APAC Industrial Robotics Market Size 2024-2028

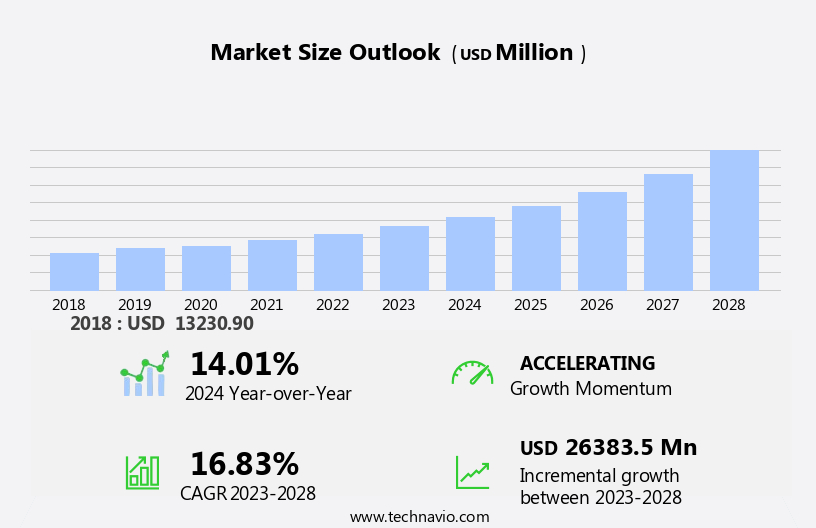

The APAC industrial robotics market size is forecast to increase by USD 26.38 billion at a CAGR of 16.83% between 2023 and 2028. In the Asia Pacific region, the industrial robotics market is experiencing significant growth, driven by the automotive and food manufacturing sectors. Automation technology, including collaborative robotics and material handling segments, is increasingly being adopted to enhance productivity and efficiency. Mechanical machines, reprogrammable for flexibility, are becoming essential in manufacturing processes. The integration of Internet of Things (IoT) with robotics is a notable trend, enabling real-time monitoring and predictive maintenance. However, the lack of skilled workers to operate industrial robots poses a challenge for market expansion.

The industrial robotics market in the APAC region is rapidly expanding, driven by the demand for AI-enabled robots across various sectors, including food and beverages, semiconductors, and high-tech electronics. SCARA robots and cylindrical robots are increasingly used for tasks requiring precision and efficiency. In the metal and machinery industry, robotic manipulators and robotic controllers enhance productivity, while robot sensors improve operational accuracy. The advanced robotic manipulator, powered by cutting-edge semi conductors, operates with precision thanks to its sophisticated robotic controller. The plastics and chemical products sector benefits from energy-efficient robotics solutions that streamline materials handling.

Additionally, modular robotics and nanorobots are emerging trends, providing flexibility and advanced capabilities. As industries focus on high-quality products, innovations in mechanical machine and robotic systems continue to reshape the landscape of manufacturing in the APAC region, fostering growth across diverse applications. Further, AI enabled robots, including SCARA robot and modular robot, are revolutionizing the food and beverages sector, as well as the rubber and plastics industry, by providing energy efficient robotics solutions and high quality products through advanced robotic manipulators and controllers, while also making significant impacts in the high tech electronics sector and metal and machinery sector, alongside emerging fields like nanorobotics

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

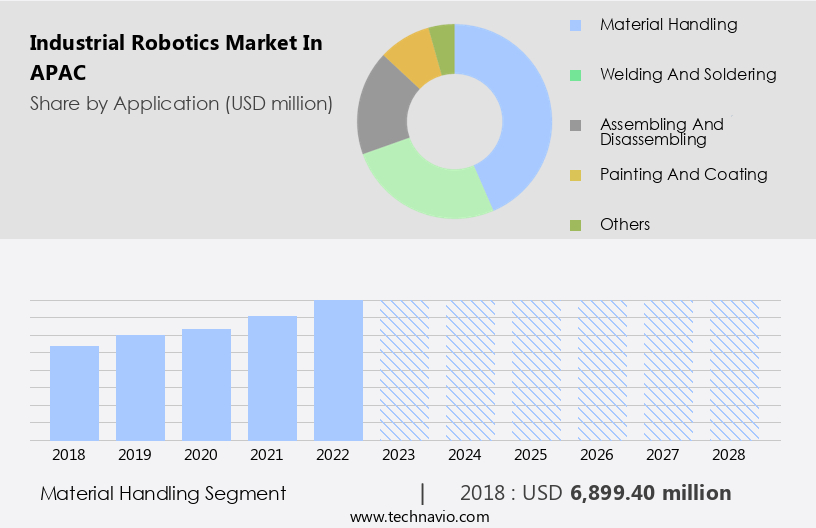

- Material handling

- Welding and soldering

- Assembling and disassembling

- Painting and coating

- Others

- End-user

- Automotive

- Electrical and electronics

- Metal and heavy machinery

- Food and beverages

- Others

- Geography

- APAC

- China

- India

- Japan

- South Korea

- APAC

By Application Insights

The material handling segment is estimated to witness significant growth during the forecast period. In the dynamic industrial landscape of Asia Pacific (APAC), material handling is a prominent application driving the expansion of the industrial robotics market. The thriving manufacturing and e-commerce sectors in this region necessitate efficient automation solutions. Robots, including autonomous mobile robots (AMRs) and robotic manipulators, are increasingly utilized in warehouses and factories for tasks such as picking, packing, and palletizing. E-commerce giants like Alibaba and JD.Com employ order fulfillment robots to streamline their operations. Additionally, automobile manufacturers such as Toyota and Hyundai leverage robotics for assembly line processes. The APAC industrial robotics market is marked by a wave in investments, groundbreaking technologies, and strategic partnerships to cater to the escalating demand for material handling automation.

Get a glance at the market share of various segments Request Free Sample

The material handling segment accounted for USD 6.90 billion in 2018 and showed a gradual increase during the forecast period.

Our market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The swell in demand for industrial robots is the key driver of the market. The Industrial Robotics market in Asia Pacific has experienced significant growth due to technological advancements and research and development investments. Companies are automating their manufacturing processes using industrial robots to enhance productivity and operational efficiency. These robots offer minimal error margins and improved safety for employees. With increasing competition and the need for greater production capacity, small and medium-sized businesses are turning to industrial robotics.

Labor shortages, particularly in countries like Japan, are further driving the demand for automation solutions. As a result, market players are anticipated to boost their investments in robotics and related technologies to meet the escalating demand. Industrial Robotics encompasses various types of robots such as Collaborative robots, Articulated robots, SCARA robots, and Robot arms, which are increasingly being adopted for material handling applications.

Market Trends

The integration of IoT with robotics is the upcoming trend in the market. The Industrial Robotics Market in the APAC region is experiencing significant growth due to the integration of automation technology in various sectors, including the Automotive and Food Manufacturing industries. The implementation of automation technology, such as collaborative robotics and material handling systems, has revolutionized manufacturing processes. Mechanical machines, reprogrammable for various applications, are increasingly being adopted for their efficiency and precision. companies are offering advanced IoT-enabled articulated robots, providing real-time data on machine performance and enhancing overall productivity. The Food Manufacturing sector is expected to witness notable growth due to the need for hygienic and efficient production processes. In the Automotive sector, the demand for high-precision assembly and painting processes is driving the adoption of industrial robots.

Market Challenge

The lack of skilled workers to operate industrial robots is a key challenge affecting the market growth. Industrial robots have gained significant traction in various industries across Asia Pacific, particularly in sectors such as semiconductors, electronic devices, and manufacturing. These robots are utilized for applications like painting, assembly, welding, palletizing, packaging, and labeling. However, the market expansion is hampered by the shortage of a skilled workforce. Industrial facilities find it challenging to recruit workers with the necessary qualifications and expertise to operate and manage robotic systems. Robotic technology offers enhanced precision and efficiency in industrial processes. Nevertheless, the successful implementation of these advanced solutions necessitates the involvement of skilled labor. The intricacies of data exchange between robots and the production line require a well-trained workforce. Unfortunately, acquiring a competent workforce with the required technical knowledge is a significant hurdle. Consequently, unskilled operators cannot effectively utilize robots, making it a major limitation to their adoption in manufacturing facilities.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

ABB Ltd. - The company offers a comprehensive range of industrial robots under the brand IRB series to help various manufacturers, including automotive manufacturers, improve productivity, product quality, and worker safety.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aurotek Corp. Inc.

- Daikin Industries Ltd.

- DENSO Corp.

- Durr AG

- FANUC Corp.

- General Electric Co.

- Hans Laser Technology Industry Group Co. Ltd.

- Kawasaki Heavy Industries Ltd.

- KUKA AG

- MIDEA Group Co. Ltd.

- Mitsubishi Electric Corp.

- NACHI FUJIKOSHI Corp.

- OMRON Corp.

- Panasonic Holdings Corp.

- Seiko Epson Corp.

- Stellantis NV

- Universal Robots AS

- Yamaha Motor Co. Ltd.

- Yaskawa Electric Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is witnessing significant growth due to the increasing adoption of automation technology in various industries. Robots, such as collaborative robots, AI-enabled robots, articulated robots, robot arms, SCARA robots, and cartesian robots, are increasingly being used in sectors like semiconductors, electronic devices, automotive, and food manufacturing. These robots are reprogrammable and offer high-quality products through automation applications. Collaborative robotics, a segment of the industrial robotics market, is gaining popularity due to its ability to work alongside human workers. These robots are equipped with sensors and controllers, enabling them to interact safely with their human counterparts. Material handling is a major application area for industrial robots, with applications ranging from palletizing and packaging and labeling to soldering and welding.

Additionally, other applications include assembly, painting, and dispensing. The microelectronics industry, warehouses, metals industry, and automotive sector are some of the key industries driving the growth of the market. Mobile robots and parallel robots are also gaining traction in various industries due to their flexibility and versatility. Industrial robots are used in various industries for automation applications, including material handling, assembly, and disassembling, painting and dispensing, and soldering and welding. These robots are essential for producing high-quality products efficiently and cost-effectively. Robotic manipulators, equipped with microphones, cameras, and other sensors, are used in various applications, including material handling, automotive manufacturing, and food manufacturing.

Further, the use of these robots is expected to increase in the coming years due to their ability to improve productivity and reduce labor costs. In conclusion, the market is witnessing significant growth due to the increasing adoption of automation technology in various industries. The use of industrial robots, including collaborative robots, AI-enabled robots, and various types of robotic arms, is expected to continue growing in the coming years, driven by the need for high-quality products and efficient production processes.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

170 |

|

Base year |

2023 |

|

Historic period |

2017-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 16.83% |

|

Market growth 2024-2028 |

USD 26.38 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

14.01 |

|

Key companies profiled |

ABB Ltd., Aurotek Corp. Inc., Daikin Industries Ltd., DENSO Corp., Durr AG, FANUC Corp., General Electric Co., Hans Laser Technology Industry Group Co. Ltd., Kawasaki Heavy Industries Ltd., KUKA AG, MIDEA Group Co. Ltd., Mitsubishi Electric Corp., NACHI FUJIKOSHI Corp., OMRON Corp., Panasonic Holdings Corp., Seiko Epson Corp., Stellantis NV, Universal Robots AS, Yamaha Motor Co. Ltd., and Yaskawa Electric Corp. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -