Automotive Infotainment Testing Platform Market Size 2024-2028

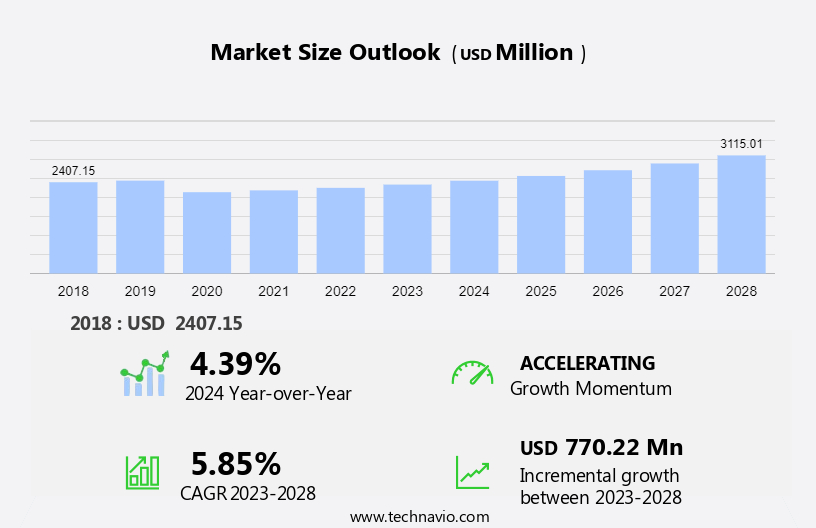

The automotive infotainment testing platform market size is forecast to increase by USD 770.22 million at a CAGR of 5.85% between 2023 and 2028.

- The market is experiencing significant growth, driven by innovation in operating systems that enhance the functionality and user experience of infotainment systems. Media Oriented Systems Transport (MOST) technology is simplifying system upgrades, allowing for seamless integration of new features and improvements. However, data security remains a major challenge, as the increasing connectivity of infotainment systems presents new vulnerabilities that must be addressed to protect consumer privacy and ensure the safety of vehicle operations. Centralized management and governance, risk analytics, and IAM certifications from reputable companies further enhance security and compliance. These trends and challenges are shaping the future of the market, providing opportunities for companies to develop advanced solutions that meet the evolving needs of consumers and automakers alike. The market analysis report offers an in-depth examination of these and other key factors impacting market growth.

What will be the Size of the Automotive Infotainment Testing Platform Market During the Forecast Period?

- The market is experiencing significant growth due to the increasing adoption of cloud architecture In the automotive industry. Cloud services have become essential components of modern infotainment systems, enabling advanced features such as federation, OpenID Connect, and multifactor authentication. Automated provisioning and deprovisioning, along with Identity and Access Management (IAM) best practices, ensure centralized security and control over user accounts and their lifecycle. IAM risks, including configuration oversights and identity theft, are major concerns for automotive infotainment system providers. To mitigate these risks, cloud-based IAM solutions offer biometric authentication, single sign-on, and passwordless IAM. These trends underscore the importance of strong IAM capabilities In the market.

How is this Automotive Infotainment Testing Platform Industry segmented and which is the largest segment?

The automotive infotainment testing platform industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

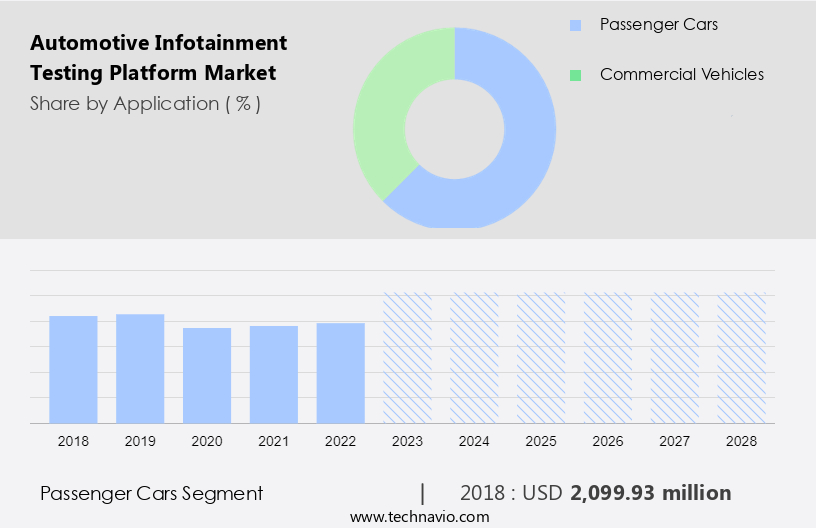

- Application

- Passenger cars

- Commercial vehicles

- Type

- QNX system

- WinCE system

- Linux system

- Others

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- South America

- Middle East and Africa

- North America

By Application Insights

- The passenger cars segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant growth due to the increasing demand for advanced in-vehicle technologies. Automotive infotainment systems offer various features such as video, audio, navigation, and communication services, making them an essential component of modern passenger cars. Vehicle Original Equipment Manufacturers (OEMs) like BMW, Audi, Infiniti, Jaguar Land Rover, and Daimler are investing in innovative infotainment systems to differentiate their models. Cloud architecture plays a crucial role In the development of these systems, enabling services such as multifactor authentication, automated provisioning, and deprovisioning. Centralized security, identity management, and access management are essential components of cloud-based infotainment systems. IAM best practices, including single sign-on, role-based access control, and fine-grained access control, ensure secure access to these systems.

IAM certifications and companies provide centralized management and application integration. With the increasing focus on user experience, healthcare interoperability, and corporate identities, the vulnerability landscape and online security are becoming critical concerns. IAM solutions, including passwordless IAM, HIPAA, NIST guidelines, decentralized identity framework, and blockchain technology, address these concerns. IAM solutions also provide centralized management, reporting, and policy-based control. Zero trust architecture, secured privileged accounts, training and support, and data protection standards are other essential features of IAM solutions.

Get a glance at the Automotive Infotainment Testing Platform Industry report of share of various segments Request Free Sample

The passenger cars segment was valued at USD 2.1 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

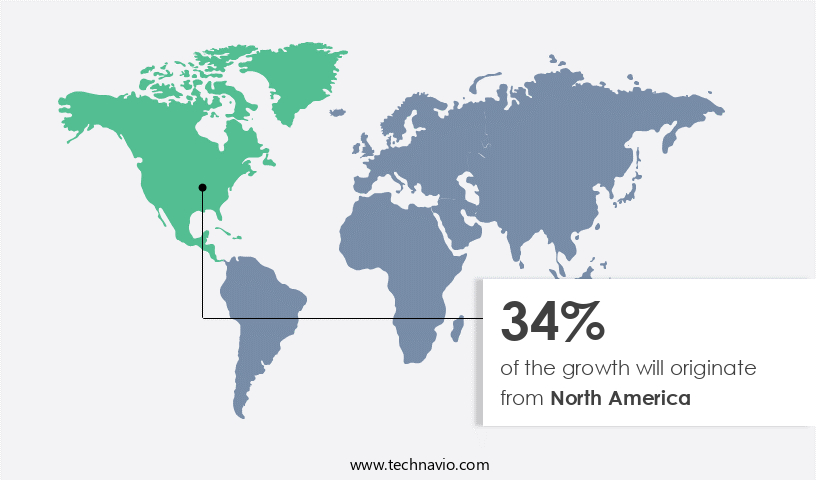

- North America is estimated to contribute 34% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American market is experiencing significant growth due to the increasing demand for advanced infotainment systems in luxury vehicles. The US and Canada are major contributors to this market, driven by the rising number of baby boomers and the adoption of these systems in new vehicles. OEMs, such as Ford and GM, are focusing on developing efficient infotainment technologies, with Ford transitioning from Microsoft OS to QNX OS for the SYNC 3 system. Advanced Driver-Assistance Systems (ADAS) are also gaining popularity In the region, driving market growth. Additionally, the deployment of cloud architecture in automotive infotainment systems is increasing, with services such as OpenID Connect, multifactor authentication, automated provisioning, and deprovisioning being implemented for Identity and Access Management (IAM) best practices.

Centralized security, identity, and IAM risks are addressed through cloud-based IAM solutions, which offer user accounts, lifecycle control, audit capabilities, IAM certifications, and company support. Other trends include centralized management, single sign-on, governance, risk analytics, passwordless IAM, and compliance with regulations such as HIPAA and NIST guidelines. The decentralized identity framework and blockchain technology are also gaining traction In the healthcare sector for interoperability and user experience improvements. The market is expected to continue growing, driven by the need for fine-grained access control, security policies, zero trust architecture, and user productivity enhancements.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Automotive Infotainment Testing Platform Industry?

Innovation in OS to drive infotainment testing platform market is the key driver of the market.

- The market is witnessing significant growth as cloud architecture becomes increasingly prevalent In the development of automotive infotainment systems. Cloud-based services are transforming the industry by enabling components such as federation, OpenID Connect, multifactor authentication, automated provisioning, and deprovisioning. IAM best practices, including centralized security, identity management, and risk analytics, are crucial in mitigating identity risks and configuration oversights. Biometric authentication and data theft prevention are essential considerations for cloud-based IAM solutions. Compliance with certifications such as HIPAA and NIST guidelines is also vital for healthcare applications. The decentralized identity framework and blockchain technology are gaining traction for their enhanced security and interoperability benefits.

- User experience, corporate identities, and employee productivity are key priorities for automotive infotainment system manufacturers. Passwordless IAM, single sign-on, role-based access control, and reporting are essential features for these systems. Cloud IAM and on-premises IAM solutions offer fine-grained access control and security policies, while zero trust architecture and central identity management ensure secure access. Training and support are crucial for IT professionals managing these complex systems. Data protection standards and identity management companies provide the necessary tools and resources for effective implementation and maintenance. In summary, the market is dynamic and complex, requiring a deep understanding of the latest IAM trends, technologies, and best practices.

What are the market trends shaping the Automotive Infotainment Testing Platform Industry?

Use of Media Oriented Systems Transport technology to simplify system upgrades is the upcoming market trend.

- In the realm of automotive infotainment, the demand for advanced features such as high-definition video decoding and multiple displays for rear-seat entertainment necessitates the development of more powerful processors. This trend has also led to the adoption of Media Oriented Systems Transport (MOST) network technology in automotive infotainment systems. MOST technology, a communication backbone solution, enables seamless connectivity between rear-seat entertainment systems and the front-seat infotainment system. Brands like Audi, BMW, Jaguar Land Rover, Daimler, Porsche, Toyota, Volkswagen, SAAB, SKODA, SEAT, and Volvo have incorporated MOST technology into their vehicles. This innovation facilitates the transmission of audio and video from the front-seat head unit to the displays on the rear seats. In the context of identity and access management (IAM) for cloud-based automotive infotainment systems, several components and services are essential. These include centralized security, identity, IAM risks, configuration oversights, biometrics, data theft, cloud-based IAM, user accounts, lifecycle control, audit capabilities, IAM certifications, IAM companies, centralized management, single sign-on, governance, risk analytics, passwordless IAM, HIPAA, NIST guidelines, decentralized identity framework, and blockchain technology.

- To ensure optimal security, IAM's best practices such as multi-factor authentication, automated provisioning, deprovisioning, and fine-grained access control are crucial. Centralized identity management, secure access, policy-based control, secured privileged accounts, training and support, data protection standards, and administrative transparency are also essential. The market is witnessing significant growth due to the increasing demand for advanced features, user experience, and online security. As IT professionals manage user identities, identity repositories, and application integration, they must adhere to IAM risks, configuration oversights, and vulnerability landscape to maintain administrative transparency and user roles. Identity providers play a vital role in ensuring secure access and single sign-on, while role-based access control and reporting enable fine-grained access control and policy-based control. Thus, the market is a dynamic and evolving landscape that requires a comprehensive approach to identity and access management. By focusing on centralized management, security policies, zero trust architecture, and user experience, IT professionals can mitigate IAM risks, ensure administrative transparency, and maintain secure access to critical systems and data.

What challenges does the Automotive Infotainment Testing Platform Industry face during its growth?

Data security issues is a key challenge affecting the industry growth.

- The market is gaining significance due to the increasing adoption of cloud architecture in automotive telematics applications. These platforms offer services that ensure the security and functionality of components such as multifactor authentication, automated provisioning, and deprovisioning. Centralized security, identity management, and access management are crucial aspects of these platforms, which follow IAM best practices and employ centralized management, single sign-on, and role-based access control. Cloud-based IAM solutions offer advantages like user lifecycle control, audit capabilities, IAM certifications, and IAM companies' support. However, the vulnerability landscape of these platforms includes identity risks, configuration oversights, and passwordless IAM. To mitigate these risks, biometric authentication, data theft protection, and HIPAA and NIST guidelines compliance are essential.

- Decentralized identity frameworks and blockchain technology offer enhanced security and interoperability in healthcare applications. User experience, corporate identities, and online security are other critical factors that influence the market's growth. IT professionals must address password and authentication vulnerabilities, authorization, and multi-factor authentication to ensure secure access to these platforms. Zero trust architecture, central identity management, and policy-based control are essential for securing privileged accounts and providing training and support to users. Data protection standards and reporting capabilities are also vital for ensuring administrative transparency and application integration. Fine-grained access control, security policies, and secured privileged accounts are necessary for maintaining a strong security posture.

Exclusive Customer Landscape

The automotive infotainment testing platform market forecasting report includes the adoption lifecycle of the market, market growth and forecasting, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive infotainment testing platform market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive infotainment testing platform market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alten SA

- Anritsu Corp.

- Arrow Electronics Inc.

- Averna Technologies Inc.

- Changyuan Technology Group Ltd.

- Danlaw Inc.

- FEV Group GmbH

- Fraunhofer Gesellschaft

- Functionize Inc.

- GOPEL electronic GmbH

- HeadSpin Inc.

- Infineon Technologies AG

- Intertek Group Plc

- Keysight Technologies Inc.

- Nextgen Technology Ltd.

- Rohde and Schwarz GmbH and Co. KG

- Softing AG

- Testfabrik AG

- Volkswagen AG

- Wind River Systems Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is experiencing significant growth as the demand for advanced in-vehicle connectivity and security solutions continues to rise. This market encompasses a range of cloud-based services and components that enable identity and access management (IAM) for automotive applications. Cloud architecture plays a crucial role In the market, providing scalability, flexibility, and cost savings. Services offered include automated provisioning and deprovisioning, centralized security, and single sign-on (SSO) for seamless user experience. IAM best practices, such as multifactor authentication and centralized identity management, are essential to mitigate risks associated with configuration oversights and identity theft. Biometric authentication and passwordless IAM are gaining popularity In the market due to their convenience and enhanced security. Healthcare applications, in particular, require strict adherence to data protection standards, such as HIPAA and NIST guidelines, which are addressed through cloud-based IAM solutions. Interoperability is another critical factor In the market, allowing for seamless integration of various applications and corporate identities. The vulnerability landscape is constantly evolving, necessitating ongoing risk analytics and training and support for IT professionals. Zero trust architecture is a key trend In the market, emphasizing the importance of securing privileged accounts and implementing fine-grained access control.

Moreover, policy-based control and administrative transparency are also essential components of a strong IAM solution. The market caters to various industries, including healthcare, finance, and transportation, among others. These industries require stringent security measures to protect sensitive data and ensure employee productivity. The IAM market is highly competitive, with various companies offering solutions tailored to the unique needs of the automotive industry. Centralized management, role-based access control, reporting, and governance are common features of IAM solutions in this market. Thus, the market is a dynamic and evolving landscape, driven by the demand for advanced security and connectivity solutions. IAM plays a crucial role in addressing the unique challenges of the automotive industry, including identity risks, configuration oversights, and data theft. Cloud-based IAM solutions offer scalability, flexibility, and cost savings, making them an attractive option for organizations in various industries.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

171 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.85% |

|

Market growth 2024-2028 |

USD 770.22 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.39 |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Automotive Infotainment Testing Platform Market Research and Growth Report?

- CAGR of the Automotive Infotainment Testing Platform industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the automotive infotainment testing platform market growth of industry companies

We can help! Our analysts can customize this automotive infotainment testing platform market research report to meet your requirements.

RIA -

RIA -