Radar Sensors Market Size 2024-2028

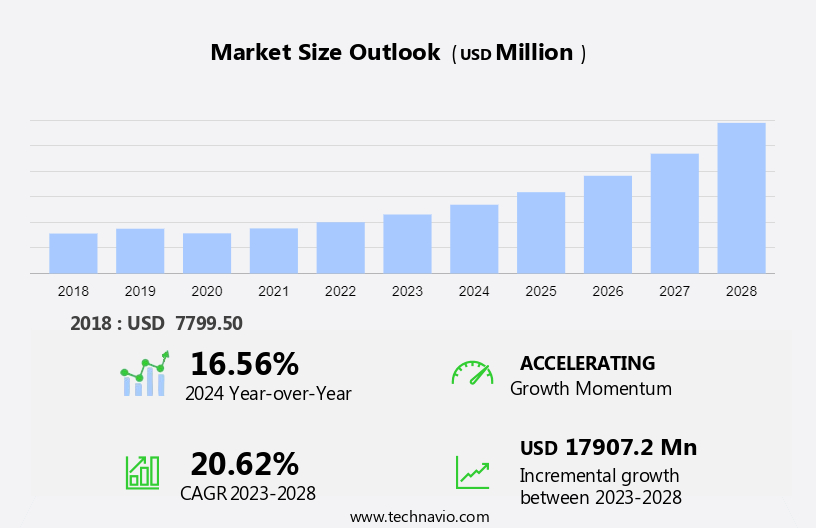

The radar sensors market size is forecast to increase by USD 17.91 billion at a CAGR of 20.62% between 2023 and 2028.

- Radar sensors have gained significant traction in various industries due to their ability to detect objects in various environments. Advanced driver assistance systems (ADAS) in automobiles and global positioning systems (GPS) in logistics are prime examples of this technology's application. Radar sensors are also finding extensive use in insulators for monitoring power lines and in surveillance applications. With the proliferation of Internet of Things (IoT) devices, these are increasingly being integrated into industrial automation systems for predictive maintenance and quality control. Furthermore, these are essential for blind spot detection in vehicles and are increasingly being used in marine vessels and Unmanned Aerial Vehicles (UAVs). Market trends include the increasing use of drones in numerous applications, the emergence of high-resolution radar imaging sensors, and the cost pressure faced by Original Equipment Manufacturers (OEMs). These trends are shaping the market and driving its growth.

What will be the Size of the Market During the Forecast Period?

- The market encompasses a diverse range of electronic devices employing radio waves to detect and measure various objects, including imaging and non-imaging radar sensors. Short-range and long-range radar sensors cater to distinct applications, such as security and surveillance, industrial processes, traffic monitoring, and IoT devices. Sub-millimeter-wave radar sensors have gained traction due to their ability to penetrate through obstacles and provide high-resolution imaging. CW radar sensors and frequency-modulated continuous wave (FMCW) radar sensors are integral to applications like autonomous vehicles, radar detectors, and radar scrambling In the aerospace and defense sector. These are also pivotal in weather monitoring, with applications including altitude measurement for aircraft, marine vessels, two-wheelers, and automobiles.

- In addition, antenna technology plays a crucial role in enhancing radar sensor performance, while electromagnetic emissions remain a key consideration In their design and implementation. The market is poised for significant growth, driven by the increasing demand for advanced sensing technologies in various industries.

How is this Industry segmented and which is the largest segment?

The industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Automotive

- Aerospace and defense

- Industrial

- Others

- Product

- Non-imaging sensors

- Imaging sensors

- Geography

- North America

- US

- APAC

- China

- Japan

- Europe

- Germany

- UK

- South America

- Middle East and Africa

- North America

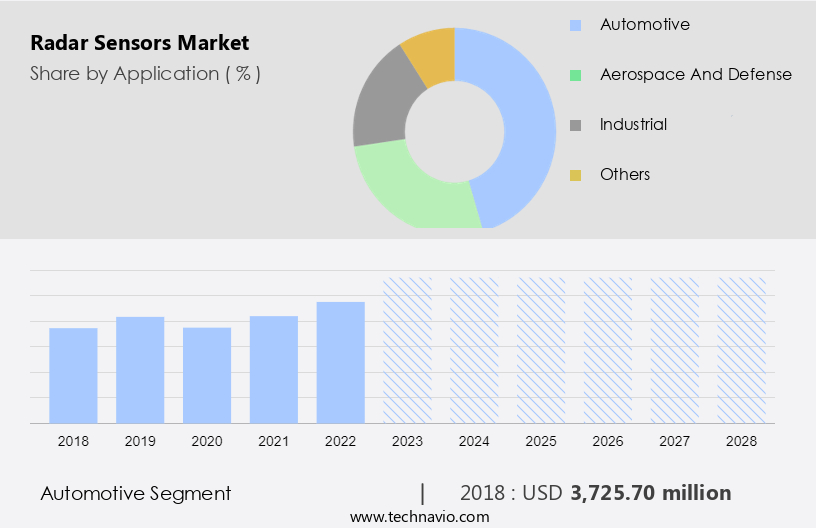

By Application Insights

- The automotive segment is estimated to witness significant growth during the forecast period.

Radar sensors, integral to automobiles, utilize radio waves for object detection and localization. Two primary frequency bands, 24 GHz and 77 GHz, are employed In the automotive industry. The higher frequency 77 GHz radar sensors offer superior accuracy for distance and speed measurement. In contrast, 24 GHz radar sensors provide less accurate readings. Applications of radar sensors in automobiles encompass blind-spot detection, lane-change assistance, collision warning or avoidance systems, parking assistance, and cross-traffic monitoring. Regulatory requirements and the growing emphasis on safety are driving the adoption of radar sensors in motor vehicles.

Get a glance at the Radar Sensors Industry report of share of various segments Request Free Sample

The automotive segment was valued at USD 3.73 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

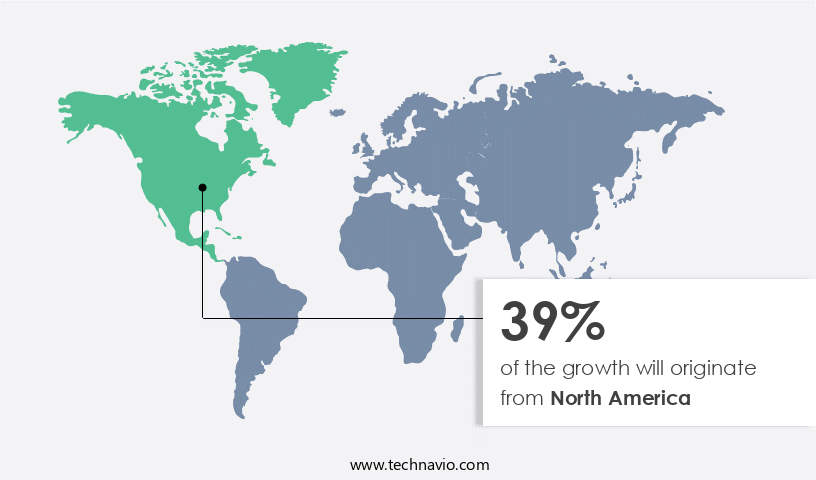

- North America is estimated to contribute 39% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market in North America is experiencing significant growth due to the expansion of the manufacturing sector In the region. Governments In the US and Canada are offering incentives and subsidies to attract manufacturing companies to set up operations, particularly in Canada due to its abundant natural resources and increasing labor costs in Asia Pacific. As manufacturing industries continue to grow, there is a rising demand for automation in production plants. It plays a crucial role in automation, enabling applications such as collision avoidance systems, blind spot detection, and lane change assistance in motor vehicles. In addition, these are used in industrial automation, traffic monitoring, security and surveillance, and building automation solutions.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Radar Sensors Industry?

Increasing use of drones in numerous applications is the key driver of the market.

- Radar sensors play a crucial role In the autonomous navigation of drones, providing real-time obstacle detection and facilitating safe flight. Non-imaging radar sensors, such as Short-Range Radar (SRR) and Long-Range Radar (LRR), employ reflected radio waves to identify objects and measure their distance, velocity, and size. These sensors are essential for drone applications, including target surveillance, interception, missile guidance, and terrain tracking. In the industrial sector, these are utilized in various applications, such as automation, traffic monitoring, and security and surveillance. Short-Range Radar Sensors are employed for blind spot detection, collision mitigation, lane change assistance, parking assistance, and rear cross-traffic alert in motor vehicles.

- Furthermore, Long-Range Radar Sensors, operating at 77-GHz or 79GHz frequency, enable high-resolution tracking and 360-degree car surveillance. Radar Applications extend beyond automotive and include biomedical, defense, weather monitoring, and aerospace and defense industries. Digital technologies, such as 5G technology and wireless detecting technologies, are driving the integration of it in IoT devices, such as CW radar sensors and sub-millimeter-wave radar sensors. The autonomous car market is expected to grow significantly, leading to increased demand for it in Automotive Radar systems. Radar Detector and Radar Scrambling technologies are being developed to counteract the use of it for law enforcement purposes.

What are the market trends shaping the Radar Sensors Industry?

Emergence of the high-resolution radar imaging sensor is the upcoming market trend.

- Radar sensors, a critical component of Advanced Driver-Assistance Systems (ADAS) and autonomous vehicles, are essential for imaging and non-imaging applications. In the US market, high-resolution radar sensors, which operate at frequencies such as 77-GHz and 79GHz, are increasingly adopted for improved object recognition and detection in various industries. These sensors enable precise detection of blind spots, collision mitigation, lane change assistance, parking assistance, and rear cross-traffic alert. The growing demand for autonomous cars necessitates the development of advanced radar technologies, as demonstrated by incidents involving self-driving vehicles. Long-range radar sensors are also used for security and surveillance, industrial automation, traffic monitoring, and defense applications.

- In addition, digital technologies, such as 5G and wireless detecting technologies, are enhancing the capabilities of it in various sectors. IoT devices, CW radar sensors, and corner radar sensors are other emerging radar applications. The radar market is expected to grow significantly due to the increasing penetration of consumer electronic devices, smart grids, smart homes, smart water networks, intelligent transport systems, and 5G technology. The radar market encompasses various components, including antennas, duplexers, transmitters, receivers, video amplifiers, processors, sensors, and electronic devices. Electromagnetic emissions from these components must be managed to ensure passenger safety and minimize interference with other systems. These are used in various industries, including automotive, aerospace and defense, weather monitoring, and marine vessels.

What challenges does the Radar Sensors Industry face during its growth?

Cost pressure faced by OEMs is a key challenge affecting the industry growth.

- In the realm of automotive technology, radar sensors play a pivotal role in enhancing vehicle safety and functionality. These sensors employ electromagnetic waves to detect objects and their motion, enabling applications such as collision avoidance systems, adaptive cruise control, and blind spot detection. These are categorized into Imaging and Non-Imaging types, with Short-Range and Long-Range variants. The former is used for applications like parking assistance and blind spot detection, while the latter is utilized for long-range surveillance and target separation. Security and surveillance, industrial automation, traffic monitoring, and automotive industries are primary markets for radar applications. Automotive radar, including Automotive Radar, Biomedical Radar, and Digital Technologies, is a significant segment.

- In addition, these are also employed in consumer electronic devices, smart grids, smart homes, and smart water networks for intelligent transportation and 5G technology. The autonomous driving market, including Motor Vehicles, Aircraft, Marine vessels, and Two-wheelers, is a significant growth area for radar sensors. Radar applications include speed gauge, altimeter, pulse, continuous wave, and non-imaging, utilizing reflected radio waves and signals for motion trajectory detection. Global positioning systems and optical, infrared, wireless, and dense mediums are some of the environments in which radar sensors operate. Passenger safety, collision avoidance systems, heavy commercial automobiles, target surveillance, interception, missile guidance, terrain tracking, navigation, airport intrusion detection, prison perimeter, oil depot, and corner radar sensors are various applications.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ainstein Inc.

- Arbe Robotics Ltd

- Banner Engineering Corp.

- Continental AG

- DENSO Corp.

- HELLA GmbH and Co. KGaA

- Infineon Technologies AG

- InnoSenT GmbH

- Israel Aerospace Industries Ltd.

- Lockheed Martin Corp.

- MediaTek Inc.

- NXP Semiconductors NV

- Robert Bosch GmbH

- RTX Corp.

- S.m.s Smart Microwave Sensors GmbH

- Sivers Semiconductors AB

- Steradian Semiconductors Pvt. Ltd.

- Texas Instruments Inc.

- Vayyar Imaging Ltd.

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Radar sensors have gained significant traction in various industries due to their ability to detect objects and measure their distance, velocity, and size. These sensors employ electromagnetic waves to identify and track targets, making them an essential component in numerous applications. Non-imaging radar sensors differ from imaging radar In their functionality. While imaging radar creates visual representations of objects, non-imaging radar focuses on measuring specific parameters such as distance, velocity, and size. Short-range radar sensors are commonly used for applications like blind spot detection, collision mitigation, lane change assistance, parking assistance, and rear cross-traffic alert in automobiles. Long-range radar sensors, on the other hand, are utilized for target surveillance, interception, missile guidance, and terrain tracking in defense applications.

In addition, the integration of it into security and surveillance systems has been a game-changer. Radar technology is employed in various sectors, including industrial automation, traffic monitoring, and automotive industries. In industrial applications, these are used for process control, level measurement, and object detection. In the automotive industry, these are a crucial component of advanced driver-assistance systems (ADAS), enabling features such as automatic emergency braking and collision avoidance systems. The advent of digital technologies has led to the development of advanced radar sensors. Sub-millimeter-wave radar sensors, for instance, offer high-resolution tracking and can penetrate through dense mediums like fog, rain, and snow.

Furthermore, radar applications extend beyond automotive and industrial sectors. In the biomedical field, radar sensors are used for non-invasive health monitoring. The integration of radar sensors in consumer electronic devices, smart grids, smart homes, and smart water networks has led to the development of intelligent transport systems and 5G technology. Wireless detecting technologies, including radar sensors, are essential for enabling seamless connectivity and communication between various devices. These are also employed in aerospace and defense applications, including weather monitoring, aircraft, marine vessels, and two-wheelers. Radar technology plays a vital role in airport intrusion detection, prison perimeter security, oil depot security, and other defense applications.

In addition, the radar market is expected to grow significantly due to the increasing demand for autonomous vehicles and the integration of it in various industries. The integration of it in autonomous cars is expected to revolutionize the automotive industry, enabling features like speed gauge, altimeter, pulse, and continuous wave. From automotive and industrial applications to defense and biomedical sectors, radar sensors offer numerous benefits, including high accuracy, reliability, and flexibility. The integration of it in consumer electronic devices, smart grids, and intelligent transport systems is expected to drive the growth of the radar market In the coming years.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

171 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 20.62% |

|

Market growth 2024-2028 |

USD 17.91 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

16.56 |

|

Key countries |

US, China, Germany, Japan, and UK |

|

Competitive landscape |

Leading Companies, market growth and forecasting , Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Radar Sensors Market Research and Growth Report?

- CAGR of the Radar Sensors industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the radar sensors market growth of industry companies

We can help! Our analysts can customize this radar sensors market research report to meet your requirements.

RIA -

RIA -