Automotive Brake Fluid Market Size 2024-2028

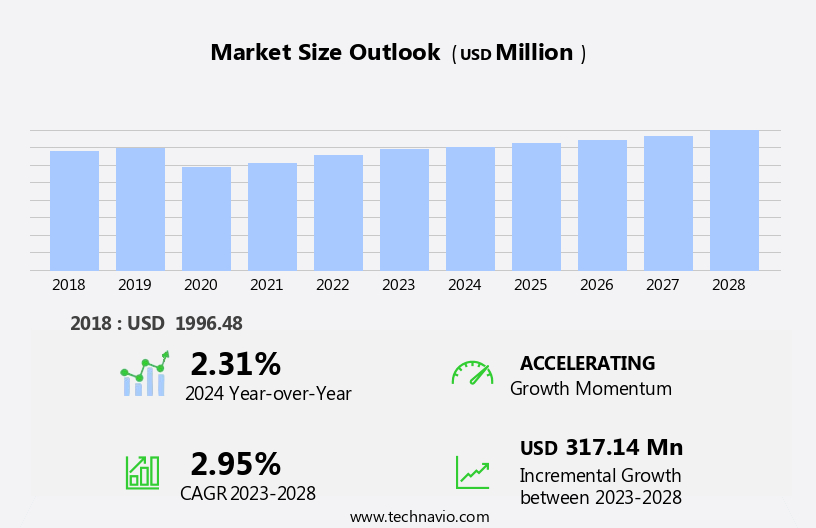

The automotive brake fluid market size is forecast to increase by USD 317.14 million at a CAGR of 2.95% between 2023 and 2028.

- The market is witnessing significant growth due to the increasing number of vehicles in use and the growing popularity of electric vehicles (EVs). With the rise of EVs, there is an increasing demand for hydraulic fluids, including automotive brake fluids, to ensure the proper functioning of hydraulic cylinders in EVs and conventional vehicles. However, the market is also facing challenges such as volatility in raw material prices, particularly for crude oil and ethylene, which are used In the production of glycol ethers and ethylene glycol, key components of automotive brake fluids. Additionally, the safety concerns associated with the use of non-compatible brake fluids in electric vehicles and buses can pose a significant risk to road safety. Rubber components in hydraulic systems can also degrade when exposed to incompatible fluids, leading to costly repairs. Therefore, it is crucial for automotive manufacturers and suppliers to use high-quality, compatible brake fluids to ensure the safety and reliability of their vehicles.

What will be the Size of the Automotive Brake Fluid Market During the Forecast Period?

- The market encompasses the production and distribution of hydraulic fluids specifically designed for use in automotive applications, including hydraulic braking systems and clutches. These fluids, also known as brake fluid oil or polyethylene glycols, play a crucial role In the lubrication and corrosion prevention of mechanical elements such as the main hydraulic cylinder, wheel cylinder, brake caliper, brake pads, rotors, and brake liners. The market's growth is driven by the increasing demand for reliable and efficient braking systems in both traditional passenger cars and the emerging electric vehicle sector. As hydraulic brakes remain a critical component of vehicles, the market's size is substantial and continues to expand.

- Additionally, the development of high-performance fluids with extended boiling points caters to the needs of high-performance vehicles and heavy-duty applications. The automotive sector's ongoing advancements contribute to the market's dynamic nature.

How is this Automotive Brake Fluid Industry segmented and which is the largest segment?

The automotive brake fluid industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Channel

- OEM

- Aftermarket

- Application

- Passenger cars

- Commercial vehicles

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- North America

- US

- South America

- Middle East and Africa

- APAC

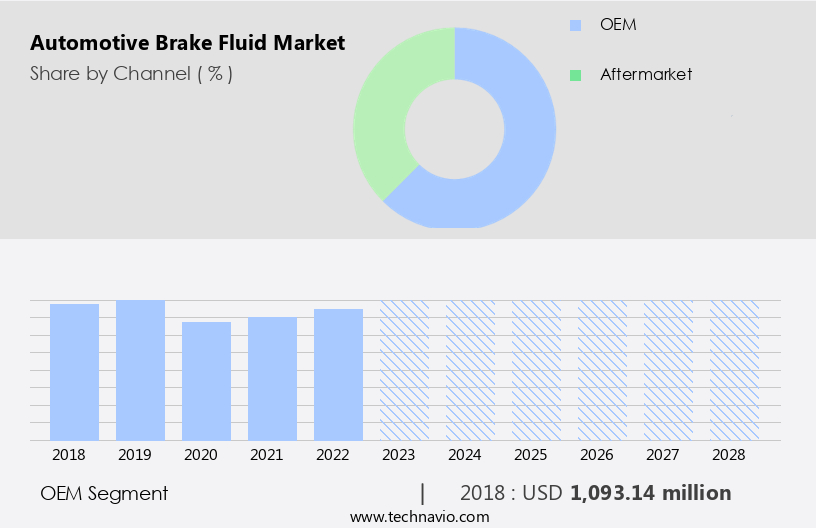

By Channel Insights

The OEM segment is estimated to witness significant growth during the forecast period. The market has experienced significant growth in recent years, driven primarily by the increasing production of passenger and commercial vehicles. Automotive original equipment manufacturers (OEMs) are the primary consumers of automotive brake fluids due to their role in both initial installation during vehicle production and ongoing maintenance and repair services. The focus on quality in brake fluid selection by OEMs is a key market trend, as they seek reliable and effective solutions to ensure vehicle safety standards are met. Automotive applications for brake fluids include hydraulic braking systems, hydraulic brakes, clutches, and various mechanical elements such as pistons, cylinders, and brake calipers.

Get a glance at the market report of share of various segments Request Free Sample

The OEM segment was valued at USD 1.09 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 49% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market In the Asia Pacific region is experiencing significant growth due to increasing sales of passenger vehicles and the adoption of synthetic brake fluids in automobiles. Developing economies, such as India and China, are major contributors to this growth, alongside established markets like Japan and South Korea. The demand for automotive braking fluids is driven by the high volume sales of passenger vehicles. Furthermore, consumer awareness regarding the benefits of using synthetic brake fluids in automobiles is fueling market revenue generation. Government initiatives, such as the Indian government's plan to deploy 10,000 electric buses, are also supporting the adoption of electric vehicles (EVs) and the associated demand for brake fluids.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Automotive Brake Fluid Industry?

- Growing number of vehicles in use is the key driver of the market. The market is experiencing growth due to the rising number of vehicles in use worldwide. For instance, In the European Union, the number of registered passenger cars reached nearly 253 million in 2022, marking a 7% increase over 2017. Similarly, In the US, sales of new lightweight vehicles grew from 8,568 units in 2017 to 9,069 units in 2022, according to the US Department of Transportation (DOT). This increasing vehicle population necessitates the regular use of hydraulic fluids, such as brake fluid oil, in various automotive applications. Automotive brake fluids are essential components of hydraulic braking systems, which include hydraulic brakes, clutches, pistons, cylinders, brake liners, mechanical elements, and rubber components.

- These fluids prevent corrosion In the hydraulic system, ensuring the efficient operation of the brake system. The chemical composition of automotive brake fluids varies, with some using borate esters, glycol ethers, or polyethylene glycols. DOT 3, DOT 4, and DOT 5 are common types of automotive brake fluids, each with different boiling points and properties. Brake fluid plays a crucial role in vehicle safety, as it facilitates the conversion of pedal pressure into braking force. It is used in various automotive applications, including passenger cars, commercial vehicles, electric vehicles, and heavy-duty vehicles. In addition to brake systems, brake fluid is also used in brake by wire systems, anti-lock brake systems, and electronic stability programs.

What are the market trends shaping the Automotive Brake Fluid Industry?

- Growing popularity of EVs is the upcoming market trend. The market experiences growth due to the increasing sales of electric vehicles (EVs). In 2023, EV sales have surpassed 2.3 million In the first quarter, accounting for approximately 14% of total automotive sales. China, Europe, and the US are the leading markets for EV sales. The rise in EV adoption is driven by the decreasing battery prices and the need for high-performance fluids for electric brake systems. Automotive brake fluids, including glycol ethers and polyethylene glycols, are essential components of hydraulic braking systems. They lubricate mechanical elements, such as pistons and cylinders, In the hydraulic braking system, ensuring vehicle safety.

- These fluids also prevent metal corrosion and reduce brake fade, noise, and vibration. Automotive brake fluids come in various types, including DOT 3 glycol, DOT 4 glycol, and DOT 5 silicon. The chemical composition of these fluids varies, with borate and silicon-based options available. Automotive service centers, retailers, and OEMs use these fluids for replacement and maintenance of vehicles, including passenger cars, commercial vehicles, and heavy-duty vehicles.

What challenges does the Automotive Brake Fluid Industry face during its growth?

- Volatility in raw material prices is a key challenge affecting the industry growth. The production of automotive brake fluids relies heavily on ethylene glycol, which is derived from ethylene. The oil and gas industry is a significant supplier of ethylene for ethylene oxide production, making it a crucial factor In the pricing of automotive brake fluids. In 2022, the global crude oil market experienced volatile price fluctuations, leading to potential increases In the cost of ethylene glycol production. This could negatively impact the overall cost of manufacturing automotive brake fluids. Automotive brake fluids are essential components in hydraulic braking systems, including hydraulic brakes, clutches, and mechanical elements such as pistons and cylinders in vehicles.

- They are available in various types, including glycol ethers and polyethylene glycols, each catering to specific vehicle safety standards. Deterioration of brake fluids due to water content, boiling point, and chemical composition can lead to issues like brake fade reduction, noise elimination, and metal corrosion prevention. Brake fluid is used in various automotive applications, including passenger cars, commercial vehicles, electric vehicles, and specialized vehicles like antique cars, weekend cars, collector cars, military vehicles, heavy-duty vehicles, towing vehicles, and race cars. Automobile service centers, workshops, retailers, and OEMs are key consumers of automotive brake fluids. High-performance fluids cater to the specific requirements of various applications, ensuring optimal vehicle safety and performance.

Exclusive Customer Landscape

The automotive brake fluid market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive brake fluid market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive brake fluid market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ADVICS

- AutoChemie Bitterfeld GmbH

- BASF SE

- BP Plc

- Chevron Corp.

- China Petroleum and Chemical Corp.

- Clariant International Ltd.

- DuPont de Nemours Inc.

- Exxon Mobil Corp.

- FUCHS PETROLUB SE

- Granville Oil and Chemicals Ltd.

- Guangdong Delian Group Co., Ltd.

- Hinduja Group Ltd.

- HKS Co. Ltd.

- Indian Oil Corp. Ltd.

- Lubrex FZC

- Saudi Arabian Oil Co.

- Shell plc

- TotalEnergies SE

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses hydraulic fluids specifically designed for use in automotive applications. These fluids play a crucial role In the lubrication and corrosion protection of various mechanical elements withIn the hydraulic braking system. The chemical composition of automotive brake fluids varies, with some containing glycol ethers and others polyethylene glycols. Brake fluids are essential for maintaining the efficient operation of hydraulic brakes, clutches, and other mechanical components. The hydraulic braking system relies on the fluid to transmit pressure from the brake pedal to the brake liners and other mechanical components, enabling the vehicle to stop efficiently and safely. The chemical composition of automotive brake fluids is carefully formulated to meet vehicle safety standards.

For instance, they are designed to prevent metal corrosion and ensure the fluid's boiling point remains consistent under various operating conditions. The fluids are also engineered to work effectively with rubber components, such as brake pads and rotors, to prevent deterioration and ensure optimal performance. Automotive brake fluids are available in various types, including DOT 3 glycol, DOT 4 glycol, and DOT 5 silicon-based fluids. DOT 3 and DOT 4 fluids are glycol-based, while DOT 5 fluids are silicon-based. Each type offers unique benefits, such as improved boiling points, longer service life, and enhanced corrosion protection. The market caters to a diverse range of vehicles, from passenger cars and commercial vehicles to heavy-duty vehicles, military vehicles, antique cars, weekend cars, collector cars, towing vehicles, and race cars.

In addition, the market serves various channels, including automobile service centers, workshops, retailers, general retailers, gasoline retailers, and automotive retailers. The demand for automotive brake fluids is driven by the need to ensure vehicle safety and efficiency. As the automotive industry evolves, so too do the requirements for brake fluids. High-performance fluids are increasingly popular, offering benefits such as metal corrosion prevention, brake fade reduction, and noise elimination. The market for automotive brake fluids is expected to grow, driven by factors such as the increasing demand for vehicle safety and the development of advanced technologies, such as brake by wire systems and electronic stability programs.

Additionally, the falling battery prices in electric vehicles are expected to drive demand for high-performance brake fluids that cater to the unique requirements of electric vehicle braking systems. The market caters to a diverse range of vehicles and serves various channels, offering a range of brake fluid types to meet the unique requirements of each application. The market is expected to grow, driven by factors such as the increasing demand for vehicle safety, the development of advanced technologies, and the evolving needs of the automotive industry.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

171 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.95% |

|

Market growth 2024-2028 |

USD 317.14 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

2.31 |

|

Key countries |

US, China, Japan, India, and Germany |

|

Competitive landscape |

Leading Companies, market growth and forecasting, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Automotive Brake Fluid Market Research and Growth Report?

- CAGR of the Automotive Brake Fluid industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the automotive brake fluid market growth of industry companies

We can help! Our analysts can customize this automotive brake fluid market research report to meet your requirements.

RIA -

RIA -