Access Control Solutions Market Size 2024-2028

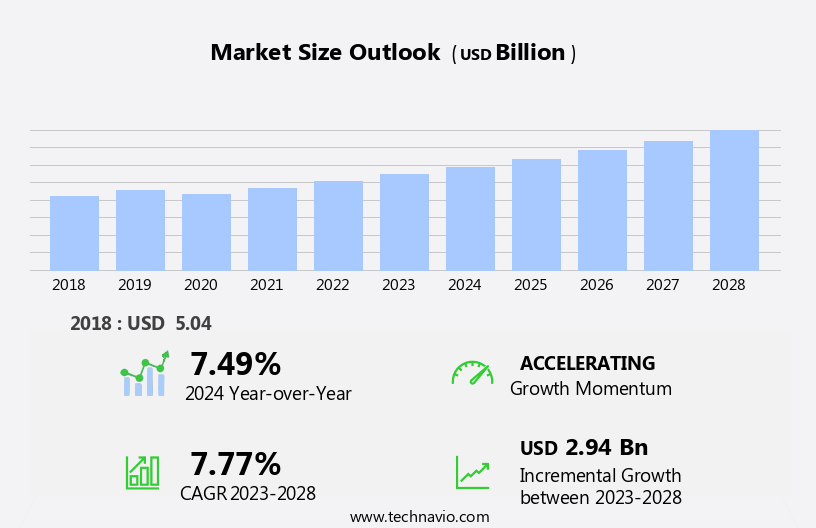

The access control solutions market size is forecast to increase by USD 2.94 billion, at a CAGR of 7.77% between 2023 and 2028.

- The market is witnessing significant growth, driven by the increasing awareness of sophisticated data security threats. With the digital transformation of businesses and the proliferation of IoT devices, the need for robust access control systems has become paramount. Furthermore, governments worldwide are initiating projects to implement biometric access control systems, adding impetus to the market's expansion. However, the market faces challenges as well. The lack of technological awareness among organizations about access control solutions may hinder market penetration. Companies must invest in marketing efforts and education to increase market reach and address this challenge effectively.

- The market is poised for growth, fueled by heightened security concerns and government initiatives, while facing challenges related to technological awareness. Companies seeking to capitalize on market opportunities must focus on marketing efforts and education to overcome these challenges and meet the evolving access control needs of businesses and governments.

What will be the Size of the Access Control Solutions Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, with dynamic market activities unfolding across various sectors. Remote management capabilities enable organizations to monitor and manage access permissions from anywhere, while fingerprint scanning and biometric authentication add an extra layer of security. Centralized management systems allow for efficient control of multiple access points, and wireless access control and RFID tags offer convenience and flexibility. Access control integration with alarm systems, reporting and analytics, and mobile access control enhances security and facilitates real-time monitoring. Perimeter security solutions, multi-factor authentication, and threat detection further strengthen security measures. Access control policies, Physical Security, and audit trails ensure compliance with regulations and provide valuable data for risk assessment.

Security cameras, door controllers, and access control panels offer additional layers of protection, while support services, network access control, user management, and installation services ensure seamless implementation and maintenance. Authentication protocols, voice recognition, Bluetooth beacons, and incident response capabilities further enhance the functionality of access control systems. Door hardware, smart cards, proximity readers, deadbolt locks, security software, Iris Recognition, Facial Recognition, and card readers are integral components of comprehensive access control solutions. Compliance regulations continue to evolve, emphasizing the importance of ongoing adaptation and innovation in the market.

How is this Access Control Solutions Industry segmented?

The access control solutions industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Accounts management and identity synchronization

- Unified authentication

- Others

- End-user

- Government

- BFSI

- Healthcare

- Transportation

- Component

- Hardware (Readers, Controllers, Locks, Biometrics)

- Software (Management Software, Analytics)

- Services (Installation, Maintenance, Integration)

- Technology

- Biometric (Fingerprint, Facial, Iris, Voice)

- Card-based (Proximity, Smart Card)

- Keypad-based

- Mobile-based

- Deployment Model

- On-Premise

- Cloud-Based (ACaaS)

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

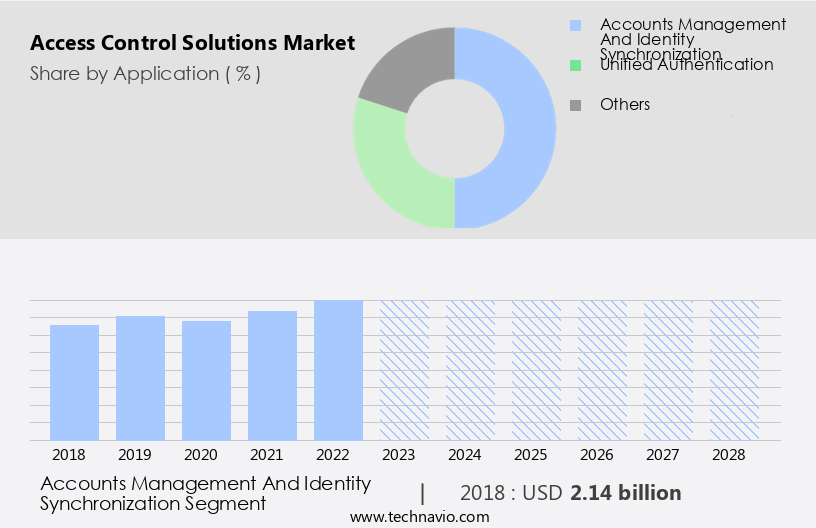

By Application Insights

The accounts management and identity synchronization segment is estimated to witness significant growth during the forecast period.

End-users in sectors such as government, healthcare, and financial services are increasingly focusing on managing access to confidential information and applications dispersed across internal and external systems. In response to this need, enterprises are embracing multi-channel user access, including cloud, social, and mobile platforms. Simultaneously, they must address business requirements like compliance and audit reporting. Access control solutions play a crucial role in mitigating risk and ensuring compliance by monitoring and securing user access in multi-perimeter environments. These solutions provide essential features like automated account provisioning, access request fulfillment, password management, and user access control to target systems.

Furthermore, advanced access control solutions offer capabilities such as biometric authentication, Video Surveillance, risk assessment, and centralized management. Access control systems employ various authentication protocols, including two-factor authentication and single sign-on, to enhance security. Additionally, network access control, user management, and access control integration are critical components of comprehensive access control solutions. Access control panels, support services, and installation services ensure seamless implementation and maintenance. Access control policies, door controllers, proximity readers, and smart cards are integral components of these systems. Compliance regulations mandate incident response, maintenance services, and access control training to maintain security and mitigate potential threats.

Access control solutions also integrate with alarm systems, perimeter security, and Threat Detection Systems to provide a holistic security approach. Wireless access control, RFID tags, Bluetooth beacons, and voice recognition are emerging technologies enhancing access control capabilities. In summary, access control solutions are essential for enterprises to secure their valuable applications and data, enforce security policies, and ensure business-driven identity governance in today's complex IT environments.

The Accounts management and identity synchronization segment was valued at USD 2.14 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

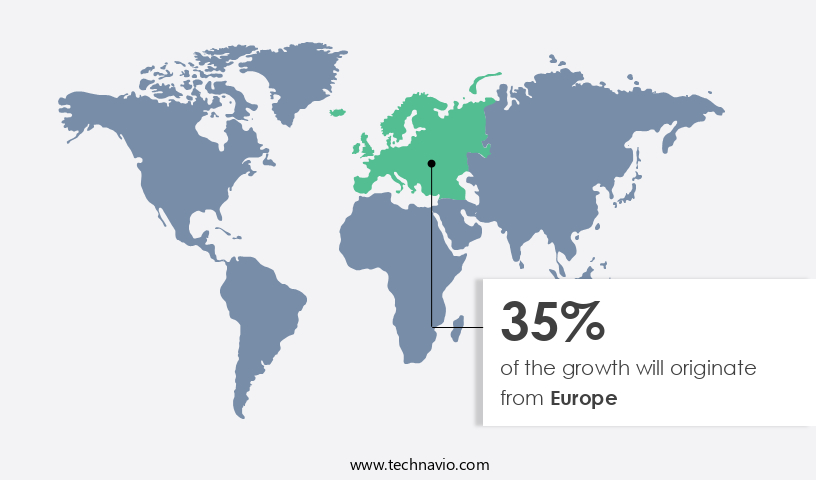

Europe is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in Europe is experiencing significant growth, driven by the early adoption of advanced technologies and a well-established end-user base. Advanced economies, such as Germany, France, and the United Kingdom, currently dominate the market due to their robust industrial sectors and high demand for security solutions. However, emerging economies, including Poland, Romania, and the Czech Republic, are poised to contribute significantly to the market's growth in the future. Technological innovations, such as cloud-based access control, biometric authentication, and remote management, are transforming the access control landscape. Two-factor authentication, video surveillance, and alarm systems provide an additional layer of security, while access control policies and compliance regulations ensure data privacy and security.

Centralized management systems, wireless access control, and mobile access control offer flexibility and convenience. Physical security measures, such as electric strikes, magnetic locks, and deadbolt locks, continue to be essential components of access control systems. Access control panels, door controllers, and authentication protocols ensure seamless integration of various security components. User management, incident response, and maintenance services ensure optimal system performance and user experience. Network access control, threat detection, and reporting and analytics provide valuable insights into system performance and potential vulnerabilities. Proximity readers, RFID tags, and smart cards offer contactless access control solutions. Multi-factor authentication, voice recognition, and facial recognition provide enhanced security and convenience.

The market in Europe is expected to witness high growth due to the increasing adoption of these advanced technologies across various industries, including BFSI, healthcare, and manufacturing. Compliance regulations, such as GDPR and HIPAA, are driving the demand for access control solutions that offer robust data encryption, audit trails, and incident response capabilities. Installation services and support services ensure seamless implementation and maintenance of access control solutions.

Market Dynamics

The Access Control Solutions Market is booming, driven by biometric access control and RFID access control for secure access solutions. Cloud-based access control and facial recognition systems enhance efficiency in the commercial access control market and healthcare access control market. Touchless access control and AI-driven access security cater to modern safety needs, while mobile-based access control and GDPR-compliant access solutions ensure flexibility and compliance. Key phrases like biometric access control for commercial buildings, RFID access control for data centers, cloud-based access control for smart cities, facial recognition systems for airport security, touchless access control for healthcare facilities, AI-driven access security for government buildings, mobile-based access control for residential properties, scalable access control systems for industrial facilities, GDPR-compliant access solutions for European businesses, and cost-effective access control for small businesses 2025 shape the industry's future.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Access Control Solutions Industry?

- The increasing recognition of complex data security risks serves as the primary catalyst for market growth.

- The market is witnessing significant growth due to the increasing threat of cyber-attacks and data breaches. As businesses increasingly rely on digital data and applications, securing access to these assets has become a top priority. Access control solutions offer a secure and convenient way to manage access to digital assets, providing businesses with expert security capabilities and technologies without the need for extensive investment and management of their own infrastructure. Two essential components of access control solutions are electric strikes and magnetic locks, which ensure physical security by controlling access to buildings and rooms. Additionally, intrusion detection systems, video surveillance, biometric authentication, and two-factor authentication provide an extra layer of security against unauthorized access.

- Access control policies and audit trails help businesses maintain regulatory compliance and monitor access activity. Cloud-based access control solutions offer flexibility and scalability, allowing businesses to manage access to their digital assets from anywhere, at any time. Data encryption and audit trails ensure data security and compliance, while video surveillance provides an additional layer of security against potential threats. The market is expected to continue growing as businesses seek to mitigate the risks associated with digital data and applications.

What are the market trends shaping the Access Control Solutions Industry?

- The implementation of biometric access control systems is becoming increasingly mandated by government initiatives, making it a prominent market trend. This shift towards advanced security measures is a professional and effective solution for enhancing access control and security.

- Access control solutions have gained significant importance in securing facilities and enhancing operational efficiency. Remote management of these systems has become increasingly popular, enabling administrators to control access permissions from anywhere. Biometric technologies, such as fingerprint scanning and facial recognition, offer enhanced security by providing unique identification for each individual. Centralized management of access control systems allows for wireless access control using RFID tags and mobile devices, providing convenience and flexibility. Integration of access control systems with security cameras, alarm systems, and reporting and analytics tools enhances security and facilitates comprehensive monitoring. Perimeter security measures, including multi-factor authentication, add an extra layer of protection against unauthorized access.

- The market is driven by the need for advanced security solutions and the increasing adoption of technology in various industries. Governments have prioritized the use of biometric access control systems for heightened security checks, particularly in airports, due to their ability to verify individuals based on behavioral and physiological characteristics. These systems offer a more reliable and efficient solution compared to traditional access control methods, ensuring a harmonious balance between security and productivity.

What challenges does the Access Control Solutions Industry face during its growth?

- The absence of technological awareness regarding access control solutions poses a significant challenge to the industry's growth. Companies and organizations may struggle to implement effective security measures without understanding the latest advancements and benefits of access control technologies. This lack of knowledge can hinder progress and limit the potential for innovation within the industry.

- The market has faced challenges in the past due to limited awareness among end-users, resulting in slow adoption rates. Advanced access control systems, such as authentication protocols, access control panels, network access control, user management, voice recognition, Bluetooth beacons, single sign-on, and threat detection, were not widely recognized in various industries and organizations. This trend was more pronounced in emerging economies. However, as technology advances, the market is poised for growth during the forecast period. A common misconception exists regarding the implementation and management costs of these systems. Despite the benefits of enhanced security and improved user experience, some organizations have been hesitant to invest in access control solutions due to perceived high costs.

- However, as technology continues to evolve and become more cost-effective, the market is expected to expand and offer significant value to businesses worldwide. Access control systems, including door controllers and proximity readers, play a crucial role in securing facilities and protecting valuable assets. By implementing these solutions, organizations can streamline their security processes, minimize risks, and ensure the safety of their employees and customers.

Exclusive Customer Landscape

The access control solutions market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the access control solutions market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, access control solutions market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ASSA ABLOY AB - This company specializes in access control systems, providing innovative solutions such as Cliq, SMARTair, Incedo Business, and Aperio. Their offerings ensure secure and efficient entry management for various industries. The solutions are designed to integrate seamlessly with diverse business environments, enhancing security and convenience.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ASSA ABLOY AB

- Brivo Inc.

- Broadcom Inc.

- Centrify Corp.

- Cisco Systems Inc.

- Cloudastructure Inc.

- Datawatch Systems Inc.

- dormakaba Holding AG

- Feenics Inc.

- Honeywell International Inc.

- International Business Machines Corp.

- M3T Corp.

- Microsoft Corp.

- Motorola Solutions Inc.

- Okta Inc.

- Oracle Corp.

- Ping Identity Corp.

- SecureAuth Corp.

- Thales Group

- Vector Security Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Access Control Solutions Market

- In January 2024, HID Global, a leading provider of trusted identity solutions, announced the launch of its new Seos-enabled access control readers, expanding its Seos platform's capabilities to include contactless smart card technology (HID Global Press Release, 2024). This development aimed to meet the growing demand for touchless access control systems in response to the COVID-19 pandemic.

- In March 2024, Tyco International plc, a leading provider of security products and services, entered into a strategic partnership with Bosch Building Technologies to offer integrated security and building automation solutions. The collaboration aimed to provide customers with a more comprehensive and efficient security solution, combining access control, video surveillance, and building management systems (Tyco International Press Release, 2024).

- In May 2024, LenelS2, a global leader in advanced security systems, raised USD100 million in a funding round led by Blackstone Growth. The investment will support LenelS2's continued growth and product development, particularly in the areas of cloud services and artificial intelligence (LenelS2 Press Release, 2024).

- In January 2025, the European Union Agency for Cybersecurity (ENISA) published new guidelines for secure implementation of access control systems in critical infrastructure. The guidelines aim to strengthen cybersecurity measures and protect against potential threats, including insider attacks and cyber-physical risks (ENISA Press Release, 2025).

Research Analyst Overview

- In the dynamic market, various technologies and trends are shaping the industry's future. Blockchain technology is revolutionizing access control by providing secure, decentralized solutions for managing identities and permissions. Remote monitoring and real-time analytics enable organizations to detect and respond to security threats in real-time. APIs facilitate seamless integration with other systems, such as inventory management and data analytics. Multi-tenant access control caters to the needs of organizations with multiple clients or departments, while asset tracking ensures accountability and security. User behavior analytics and AI-powered access control provide advanced security features, including predictive analytics and tailgate detection.

- Open standards and IoT integration enable interoperability and connectivity across various systems, from parking access control and elevator access to man-trap systems and boom gates. Security audits, Penetration Testing, vulnerability assessments, and incident management are essential components of a comprehensive access control strategy. Role-based access control and employee management streamline access and permissions for workforce members, while emergency response and visitor management ensure safety and compliance. Zone-based access control and time-based access control offer granular control and flexibility for organizations. Behavioral biometrics and predictive analytics enhance security by identifying anomalous user behavior and potential threats.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Access Control Solutions Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

165 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.77% |

|

Market growth 2024-2028 |

USD 2.94 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.49 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Access Control Solutions Market Research and Growth Report?

- CAGR of the Access Control Solutions industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across Europe, North America, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the access control solutions market growth of industry companies

We can help! Our analysts can customize this access control solutions market research report to meet your requirements.

RIA -

RIA -