Americas Immunochemistry Market Size 2024-2028

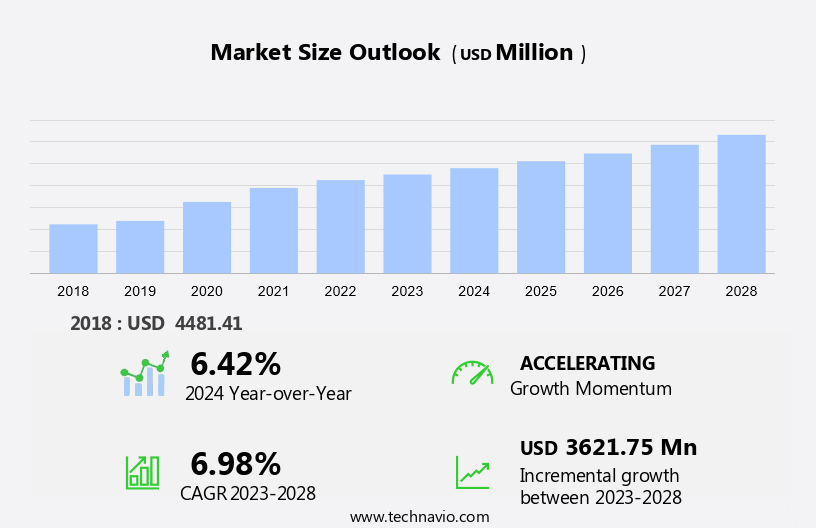

The Americas immunochemistry market size is forecast to increase by USD 3.62 billion at a CAGR of 6.98% between 2023 and 2028.

- The market is witnessing significant growth due to several key factors. The region's aging population is a major driver, as the increasing prevalence of chronic diseases among the elderly population necessitates frequent diagnostic tests. Additionally, the market is witnessing a rise in new product launches, which is expanding the product portfolio and catering to the diverse needs of customers. The market is experiencing significant growth as artificial intelligence is increasingly used to analyze biomarkers, enabling faster and more accurate diagnostic results. However, the lack of trained professionals In the field poses a challenge, as it may hinder the accurate execution of immunochemistry tests and affect market growth. Overall, the market is expected to experience strong growth In the coming years, driven by these trends and challenges.

What will be the size of the Americas Immunochemistry Market during the forecast period?

- The Immunochemistry market In the Americas is experiencing significant growth due to the increasing prevalence of chronic illnesses, particularly cancer diseases and cardiovascular disorders, In the geriatric population. Immunochemistry products, including IHC (Immunohistochemistry) and related diagnostic tools, play a crucial role in disease diagnosis and personalized medicine. Healthcare professionals rely on these technologies to improve diagnostic accuracy and enhance patient care. Automation, digital imaging, and machine learning are driving innovation In the Immunochemistry market. IHC protocols are being optimized to reduce manual labor and increase throughput. RNA and transcriptome sequencing are also gaining traction, offering new opportunities for mutation-specific immunochemistry tests.

- The market is being shaped by advancements in clinical diagnostics, with a focus on non-small-cell lung cancer and other cancer types. Mass spectrometric detection and antibody-based assays are key technologies enabling the development of multiplexed IHC tests. As the demand for early and accurate disease diagnosis continues to grow, the market is expected to expand further.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Consumables

- Equipment

- Application

- Infectious disease

- Cardiology

- Oncology

- Autoimmune disease

- Nephrology and others

- Geography

- Americas

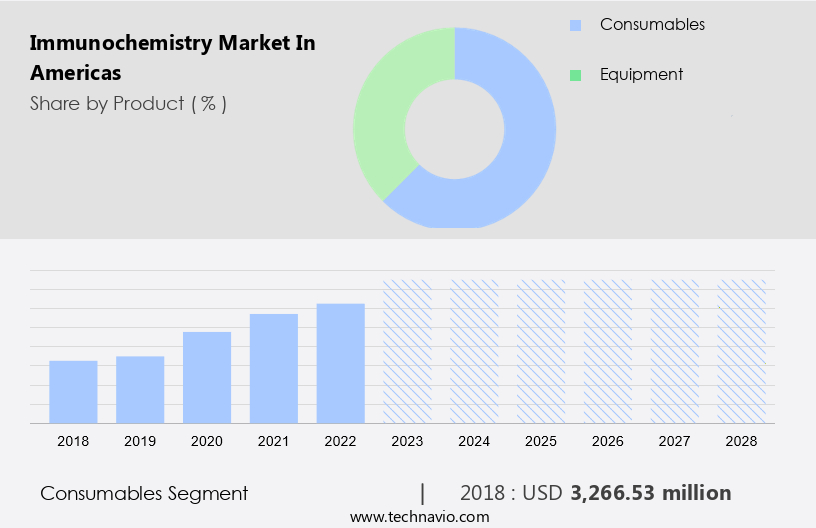

By Product Insights

- The consumables segment is estimated to witness significant growth during the forecast period.

The Immunochemistry Market In the Americas focuses on the consumption of essential products for performing immunochemical assays, diagnostics, and research activities. Key consumables include immunoassay, antibodies, and enzymes. Immunoassay kits, such as ELISA, offer ready-to-use components for detecting proteins, hormones, or antibodies in samples. Antibodies, including monoclonal and polyclonal, target specific antigens or proteins for use as primary or secondary reagents. Substrates and enzymes, like chromogenic, fluorogenic, or chemiluminescent, amplify and detect signals in immunochemical assays. This market caters to various applications, including cancer diagnostics, chronic diseases, neurological disorders, autoimmune conditions, and cardiovascular disorders. Healthcare professionals in hospitals and diagnostic laboratories utilize immunochemistry products for disease diagnosis, personalized medicine, and research.

Technological advancements, such as automation, digital imaging, RNA sequencing, transcriptome sequencing, companion diagnostics, and machine learning, enhance the market's growth.

Get a glance at the market share of various segments Request Free Sample

The Consumables segment was valued at USD 3.26 billion in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Americas Immunochemistry Market?

The growing geriatric population is the key driver of the market.

- The aging population is witnessing a significant increase, leading to a corresponding rise In the prevalence of chronic diseases, cancer, neurological disorders, autoimmune conditions, and infectious diseases. Immunochemistry assays are essential for diagnosing and managing these conditions, particularly in elderly individuals who are more susceptible. According to the Population Reference Bureau, the elderly population in Americas is projected to grow by 47% from 58 million in 2022 to 82 million in 2050. Immunochemistry products, including Immunohistochemistry (IHC) and clinical diagnostics, play a pivotal role in disease diagnosis. Advanced technologies such as digital imaging, RNA sequencing, and transcriptome sequencing are revolutionizing diagnostic accuracy.

- Companion diagnostics, machine learning, and IHC protocols are enabling personalized medicine and improving treatment outcomes. Diseases such as cardiovascular disorders, non-small-cell lung cancer, diabetes mellitus, and chronic conditions continue to drive demand for immunochemistry-based diagnostic tools. Monoclonal antibodies, antibody fragments, and antibody-drug conjugates are key components of these tests. Mass spectrometric detection and multiplexed IHC are also gaining popularity due to their ability to provide multiple diagnostic results from a single sample. Immunochemistry products are essential diagnostic facilities for hospitals and diagnostic laboratories.

What are the market trends shaping the Americas Immunochemistry Market?

Rising new product launches is the upcoming trend In the market.

- The market is experiencing significant growth due to the introduction of innovative products that cater to the needs of healthcare professionals and researchers. These new launches include advanced technologies, improved instrumentation, and sophisticated assays, enhancing diagnostic accuracy in various medical specialties. The market is witnessing a focus on chronic conditions such as cancer, cardiovascular disorders, chronic diseases, neurological disorders, autoimmune conditions, and infectious diseases.

- Technological advancements in areas like automation, digital imaging, RNA sequencing, transcriptome sequencing, and companion diagnostics are revolutionizing disease diagnosis and personalized medicine. Furthermore, machine learning and IHC protocols are streamlining the diagnostic process, while multiplexed IHC and mass spectrometric detection offer increased sensitivity and specificity. Monoclonal antibodies, antibody fragments, and antibody-drug conjugates are essential components of these advanced solutions. Overall, the market is poised for expansion, driven by the evolving needs of healthcare facilities and diagnostic laboratories.

What challenges does Americas Immunochemistry Market face during the growth?

Lack of trained professionals is a key challenge affecting the market growth.

- Immunochemistry plays a crucial role in disease diagnosis, particularly in identifying cancer, chronic diseases, neurological disorders, and autoimmune conditions. Healthcare professionals rely on immunochemistry products, such as Immunohistochemistry (IHC) and clinical diagnostics, for diagnostic accuracy. The geriatric population and the rise of chronic conditions, including cardiovascular disorders, diabetes mellitus, and infectious diseases, necessitate advanced diagnostic tools. Automation, digital imaging, RNA sequencing, and transcriptome sequencing are transforming the diagnostics landscape. Companion diagnostics, which combine immunochemistry with other technologies, offer personalized medicine solutions for non-small-cell lung cancer and other mutation-specific diseases. Machine learning and IHC protocols enhance disease diagnosis, enabling multiplexed IHC and mass spectrometric detection.

- Monoclonal antibodies, antibody fragments, and antibody-drug conjugates are essential components of immunochemistry products. Hospitals & Diagnostic Laboratories benefit from these advancements, ensuring timely and accurate diagnosis for their patients. Challenges, such as limited availability of trained specialists, high costs, and resource constraints, persist In diagnostic facilities. However, innovations in technology and the increasing adoption of automation and digital solutions are addressing these challenges, making immunochemistry a vital component of the healthcare industry.

Exclusive Americas Immunochemistry Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Agilent Technologies Inc.

- Becton Dickinson and Co.

- Bio Rad Laboratories Inc.

- Bio Techne Corp.

- bioMerieux SA

- Danaher Corp.

- DiaSorin SpA

- Enzo Biochem Inc.

- F. Hoffmann La Roche Ltd.

- Fujirebio Holdings Inc.

- Grifols SA

- Hologic Inc.

- Merck and Co. Inc.

- Mindray Bio medical Electronics Co. Ltd.

- PerkinElmer Inc.

- Quanterix Corp.

- Randox Laboratories Ltd.

- Siemens AG

- Sysmex Corp.

- Thermo Fisher Scientific Inc.

- Tosoh Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is witnessing significant growth due to the increasing prevalence of chronic diseases, cancer, and neurological disorders. The geriatric population, with its higher susceptibility to various health conditions, is a key driver for the market's expansion. Healthcare professionals are increasingly relying on immunochemistry products to enhance diagnostic accuracy and improve patient outcomes. Automation and digital imaging are transforming the landscape of immunochemistry. RNA sequencing and transcriptome sequencing are revolutionizing disease diagnosis, enabling a deeper understanding of the molecular mechanisms underlying various conditions. Companion diagnostics, which facilitate personalized medicine, are gaining popularity in clinical diagnostics.

Immunochemistry products, including IHC (Immunohistochemistry) and immunohistochemistry kits, are essential tools for hospitals and diagnostic laboratories. IHC protocols are continually evolving, with multiplexed IHC and mass spectrometric detection techniques offering improved sensitivity and specificity. Cardiovascular disorders, cancer, and chronic illnesses are major areas of application for immunochemistry. Non-small-cell lung cancer, for instance, is a significant focus due to the development of mutation-specific immunochemistry tests. Diagnostic facilities are increasingly adopting these advanced tests to provide accurate and timely diagnoses. Machine learning algorithms are being integrated into immunochemistry workflows to streamline processes and enhance diagnostic accuracy. The use of monoclonal antibodies, antibody fragments, and antibody-drug conjugates is on the rise, reflecting the growing importance of immunochemistry in disease diagnosis and treatment. Chronic conditions such as diabetes mellitus, autoimmune diseases, and nephrological diseases are other significant applications for immunochemistry. Infectious diseases are also a growing area of interest, with immunochemistry playing a crucial role in disease detection and monitoring.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

160 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.98% |

|

Market Growth 2024-2028 |

USD 3.62 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.42 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across the Americas

- A thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -