Secondary Packaging Market Size 2026-2030

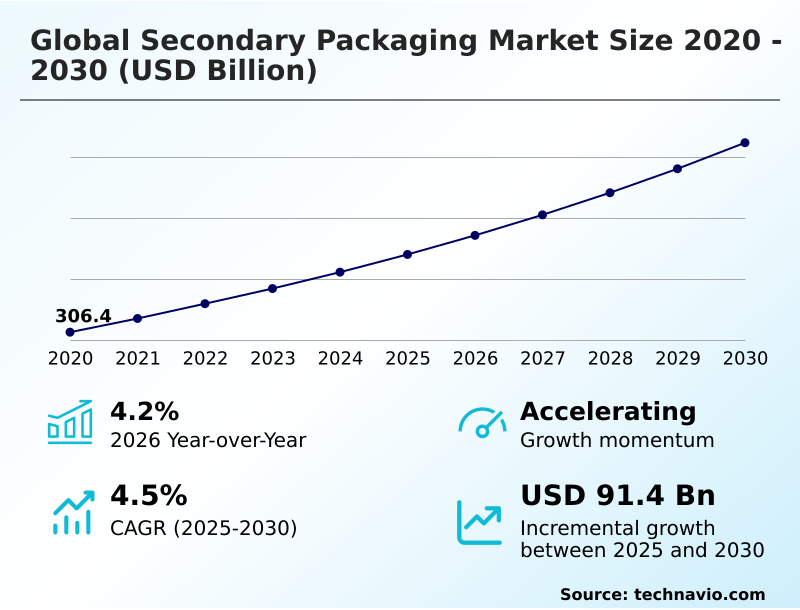

The Secondary Packaging Market size was valued at USD 370 billion in 2025, growing at a CAGR of 4.5% during the forecast period 2026-2030.

Major Market Trends & Insights

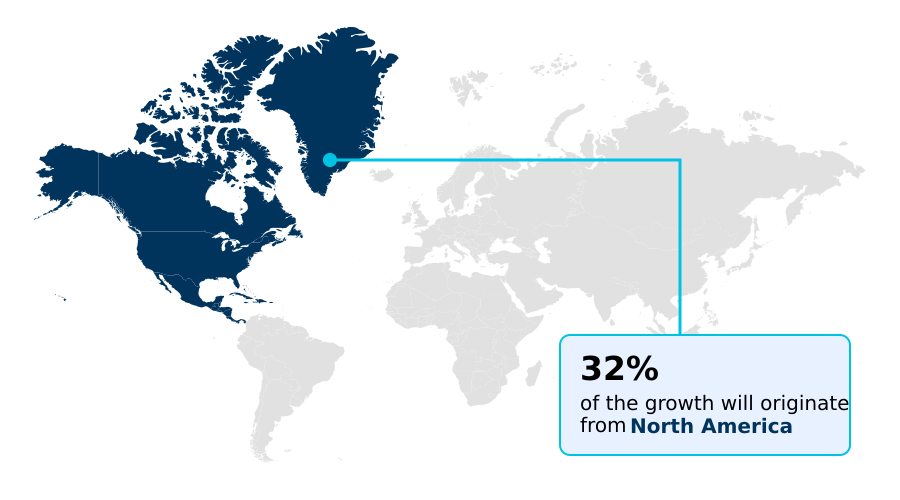

- North America dominated the market and accounted for a 32.2% growth during the forecast period.

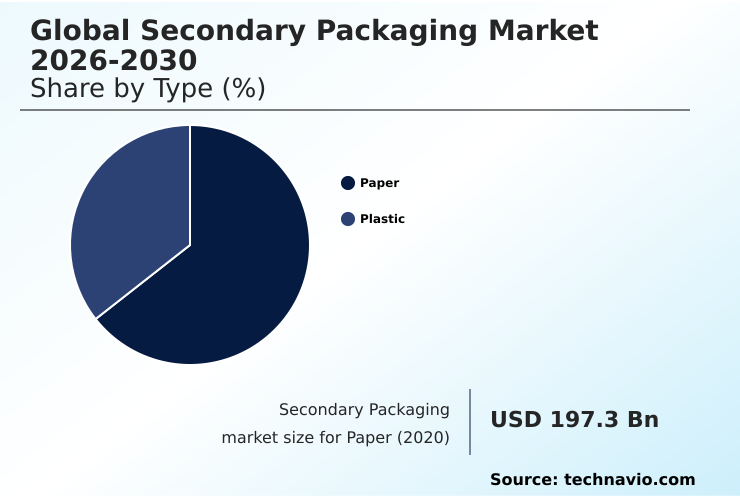

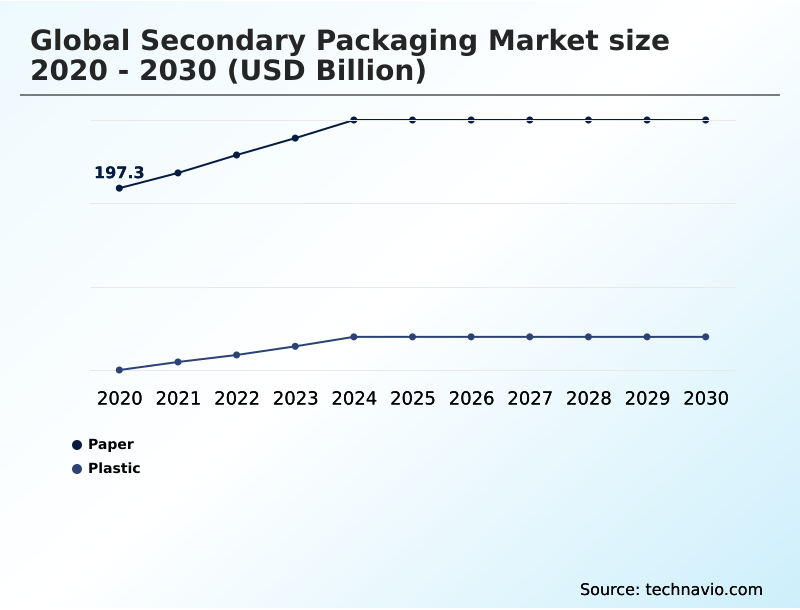

- By Type - Paper segment was valued at USD 230.4 billion in 2024

- By Application - Food segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 155 billion

- Market Future Opportunities 2025-2030: USD 91.4 billion

- CAGR from 2025 to 2030 : 4.5%

Market Summary

- The secondary packaging market is defined by a major shift toward sustainable materials, with paper-based solutions now accounting for over 60% of the market. In a typical business scenario, an e-commerce distributor adopting custom-fit corrugated boxes has reduced transit-related product damages by 15%, which minimizes waste and lowers return processing costs.

- This evolution is driven by the rapid expansion of online retail, which requires durable packaging capable of withstanding the rigors of complex, multi-touchpoint delivery networks. However, the industry grapples with the significant challenge of volatile raw material prices for both pulp and plastics, which can compress profit margins.

- To remain competitive, manufacturers are increasingly implementing end-of-line automation, a strategy essential for enhancing throughput and managing the high-volume demands of modern commerce while controlling operational expenses.

What will be the Size of the Secondary Packaging Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Secondary Packaging Market Segmented?

The secondary packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Paper

- Plastic

- Application

- Food

- Beverages

- Pharmaceuticals

- Personal and home care

- Others

- Product

- Folding cartons

- Corrugated boxes

- Plastic crates and totes

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

How is the Secondary Packaging Market Segmented by Type?

The paper segment is estimated to witness significant growth during the forecast period.

Paper-based solutions dominate the secondary packaging market, accounting for over 64% of total material use due to their superior recyclability and structural integrity.

The adoption of advanced corrugated fiberboard has improved load stability by over 15% in high-volume logistics, directly impacting operational efficiency for e-commerce and retail distribution.

This segment, encompassing corrugated boxes, folding cartons, and paperboard, is driven by sustainability mandates and consumer preference for plastic-free options. Innovations in lightweighting allow for material reduction without compromising protective qualities, which is critical for optimizing freight costs.

The shift to retail-ready packaging formats made from paper further enhances in-store efficiency, making it the preferred choice for the food, beverage, and consumer goods sectors.

The Paper segment was valued at USD 230.4 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Secondary Packaging market is rising in the leading region?

North America is estimated to contribute 32.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Secondary Packaging Market demand is rising in North America Request Free Sample

North America leads the global secondary packaging market, holding approximately 32% of the share, a position sustained by its massive e-commerce sector and advanced logistics networks.

In contrast, APAC is the fastest-growing region, set to account for nearly 30% of incremental market growth, driven by its expanding manufacturing base and the rise of modern retail.

Within North America, the US represents over 80% of the regional demand. European markets, led by Germany, demonstrate higher adoption rates of automated systems and returnable transit packaging, enabling some FMCG supply chains to cut packaging waste by 25%.

This geographic variance requires distinct business strategies, from high-automation and retail-ready packaging in Europe to scalable, cost-effective corrugated boxes and flexible packaging solutions to support industrialization and rising consumer demand across APAC.

What are the key Drivers, Trends, and Challenges in the Secondary Packaging Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions within secondary packaging increasingly balance performance, sustainability, and cost, compelling businesses to look beyond simple material choices. Evaluating the cost of corrugated vs plastic packaging, for example, now involves lifecycle assessments, where paper-based options often yield a 5% higher effective recycling rate.

- The search for the best secondary packaging for shipping sensitive goods is driving the adoption of engineered protective packaging solutions that reduce damage. In parallel, the growing demand for sustainable secondary packaging for food is accelerating innovation in biodegradable coatings and compostable materials. Adherence to pharmaceutical secondary packaging compliance remains non-negotiable, mandating investments in traceability and tamper-evident features.

- To enhance efficiency, firms are deploying automated end of line packaging systems, with some reporting a 30% increase in throughput. This automation is crucial for managing the demands of e-commerce protective packaging solutions, where the unboxing experience is paramount. Understanding the secondary packaging design process for retail is essential for creating effective shelf-ready formats.

- Likewise, selecting the appropriate secondary packaging materials for beverages requires balancing structural integrity with lightweighting goals. The role of secondary packaging in supply chain optimization is undeniable, serving as the foundation for unitization and streamlined logistics.

What are the key market drivers leading to the rise in the adoption of Secondary Packaging Industry?

- Rapid growth in e-commerce is a key market driver, increasing the demand for protective and efficient transport packaging solutions.

- Rapid e-commerce growth is a primary market driver, with direct-to-consumer channels requiring up to 30% more protective transport packaging compared to traditional retail logistics.

- The cause of this is the greater number of handling points in the fulfillment chain, which directly impacts businesses by increasing demand for durable corrugated boxes and custom inserts.

- Another key driver is the rising consumption in the food and beverage packaging sector, which boosts demand for bulk secondary packaging formats.

- To handle this increased volume and address labor shortages, the adoption of end-of-line automation is critical, as implementing robotic packaging systems like palletizers can improve throughput by over 40% and significantly reduce operational costs.

What are the market trends shaping the Secondary Packaging Industry?

- The growing adoption of sustainable and recyclable materials is a primary trend, driven by regulatory pressures and consumer demand for eco-friendly solutions. This shift is reshaping material science and supply chains across the industry.

- A dominant trend in secondary packaging is the shift to sustainable packaging materials, with many brands replacing plastic components with fiber-based alternatives, contributing to a 20% reduction in plastic waste for certain multipack applications.

- Simultaneously, the integration of smart packaging technologies such as QR codes and RFID tags is accelerating, improving supply chain transparency and helping reduce stock losses by up to 25% for high-value goods. This digital transformation is caused by the demand for better inventory management and anti-counterfeiting measures. It affects businesses by requiring investments in data platforms and sensor-enabled logistics.

- Furthermore, increasing customization needs are fueling the adoption of digital printing, allowing for cost-effective, short-run production that enhances brand visibility on retail-ready packaging.

What challenges does the Secondary Packaging Industry face during its growth?

- Volatile raw material prices represent a key challenge, significantly impacting manufacturer profit margins and affecting overall industry growth.

- A primary challenge facing the secondary packaging market is the extreme volatility of raw material prices, with sudden fluctuations in pulp and polymer resins leading to cost increases of up to 20% for manufacturers in a single quarter. This unpredictability directly compresses profit margins and complicates long-term financial planning for packaging converters.

- Another significant challenge stems from stringent environmental regulations, which can elevate compliance costs by 10-15% through mandates for higher recycled content and bans on certain single-use plastics. The cause is a global legislative movement toward a circular economy, which forces companies to invest heavily in R&D for alternative materials and product redesigns, impacting capital expenditure and operational workflows.

Exclusive Technavio Analysis on Customer Landscape

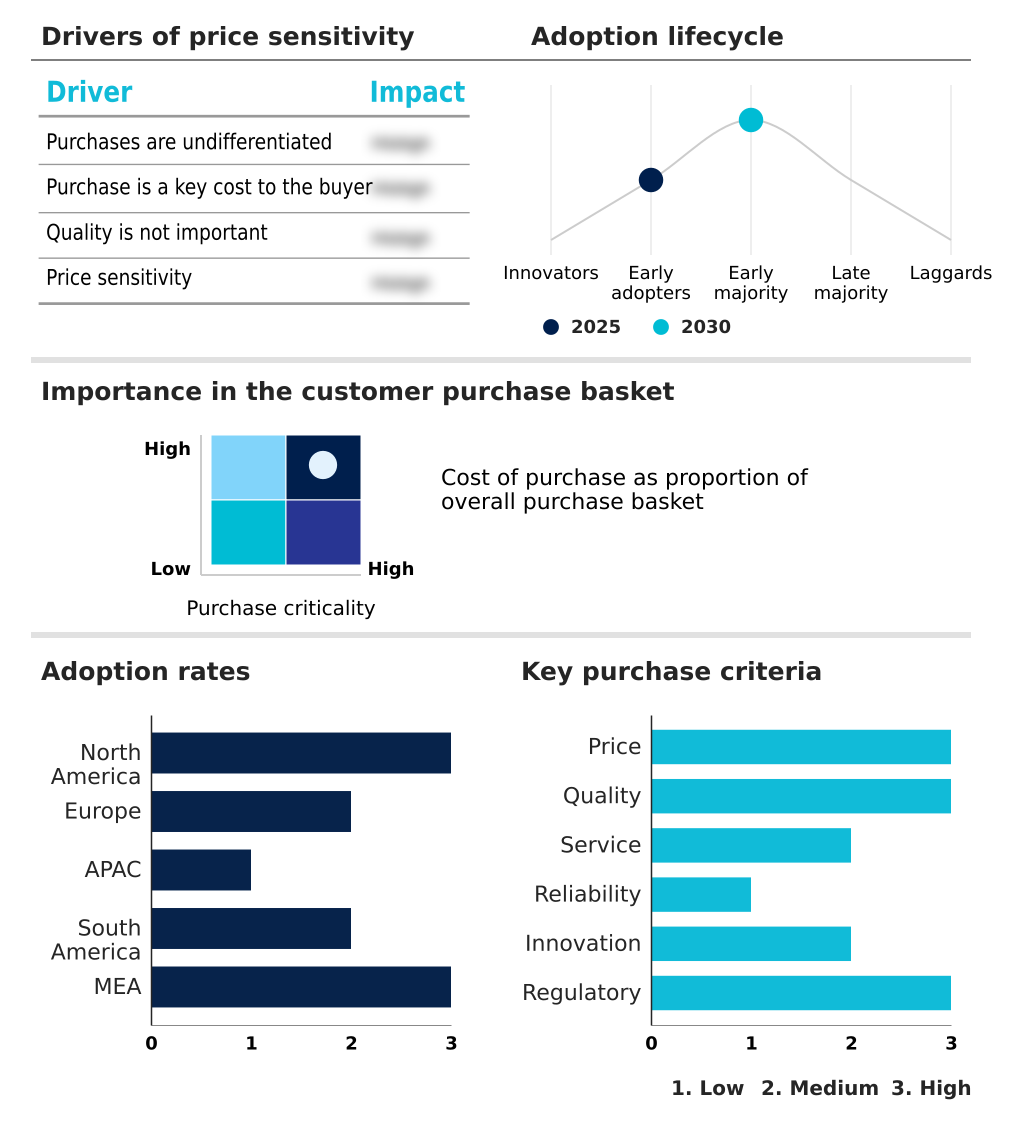

The secondary packaging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the secondary packaging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Secondary Packaging Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, secondary packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amcor Plc - Offers a portfolio of secondary packaging, from corrugated cartons to shrink films, designed for robust product protection and optimized supply chain handling.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amcor Plc

- Ball Corp.

- Crown Holdings Inc.

- Daio Paper Corp.

- DS Smith Plc

- Graphic Packaging Holding Co.

- Huhtamaki Oyj

- International Paper Co.

- Mondi Plc

- Packaging Corp. of America

- Rengo Co. Ltd.

- Salzgitter AG

- Sealed Air Corp.

- Smurfit Kappa Group

- Sonoco Products Co.

- Stora Enso Oyj

- Tetra Laval SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Metal, Glass and Plastic Containers industry, the implementation of stringent regulations, particularly in Europe, targeting single-use plastics has significantly increased demand for fiber-based secondary packaging, such as paperboard multipack carriers and corrugated trays, as direct replacements for shrink films.

- A widespread push for a minimum of 30% post-consumer recycled (PCR) content in plastic containers is reshaping material sourcing, compelling secondary packaging converters to develop solutions that are not only made from recycled materials but also designed for simplified end-of-life disassembly and recycling.

- The adoption of advanced lightweighting technologies for PET bottles and aluminum cans has reduced the inherent rigidity of primary packs, heightening the reliance on high-performance corrugated boxes and internal partitions to provide necessary structural integrity and prevent damage during transit.

- Persistent volatility in the global prices of raw materials, including aluminum, PET resins, and wood pulp, has prompted secondary packaging manufacturers to invest in more agile production lines capable of switching between different material formats to mitigate cost-related supply chain disruptions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Secondary Packaging Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.5% |

| Market growth 2026-2030 | USD 91.4 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The secondary packaging ecosystem originates with raw material suppliers providing wood pulp and polymer resins, where price fluctuations can alter manufacturer costs by up to 15% quarterly. Packaging converters transform these inputs into finished goods like corrugated boxes and folding cartons, leveraging machinery from technology providers to enable automated end-of-line processes.

- Regulatory bodies mandate strict safety and recyclability standards, particularly for the food and pharmaceutical sectors, which collectively represent over 50% of the market's end-user base. Distribution networks, comprising logistics firms and wholesalers, are indispensable for moving packaged goods to retailers and e-commerce fulfillment centers.

- Ultimately, end-user demand from CPG brands and industrial manufacturers, driven by needs for product protection, branding, and supply chain efficiency, dictates the market's direction and innovation priorities.

What are the Key Data Covered in this Secondary Packaging Market Research and Growth Report?

-

What is the expected growth of the Secondary Packaging Market between 2026 and 2030?

-

The Secondary Packaging Market is expected to grow by USD 91.4 billion during 2026-2030, registering a CAGR of 4.5%. Year-over-year growth in 2026 is estimated at 4.2%%. This acceleration is shaped by rapid e-commerce growth increasing demand for protective transport packaging solutions, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Paper, and Plastic), Application (Food, Beverages, Pharmaceuticals, Personal and home care, and Others), Product (Folding cartons, Corrugated boxes, Plastic crates and totes, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa). Among these, the Paper segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, South America and Middle East and Africa. North America is estimated to contribute 32.2% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is rapid e-commerce growth increasing demand for protective transport packaging solutions, which is accelerating investment and industry demand. The main challenge is volatile raw material prices impacting manufacturer profit margins, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Secondary Packaging Market?

-

Key vendors include Amcor Plc, Ball Corp., Crown Holdings Inc., Daio Paper Corp., DS Smith Plc, Graphic Packaging Holding Co., Huhtamaki Oyj, International Paper Co., Mondi Plc, Packaging Corp. of America, Rengo Co. Ltd., Salzgitter AG, Sealed Air Corp., Smurfit Kappa Group, Sonoco Products Co., Stora Enso Oyj and Tetra Laval SA. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape for secondary packaging is concentrated, with the top ten firms capturing nearly 40% of the market. Key players like International Paper Co. and Smurfit Kappa Group are channeling significant investments into sustainable fiber-based solutions and advanced digital printing capabilities to align with evolving brand owner requirements.

- These innovations address the growing demand for recyclable and retail-ready packaging, which has been demonstrated to improve shelf velocity by up to 20% in mass-market retail settings. This strategic pivot toward value-added features helps companies create differentiation amid persistent cost pressures from raw material price volatility.

- In response, firms are also broadening their service offerings to include packaging design optimization and automation consulting, adapting to customer demands for more integrated and efficient supply chain solutions.

We can help! Our analysts can customize this secondary packaging market research report to meet your requirements.

RIA -

RIA -