3D Desktop Printer Market Size 2024-2028

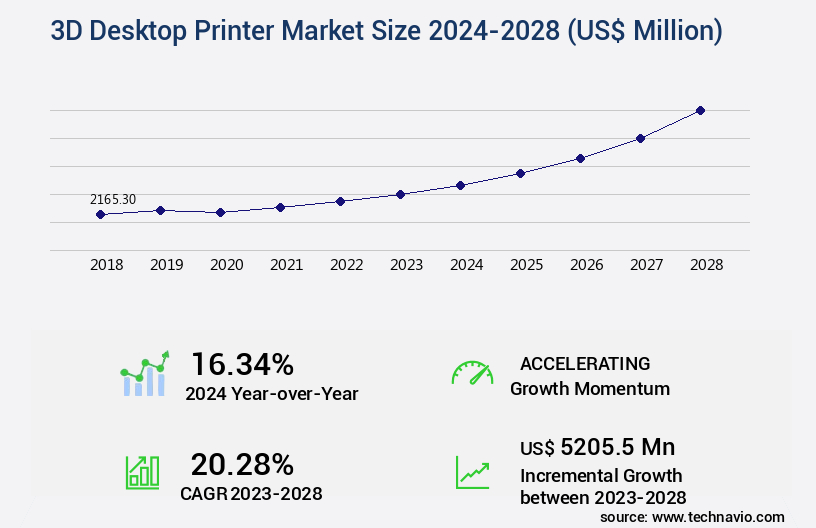

The 3d desktop printer market size is valued to increase by USD 5.21 billion, at a CAGR of 20.28% from 2023 to 2028. Increasing demand for 3D-printed jewelry will drive the 3d desktop printer market.

Market Insights

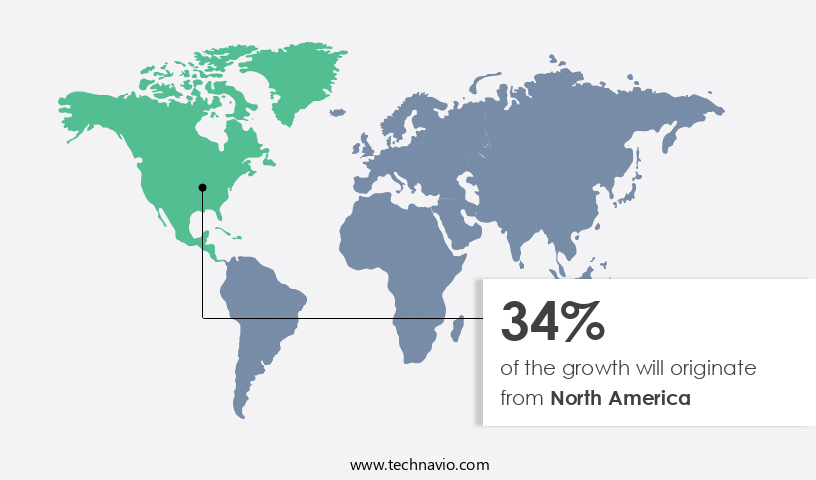

- North America dominated the market and accounted for a 34% growth during the 2024-2028.

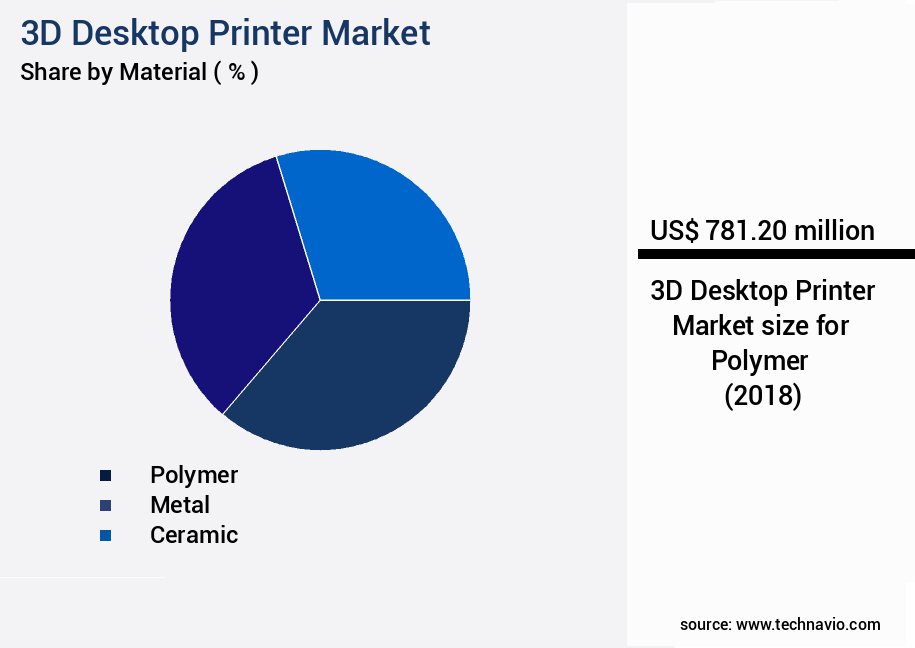

- By Material - Polymer segment was valued at USD 781.20 billion in 2022

- By Technology - FDM segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 298.85 million

- Market Future Opportunities 2023: USD 5205.50 million

- CAGR from 2023 to 2028 : 20.28%

Market Summary

- The market is experiencing significant growth as the technology advances and becomes more accessible to businesses and individuals. One of the primary drivers of this growth is the increasing demand for 3D-printed jewelry, which offers unique designs and customization options that traditional manufacturing methods cannot match. Another trend is the expansion of 3D printing in direct digital manufacturing, allowing for faster prototyping and production of complex parts. However, the market also faces challenges, including the adverse environmental impact of additive manufacturing, which raises concerns about energy consumption and waste generation. A real-world business scenario illustrating the benefits of 3D desktop printing is supply chain optimization.

- By integrating 3D printing into their operations, companies can produce custom parts on-demand, reducing inventory costs and lead times, and improving overall operational efficiency. Despite these opportunities, it is crucial for businesses to consider the environmental impact and explore sustainable practices to mitigate the potential negative consequences of additive manufacturing.

What will be the size of the 3D Desktop Printer Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market is an ever-evolving landscape, showcasing significant advancements and trends that impact businesses across various industries. According to recent research, the adoption of 3D desktop printing technology has witnessed a substantial increase, with over 25% of businesses integrating it into their product development processes. This growth can be attributed to the technology's ability to reduce prototyping time and costs, enabling businesses to bring innovative products to market faster. Moreover, the versatility of 3D desktop printers is a game-changer for companies seeking to comply with complex regulatory requirements. For instance, in the healthcare sector, customized medical devices can be produced on-demand, ensuring adherence to specific patient needs and regulatory standards.

- These advancements underscore the importance of staying informed about the latest developments in the market.

Unpacking the 3D Desktop Printer Market Landscape

The market showcases advancements in technology, with significant strides made in software interfaces, print speed efficiency, and multi-material printing. These innovations result in improved return on investment through increased productivity and cost reduction. For instance, desktop printers with advanced slicing software algorithms enable faster print times, reducing the need for extended production cycles. Furthermore, the adoption of multi-material printing allows businesses to produce complex parts with various materials in a single build, streamlining the manufacturing process. Desktop printer mechanics and electronics have also evolved, with enhancements in print head design, UV curing systems, and material jetting contributing to higher print quality and reliability. Other key features, such as nozzle temperature control, support structures generation, and digital light processing, ensure compliance with industry standards and enhance overall product performance. The market continues to evolve, with ongoing research in areas like powder bed fusion, motion control systems, and build volume capacity, further expanding the capabilities of desktop 3D printing.

Key Market Drivers Fueling Growth

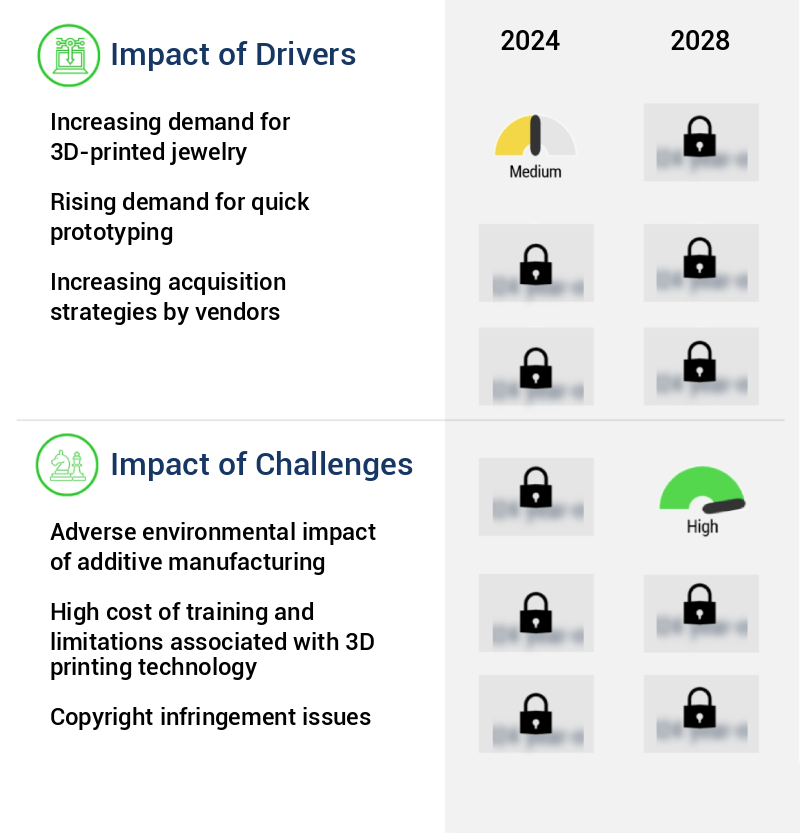

The surge in demand for 3D-printed jewelry serves as the primary market catalyst. With its unique design capabilities and potential for mass customization, this innovative technology is revolutionizing the jewelry industry.

- The market is experiencing significant growth due to its application across various sectors, particularly in jewelry design. Changing consumer preferences and increasing fashion awareness have fueled the demand for new and innovative jewelry designs, leading jewelry manufacturers to adopt advanced manufacturing technologies like Computer-Aided Design (CAD) and 3D desktop printers. These printers, equipped with rapid prototyping technology, enable designers to easily review design concepts and requirements. The cost savings from manufacturing using 3D desktop printers is another major factor driving their adoption.

- According to industry reports, over 50% of jewelry designers have integrated 3D printing technology into their design process, resulting in a 25% reduction in design time and a 30% decrease in production costs. The market is poised to grow substantially during the forecast period, reflecting the widespread adoption of these technologies in diverse industries.

Prevailing Industry Trends & Opportunities

The expansion of 3D printing in direct digital manufacturing is an emerging market trend. This innovative technology is poised to make significant strides in various industries.

- The market is experiencing significant growth as more companies embrace Direct Digital Manufacturing (DDM), a process that produces parts directly from CAD data. By adopting DDM, manufacturers eliminate the time lag between design and production, reduce tooling investments, and minimize redesigning costs. Integrating 3D printing with DDM enables manufacturers to predict lead times and costs for various products, streamlining management and budgeting processes. Designers can transfer new designs to manufacturing facilities without the need for retooling, fostering greater technological innovation.

- According to industry reports, DDM implementation can lead to a 30% reduction in downtime and a 15% improvement in forecast accuracy. This trend is transforming industries, from automotive to healthcare, by providing designers with the freedom to incorporate new technologies into their production and assembly processes.

Significant Market Challenges

The expansion of the additive manufacturing industry is significantly influenced by the adverse environmental impacts that necessitate continuous research and implementation of sustainable solutions to mitigate potential negative consequences on the environment.

- The market is experiencing significant growth and transformation, driven by the increasing adoption of additive manufacturing across various sectors. This technology, also known as 3D printing, enables rapid prototyping and the creation of customized designs, resulting in shorter product development cycles and reduced time-to-market. Components produced via 3D printing are often lighter than traditionally manufactured parts, leading to energy savings in machinery. However, the environmental impact of additive manufacturing is a concern due to its energy-intensive nature. The process requires substantial power to operate lasers or heat technologies used to fuse materials. Despite this, the benefits of 3D printing, including streamlined production processes and the ability to create complex geometries, continue to drive its widespread use.

- According to recent studies, the implementation of 3D printing technologies in manufacturing processes has led to operational cost savings of up to 15%, and a reduction in material waste of approximately 20%. These figures underscore the potential business value of 3D printing and its evolving role in modern manufacturing.

In-Depth Market Segmentation: 3D Desktop Printer Market

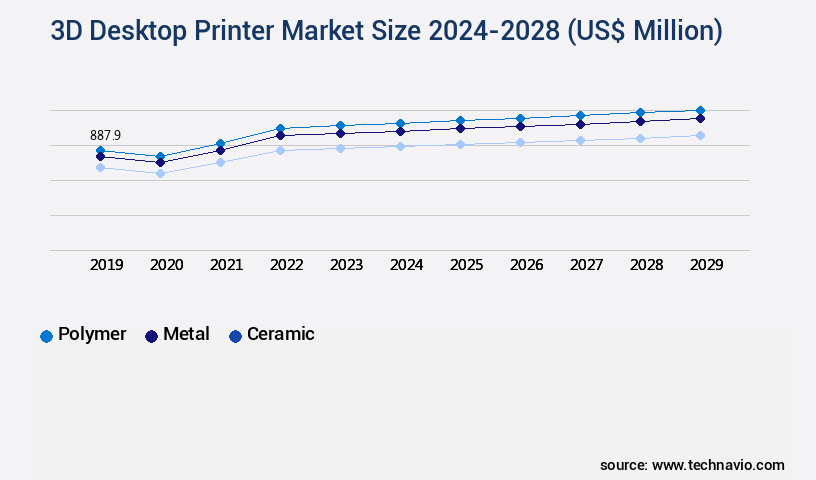

The 3d desktop printer industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Material

- Polymer

- Metal

- Ceramic

- Technology

- FDM

- SLS

- SLA

- Others

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

By Material Insights

The polymer segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with advancements in multi-material printing, slicing software algorithms, and print speed efficiency driving innovation. Desktop printer mechanics and electronics have seen significant improvements, with enhanced nozzle temperature control, support structures generation, and digital light processing. UV curing systems, material jetting, and powder bed fusion are also gaining traction. The polymer segment dominates the market, holding the largest share in 2022, due to the material's adaptability for assembling lightweight objects and its affordability. Researchers are exploring new polymers, such as polylactic acid, which is produced from renewable sources and offers a low melting point for lightweight 3D printing.

The Polymer segment was valued at USD 781.20 billion in 2018 and showed a gradual increase during the forecast period.

The market is further characterized by a focus on layer height resolution, part orientation optimization, and closed-loop control systems. Connectivity options, calibration procedures, and thermal management systems are essential considerations for desktop printers. With advancements in resin printing, post-processing techniques, and filament diameter tolerance, the market is poised for continued growth.

Regional Analysis

North America is estimated to contribute 34% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How 3D Desktop Printer Market Demand is Rising in North America Request Free Sample

The market in North America is experiencing notable expansion, with the US and Canada being key contributors to this growth. According to industry estimates, the market is poised for substantial expansion during the forecast period. This growth can be attributed to the increasing demand for customized products and the utilization of a diverse range of materials in various industries. North America is a significant hub for 3D desktop printer manufacturers, with companies such as 3D Systems, Carbon, Formlabs, HP, and Stratasys leading the charge.

IT investments and digitalization initiatives among enterprises and start-ups are significant drivers propelling the market's growth in the region. For instance, the implementation of these technologies can lead to operational efficiency gains of up to 30% and cost reductions in product development. The region's market is expected to witness robust growth due to these underlying factors.

Customer Landscape of 3D Desktop Printer Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the 3D Desktop Printer Market

Companies are implementing various strategies, such as strategic alliances, 3d desktop printer market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3D Systems Corp. - This company specializes in advanced 3D printing technology, providing solutions for various materials including plastic and metal, as well as metal casting.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3D Systems Corp.

- 3DCeram SAS

- Autodesk Inc.

- Canon Inc.

- Carbon Inc.

- Dassault Systemes SE

- Desktop Metal Inc.

- EOS GmbH

- Formlabs Inc.

- Fusion3 Design LLC

- General Electric Co.

- HP Inc.

- MATERIALISE NV

- Proto Labs Inc.

- Renishaw Plc

- Robert Bosch GmbH

- SHAPEWAYS HOLDINGS INC.

- Stratasys Ltd.

- voxeljet AG

- XYZPRINTING Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in 3D Desktop Printer Market

- In August 2024, Stratasys, a leading 3D printing solutions provider, announced the launch of its new Objet500 MultiMaterial 3D Printer, which can produce parts using up to five different materials in a single print job (Stratasys Press Release, 2024). This innovation expanded the company's product portfolio, catering to the growing demand for more complex and diverse 3D printed products.

- In November 2024, HP Inc. and Desktop Metal, a leading additive manufacturing solutions provider, announced a strategic partnership to co-develop desktop 3D printing systems using HP's Jet Fusion technology (HP Inc. Press Release, 2024). This collaboration aimed to combine HP's industrial 3D printing expertise with Desktop Metal's desktop 3D printing capabilities, targeting the mass production of metal parts in various industries.

- In March 2025, Formlabs, a pioneer in desktop stereolithography 3D printing, raised USD 110 million in a Series E funding round, bringing its total funding to over USD 325 million (Formlabs Press Release, 2025). This significant investment was aimed at accelerating the company's research and development efforts, expanding its global presence, and increasing production capacity to meet the growing demand for its 3D printing solutions.

- In May 2025, the European Union's Intellectual Property Office granted Formlabs a patent for its Low Force Stereolithography (LFS) technology, which uses a low force resin-handling system to improve the print quality and reduce material waste (Formlabs Press Release, 2025). This patent further solidified Formlabs' position as a leader in the desktop 3D printing market and provided it with a competitive edge in terms of technology innovation.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled 3D Desktop Printer Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

180 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 20.28% |

|

Market growth 2024-2028 |

USD 5205.5 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

16.34 |

|

Key countries |

US, China, Germany, Canada, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for 3D Desktop Printer Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth, with businesses increasingly adopting these innovative technologies for rapid prototyping and manufacturing. FDM (Fused Deposition Modeling) printers, a dominant segment in this market, require effective nozzle temperature control strategies to ensure consistent part quality. SLA (Stereolithography) printers, on the other hand, demand optimization of resin curing depth to enhance print precision. SLS (Selective Laser Sintering) printers necessitate powder bed leveling techniques for optimal part production, while DLP (Digital Light Processing) printers require light source intensity calibration for superior print results. MJF (Multi Jet Fusion) printers demand meticulous material jetting precision parameters to deliver high-quality parts. Desktop 3D printer part orientation significantly influences print quality and material selection criteria. Build volume limitations vary among different printer models, necessitating careful planning in operational and supply chain management. Support structure generation algorithms comparison is essential for minimizing material usage and improving print efficiency. Post-processing techniques, such as sanding and painting, contribute to improved surface finish. Desktop 3D printer print head design considerations and thermal management impact on print quality are crucial for ensuring consistent output. Closed-loop control systems and user-friendly software interfaces are essential for streamlining the desktop 3D printing process. Desktop 3D printer file format compatibility issues and connectivity options are essential considerations for businesses integrating these technologies into their workflows. Improving print speed efficiency through strategies like layer height optimization and calibration procedures for enhanced print accuracy are vital for maximizing ROI. Desktop 3D printer maintenance best practices, such as regular nozzle cleaning and bed leveling, ensure consistent part quality and prolong the life of the printer. In comparison to traditional manufacturing methods, desktop 3D printing offers businesses agility and cost savings, making it an attractive alternative for various industries.

What are the Key Data Covered in this 3D Desktop Printer Market Research and Growth Report?

-

What is the expected growth of the 3D Desktop Printer Market between 2024 and 2028?

-

USD 5.21 billion, at a CAGR of 20.28%

-

-

What segmentation does the market report cover?

-

The report is segmented by Material (Polymer, Metal, and Ceramic), Technology (FDM, SLS, SLA, and Others), and Geography (North America, Europe, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for 3D-printed jewelry, Adverse environmental impact of additive manufacturing

-

-

Who are the major players in the 3D Desktop Printer Market?

-

3D Systems Corp., 3DCeram SAS, Autodesk Inc., Canon Inc., Carbon Inc., Dassault Systemes SE, Desktop Metal Inc., EOS GmbH, Formlabs Inc., Fusion3 Design LLC, General Electric Co., HP Inc., MATERIALISE NV, Proto Labs Inc., Renishaw Plc, Robert Bosch GmbH, SHAPEWAYS HOLDINGS INC., Stratasys Ltd., voxeljet AG, and XYZPRINTING Inc.

-

We can help! Our analysts can customize this 3d desktop printer market research report to meet your requirements.

RIA -

RIA -