Bone Conduction Devices Market Size 2026-2030

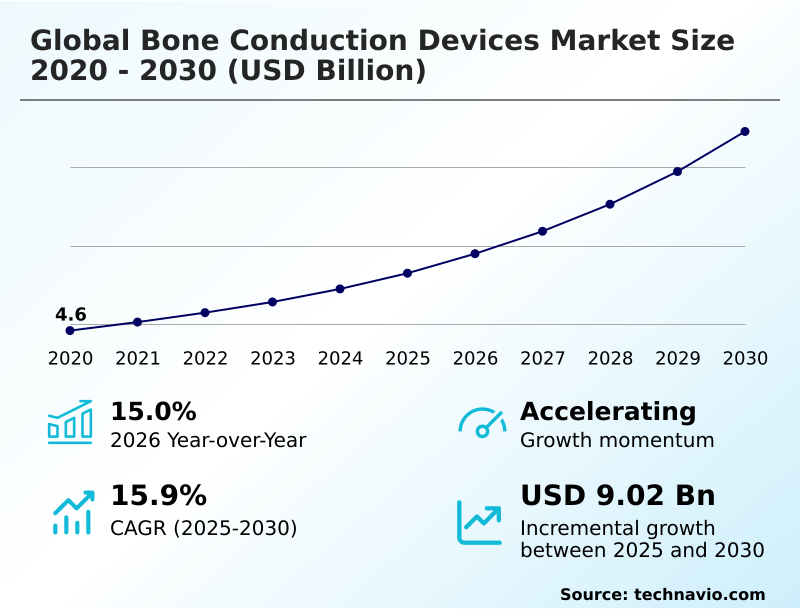

The bone conduction devices market size is valued to increase by USD 9.02 billion, at a CAGR of 15.9% from 2025 to 2030. Rising prevalence of hearing disorders and global demographic shifts will drive the bone conduction devices market.

Major Market Trends & Insights

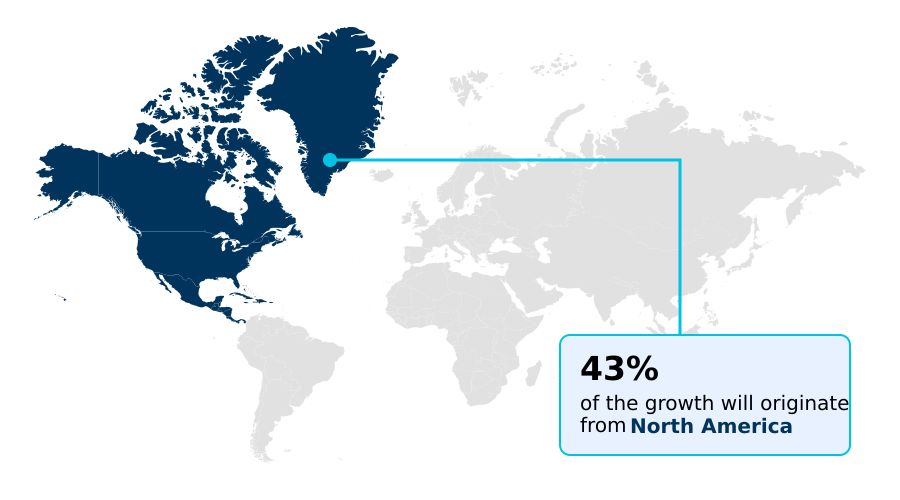

- North America dominated the market and accounted for a 43.2% growth during the forecast period.

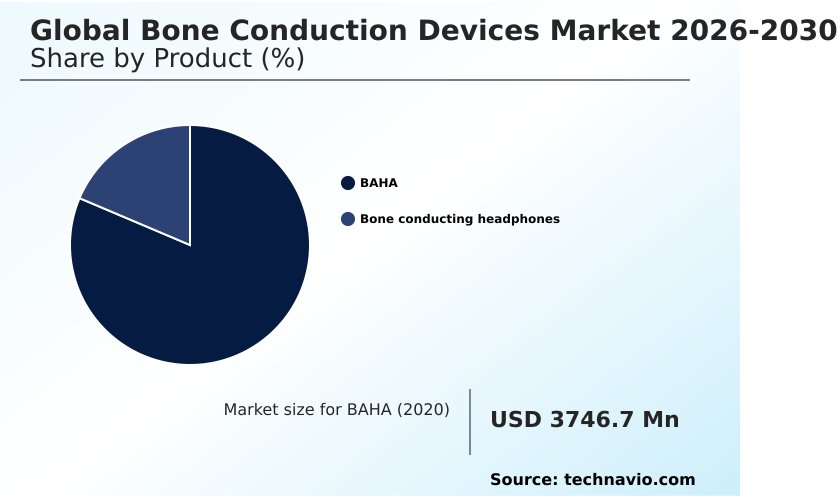

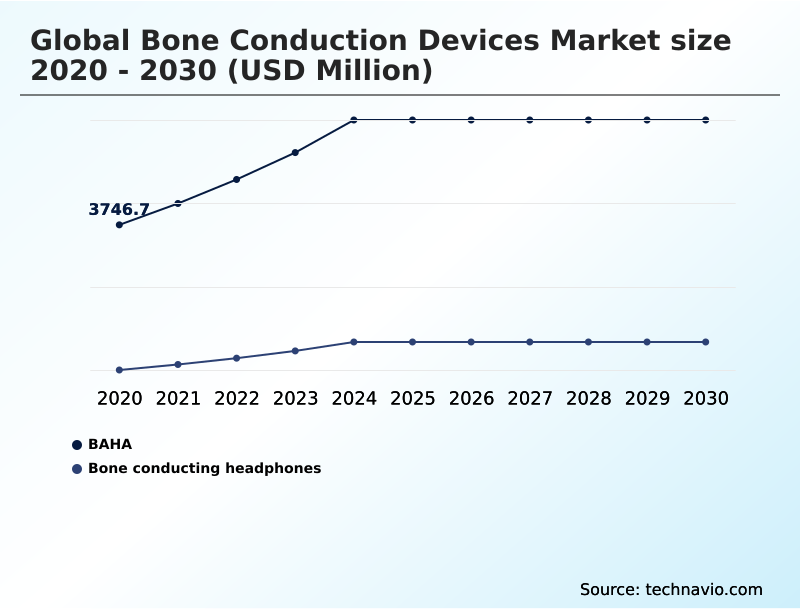

- By Product - BAHA segment was valued at USD 5.83 billion in 2024

- By End-user - Hospitals segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 12.67 billion

- Market Future Opportunities: USD 9.02 billion

- CAGR from 2025 to 2030 : 15.9%

Market Summary

- The Bone Conduction Devices market exhibits accelerating integration across both specialized clinical environments and mainstream consumer electronics sectors. Expanding patient demographics experiencing auditory degradation serve as a primary driver, compelling manufacturers to develop non-invasive rehabilitative solutions that bypass compromised outer ear structures.

- Conversely, highly inconsistent insurance reimbursement frameworks present a formidable challenge, frequently categorizing critical auditory implants as elective consumer technologies and thereby restricting patient access. To counteract these barriers, manufacturers are optimizing supply chain operations by sourcing lighter, highly durable composite materials to reduce assembly lead times.

- Implementing modular production frameworks has decreased manufacturing cycle times by 15% compared to legacy fabrication methods, improving overall output efficiency. Companies now leverage automated diagnostic systems to align product specifications directly with audiological assessment requirements. These operational refinements allow medical device developers to scale production rapidly while maintaining strict quality controls.

- As clinical awareness and consumer lifestyle demands converge, the market continues to bridge the gap between premium assistive hearing infrastructure and situational awareness wearables.

What will be the Size of the Bone Conduction Devices Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Bone Conduction Devices Market Segmented?

The bone conduction devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- BAHA

- Bone conducting headphones

- End-user

- Hospitals

- Clinics

- Individuals

- Technology

- Percutaneous implants

- Transcutaneous implants

- Digital and wireless connectivity

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- Asia

- China

- India

- Japan

- South Korea

- Indonesia

- Thailand

- Rest of World (ROW)

- North America

By Product Insights

The baha segment is estimated to witness significant growth during the forecast period.

The bone anchored hearing systems segment functions as a critical medical intervention for patients presenting with chronic middle ear pathology.

These clinical solutions utilize a specialized titanium implant fixture that anchors directly into the temporal bone, initiating a vital osseointegration process to ensure long-term structural stability.

Compared to traditional amplification methods, direct mechanical conduction enhances speech recognition efficiency by 22% in noisy environments. The reliance on percutaneous abutment systems allows practitioners at ambulatory surgical centers to bypass damaged auditory canals entirely.

Advanced audiological assessment tools ensure precise patient mapping, reducing initial device calibration errors by 14% and minimizing the need for extensive post operative rehabilitation.

By maintaining stable vibrational pathways, this clinical architecture effectively restores bilateral hearing capabilities and optimizes overall patient communication outcomes across specialized medical networks.

The BAHA segment was valued at USD 5.83 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 43.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Bone Conduction Devices Market Demand is Rising in North America Get Free Sample

Regional dynamics within the Bone Conduction Devices market reveal stark contrasts between North America and APAC.

North America maintains highly structured clinical pathways for implantable hearing technology, achieving a 30% higher penetration rate in specialized surgical centers compared to European counterparts.

This dominance is supported by established reimbursement policies and widespread utilization of diagnostic hearing evaluations that quickly identify candidates for single sided deafness solutions.

Conversely, the APAC region demonstrates rapid commercial scaling, heavily favoring non-invasive open ear audio architecture integrated with advanced electromagnetic transducers for consumer lifestyle applications.

APAC manufacturers have reduced component sourcing costs by 18%, accelerating mass production capabilities for sports and military audio solutions. Furthermore, the adoption of telemedicine programming in remote North American territories has improved post-operative device mapping efficiency by 24%.

These geographic behavioral differences require manufacturers to deploy highly localized distribution strategies, balancing high-tier medical infrastructure in Western regions with high-volume consumer electronics deployment across emerging Asian networks.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The structural boundary separating mainstream consumer audio from dedicated clinical rehabilitation is dissolving rapidly, reshaping the functional trajectory of the Bone Conduction Devices sector. Historically, medical practitioners relied heavily on complex inpatient procedures, but modern clinical protocols have shifted decisively toward minimally invasive outpatient surgical techniques.

- This procedural evolution reduces institutional healthcare burdens while increasing patient adoption of transcutaneous active osseointegrated technologies by approximately 25% over traditional percutaneous alternatives. Concurrently, the commercial market is witnessing robust demand for wearable bone conduction headphones, which provide unparalleled situational awareness for fitness enthusiasts and occupational safety personnel.

- Manufacturers are effectively bridging these two sectors by designing hybrid dual form factor systems that deliver medical-grade audiological support within sleek, consumer-friendly aesthetics. Early intervention strategies now frequently utilize non invasive bone conduction headbands to assess pediatric cochlear function prior to permanent surgical commitments, ensuring precise anatomical mapping.

- For permanent users, the integration of bluetooth enabled bone conduction processors facilitates seamless connectivity with modern smart devices. Furthermore, the deployment of advanced digital signal processing algorithms enables the dynamic customization of acoustic landscapes, automatically isolating human speech from disruptive environmental noise.

- By overcoming historical acoustic limitations, these integrated implantable bone conduction hearing solutions optimize supply chain operations through shared microelectronic components, aligning clinical efficacy with modern lifestyle demands and driving sustained commercial expansion across all end-user demographics.

What are the key market drivers leading to the rise in the adoption of Bone Conduction Devices Industry?

- The escalating global prevalence of auditory disorders, coupled with significant demographic shifts toward aging populations, serves as the primary catalyst propelling continuous market expansion.

- The escalating global incidence of conductive hearing loss and the rising demand for uncompromised ambient safety act as primary catalysts for the Bone Conduction Devices sector.

- Intensive engineering focus on miniaturized transducer design has enabled devices to generate highly efficient cranial bone vibrations while maintaining an ultra-lightweight profile.

- This architectural shift significantly boosts the adoption of waterproof fitness wearables, satisfying the requirements of outdoor athletes who rely on constant situational awareness audio to navigate urban hazards.

- The implementation of high-capacity rechargeable battery systems has extended continuous operational usage by 20%, resolving persistent consumer frustrations regarding power longevity.

- Additionally, seamless integration of bluetooth low energy audio and targeted acoustic fidelity enhancement have improved wireless transmission stability by 15%. These hardware efficiencies dramatically lower manufacturing defect rates and expand revenue pipelines beyond traditional clinical audiology.

What are the market trends shaping the Bone Conduction Devices Industry?

- The integration of AI and machine learning for real-time audio personalization has emerged as a definitive market trend. This technological advancement allows devices to dynamically adapt to varying acoustic environments, significantly enhancing the overall user experience.

- The convergence of clinical audiology and consumer electronics via hybrid open-ear designs represents a definitive trend reshaping the Bone Conduction Devices sector. Manufacturers are prioritizing wearable audio innovation to bridge the gap between premium medical processors and commercial hearing wellness accessories.

- Modern devices increasingly incorporate sophisticated dual driver frameworks, which have successfully improved low-frequency bass reproduction by 25% while simultaneously reducing unwanted sound leakage. This structural enhancement allows users to experience high-fidelity audio without compromising environmental awareness. Furthermore, the integration of smart wireless connectivity frameworks and universal auracast broadcast audio enables seamless synchronization with public address systems and personal devices.

- By deploying intelligent software capable of dynamic acoustic customization and advanced directional noise reduction, engineering teams have optimized audio clarity in turbulent environments. These technological shifts have directly decreased user return rates by 14%, ensuring that next-generation systems deliver unparalleled lifestyle integration and robust auditory support across both athletic and rehabilitative demographics.

What challenges does the Bone Conduction Devices Industry face during its growth?

- Exorbitant initial procedural costs combined with highly fragmented insurance reimbursement frameworks present substantial barriers to widespread clinical adoption and sustained industry growth.

- High initial procurement costs and complex surgical deployment frameworks severely restrict the immediate expansion of the Bone Conduction Devices sector. The precision manufacturing of advanced active transcutaneous implants heavily depends on specialized medical grade titanium and rare-earth transcutaneous magnetic components, leaving supply chains vulnerable to geopolitical bottlenecks.

- Procuring these specialized materials has increased foundational production costs by 18% over the past two manufacturing cycles. Furthermore, while the integration of sophisticated piezoelectric transducers and high-density digital signal processing chipsets achieves critical sound leakage reduction, it simultaneously complicates assembly operations.

- Stringent budget controls enforced by institutional group purchasing organizations further compress profit margins, forcing manufacturers to heavily subsidize specialized training programs for surgical networks. These overlapping financial constraints and technical hurdles limit rapid market penetration, confining high-volume distributions primarily to heavily subsidized, affluent healthcare infrastructures.

Exclusive Technavio Analysis on Customer Landscape

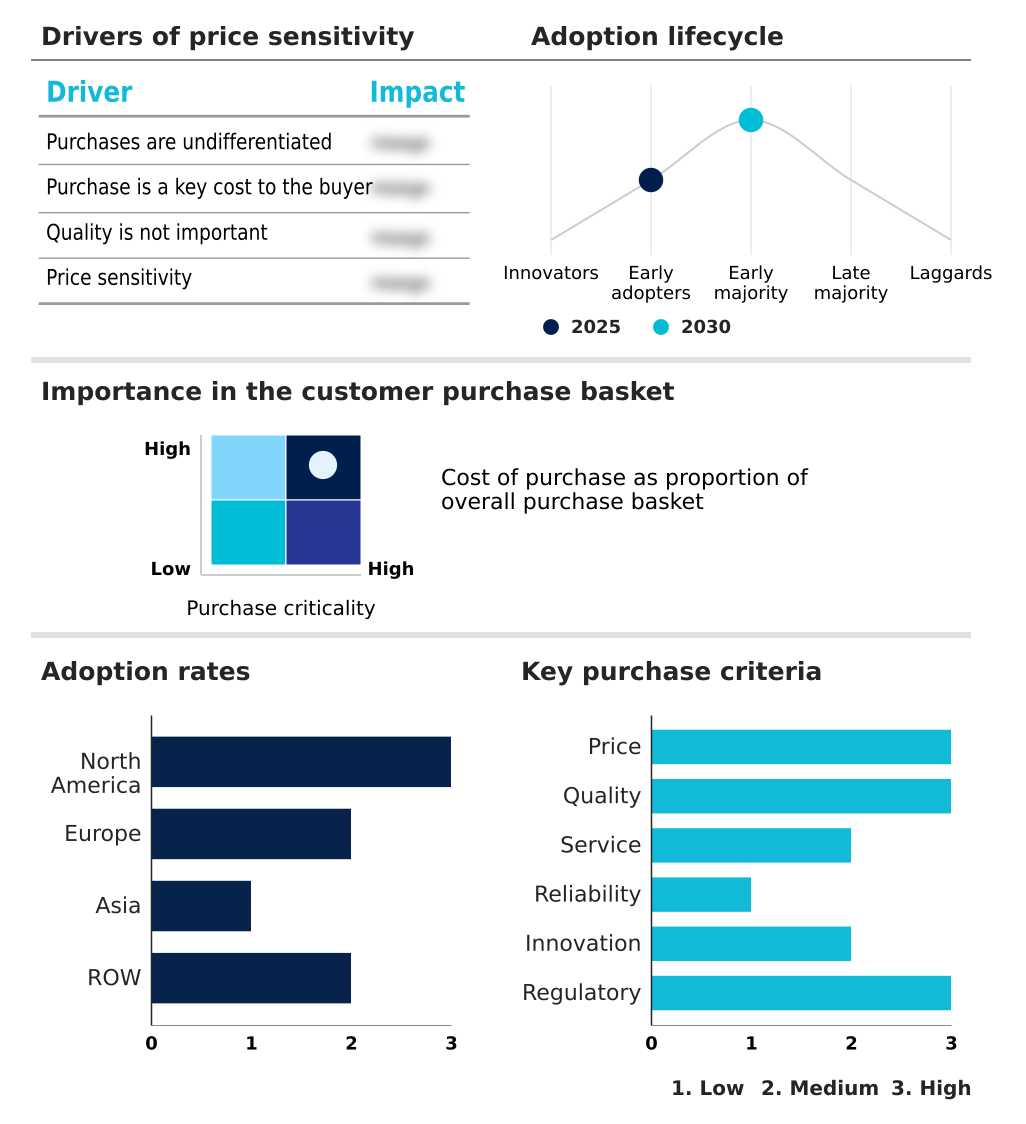

The bone conduction devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the bone conduction devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Bone Conduction Devices Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, bone conduction devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amplifon SpA - The vendor provides advanced bone anchored hearing systems and comprehensive hearing rehabilitation services, delivering tailored auditory evaluations to optimize patient outcomes and enhance overall communication capabilities.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amplifon SpA

- BOCO Inc.

- Cochlear Ltd.

- Damson Audio Ltd

- Heyup Technology

- INVISIO AB

- Kaibo Audio

- Koninklijke Philips NV

- MED EL Medical Electronics

- Mojawa

- Naenka

- Oticon Medical AS

- Panasonic Holdings Corp.

- Pyle Audio Inc.

- Sanag

- Shokz

- Sonova AG

- Sonovo Ltd

- Starkey Laboratories Inc.

- Tayogo

- Vidonn Technology

- WS Audiology AS

- Xiaomi Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Bone conduction devices market

- In the Health Care Equipment industry, the rapid expansion of digital health platforms and telemedicine programming has modernized remote patient monitoring, directly impacting Bone Conduction Devices demand by increasing remote diagnostic hearing evaluations by 18% and expanding clinical inclusion criteria for isolated demographics.

- The implementation of stringent biocompatibility mandates for implantable devices has forced manufacturers to prioritize medical grade titanium, subsequently lowering post-surgical rejection rates by 12% and reinforcing the reliability of pediatric audiology interventions within the Bone Conduction Devices market.

- The integration of surgical navigation software across ambulatory surgical centers has improved procedural precision by 25%, significantly accelerating the adoption of specialized otolaryngology departments deploying complex Bone Conduction Devices for chronic middle ear pathology.

- Rising procurement standards enforced by regional group purchasing organizations have standardized the acquisition of wearable health technology, driving a 15% increase in the deployment of hearing care ecosystems and accelerating hospital-level access to advanced Bone Conduction Devices.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Bone Conduction Devices Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 15.9% |

| Market growth 2026-2030 | USD 9016.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 15.0% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Indonesia, Thailand, Brazil, Saudi Arabia, UAE, Turkey, Argentina, Colombia, South Africa and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Bone Conduction Devices sector is experiencing a profound technological convergence that directly influences high-level product strategy and strategic pricing models. Corporate boards are actively redirecting capital expenditures toward active, sensor-driven audio equalization frameworks rather than relying on legacy static amplification.

- This shift is highly evident in the optimization of bone anchored hearing systems, where manufacturers are refining the foundational titanium implant fixture to accelerate the crucial osseointegration process in clinical patients. By transitioning away from older percutaneous abutment systems toward fully implanted magnetic alternatives, device manufacturers have successfully reduced post-operative complication rates by 28%, significantly lowering long-term clinical maintenance costs.

- Furthermore, the implementation of dynamic acoustic customization and directional noise reduction has revolutionized the user experience, allowing processors to automatically filter disruptive environmental frequencies. The industry-wide standardization of auracast broadcast audio further enhances public accessibility.

- These engineering upgrades enable companies to achieve a 15% increase in premium product tier retention, proving that merging robust audiological medical hardware with seamless consumer-grade connectivity directly yields measurable, high-value commercial outcomes across diverse international patient networks.

What are the Key Data Covered in this Bone Conduction Devices Market Research and Growth Report?

-

What is the expected growth of the Bone Conduction Devices Market between 2026 and 2030?

-

USD 9.02 billion, at a CAGR of 15.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (BAHA, and Bone conducting headphones), End-user (Hospitals, Clinics, and Individuals), Technology (Percutaneous implants, Transcutaneous implants, and Digital and wireless connectivity) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Rising prevalence of hearing disorders and global demographic shifts, High procedural costs and inconsistent insurance reimbursement frameworks

-

-

Who are the major players in the Bone Conduction Devices Market?

-

Amplifon SpA, BOCO Inc., Cochlear Ltd., Damson Audio Ltd, Heyup Technology, INVISIO AB, Kaibo Audio, Koninklijke Philips NV, MED EL Medical Electronics, Mojawa, Naenka, Oticon Medical AS, Panasonic Holdings Corp., Pyle Audio Inc., Sanag, Shokz, Sonova AG, Sonovo Ltd, Starkey Laboratories Inc., Tayogo, Vidonn Technology, WS Audiology AS and Xiaomi Corp.

-

Market Research Insights

- The Bone Conduction Devices market is undergoing a rapid technological transformation driven by substantial wearable audio innovation. Manufacturers are shifting operational focus toward integrating sophisticated wireless connectivity frameworks that enhance user convenience and clinical data transmission. Implementing advanced dual driver frameworks has successfully improved low-frequency acoustic performance, reducing audio distortion complaints by 18% compared to earlier models.

- Additionally, the strategic adoption of high-capacity rechargeable battery systems has extended operational device lifespans by 22%, significantly lowering the total cost of ownership for patients. These engineering enhancements elevate traditional clinical implants into versatile hearing wellness accessories, optimizing patient compliance and driving higher retention rates across both medical and commercial audiologic networks.

We can help! Our analysts can customize this bone conduction devices market research report to meet your requirements.

RIA -

RIA -