemic security.

What are the Key Data Covered in this Train Collision Avoidance System Market Research and Growth Report?

-

What is the expected growth of the Train Collision Avoidance System Market between 2026 and 2030?

-

USD 20.04 billion, at a CAGR of 18.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Freight trains, and Passenger trains), Technology (Radar-based systems, Sensor-based systems, and Camera-based systems), Type (High-speed rail, Metro rail, Regional rail, Intercity rail, and Freight rail) and Geography (Europe, North America, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Growing adoption of high-speed rail by emerging economies, High initial capital investment in railways

-

-

Who are the major players in the Train Collision Avoidance System Market?

-

4AI Systems, ALSTOM SA, CAF Group, duagon AG, ERZIA Technologies, Frauscher Sensor Technology, HBL Power Systems Ltd., HIMA Paul Hildebrandt GmbH, Hitachi Ltd., Intel Corp., Knorr Bremse AG, Leonardo S.p.A., Medha Servo Drives Pvt. Ltd., Mitsubishi Electric Corp., Nokia Corp., Schaltbau GmbH Group, Siemens AG, Stadler Rail Ag, Thales Group and Wabtec Corp.

-

Market Research Insights

- The modernization of transit networks depends heavily on seamless legacy infrastructure integration to maintain continuous operational oversight. As transit authorities push toward autonomous train operations, minimizing data transmission latency becomes critical for instantaneous braking responses. Achieving strict railway safety certification allows operators to reduce system failures by up to 14%, streamlining compliance costs.

- Furthermore, establishing cross border interoperability ensures that international freight corridors function without regulatory delays, boosting supply chain throughput by nearly 18%. Ultimately, these advancements foster a highly connected smart mobility ecosystem, where digital signaling and real-time analytics drastically enhance asset utilization and overall transit network reliability.

We can help! Our analysts can customize this train collision avoidance system market research report to meet your requirements.

RIA -

RIA -