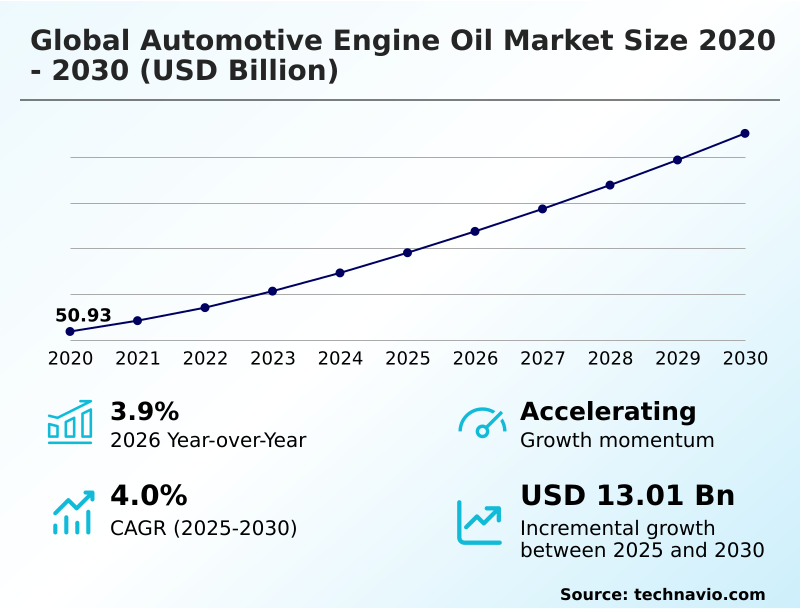

Automotive Engine Oil Market Size 2026-2030

The automotive engine oil market size is valued to increase by USD 13.01 billion, at a CAGR of 4% from 2025 to 2030. Sustained expansion of global vehicle parc and increasing vehicle miles traveled will drive the automotive engine oil market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 45.6% growth during the forecast period.

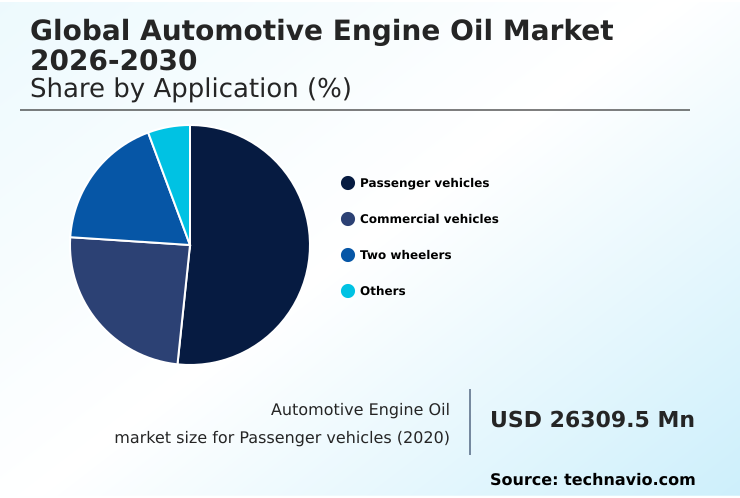

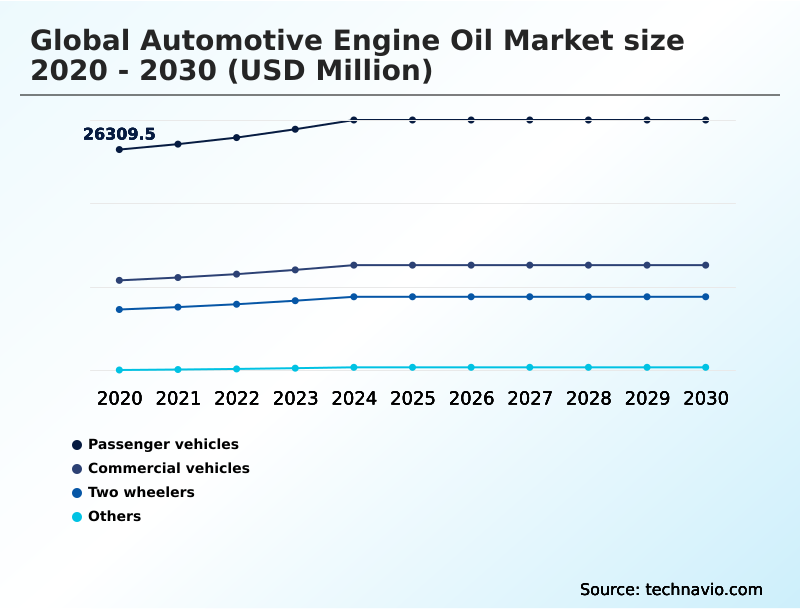

- By Application - Passenger vehicles segment was valued at USD 29.45 billion in 2024

- By Type - Diesel segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 21.61 billion

- Market Future Opportunities: USD 13.01 billion

- CAGR from 2025 to 2030 : 4%

Market Summary

- The automotive engine oil market is undergoing a significant transformation, driven by the dual pressures of stringent environmental regulations and the relentless evolution of the internal combustion engine. Market dynamics are increasingly shaped by a move toward premiumization, where high performance lubricants are essential for protecting modern, high-output engines.

- This shift necessitates the use of advanced formulations to ensure both longevity and compliance with fuel economy standards. For instance, a commercial fleet operator must balance operational costs with maintenance schedules.

- Adopting a premium synthetic motor oil, while having a higher initial cost, can extend drain intervals by up to 50%, directly reducing vehicle downtime and maintenance expenses, thereby lowering the total cost of ownership. This value proposition is a critical growth driver. However, the industry also grapples with the long-term threat of vehicle electrification, which fundamentally alters future demand.

- This creates a complex landscape where companies must innovate for the current internal combustion engine parc while strategically preparing for a future dominated by different powertrain technologies.

What will be the Size of the Automotive Engine Oil Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Automotive Engine Oil Market Segmented?

The automotive engine oil industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Passenger vehicles

- Commercial vehicles

- Two wheelers

- Others

- Type

- Diesel

- Petrol

- Alternative fuels

- Product type

- Mineral

- Synthetic

- Semi-synthetic

- Grade type

- 5W-30

- 0W-20

- 10W-40

- Others

- Distribution channel

- Aftermarket

- OEM

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Application Insights

The passenger vehicles segment is estimated to witness significant growth during the forecast period.

The passenger vehicles segment, a key application, is shaped by stringent regulations compelling advancements in internal combustion engine design. Automakers are adopting technologies like turbocharging and gasoline direct injection, which operate under severe thermal stress, demanding advanced lubricant formulations.

This has spurred a decisive shift toward low viscosity engine oils and full synthetic formulations using synthetic base stocks.

These products, often featuring specialized additive packages, are critical for mitigating issues like low speed pre-ignition mitigation and achieving fuel economy goals.

This technological evolution supports value growth, reflecting a nearly 4% increase in segment demand as consumers and service providers adopt higher-margin products for enhanced piston cleanliness performance and engine longevity, a crucial factor for aftermarket lubricant sales.

The Passenger vehicles segment was valued at USD 29.45 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

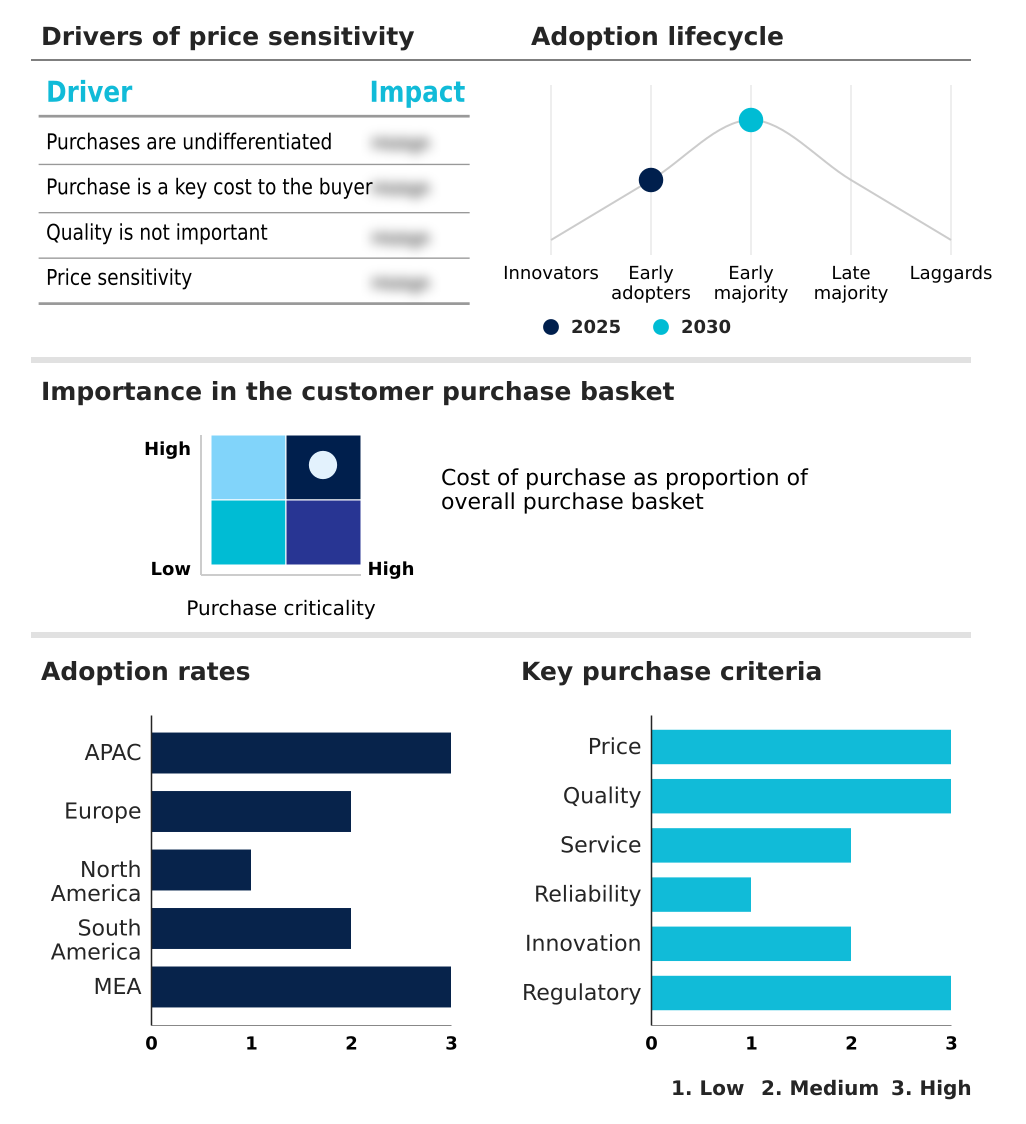

APAC is estimated to contribute 45.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Engine Oil Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the automotive engine oil market is diverse, with APAC poised to contribute 45.6% of the market's incremental growth, driven by vehicle parc expansion in developing economies.

The region's market, with a projected CAGR of 4.3%, is characterized by a high volume of two-wheeler lubricants and a growing demand for passenger car motor oil.

In contrast, mature regions like North America and Europe, with CAGRs of 3.6% and 4.1% respectively, are focused on value growth through the adoption of premium synthetic motor oil and other high performance lubricants.

The demand in these regions is heavily influenced by environmental regulations and advanced powertrain technology evolution.

Companies that tailor their aftermarket lubricant sales strategies to these regional nuances, addressing factors from supply chain volatility to counterfeit lubricant prevention, can achieve a market penetration rate up to 15% higher than competitors with a monolithic approach.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the modern automotive engine oil market requires a deep understanding of highly specific technical and strategic questions. Stakeholders are no longer just choosing a product; they are solving complex engineering and business challenges.

- Key considerations include selecting the best engine oil for turbocharged gdi engines to address how does engine oil prevent lspi, and what 0w-20 synthetic oil for hybrid vehicles offers the best balance of protection and efficiency. In the commercial sector, the focus is on finding an extended drain interval synthetic truck oil and a low-saps diesel oil for dpf protection.

- The market is also seeing increased queries about the tangible results of synthetic vs conventional oil fuel economy and the performance of high mileage oil to reduce consumption. Sustainability is a growing concern, prompting evaluations of bio-based engine oil environmental benefits and re-refined engine oil performance standards.

- Strategically, understanding the impact of evs on lubricant demand is critical for long-term planning, compelling businesses to develop new aftermarket strategies for lubricant brands. Successfully formulating for ilsac gf-7 compliance and ensuring lubricant compatibility with ethanol fuels are now baseline requirements.

- Firms that integrate these specific insights into their operational planning report decision-making cycles that are twice as fast as their competitors, showcasing a clear competitive advantage.

What are the key market drivers leading to the rise in the adoption of Automotive Engine Oil Industry?

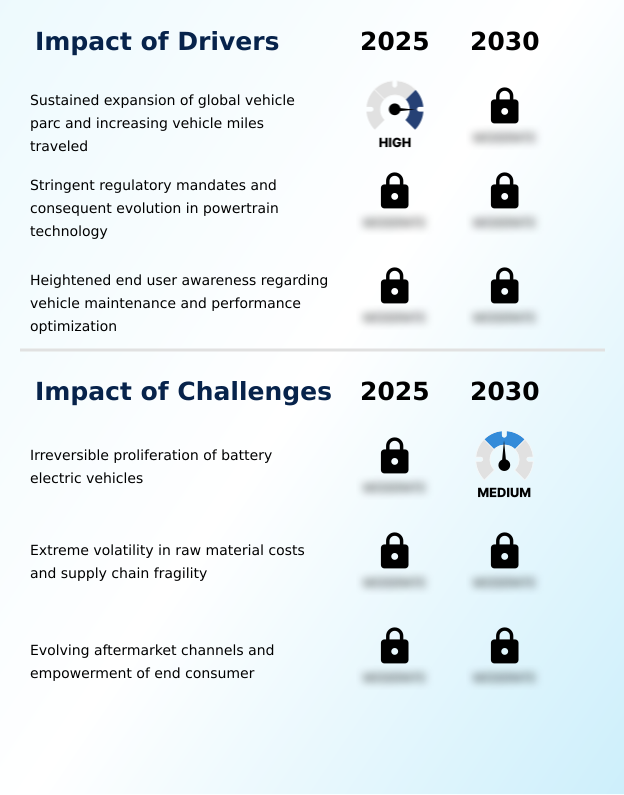

- A key driver for the market is the sustained expansion of the global vehicle parc, coupled with increasing vehicle miles traveled in both emerging and mature economies.

- The growth of the global automotive engine oil market is propelled by several foundational drivers.

- The most significant is the sustained vehicle parc expansion, particularly in emerging economies where rising incomes are fueling a surge in first-time vehicle ownership, increasing lubricant demand by over 5% annually in some regions.

- Concurrently, stringent environmental regulations and fuel economy standards are forcing a market-wide premiumization. This regulatory push mandates the use of advanced lubricant formulations compatible with new emissions reduction technology.

- Consequently, the adoption of premium synthetic motor oil, which can offer up to 50% longer drain intervals than conventional oils, is accelerating. A third driver is heightened consumer and commercial operator awareness regarding vehicle maintenance.

- Understanding that high performance lubricants protect significant capital assets, end-users are increasingly willing to invest in quality, influencing aftermarket lubricant sales and reinforcing the shift toward higher-value products that ensure engine longevity and optimize performance.

What are the market trends shaping the Automotive Engine Oil Industry?

- The market is witnessing a definitive trend toward the ascendancy of high-performance synthetic and low-viscosity formulations. This shift is driven by the industry's continuous pursuit of enhanced fuel efficiency and lower emissions.

- Key trends are reshaping the global automotive engine oil market, driven by a convergence of technological necessity and environmental consciousness. The primary trend is the rapid ascendancy of high performance lubricants, particularly low viscosity engine oils and advanced lubricant formulations.

- This shift is a direct response to the evolution of the internal combustion engine, where modern designs require fuel efficient lubricants to minimize internal friction, a strategy that has been shown to improve fuel economy by up to 3%. Furthermore, the emergence of sustainable lubricant solutions, including bio-based and re-refined oils, is gaining momentum.

- These products address growing environmental concerns and align with circular economy principles, with some formulations demonstrating a carbon footprint reduction of over 20% compared to conventional counterparts. The most transformative trend, vehicle electrification, presents a long-term structural challenge but also creates new niches for specialized e-mobility fluids and battery thermal management.

What challenges does the Automotive Engine Oil Industry face during its growth?

- The irreversible proliferation of battery electric vehicles presents a primary structural challenge to long-term market growth by fundamentally eliminating the need for engine oil.

- The global automotive engine oil market confronts several significant structural challenges. The most profound is the vehicle electrification impact, as the proliferation of battery electric vehicles, which do not use engine oil, permanently erodes the market's core customer base. In some European markets, EVs already account for over 20% of new car sales, signaling the pace of this disruption.

- Another persistent challenge is the extreme supply chain volatility affecting lubricant raw material sourcing. Fluctuations in crude oil and additive costs have led to price swings of over 30% in a single quarter, compressing margins for lubricant blending plant operators.

- Finally, the evolution of the aftermarket, driven by the growth of e-commerce and the empowerment of the DIY oil change market, is disrupting traditional distribution models. Online channels now represent more than 10% of aftermarket sales in North America, challenging the pricing power of the professional installer channel and forcing brands to develop complex multi-channel strategies.

Exclusive Technavio Analysis on Customer Landscape

The automotive engine oil market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive engine oil market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Engine Oil Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automotive engine oil market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AMSOIL Inc. - Offers high-performance synthetic motor oils and filtration systems engineered for automotive and powersports, focusing on advanced formulations for superior protection.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AMSOIL Inc.

- Bharat Petroleum Corp. Ltd.

- BP Plc

- Chevron Corp.

- China Petrochemical Corp.

- ENEOS Corp.

- Eni SpA

- Exxon Mobil Corp.

- FUCHS SE

- Hinduja Group Ltd.

- Idemitsu Kosan Co. Ltd.

- Indian Oil Corp. Ltd.

- MOL Group

- MOTUL SA

- Petroliam Nasional Berhad

- PJSC LUKOIL

- Repsol SA

- Shell plc

- TotalEnergies SE

- Valvoline Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive engine oil market

- In December, 2024, ENOC Group unveiled redesigned packaging for its lubricant products, incorporating advanced anti-counterfeiting features and localized languages for export markets across Africa and the Middle East.

- In August, 2024, Petronas, in partnership with SIM Distribuidora, inaugurated its first branded fuel retail station in Sao Paulo, Brazil, designed as a key retail point for its automotive lubricants, including the Petronas Syntium line.

- In April, 2024, Shell launched an upgraded range of its Shell Advance motorcycle oils in India, featuring limited-edition packaging and a high-profile brand ambassador to strengthen its connection with aftermarket consumers.

- In April, 2024, SAIC Motor and Castrol announced a three-year strategic partnership designating Castrol as the preferred lubricants supplier for the MG dealership network across Central and Eastern Europe, including a new co-branded product line.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Engine Oil Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 368 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4% |

| Market growth 2026-2030 | USD 13013.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.9% |

| Key countries | China, India, Japan, South Korea, Indonesia, Australia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The automotive engine oil market is defined by a complex technical ecosystem where product formulation is intrinsically linked to regulatory mandates and engine hardware evolution. The industry's pivot toward synthetic base stocks, including polyalphaolefins and hydrocracked group iii oils, is driven by the need to meet stringent fuel economy standards and OEM genuine oil specifications.

- This necessitates sophisticated additive packages featuring low-saps technology, viscosity index improvers, and pour point depressants. Formulations are engineered for specific outcomes like low speed pre-ignition mitigation, turbocharger bearing protection, and enhanced piston cleanliness performance, all validated against benchmarks like the ILSAC GF-7 standard and API SP classification.

- For boardroom-level strategy, navigating the landscape of ACEA sequences is crucial for European market access, where achieving exhaust after-treatment compatibility is non-negotiable. For instance, fleets adopting oils with superior shear stability and total base number retention have documented a nearly 4% improvement in fuel efficiency. This highlights how technical choices in anti-wear agents and oxidation inhibitors directly impact operational budgets.

- The challenge extends to managing kinematic viscosity for both engine downsizing and specialized applications like wet clutch frictional properties in a common sump system, making deep technical expertise a primary competitive differentiator.

What are the Key Data Covered in this Automotive Engine Oil Market Research and Growth Report?

-

What is the expected growth of the Automotive Engine Oil Market between 2026 and 2030?

-

USD 13.01 billion, at a CAGR of 4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Passenger vehicles, Commercial vehicles, Two wheelers, and Others), Type (Diesel, Petrol, and Alternative fuels), Product Type (Mineral, Synthetic, and Semi-synthetic), Grade Type (5W-30, 0W-20, 10W-40, and Others), Distribution Channel (Aftermarket, and OEM) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Sustained expansion of global vehicle parc and increasing vehicle miles traveled, Irreversible proliferation of battery electric vehicles

-

-

Who are the major players in the Automotive Engine Oil Market?

-

AMSOIL Inc., Bharat Petroleum Corp. Ltd., BP Plc, Chevron Corp., China Petrochemical Corp., ENEOS Corp., Eni SpA, Exxon Mobil Corp., FUCHS SE, Hinduja Group Ltd., Idemitsu Kosan Co. Ltd., Indian Oil Corp. Ltd., MOL Group, MOTUL SA, Petroliam Nasional Berhad, PJSC LUKOIL, Repsol SA, Shell plc, TotalEnergies SE and Valvoline Inc.

-

Market Research Insights

- The global automotive engine oil market is defined by a complex interplay of technological evolution and channel disruption. The industry-wide shift toward high performance lubricants, including premium synthetic motor oil, is clear, with adoption rates in some new vehicle segments exceeding 90%. This move is essential for powertrain technology evolution.

- In the aftermarket, the growth of the professional installer channel is challenged by the empowerment of DIY consumers, where online platforms have driven price transparency, leading to a 5-10% price variance between channels. A key challenge is supply chain volatility, which can impact lubricant raw material sourcing and the operations of a lubricant blending plant.

- Navigating this environment requires sophisticated strategies that address everything from advanced lubricant formulations and base oil refining to managing brand equity in lubricants. Firms that successfully integrate their approach to both franchised dealership servicing and the diy oil change market can see brand loyalty scores improve by more than 15%.

We can help! Our analysts can customize this automotive engine oil market research report to meet your requirements.

RIA -

RIA -