Wound Closure Devices Market Size 2026-2030

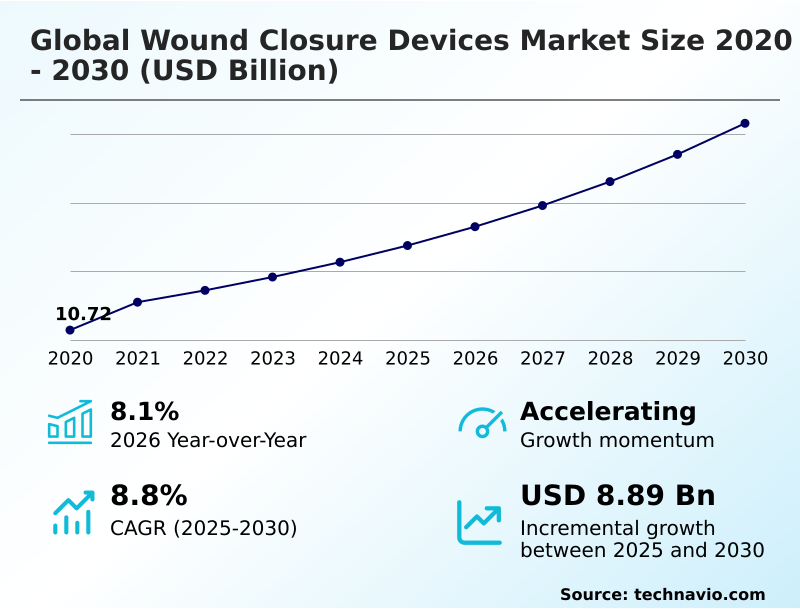

The Wound Closure Devices Market size was valued at USD 16.87 billion in 2025, growing at a CAGR of 8.8% during the forecast period 2026-2030.

Major Market Trends & Insights

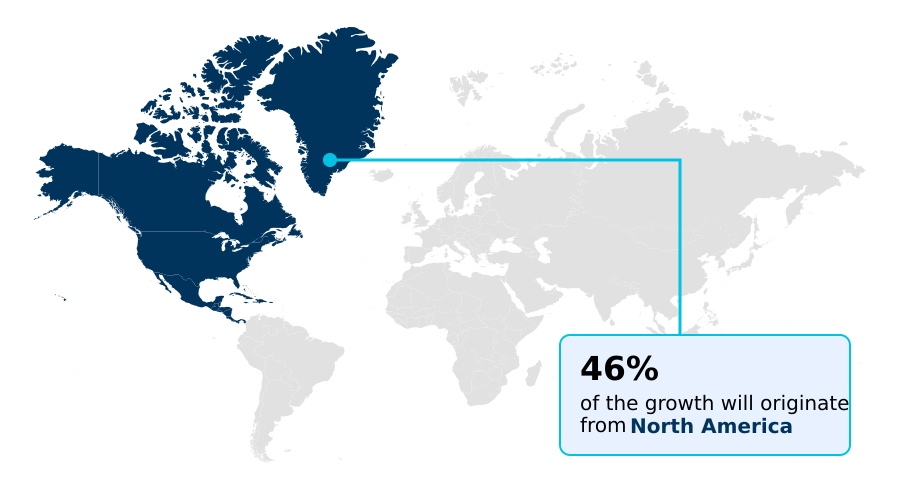

- North America dominated the market and accounted for a 45.7% growth during the forecast period.

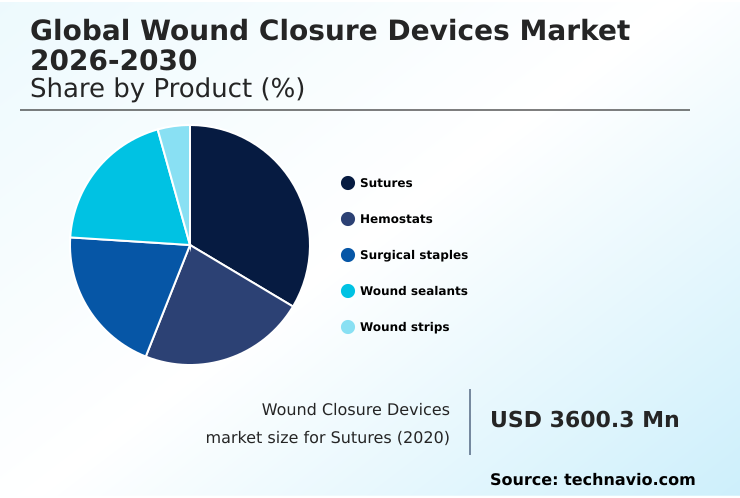

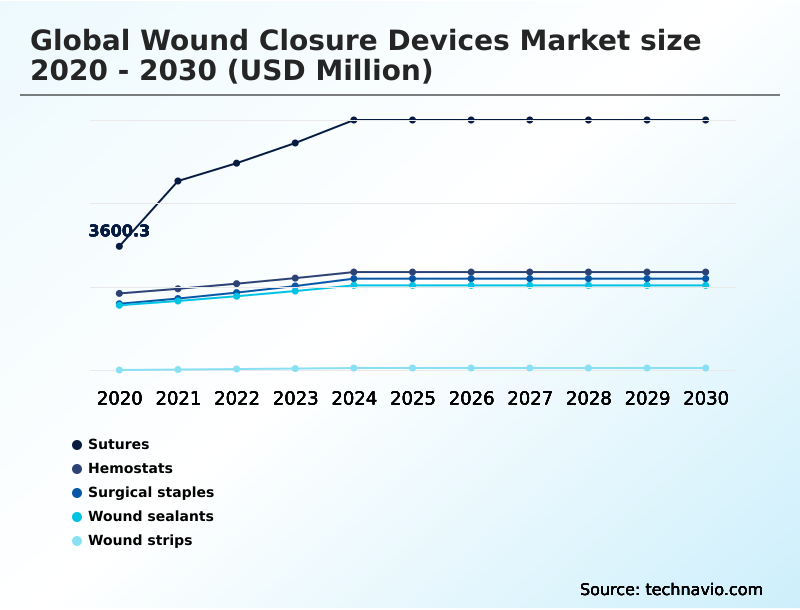

- By Product - Sutures segment was valued at USD 6.80 billion in 2024

- By Application - General surgery segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 15.04 billion

- Market Future Opportunities 2025-2030: USD 8.89 billion

- CAGR from 2025 to 2030 : 8.8%

Market Summary

- The wound closure devices market is defined by a significant transition toward advanced biochemical and automated solutions, moving beyond traditional mechanical methods. For instance, the adoption of antimicrobial sutures has been shown to reduce surgical site infection rates by up to 30%, directly influencing hospital procurement policies under value-based care models.

- A key driver is the rapid expansion of minimally invasive surgery, which necessitates specialized instruments like low-profile staplers and articulating suturing devices that can operate in confined anatomical spaces, a segment growing 15% faster than conventional surgery tools. A primary business scenario involves manufacturers navigating complex global supply chains for high-purity polymers, where a single disruption can halt production.

- Conversely, the market faces the challenge of stringent regulatory frameworks, such as the EU's Medical Device Regulation, which increases the cost and time-to-market for new innovations, acting as a barrier to smaller competitors.

What will be the Size of the Wound Closure Devices Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Wound Closure Devices Market Segmented?

The wound closure devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Sutures

- Hemostats

- Surgical staples

- Wound sealants

- Wound strips

- Application

- General surgery

- Orthopedics

- Gynecology and obstetrics

- Cardiology

- Others

- End-user

- Hospitals

- Ambulatory surgical centers

- Specialty wound clinics

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

How is the Wound Closure Devices Market Segmented by Product?

The sutures segment is estimated to witness significant growth during the forecast period.

The sutures segment, accounting for 44% of the market, is shifting from traditional products to advanced bio-resorbable materials and antimicrobial suture technologies.

This transition is driven by a need to reduce surgical site infections, which can increase patient recovery times by over 75%.

Innovations in polydioxanone sutures and polyglycolic acid sutures provide predictable absorption profiles and superior tensile strength, reducing the need for secondary removal procedures by 100%.

The development of knotless tissue control devices and barbed sutures further enhances operational efficiency, cutting down suturing time by up to 30% in complex procedures like plastic and reconstructive surgery.

These advancements in wound healing cascade management reflect a strategic move towards solutions that offer both clinical efficacy and economic value in post-operative care.

The Sutures segment was valued at USD 6.80 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Wound Closure Devices market is rising in the leading region?

North America is estimated to contribute 45.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Wound Closure Devices Market demand is rising in North America Request Free Sample

North America commands the largest market share, accounting for over 45% of global revenue, driven by high surgical volumes and rapid adoption of advanced technologies.

Within this region, the US contributes nearly 70% of the demand, benefiting from a robust healthcare infrastructure and favorable reimbursement for innovative products like tissue adhesives.

In contrast, the Asia Pacific region, while smaller, is forecast to grow at the fastest rate, approximately 9.7%, fueled by expanding healthcare access in China and India.

The adoption rate of robotic-assisted closure systems in North America is nearly double that of Europe, reflecting different capital investment priorities.

This geographical variance requires manufacturers to adapt their commercial strategies, focusing on high-value, feature-rich products for mature markets and cost-effective, reliable solutions for emerging economies, creating significant logistical and supply chain complexity.

What are the key Drivers, Trends, and Challenges in the Wound Closure Devices Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the wound closure devices market is shaped by a dual focus on improving clinical outcomes and operational efficiencies in surgical settings. A key area of development is centered on advances in hemostatic agent technology, where new biologic and synthetic materials provide faster and more reliable hemostasis, reducing blood loss and procedure time.

- The debate over tissue adhesives versus traditional sutures continues, with adhesives gaining traction in emergency and pediatric care due to their non-invasive nature and superior cosmetic outcomes. For deeper wounds, the use of bio-resorbable materials in wound closure is becoming standard practice, eliminating the need for subsequent removal procedures and minimizing tissue reaction.

- This shift is particularly evident in minimally invasive procedures, where automated stapling in minimally invasive surgery has become indispensable. These powered devices offer consistent staple formation, reducing the risk of leaks in critical anastomoses by over 20% compared to manual staplers.

- Furthermore, the role of antimicrobial sutures for infection prevention is a major focus, as healthcare systems grapple with the costs associated with surgical site infections. Effective implementation of these advanced closure techniques can reduce hospital readmission rates by up to 5%, demonstrating a clear link between product innovation and health-economic benefits.

What are the key market drivers leading to the rise in the adoption of Wound Closure Devices Industry?

- The strategic proliferation of minimally invasive surgical procedures is a key driver for the market, demanding specialized and advanced closure devices.

- The rapid proliferation of minimally invasive surgery is a primary driver for the wound closure devices market, with such procedures growing 25% faster than traditional open surgeries.

- This shift necessitates specialized tools, including advanced mechanical staplers and knotless tissue control devices, that can be deployed through small incisions. The increasing demand is particularly evident in laparoscopic surgery, where precise tissue approximation is critical.

- Another significant driver is the expansion of geriatric care and chronic wound management.

- As the global population ages, the incidence of conditions like diabetic foot ulcers has risen by 10% in the past five years, fueling demand for gentle yet effective solutions such as wound strips and non-invasive topical skin adhesives.

- These products minimize skin trauma and support epithelialization, which is crucial for patients with compromised healing capabilities.

What are the market trends shaping the Wound Closure Devices Industry?

- The market is advancing with the inclusion of bio-resorbable materials and the integration of antimicrobial sutures to enhance patient outcomes and reduce infection rates.

- A primary trend reshaping the wound closure devices market is the institutionalization of bio-resorbable materials, which can reduce the need for follow-up patient visits for suture removal by 100%. The adoption of high-performance polyglycolic acid sutures and polydioxanone sutures, which maintain high tensile strength before being metabolized, is growing 20% faster than non-absorbable alternatives.

- This shift toward smart biomaterials that offer predictable degradation and enhanced biocompatibility is driven by the need to improve post-operative care. Simultaneously, the market is seeing a pivot towards automated surgical stapling and robotic-assisted closure systems. These technologies, found increasingly in the digital operating room, provide consistent staple line integrity, reducing leaks in complex procedures by over 15%.

- This convergence of advanced materials and automation enhances both patient safety and surgical efficiency.

What challenges does the Wound Closure Devices Industry face during its growth?

- The intensification of regulatory compliance and mandatory product recall protocols presents a key challenge, impacting industry growth and operational costs.

- A significant challenge confronting the wound closure devices market is the intensification of regulatory compliance, with new frameworks like the EU's Medical Device Regulation increasing the cost of clinical trials by up to 40%. This stringent oversight, coupled with mandatory product recall protocols, creates substantial financial and operational burdens, particularly for smaller innovators.

- Supply chain vulnerability for specialized raw materials like cyanoacrylate and chitosan-based hemostatic agents presents another hurdle, leading to price increases of over 15% and potential production delays. Furthermore, the market grapples with economic pressures from value-based procurement models in hospitals, which prioritize cost-effectiveness and force manufacturers into tighter profit margins.

- This is compounded by a scarcity of surgical staff trained in advanced closure techniques, leading to suboptimal use of innovative products like fibrin sealants and powered stapling devices.

Exclusive Technavio Analysis on Customer Landscape

The wound closure devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the wound closure devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Wound Closure Devices Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, wound closure devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3M Co. - Offerings include wound closure devices like antimicrobial skin closures and steri-strips, prioritizing infection prevention and superior healing.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- Advanced Medical Solutions Group

- Ansell Ltd.

- Artivion Inc.

- B.Braun SE

- Cardinal Health Inc.

- Chemence Medical Inc.

- Corza Medical

- DUKAL Corp.

- Dynarex Corp.

- Elkem ASA

- Integra LifeSciences Corp.

- Johnson and Johnson Services

- Medline Inc.

- Medtronic Plc

- Smith and Nephew plc

- Stryker Corp.

- SubQ It Inc.

- Teleflex Inc.

- Tricol Biomedical Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Health Care Equipment industry, the implementation of stricter regulations, such as the EU's Medical Device Regulation, has elevated the requirements for clinical evidence and post-market surveillance, directly increasing compliance costs and extending development timelines for new wound closure devices.

- A significant shift in surgical procedures towards outpatient settings and ambulatory surgical centers is driving demand for user-friendly wound closure solutions like topical skin adhesives and all-in-one kits that facilitate faster patient turnover and simplify post-operative care.

- The integration of digital technologies and robotics into surgical workflows has created a need for specialized, compatible wound closure devices, such as robotic-assisted closure systems and intelligent staplers, that can function within a digital operating room environment.

- Supply chain vulnerabilities for critical raw materials, including high-purity medical-grade polymers and specialty metals, have intensified, compelling manufacturers of wound closure devices to diversify their sourcing strategies and invest in more resilient production networks to mitigate disruption risks.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Wound Closure Devices Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 313 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.8% |

| Market growth 2026-2030 | USD 8893.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.1% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Thailand, Indonesia, Brazil, Saudi Arabia, UAE, Turkey, Argentina, South Africa, Colombia and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The wound closure devices market ecosystem is a complex network of stakeholders, beginning with suppliers of raw materials like medical-grade polymers and metals, which have seen price volatilities of up to 15% affect production costs. Manufacturers transform these inputs into sterile products, which are then subjected to rigorous regulatory approval by bodies such as the FDA and EMA.

- These agencies have increased clinical data requirements by an estimated 25%, raising entry barriers. Distribution occurs through direct sales forces and group purchasing organizations (GPOs), which leverage their large member base to negotiate lower prices. The primary end-users are hospitals and ambulatory surgical centers, with hospitals accounting for over 65% of consumption.

- The value chain is heavily influenced by clinical research from academic institutions, which drives innovation in areas like biocompatibility and regenerative medicine, ensuring the continuous evolution of products to meet surgical demands.

What are the Key Data Covered in this Wound Closure Devices Market Research and Growth Report?

-

What is the expected growth of the Wound Closure Devices Market between 2026 and 2030?

-

The Wound Closure Devices Market is expected to grow by USD 8.89 billion during 2026-2030, registering a CAGR of 8.8%. Year-over-year growth in 2026 is estimated at 8.1%%. This acceleration is shaped by strategic proliferation of minimally invasive surgical procedures, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Sutures, Hemostats, Surgical staples, Wound sealants, and Wound strips), Application (General surgery, Orthopedics, Gynecology and obstetrics, Cardiology, and Others), End-user (Hospitals, Ambulatory surgical centers, and Specialty wound clinics) and Geography (North America, Europe, Asia, Rest of World (ROW)). Among these, the Sutures segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, Asia and Rest of World (ROW). North America is estimated to contribute 45.7% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Thailand, Indonesia, Brazil, Saudi Arabia, UAE, Turkey, Argentina, South Africa, Colombia and Israel, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is strategic proliferation of minimally invasive surgical procedures, which is accelerating investment and industry demand. The main challenge is intensification of regulatory compliance and mandatory product recall protocols, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Wound Closure Devices Market?

-

Key vendors include 3M Co., Advanced Medical Solutions Group, Ansell Ltd., Artivion Inc., B.Braun SE, Cardinal Health Inc., Chemence Medical Inc., Corza Medical, DUKAL Corp., Dynarex Corp., Elkem ASA, Integra LifeSciences Corp., Johnson and Johnson Services, Medline Inc., Medtronic Plc, Smith and Nephew plc, Stryker Corp., SubQ It Inc., Teleflex Inc. and Tricol Biomedical Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape for wound closure devices is concentrated among diversified medical technology firms, with the top three companies commanding over 50% of the market. Key players like Johnson & Johnson, Medtronic, and B. Braun are heavily investing in R&D to innovate beyond traditional sutures and staples.

- Recent developments center on bio-resorbable materials and automated surgical stapling systems that offer real-time feedback, a market segment showing a 12% higher growth rate than manual devices. This focus on intelligent solutions addresses the critical need to reduce surgical site infections, which can increase patient care costs by more than $20,000 per incident.

- The market is also impacted by the strategic acquisition of niche technology firms specializing in high-strength tissue adhesives and sealants. Companies are adapting to pricing pressures from group purchasing organizations by bundling products and offering long-term value contracts to hospital networks.

We can help! Our analysts can customize this wound closure devices market research report to meet your requirements.

RIA -

RIA -