Organic Pigments Market Size 2025-2029

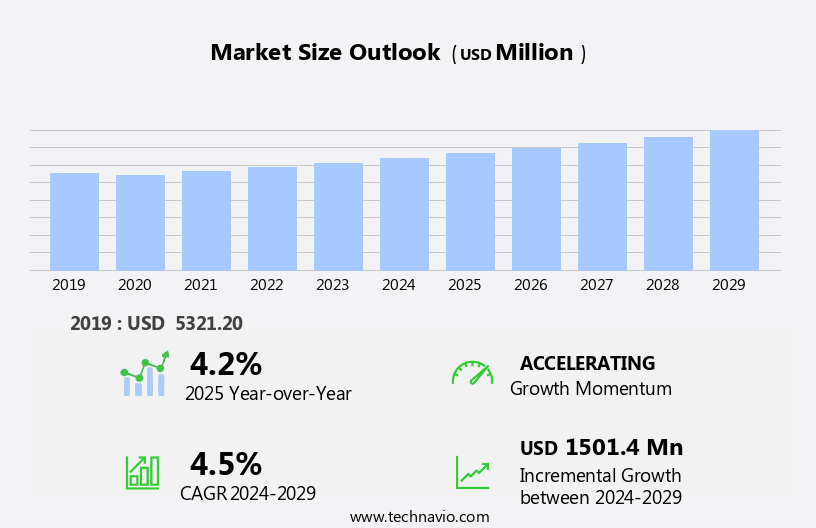

The organic pigments market size is forecast to increase by USD 1.5 billion at a CAGR of 4.5% between 2024 and 2029.

- The market is experiencing significant growth, driven by the increasing population and the demand for urbanized areas. The global population's expansion is leading to a rise in demand for various consumer goods, particularly in the food, cosmetics, and textile industries. These sectors heavily rely on pigments for coloring their products, creating a substantial market opportunity for organic pigments. The advancement of organic pigments, derived from natural sources, is another critical factor fueling market growth. In industrial paints and coatings, they offer excellent resistance to weathering and corrosion. Consumers' growing preference for eco-friendly and sustainable products has led to a shift from synthetic pigments to organic alternatives. However, the high cost of producing organic pigments poses a significant challenge for market expansion.

- Organic pigments are typically more expensive than their synthetic counterparts due to the complex and labor-intensive production process. Companies seeking to capitalize on this market must navigate this cost barrier while maintaining product quality and competitiveness. To overcome this challenge, innovations in production techniques and economies of scale could provide potential solutions. Effective strategies for managing production costs while maintaining high-quality organic pigments will be crucial for market success. Technological advancements in dyeing and printing processes are also driving market growth, enabling manufacturers to produce high-quality products with improved efficiency and consistency.

What will be the Size of the Organic Pigments Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market encompasses a diverse range of products, including ISOindolinone pigments, Azo pigments, Quinacridone pigments, Phthalocyanine pigments, Perylene pigments, Dioxazine pigments, and Lake pigments, among others. These pigments exhibit various properties, such as UV resistance, color fastness, film formation, and drying time, which influence their application methods and competitive advantages. ISOindolinone pigments, for instance, offer excellent color stability and migration resistance, making them suitable for high-performance coatings and plastics. Azo pigments, known for their bright hues and good lightfastness, dominate the market due to their wide usage in printing inks. Bio-based pigments, such as those derived from Quinacridone and Perylene, are gaining traction due to their eco-friendly nature and reduced environmental impact. In the US, zinc oxide and titanium dioxide are commonly used pigments in paints and coatings, industrial coatings, construction materials, personal care, toys, and construction.

Inorganic pigments, like Phthalocyanine and Dioxazine, provide excellent abrasion resistance and shelf life, making them popular choices in industrial applications. Milling techniques and pigment blending play a crucial role in enhancing the performance and economy of organic pigments. Nano pigments, a recent development, offer improved color intensity and faster curing process, creating new opportunities for innovation. Economic analysis of the market reveals that the demand for organic pigments is driven by the growing need for sustainable, high-performance, and cost-effective solutions in various industries. The Color Index, a standardized system for identifying pigments, ensures consistency and quality in the market. Pigment stability, drying time, and migration resistance are critical factors influencing the adoption and success of organic pigments in diverse applications. Waste management and efficient production processes are essential for minimizing environmental impact and maintaining competitiveness.

How is this Organic Pigments Industry segmented?

The organic pigments industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

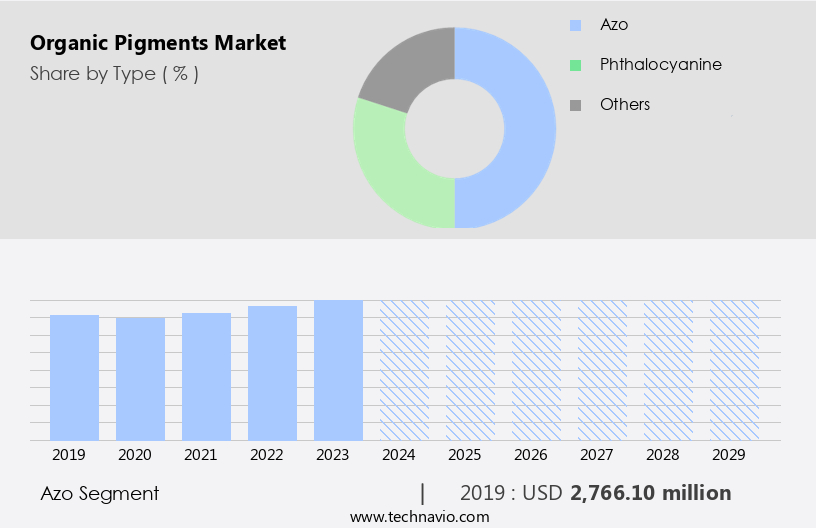

- Azo

- Phthalocyanine

- Others

- Application

- Printing inks

- Paints and coatings

- Plastics

- Others

- Source

- Synthetic

- Natural

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Type Insights

The azo segment is estimated to witness significant growth during the forecast period. Azo pigments, derived from diazine compounds, are integral to various industries due to their ability to impart vibrant colors, particularly red, yellow, and orange. Produced via diazotization and coupling processes, these pigments are colorless earth and clay materials that transform upon treatment. The pigment carrier significantly influences their light fastness. The paints and coatings sector holds the largest market share for azo pigments, fueled by robust demand from the global construction industry. Quality control is paramount in the production process to ensure color consistency and compliance with regulatory standards. Inkjet and flexographic printing techniques utilize azo pigments for their excellent color strength and durability.

Heat resistance and chemical resistance are essential properties, making azo pigments suitable for automotive coatings and industrial applications. Pigment dispersions and formulations are critical in enhancing pigment application efficiency and solvent resistance. Digital printing and screen printing also benefit from azo pigments' weather resistance and color calibration capabilities. The supply chain management of raw materials, from synthesis methods to pigment manufacturing, plays a significant role in maintaining pigment concentration and particle size distribution. Binder systems, surface treatment, and pigment pastes are essential components in the production of printing inks and coatings. The environmental impact of azo pigments is a growing concern, necessitating continuous research and development in pigment dispersion technologies and life cycle assessment strategies.

The Azo segment was valued at USD 2.77 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

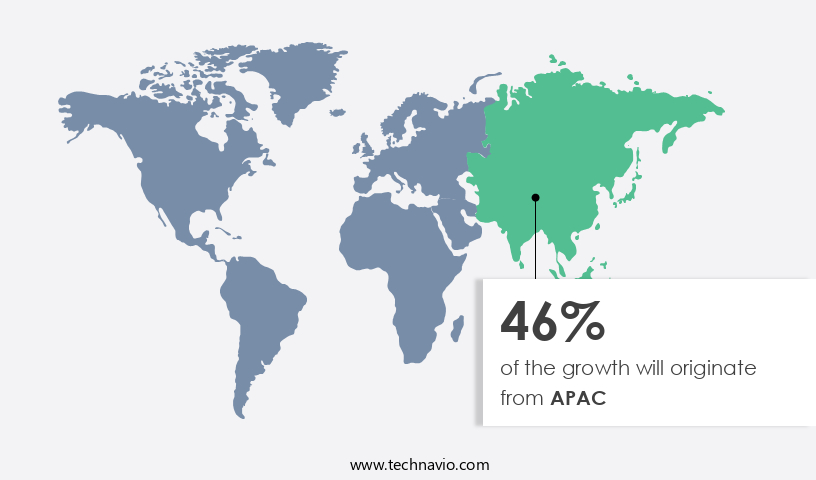

APAC is estimated to contribute 46% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is experiencing significant growth due to the increasing demand for paints and coatings in industries such as automotive and construction, particularly in Asia Pacific (APAC). With China and India leading the way in industrialization and automotive production, the region is anticipated to dominate the global market. In 2024, China produced approximately 33.5% of the world's automotive output. In construction, they are used in the production of concrete and masonry products to provide color and durability. This high demand for automotive coatings necessitates the use of organic pigments, which offer desirable properties such as heat resistance, weather resistance, and chemical resistance. The market is characterized by various manufacturing methods, including synthesis and formulation, and the use of raw materials like pigment powders and dispersions.

Pricing strategies and pigment concentration are crucial factors influencing market dynamics. Digital printing and regulatory compliance are also significant trends. The market's environmental impact is a critical consideration, with life cycle assessment and supply chain management playing essential roles. Coating techniques, such as flexographic printing, screen printing, roll coating, and gravure printing, require pigments with specific properties for optimal results. Surface treatment, binder systems, and pigment pastes are other essential components of the market. The market is a dynamic and evolving industry, driven by the demands of various end-use sectors and the ongoing pursuit of improved product performance and sustainability. The market is witnessing significant growth due to the advancements in pigment formulation and the emergence of smart pigments and functional additives.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Organic Pigments market drivers leading to the rise in the adoption of Industry?

- The primary factor fueling market growth is the increasing population and resulting demand for urbanized areas. The pigments market has experienced significant growth due to the increasing demand from various industries, including automotive, construction, and general manufacturing. This trend can be attributed to the global population shift towards urban areas, leading to improved living standards and increased expenditure on aesthetics. The automotive industry, for instance, relies heavily on pigments for imparting color and enhancing the visual appeal of vehicles. Similarly, the construction sector uses pigments for painting and coating buildings, while the general industrial segment employs them in various applications. Moreover, the demand for organic pigments is on the rise due to their superior color standards, chemical resistance, and pigment durability.

- Organic pigments offer excellent color management, making them suitable for digital printing applications. Regulatory compliance is another crucial factor driving the market's growth, as organic pigments meet the stringent safety and environmental regulations. Furthermore, the pigment dispersion process and synthesis methods have evolved significantly, leading to improved pigment quality and consistency. The life cycle assessment of organic pigments is also gaining importance, as companies focus on sustainable production methods and reducing their carbon footprint. Overall, the market is expected to continue its growth trajectory, driven by these market dynamics.

What are the Organic Pigments market trends shaping the Industry?

- Organic pigments are experiencing significant advancements, positioning them as the emerging market trend in the industry. This progression signifies a notable shift towards more sustainable and eco-friendly alternatives in colorants. Organic pigments are gaining traction in the market due to growing consumer and manufacturer concerns over health and safety. In contrast to inorganic pigments, which often contain lead, chromium, and cadmium, organic pigments offer a more sustainable alternative. However, they may not provide the same level of color fastness as inorganic pigments.

- This shift toward natural pigments aligns with the trend toward sustainability in various industries, including automotive coatings, coating techniques, printing inks, and more. By prioritizing the use of organic pigments, manufacturers can meet consumer demands for eco-friendly products without compromising on performance. To address this concern, recent research focuses on developing organic pigments from bio-based raw materials, reducing volatile organic compounds (VOCs) and offering equal color strength and other functionalities. The market is experiencing significant growth due to the increasing demand from various industries, particularly in the plastic, ceramic, and glass sectors.

How does Organic Pigments market faces challenges during its growth?

- The high cost of organic pigments poses a significant challenge to the growth of the industry, as these natural colorants are increasingly preferred for their health benefits and eco-friendly production methods. Organic pigments have gained significant traction in various end-user industries, including paints and coatings, plastics, and automotive, due to their wide array of vibrant color options. These pigments, primarily azo-based or polycyclic in nature, are increasingly preferred over inorganic pigments as manufacturers prioritize sustainability. However, the transition from inorganic to organic pigments is influenced by cost considerations. Although historically more expensive, the growing acceptance of organic pigments has led to more competitive pricing, making them a viable alternative. Moreover, the market dynamics are further shaped by advancements in technology. For instance, wetting agents are used to improve the dispersibility of pigments in industrial coatings, ensuring better resin compatibility.

- Gravure printing, a popular printing technique, benefits from particle size distribution optimization for improved color consistency. Supply chain management plays a crucial role in ensuring the smooth delivery of pigment pastes to manufacturers, while binder systems and surface treatment technologies are essential for enhancing pigment performance. Hybrid pigments, offering a blend of organic and inorganic properties, are emerging as a new category in the market. These pigments combine the best of both worlds, offering improved color stability, lightfastness, and cost-effectiveness. As the market evolves, it is essential for manufacturers to focus on optimizing their production processes and distribution channels to cater to the evolving demands of their customers.

Exclusive Customer Landscape

The organic pigments market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the organic pigments market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, organic pigments market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

artience Co. Ltd. - This company specializes in supplying organic pigments for various industries, including printing inks, paints, plastics, cosmetics, LCD filters, and inkjet printers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- artience Co. Ltd.

- BASF SE

- Changzhou Longyu Pigment Chemical Co. Ltd.

- Dainichiseika Color and Chemicals Mfg. Co. Ltd.

- DCL Corp.

- DIC Corp.

- Jet-Mate Canada Inc.

- Lanxess AG

- Neochem Technologies Pvt. Ltd.

- Sensient Technologies Corp.

- Sudarshan Chemical Industries Ltd.

- Sun Chemical Corp.

- Synthesia a.s.

- Trust Chem Co. Ltd.

- VIBFAST PIGMENTS PVT. LTD.

- Vibrantz

- Vipul Organics Ltd.

- Yuhong Pigment Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Organic Pigments Market

- In January 2024, DSM, a leading global science-based company in Nutrition, Health and Sustainable Living, announced the expansion of its global production capacity for carmine, a natural red pigment, by 30% at its facility in Spain. This move aimed to meet the growing demand for organic pigments in various industries, including food, cosmetics, and textiles (DSM Press Release, 2024).

- In March 2024, BASF, the world's leading chemical producer, entered into a strategic partnership with German colorant manufacturer, Wacker Chemicals, to develop and produce organic pigments based on bio-based raw materials. The collaboration aimed to reduce the carbon footprint of pigments and contribute to the circular economy (BASF Press Release, 2024).

- In May 2024, Clariant, a leading global specialty chemical company, completed the acquisition of Huntsman Corporation's pigments and additives business. The acquisition expanded Clariant's portfolio in the market and strengthened its position as a global leader in this sector (Clariant Press Release, 2024).

- In April 2025, the European Union (EU) approved the use of natural pigments derived from cochineal insects, such as carmine, for organic food products. This decision was a significant shift in the EU's regulatory framework, allowing for the use of these pigments in organic food production (European Commission Press Release, 2025).

Research Analyst Overview

The market continues to evolve, driven by advancements in technology and increasing demand across various sectors. Industrial coatings remain a significant application area, with organic pigments offering superior color strength and heat resistance. Inkjet printing and gravure printing also utilize organic pigments due to their excellent color space and particle size distribution. Distribution channels play a crucial role in the market, with suppliers adopting strategic pricing strategies to cater to diverse customer needs. Wetting agents and resin compatibility are essential considerations in pigment manufacturing, ensuring optimal performance in various applications. The unfolding market dynamics extend to pigment dispersions and formulation, with ongoing research and development efforts focusing on improving pigment durability and chemical resistance.

Surface treatment and binder systems are essential components of the pigment manufacturing process, ensuring pigment pastes maintain their desired properties during application. Supply chain management remains a critical factor, with pigment manufacturers implementing efficient strategies to meet the evolving demands of the market. Regulatory compliance and environmental impact are also significant considerations, with life cycle assessment and color management playing essential roles in ensuring sustainable and high-quality pigment production. As digital printing gains popularity, organic pigments are increasingly being used in this application due to their excellent color calibration and tinting strength. Roll coating and dip coating techniques are also employing organic pigments for their superior color matching capabilities and solvent resistance.

The market is characterized by continuous dynamism, with ongoing research and development efforts focusing on improving pigment properties and expanding applications across various sectors. The integration of advanced technologies and sustainable production methods is essential to meet the evolving demands of the market while ensuring regulatory compliance and environmental sustainability.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Organic Pigments Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

224 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2025-2029 |

USD 1.5 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.2 |

|

Key countries |

China, US, Germany, Japan, UK, India, France, South Korea, Canada, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Organic Pigments Market Research and Growth Report?

- CAGR of the Organic Pigments industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the organic pigments market growth of industry companies

We can help! Our analysts can customize this organic pigments market research report to meet your requirements.

RIA -

RIA -