Unified Communication As A Service (UCaaS) Market Size 2025-2029

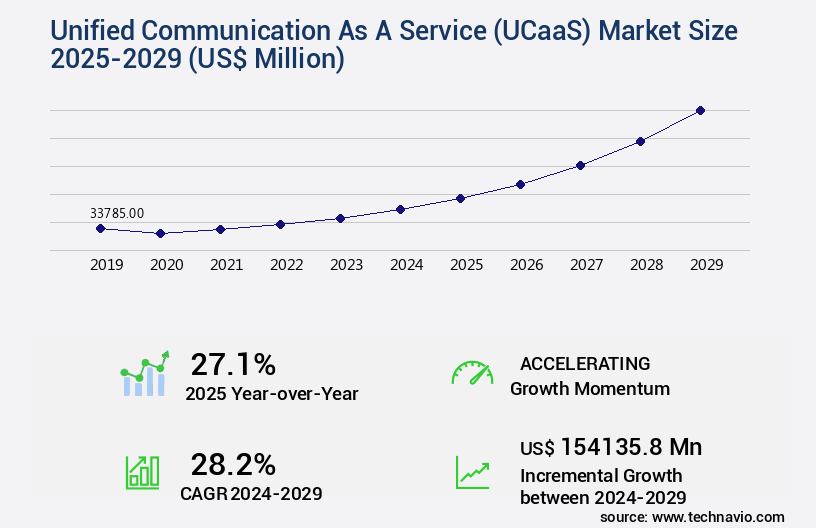

The unified communication as a service (UCaaS) market size is valued to increase USD 154.14 billion, at a CAGR of 28.2% from 2024 to 2029. Increased adoption of cloud-based services will drive the unified communication as a service (UCaaS) market.

Major Market Trends & Insights

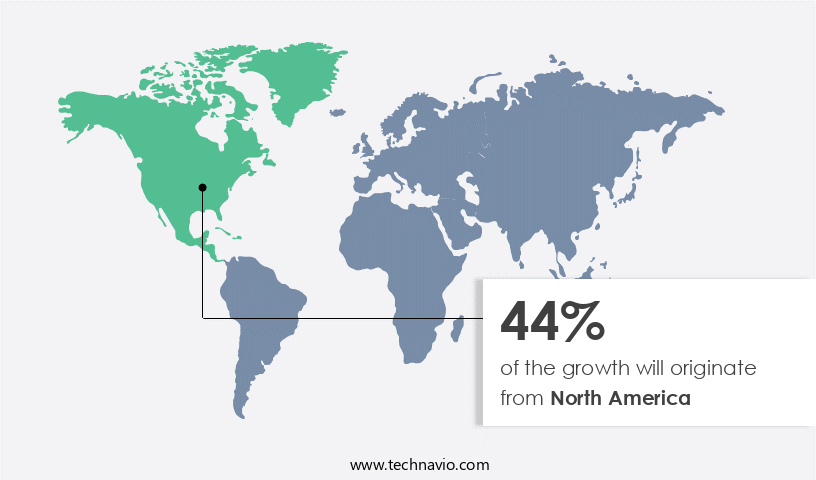

- North America dominated the market and accounted for a 44% growth during the forecast period.

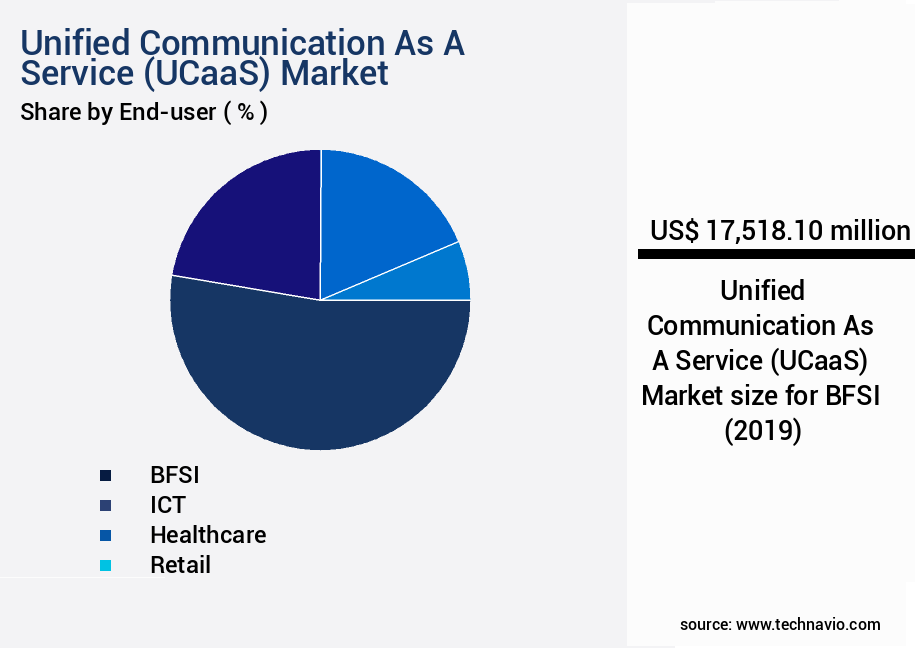

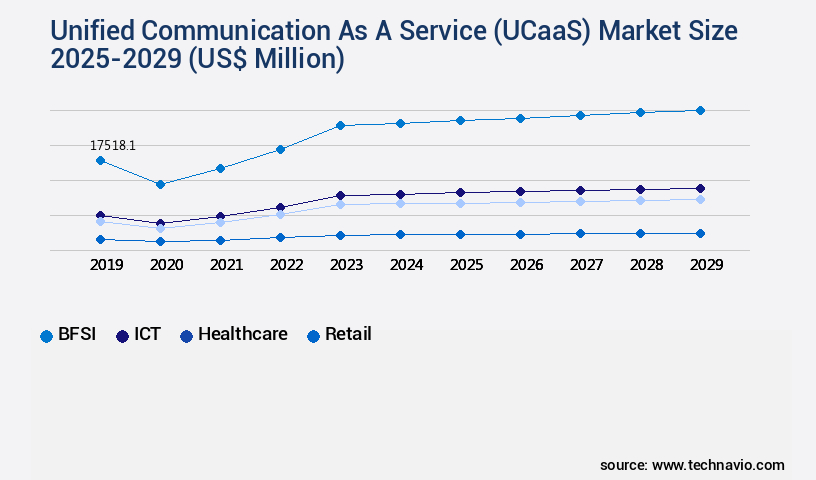

- By End-user - BFSI segment was valued at USD 17.52 billion in 2023

- By Application - Enterprise collaboration segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 541.64 million

- Market Future Opportunities: USD 154135.80 million

- CAGR from 2024 to 2029 : 28.2%

Market Summary

- The market represents a dynamic and continually evolving landscape, driven by the increasing adoption of cloud-based services and the proliferation of Bring Your Own Device (BYOD) and mobility trends. According to recent reports, the UCaaS market is expected to account for over 60% of the total enterprise communications market by 2025. This shift towards cloud-based solutions is fueled by the benefits they offer, including cost savings, scalability, and flexibility. However, challenges persist, with user training and adoption emerging as significant hurdles. Regulations, such as the General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA), also pose challenges for UCaaS providers and their clients.

- Core technologies, including Voice over IP (VoIP), video conferencing, and instant messaging, continue to evolve, while applications, such as team collaboration and contact center solutions, are gaining traction. The UCaaS market is a vibrant and ever-changing ecosystem, offering numerous opportunities for innovation and growth.

What will be the Size of the Unified Communication As A Service (UCaaS) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Unified Communication As A Service (UCaaS) Market Segmented ?

The unified communication as a service (UCaaS) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- BFSI

- ICT

- Healthcare

- Retail

- Others

- Application

- Enterprise collaboration

- Enterprise telephony

- Contact center

- Deployment

- Public cloud

- Private cloud

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By End-user Insights

The BFSI segment is estimated to witness significant growth during the forecast period.

The market expansion in the BFSI sector is fueled by the digitalization of core processes and the generation of vast data volumes. UCaaS adoption has become increasingly popular among BFSI organizations due to its potential to minimize IT expenditures and ensure regulatory compliance. Call detail records, video conferencing APIs, and contact center software are integral components of UCaaS solutions. Service level agreements, SIP trunking services, and instant messaging features provide businesses with reliable and efficient communication channels. Session border controllers, screen sharing capabilities, and unified messaging systems enhance collaboration and productivity. Scalability design, voicemail to email, packet loss analysis, media gateways, network security protocols, and collaboration tools enable seamless communication and data sharing.

The BFSI segment was valued at USD 17.52 billion in 2019 and showed a gradual increase during the forecast period.

WebRTC technology, mobile device integration, and call routing protocols facilitate real-time communication across various platforms. The UCaaS market in the BFSI sector is expected to grow significantly, with an estimated 30% of organizations planning to adopt UCaaS solutions in the next two years. Moreover, the market is projected to expand at a steady pace, with approximately 25% of BFSI companies planning to increase their UCaaS investments in the coming year. To ensure business continuity and disaster recovery, UCaaS solutions offer features like software-defined networking, data encryption methods, presence and availability, and latency measurements. Cloud telephony, file sharing services, user experience testing, VoIP infrastructure, bandwidth optimization, jitter reduction techniques, and compliance certifications further enhance the value proposition of UCaaS solutions in the BFSI sector.

Regional Analysis

North America is estimated to contribute 44% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Unified Communication As A Service (UCaaS) Market Demand is Rising in North America Request Free Sample

Unified Communication as a Service (UCaaS) has seen significant growth in the North American market, with the US leading the charge. Factors contributing to this expansion include the presence of numerous large enterprises, the availability of advanced broadband networking, and the increasing number of hosted servers. The Bring Your Own Device (BYOD) model has been a major cost-saving measure for businesses, enabling them to implement UCaaS solutions more widely.

Enterprise spending on cloud-based UC systems for collaboration and telephony services is on the rise, reflecting the growing importance of effective communication tools in today's business landscape. UCaaS adoption is increasingly popular among US businesses, as they recognize the benefits of streamlined, flexible, and cost-effective communication solutions.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is a dynamic and evolving landscape that offers businesses advanced VoIP systems and real-time communication solutions. Scalability challenges are a primary concern as organizations seek to accommodate growing user bases and increasing traffic demands. Contact center agent performance metrics are crucial, with security best practices in cloud telephony emerging as a top priority. UCaaS solutions encompass unified messaging system integration, enabling seamless communication across various channels. Real-time communication latency optimization is essential for maintaining efficient and effective interactions. APIs are increasingly integrated with CRM systems to streamline workflows and enhance customer experiences. WebRTC application development frameworks and session border controller security configurations are essential for securing UCaaS environments.

Sip trunking cost optimization strategies are a significant focus, as are multi-tenant architecture deployments for accommodating multiple clients on a single infrastructure. Call routing protocol configurations and media gateway bandwidth management are vital for ensuring high-quality communication. Interactive voice response design best practices and voicemail to email notification systems improve user experience and productivity. Instant messaging encryption methods and file sharing security protocols ensure data privacy. Screen sharing performance optimization and mobile device application security are essential for accommodating remote workforces and diverse devices. Network security protocols deployment and data encryption methods compliance are critical for maintaining robust security.

Service level agreement performance monitoring is a key performance indicator, with more than 80% of enterprises prioritizing reliability and uptime over cost savings. This comparative data underscores the importance of UCaaS solutions in addressing the complex communication needs of modern businesses.

What are the key market drivers leading to the rise in the adoption of Unified Communication As A Service (UCaaS) Industry?

- The significant rise in the utilization of cloud-based services serves as the primary catalyst for market growth.

- Cloud adoption among businesses has witnessed substantial growth, with cloud-based Unified Communications (UC) leading the charge. This trend is driven by the increasing preference for enterprise mobility and Bring Your Own Device (BYOD) policies. Enterprises are transitioning from on-premises UC systems to Software-as-a-Service (SaaS) solutions, enabling agile communications infrastructure. This shift eliminates the need for businesses to invest in hardware and software maintenance. The flexibility offered by the as-a-service model is another key factor, enabling businesses to scale their user base as needed.

- Moreover, the risk of technological obsolescence associated with on-premises solutions is minimized, making cloud UC a preferred choice for modern enterprises.

What are the market trends shaping the Unified Communication As A Service (UCaaS) Industry?

- The increasing trend in the market involves the wider adoption of Bring Your Own Device (BYOD) policies and mobility solutions.

- In today's business landscape, the Bring Your Own Device (BYOD) model has gained significant traction, empowering employees to utilize their personal devices in professional settings. This trend is fueled by the growing preference for user convenience, the increasing use of mobile devices, and the expansion of mobile workforces. Mobility is a crucial strategy employed by businesses to boost productivity, flexibility, agility, and cost savings. Unified Communications as a Service (UCaaS) adoption is on the rise due to the widespread use of smartphones, which facilitate mobility within organizations.

- UCaaS enables faster communication within enterprises, minimizes latency, and enhances overall business efficiency. The integration of mobility into UC offers numerous benefits, including real-time collaboration, seamless communication, and improved employee engagement. As a professional, it is essential to recognize the significance of this trend and adapt to the evolving needs of the market.

What challenges does the Unified Communication As A Service (UCaaS) Industry face during its growth?

- User training and adoption present significant challenges that can hinder industry growth. These challenges must be addressed effectively to ensure the successful implementation and utilization of new technologies or systems.

- In the dynamic and evolving market, the integration of advanced communication tools into organizations often faces resistance from employees due to unfamiliarity or apprehension towards change. This reluctance can adversely impact productivity and collaboration. To mitigate this challenge, companies must prioritize comprehensive training programs that empower employees with the necessary skills to effectively utilize these solutions. By emphasizing the benefits of UCaaS, such as enhanced flexibility and improved communication efficiency, organizations can foster a positive attitude towards these technologies and ultimately reap the rewards of a more connected and productive workforce.

- UCaaS adoption continues to gain traction across various sectors, with businesses recognizing the importance of streamlined communication systems to remain competitive. By addressing employee concerns and ensuring a smooth transition, companies can successfully leverage UCaaS to drive growth and innovation.

Exclusive Technavio Analysis on Customer Landscape

The unified communication as a service (UCaaS) market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the unified communication as a service (UCaaS) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Unified Communication As A Service (UCaaS) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, unified communication as a service (UCaaS) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

8x8 Inc. - The company delivers Unified Communications as a Service, including the 8x8 UC platform, catering to businesses seeking streamlined communication solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 8x8 Inc.

- ALE International

- AT and T Inc.

- Avaya LLC

- BroadSoft Inc.

- BT Group Plc

- Microsoft Corp.

- Mitel Networks Corp.

- NEC Corp.

- NTT Communications Corp.

- Oracle Corp.

- Orange SA

- PanTerra Networks Inc.

- RingCentral Inc.

- Sify Technologies Ltd.

- Tata Sons Pvt. Ltd.

- Telefonica SA

- Telstra Corp. Ltd.

- Verizon Communications Inc.

- Vonage Holdings Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Unified Communication As A Service (UCaaS) Market

- In January 2024, Microsoft Teams announced the integration of Calling for Education, a new UCaaS solution tailored for the educational sector, allowing students and teachers to communicate via voice, video, and chat (Microsoft Press Release).

- In March 2024, RingCentral and Google Cloud entered into a strategic partnership, enabling RingCentral's UCaaS services to be integrated with Google Workspace (RingCentral Press Release).

- In May 2024, Cisco Systems completed the acquisition of IMImobile, a leading provider of cloud communications software, to strengthen its UCaaS offerings and expand its presence in the global communications market (Cisco Press Release).

- In February 2025, Avaya Holdings Corp. revealed the launch of Avaya OneCloud XC, a UCaaS platform designed for midmarket and enterprise businesses, featuring advanced capabilities like AI and automation (Avaya Press Release).

- These developments demonstrate significant advancements in the UCaaS market, with companies expanding their offerings, forming strategic partnerships, and making acquisitions to cater to various sectors and enhance their technology.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Unified Communication As A Service (UCaaS) Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

228 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 28.2% |

|

Market growth 2025-2029 |

USD 154135.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

27.1 |

|

Key countries |

US, China, Canada, Germany, UK, France, India, Brazil, Japan, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- Unified Communication as a Service (UCaaS) continues to reshape business communication landscapes, with key components driving its evolution. Call Detail Records (CDRs) offer invaluable insights for call analytics, enabling businesses to optimize their communication strategies. Video Conferencing APIs facilitate seamless integration of video conferencing into various applications, fostering real-time collaboration. Service Level Agreements (SLAs) ensure reliable UCaaS performance, while Contact Center Software enhances customer engagement through advanced features. SIP Trunking Services provide cost-effective alternatives to traditional phone lines, and Instant Messaging Features foster quick, asynchronous communication. Session Border Controllers secure UCaaS networks, and Screen Sharing Capabilities enable remote assistance and collaboration.

- Unified Messaging Systems offer a centralized messaging platform, and Scalability Design ensures UCaaS can accommodate growing businesses. Voicemail to Email and Packet Loss Analysis improve communication efficiency and network performance. Media Gateways bridge the gap between VoIP and traditional phone systems, and Network Security Protocols protect UCaaS from cyber threats. Collaboration Tools, powered by WebRTC Technology and Mobile Device Integration, enable anytime, anywhere communication. Call Routing Protocols optimize call handling, and Real-Time Communication ensures immediate interaction. Multi-Tenant Architecture caters to multiple clients, and Interactive Voice Response streamlines customer interactions. Software Defined Networking, Data Encryption Methods, Presence and Availability, Disaster Recovery Planning, Latency Measurements, Cloud Telephony, File Sharing Services, User Experience Testing, VoIP Infrastructure, Bandwidth Optimization, and Jitter Reduction Techniques are all integral components of UCaaS, continually enhancing business communication capabilities.

What are the Key Data Covered in this Unified Communication As A Service (UCaaS) Market Research and Growth Report?

-

What is the expected growth of the Unified Communication As A Service (UCaaS) Market between 2025 and 2029?

-

USD 154.14 billion, at a CAGR of 28.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (BFSI, ICT, Healthcare, Retail, and Others), Application (Enterprise collaboration, Enterprise telephony, and Contact center), Deployment (Public cloud and Private cloud), and Geography (North America, APAC, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increased adoption of cloud-based services, Challenges with user training and adoption

-

-

Who are the major players in the Unified Communication As A Service (UCaaS) Market?

-

8x8 Inc., ALE International, AT and T Inc., Avaya LLC, BroadSoft Inc., BT Group Plc, Microsoft Corp., Mitel Networks Corp., NEC Corp., NTT Communications Corp., Oracle Corp., Orange SA, PanTerra Networks Inc., RingCentral Inc., Sify Technologies Ltd., Tata Sons Pvt. Ltd., Telefonica SA, Telstra Corp. Ltd., Verizon Communications Inc., and Vonage Holdings Corp.

-

Market Research Insights

- Unified Communications as a Service (UCaaS) market encompasses a range of business communication solutions delivered over the internet. According to recent estimates, the global UCaaS market size is projected to reach USD 120 billion by 2026. This expansion is driven by the increasing demand for remote workforce solutions, advanced performance monitoring, and change management capabilities. In contrast, traditional on-premise communication systems have a smaller market size, estimated at USD 35 billion in 2021.

- The UCaaS market's significant growth can be attributed to its ability to offer features such as authorization mechanisms, API integrations, network management tools, user authentication, and security features, among others. These advanced capabilities enable businesses to enhance their communication systems, improve productivity, and ensure business continuity.

We can help! Our analysts can customize this unified communication as a service (UCaaS) market research report to meet your requirements.

RIA -

RIA -