Automation Testing Market Size 2024-2028

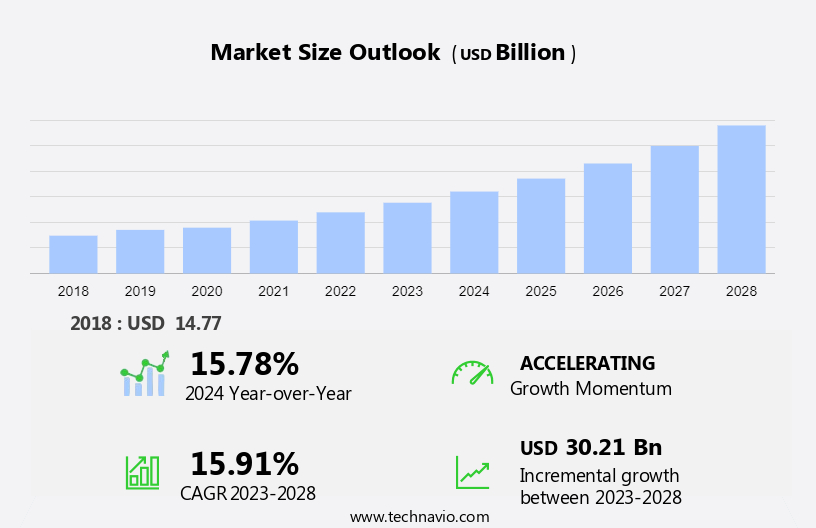

The automation testing market size is forecast to increase by USD 30.21 bn at a CAGR of 15.91% between 2023 and 2028.

- The market is experiencing significant growth due to several key trends. The increasing demand for continuous delivery and continuous integration (CD/CI) is driving market growth, as organizations seek to streamline their software development processes and release new features and updates more frequently. Additionally, the rapid digital transformation across industries is leading to an increased complexity in automation testing tool implementation. This complexity requires specialized skills and resources, creating opportunities for automation testing service providers.

- Furthermore, the need for faster time-to-market and improved product quality is also fueling the adoption of automation testing solutions. However, challenges such as high implementation costs and the need for significant upfront investment in tools and infrastructure persist.Despite these challenges, the benefits of automation testing, including increased efficiency, improved accuracy, and reduced human error, make it an essential component of modern software development.

What will be the Size of the Automation Testing Market During the Forecast Period?

- The market is experiencing significant growth due to the increasing adoption of DevOps methodologies and Agile testing In the digitalization trend. Artificial intelligence and machine learning technologies are revolutionizing testing by enabling static and dynamic analysis, enhancing test coverage, and improving resource efficiency. The market is segmented based on testing type, including application testing, compliance testing, and service segment. Large enterprises and small enterprises across various verticals, such as BFSI, electronic health records systems, and record keeping, are prioritizing test strategy and planning for critical functionalities and high-risk areas. Cloud solutions are increasingly being adopted for test environment setup and execution.

- Legacy systems and software applications require specialized testing approaches, making test planning and quality assurance essential for ensuring compliance and maintaining high-quality standards.

How is this Automation Testing Industry segmented and which is the largest segment?

The automation testing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

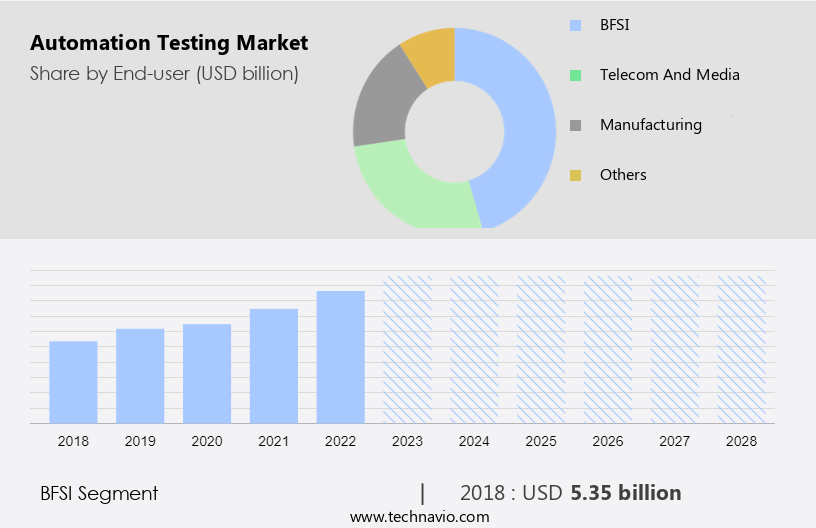

- End-user

- BFSI

- Telecom and media

- Manufacturing

- Others

- Deployment

- On-premises

- Cloud-based

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- South America

- Middle East and Africa

- North America

By End-user Insights

The bfsi segment is estimated to witness significant growth during the forecast period. Automation testing plays a pivotal role In the banking, financial services, and insurance (BFSI) sector, where security and accuracy are paramount. Given the sensitive nature of financial transactions and customer data, robust testing is essential to ensure error-free software systems. Automation testing facilitates regular security checks, identifying vulnerabilities, and verifying the functionality of banking modules such as account management, loan processing, and payment gateways. Automated functional tests ensure software adherence to specified requirements, while regression testing maintains existing functionalities amidst frequent updates. Digitalization trends and Agile testing methodologies have fueled the adoption of automation testing. Artificial Intelligence (AI) and Machine Learning (ML) are increasingly integrated into automation testing for enhanced efficiency and test coverage.

Cloud solutions offer cost savings and flexibility, while service segments include managed services and implementation services. Testing types encompass static analysis, dynamic testing, and compliance testing. Organization size, from large enterprises to small businesses, benefits from automation testing's resource efficiency and efficiency improvement. Mission-critical activities, critical functionalities, high-risk areas, and legacy systems require stringent testing. Automation testing's strategic approach to risk management and product lifecycle evolution continues to drive growth in this market.

Get a glance at the market report of various segments Request Free Sample

The BFSI segment was valued at USD 5.35 bn in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

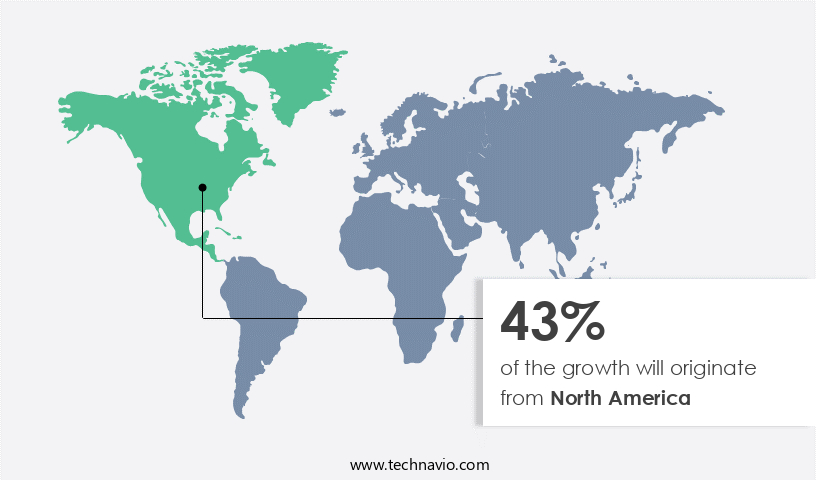

North America is estimated to contribute 43% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The North American market for automation testing is driven by the region's tech-forward economy and the increasing digitalization trends across various industries. Finance, healthcare, retail, and manufacturing sectors in North America are undergoing significant digital transformations, leading to an increased demand for automation testing to ensure the successful implementation of new digital solutions, systems, and applications. The COVID-19 pandemic has further accelerated this trend as businesses shift to remote work and rely more on digital services. Artificial Intelligence (AI) and Machine Learning (ML) are key technologies driving automation testing, enabling organizations to improve efficiency, reduce costs, and enhance test coverage.

Automation testing solutions are also increasingly being adopted by both large enterprises and small businesses to ensure quality assurance, resource efficiency, and compliance with regulatory requirements. The market for automation testing is expected to grow at a significant rate, with a strategic approach to risk management and product lifecycle being crucial for success. Cloud solutions, static testing, dynamic analysis, and managed services are some of the key areas of focus In the market. Data security is a critical concern, with organizations implementing robust security measures to protect sensitive information. The market for automation testing is evolving, with a growing emphasis on test strategy, test planning, critical functionalities, high-risk areas, mission-critical activities, legacy systems, software applications, application testing, integrated applications, and test coverage.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Automation Testing Industry?

- Increasing demand for continuous delivery and continuous integration (CD/CI) is the key driver of the market.Automation testing plays a crucial role in Agile testing methodologies, accelerating software development and ensuring high-quality outputs. Integrated into Continuous Integration and Continuous Delivery (CI/CD) pipelines, automation testing enables rapid and comprehensive testing, providing quick feedback on code changes and preventing regressions. This testing approach is essential for organizations of all sizes, from large enterprises to small businesses, as they navigate digitalization trends and the evolving product lifecycle. Automation testing offers various testing types, including static analysis and dynamic testing, to cover critical functionalities and high-risk areas. Artificial Intelligence (AI) and Machine Learning (ML) technologies are increasingly integrated into automation testing tools, enhancing test coverage and resource efficiency.

Cloud solutions provide flexibility and scalability, making automation testing a strategic approach for organizations. Test strategy and planning are essential components of automation testing. Mission-critical activities, such as compliance testing and security measures, are addressed through automation testing, ensuring data security and revenue growth. Automation testing also improves efficiency by reducing the need for manual testing and minimizing rework. Market evolution has led to the emergence of managed services and implementation services, offering organizations customized solutions for their automation testing needs. Automation testing tools are now cloud-based, providing organizations with the flexibility to test applications, integrated systems, and legacy systems across various configurations and platforms. The growth rate for automation testing is significant, driven by the increasing importance of quality assurance and risk management In the digital age.

What are the market trends shaping the Automation Testing market?

- Rapid digital transformation is the upcoming market trend.Automation testing is a crucial component of digitalization trends, enabling businesses to align with agile methodologies and DevOps practices for faster software development and deployment. With the increasing complexity of applications spanning various platforms, devices, and interfaces due to digital transformations, automation testing offers scalable and efficient testing solutions. Moreover, as new regulations and security challenges emerge, automated testing plays a vital role in ensuring compliance with standards and identifying vulnerabilities early In the development process. This market evolution is driven by the need for resource efficiency and efficiency improvement, as well as the increasing adoption of artificial intelligence and machine learning in test strategy and planning.

The service segment, which includes managed services and implementation services, is expected to dominate the market due to the growing demand for test coverage and quality assurance. The market is experiencing significant growth, with a high revenue share coming from large enterprises due to their mission-critical activities and high-risk areas. Small enterprises are also adopting automation testing to remain competitive and ensure compliance with industry standards. In the BFSI sector, electronic health records systems, and record systems, automation testing is essential for test coverage and data security. The market for automation testing is expected to grow at a robust rate, with cloud solutions and cloud-based tools becoming increasingly popular due to their cost-effectiveness and flexibility. Organizations are adopting a strategic approach to automation testing, focusing on critical functionalities and legacy systems to optimize their product lifecycle and manage risk.

What challenges does the Automation Testing Industry face during its growth?

- Complexity in automation testing tool implementation is a key challenge affecting the industry growth.Automation testing is a critical component of Agile testing In the digitalization trends era. Artificial Intelligence and Machine Learning are transforming test strategies, enabling Static Analysis and Dynamic Testing. Cloud Solutions streamline test implementation and execution, while the Service Segment offers Managed Services and Implementation Services. Organizations of all sizes, from Large Enterprises to Small Enterprises, benefit from automation testing. Vertical Insights reveal significant adoption In the BFSI Sector, Electronic Health Records Systems, and Record Systems. Test Planning and Test Strategy are essential for identifying Critical Functionalities and High-Risk Areas. Mission-critical Activities and Legacy Systems require thorough Application Testing and Integrated Applications testing.

Test Coverage is a primary concern for Quality Assurance teams, focusing on Resource Efficiency and Efficiency Improvement. Compliance Testing and Security Measures are crucial for ensuring Data Security and adhering to regulatory requirements. The market's growth rate is influenced by the strategic approach to Risk Management and the Product Lifecycle. Cloud-Based Tools are essential for implementing automation testing, offering flexibility and scalability. The market's evolution is driven by the need for seamless integration with existing systems, ensuring smooth workflows. Ensuring test coverage, improving resource efficiency, and maintaining compliance are key drivers for implementing automation testing solutions.

Exclusive Customer Landscape

The automation testing market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automation testing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, automation testing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Accenture Plc - Automation testing is a critical solution for enterprises seeking to minimize risk, enhance quality assurance, and optimize IT performance. By implementing automated testing processes, organizations can streamline testing cycles, ensure consistent results, and reduce the likelihood of errors or defects in software applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- Afour technologies

- Apexon

- Applitools Group

- Astegic Inc.

- Broadcom Inc.

- Capgemini Service SAS

- Cigniti Technologies Ltd.

- Codoid

- Cygnet Infotech

- International Business Machines Corp.

- Invensis Technologies Pvt Ltd.

- Keysight Technologies Inc.

- Microsoft Corp.

- Mobisoft Infotech

- Open Text Corp.

- Parasoft Corp.

- Sauce Labs Inc.

- Tricentis GmbH

- Worksoft

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is experiencing significant growth and transformation due to the digitalization trends sweeping across various industries. Agile testing methods have become increasingly popular, enabling faster development cycles and more frequent releases. This shift towards agility has led to an increased demand for automation testing solutions. Artificial intelligence (AI) and machine learning (ML) are revolutionizing testing by enabling static analysis and dynamic testing. Static testing identifies defects In the code without executing it, while dynamic testing simulates real-world usage scenarios to identify functional and performance issues. These advanced testing techniques are essential for large enterprises and small enterprises alike, as they help ensure critical functionalities and high-risk areas are tested thoroughly.

The service segment of the market is witnessing robust growth, with managed services and implementation services gaining traction. Managed services provide ongoing testing support, allowing organizations to focus on their core business activities. Implementation services help organizations integrate automation testing solutions into their existing IT infrastructure. The testing type market is segmented into application testing, integrated applications, and compliance testing. Application testing focuses on testing software applications, while integrated applications testing ensures the seamless functioning of multiple applications working together. Compliance testing ensures adherence to industry regulations and standards. Legacy systems continue to pose challenges for organizations, as they require specialized testing approaches.

Automation testing solutions can help organizations test these systems efficiently and effectively, reducing the risk of errors and downtime. Data security is a critical concern In the market, with cloud-based tools offering enhanced security measures. A strategic approach to automation testing, incorporating risk management and efficiency improvement, is essential for organizations looking to maximize their revenue share and growth rate. The market evolution of automation testing is driven by the need for organizations to deliver high-quality software applications quickly and efficiently. Automation testing solutions help organizations improve their test strategy and planning, enabling them to focus on mission-critical activities and critical functionalities.

In conclusion, the market is undergoing significant transformation, driven by digitalization trends, agile testing methods, and advanced testing techniques. Organizations of all sizes are recognizing the benefits of automation testing, from improved efficiency and resource efficiency to enhanced data security and compliance testing. As the market continues to evolve, organizations must adopt a strategic approach to automation testing to stay competitive and meet the demands of their customers.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

154 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 15.91% |

|

Market growth 2024-2028 |

USD 30.21 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

15.78 |

|

Key countries |

US, China, Japan, UK, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Automation Testing Market Research and Growth Report?

- CAGR of the Automation Testing industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the automation testing market growth of industry companies

We can help! Our analysts can customize this automation testing market research report to meet your requirements.

RIA -

RIA -