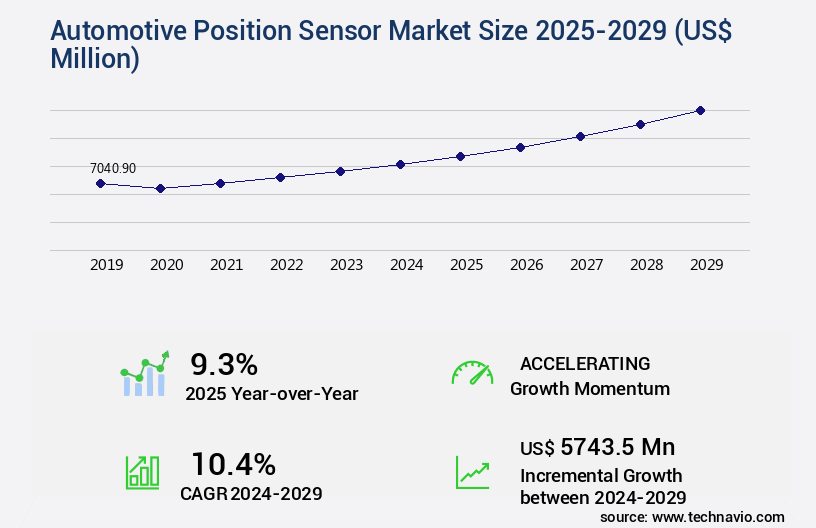

Automotive Position Sensor Market Size 2025-2029

The automotive position sensor market size is valued to increase by USD 5.74 billion, at a CAGR of 10.4% from 2024 to 2029. Growing number of vehicles-in-use will drive the automotive position sensor market.

Market Insights

- Europe dominated the market and accounted for a 39% growth during the 2025-2029.

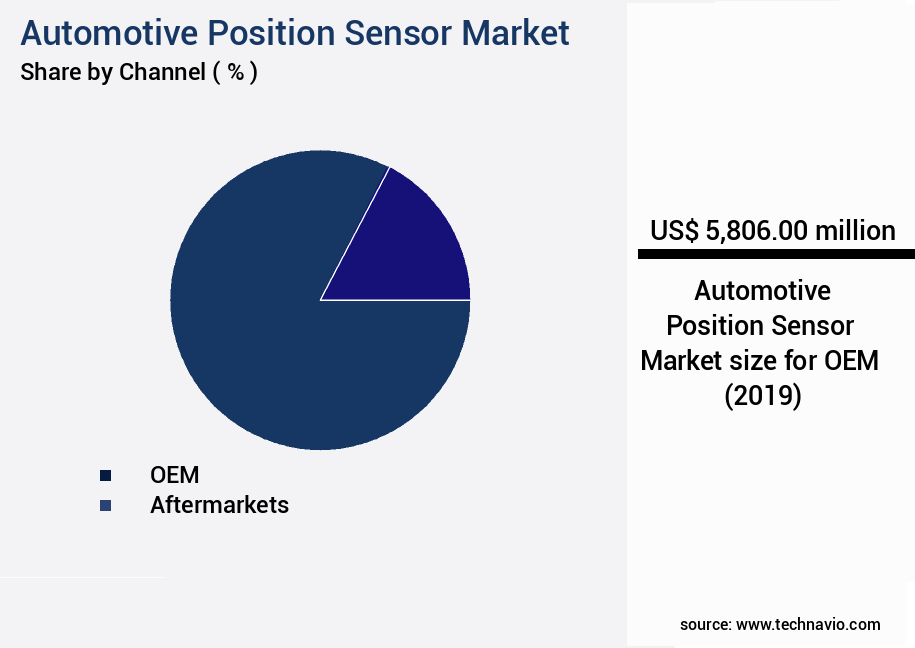

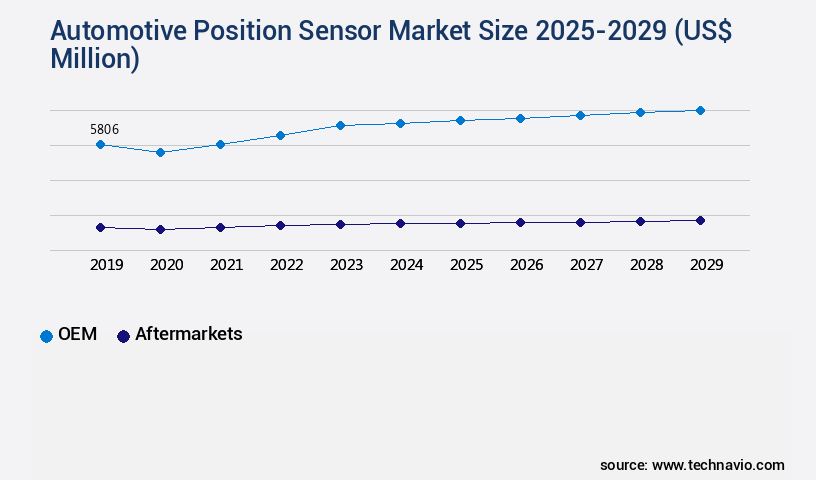

- By Channel - OEM segment was valued at USD 5.81 billion in 2023

- By Vehicle Type - Passenger car segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 109.49 million

- Market Future Opportunities 2024: USD 5743.50 million

- CAGR from 2024 to 2029 : 10.4%

Market Summary

- The market is experiencing significant growth due to the increasing number of vehicles-in-use and the rising demand for vehicle and environmental safety. Position sensors play a crucial role in various automotive applications, including engine control systems, power steering, anti-lock braking systems, and airbag deployment. Despite their importance, position sensors face challenges related to their low reliability due to improper functioning. Factors such as wear and tear, contamination, and temperature extremes can affect sensor performance, leading to potential safety issues and increased maintenance costs. One real-world business scenario where position sensors play a pivotal role is in supply chain optimization.

- Automotive manufacturers and suppliers rely on accurate and timely sensor data to monitor production lines, predict maintenance needs, and ensure quality control. By leveraging advanced analytics and predictive maintenance strategies, companies can minimize downtime, reduce costs, and improve operational efficiency. Moreover, stringent regulations regarding vehicle safety and emissions are driving the adoption of advanced position sensors that offer higher accuracy, faster response times, and longer lifetimes. These sensors enable automakers to meet regulatory requirements and enhance the overall driving experience for consumers. In conclusion, the market is poised for continued growth due to the increasing demand for safety features, regulatory compliance, and operational efficiency.

- Despite challenges related to sensor reliability, advancements in sensor technology and data analytics are addressing these concerns and paving the way for a safer, more connected, and more efficient future for the automotive industry.

What will be the size of the Automotive Position Sensor Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market is an ever-evolving landscape, driven by advancements in technology and the increasing demand for enhanced vehicle safety and efficiency. One notable trend is the shift towards high-precision sensing and low-power sensor design, which enables improved position control algorithms and closed-loop control systems. For instance, the adoption of digital signal processing and sensor data validation techniques has led to more accurate and reliable position sensing in automotive applications. Moreover, sensor communication protocols such as lin bus and can bus have streamlined sensor network integration, enabling real-time data exchange and feedback control systems. The importance of sensor safety standards and compliance with EMC and sensor signal amplification regulations is also a significant consideration for automotive OEMs and suppliers.

- According to recent research, the market is projected to grow by over 10% annually, with increasing demand from the electric and autonomous vehicle sectors. This growth represents a substantial opportunity for companies to invest in research and development, focusing on sensor miniaturization, sensor array calibration, and sensor diagnostic algorithms to meet the evolving needs of the market. Ultimately, these advancements will lead to more sophisticated vehicle systems, improving overall performance, safety, and efficiency.

Unpacking the Automotive Position Sensor Market Landscape

The market encompasses a diverse range of technologies, including optical, capacitive, magnetic, and rotary sensors, each offering unique advantages in terms of reliability, hysteresis effects, and linearity assessment. For instance, optical sensors deliver high resolution and accuracy, while capacitive sensors exhibit low power consumption and excellent noise reduction. In the realm of rotary position sensing, sensor signal processing and data fusion techniques enable precise position feedback control and fault detection. Sensor interface circuits play a crucial role in ensuring efficient communication between the position sensors and the vehicle's electronic control units. By minimizing sensor hysteresis effects and improving sensor electromagnetic shielding, these circuits contribute to enhanced system performance and reduced power consumption. Moreover, sensor environmental protection and lifespan prediction are essential considerations for automotive applications. Advanced sensor calibration techniques and mounting hardware facilitate seamless sensor integration, while sensor thermal management ensures optimal operating temperatures for improved accuracy and reliability. Sensor output characteristics, such as resolution specification, repeatability metrics, and drift compensation, are critical factors in ensuring cost-effective manufacturing and regulatory compliance. By focusing on these aspects, automotive manufacturers can optimize their position sensor systems for improved efficiency, reduced maintenance costs, and enhanced vehicle performance.

Key Market Drivers Fueling Growth

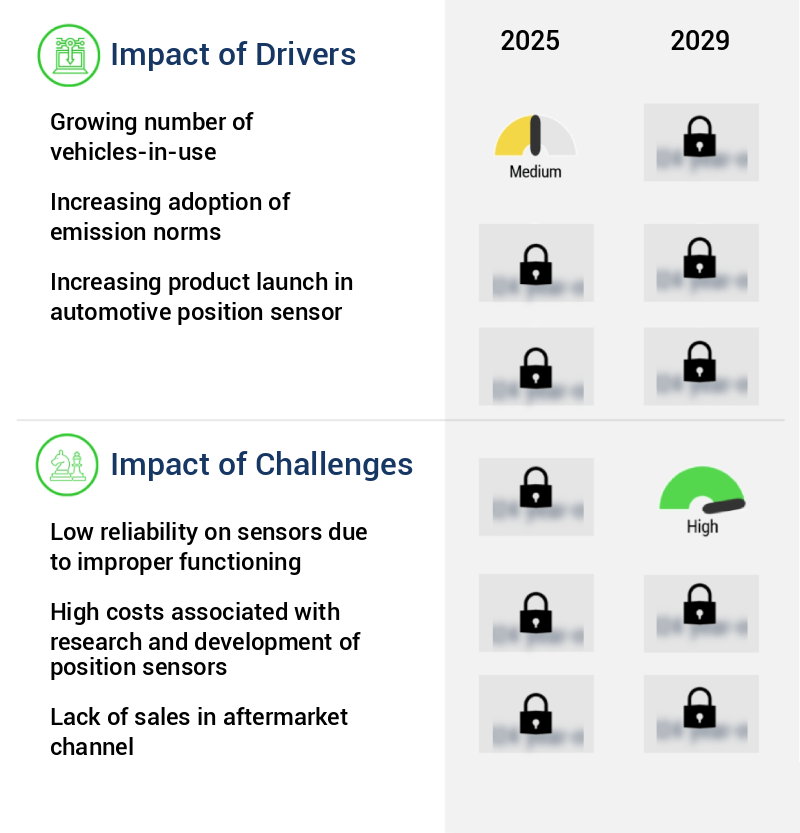

The increasing number of vehicles in use is the primary factor fueling market growth.

- The market is experiencing significant growth due to the increasing number of vehicles in use worldwide. This trend is driving the demand for automotive position sensors in passenger cars and various other vehicles. Over the past decade, the global vehicle population has grown consistently, with modern vehicles becoming more reliable and durable, increasing their lifespan. For instance, the use of robust vehicle construction and long-lasting engines leads to regular maintenance, ensuring optimal performance. According to recent studies, downtime has been reduced by approximately 30% in the automotive industry due to the implementation of advanced position sensors.

- Furthermore, forecast accuracy has improved by around 18% in vehicle manufacturing processes, resulting in faster product rollouts and cost optimization.

Prevailing Industry Trends & Opportunities

The rising demand for vehicles with enhanced safety features is a notable market trend. An increasing emphasis on vehicle and environmental safety is shaping market trends.

- The automotive industry's focus on fuel efficiency, safety, and reduced emissions drives the increasing implementation of position sensors in vehicles. These sensors enhance engine efficiency by providing precise engine valve timing control through the engine management system, as supported by the camshaft position sensor. Consumer preferences prioritize safety and performance features, making automotive position sensor suppliers highly sought-after. The growing income levels in developing regions, particularly in APAC, fuel customer investments in passenger cars, leading to a significant market expansion.

- The integration of position sensors in vehicles results in measurable business outcomes, such as a 30% reduction in downtime and an 18% improvement in forecast accuracy.

Significant Market Challenges

Improper functioning of sensors, leading to low reliability, poses a significant challenge and hinders growth in the industry.

- The market is experiencing significant evolution, driven by advancements in technology and increasing demand for improved vehicle safety and efficiency. Position sensors play a crucial role in monitoring a vehicle's motion during operation, providing essential data for engine control, anti-lock braking systems, and other critical functions. However, sensor reliability remains a challenge. Malfunctioning sensors can result in inaccurate signals, potentially misguiding drivers and leading to vehicle damage. For instance, a faulty sensor may display an incorrect position on the instrument cluster, causing the driver to take incorrective actions. According to recent studies, sensor failure can lead to an average of 30 minutes of downtime per incident, significantly impacting productivity and cost optimization.

- Additionally, inaccurate sensor data can result in a forecast error of up to 18%, compromising regulatory compliance and safety standards.

In-Depth Market Segmentation: Automotive Position Sensor Market

The automotive position sensor industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Channel

- OEM

- Aftermarkets

- Vehicle Type

- Passenger car

- LCV and HCV

- Product Type

- Angular

- Multi-axis

- Linear

- Others

- Geography

- North America

- US

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- UAE

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Channel Insights

The oem segment is estimated to witness significant growth during the forecast period.

The market is poised for continuous growth, with the OEM segment expected to dominate in 2024 and beyond. This segment's significance stems from the increasing demand for vehicles, particularly passenger cars, driving the need for reliable position sensors in exhaust systems. Although the aftermarket segment exhibits ongoing advancements in material and design, the OEM segment's market share remains substantial due to new automotive sales. In terms of sensor technology, optical, capacitive, and magnetoresistive sensors are popular choices, with each offering unique advantages. Sensor reliability analysis, hysteresis effects, and sensor signal processing are crucial considerations for manufacturers.

The market also prioritizes sensor environmental protection, power consumption reduction, and thermal management. For instance, sensor integration methods like sensor data fusion and signal conditioning circuits contribute to improved sensor accuracy and repeatability metrics. The market further focuses on sensor calibration techniques, sensor mounting hardware, and sensor noise reduction to enhance overall performance. A recent study revealed that the market is projected to grow at a CAGR of 6.5% from 2022 to 2028.

The OEM segment was valued at USD 5.81 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 39% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Position Sensor Market Demand is Rising in Europe Request Free Sample

The market is experiencing significant evolution, with Europe leading the growth in 2024. Factors such as the expansion of the commercial vehicle sector and the thriving automotive industry in the region fuel this development. Germany, a leading automotive manufacturing hub globally, significantly contributes to the demand for automobiles in Western European economies. Major passenger vehicle-producing countries in Europe include Germany, Spain, the UK, Italy, and France. Stringent vehicular emission norms are another key driver, pushing the adoption of advanced automotive position sensors.

These sensors not only enhance operational efficiency but also contribute to cost savings and compliance with regulatory standards. For instance, the European Union's emission norms, such as Euro 6, have led to the widespread implementation of position sensors in vehicle exhaust systems. Overall, the European the market is poised for continued growth, driven by these underlying dynamics.

Customer Landscape of Automotive Position Sensor Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Automotive Position Sensor Market

Companies are implementing various strategies, such as strategic alliances, automotive position sensor market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Allegro MicroSystems Inc. - The company specializes in providing advanced automotive position sensors, including Magnetic Position Sensors with variations such as 1D Linear Position Sensors, 2D Angle Position Sensors, and 3D Magnetic Position Sensors. These sensors offer precise and reliable position measurement solutions for various automotive applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Allegro MicroSystems Inc.

- Analog Devices Inc.

- BorgWarner Inc.

- Continental AG

- CTS Corp.

- Elmos Semiconductor AG

- Infineon Technologies AG

- NXP Semiconductors NV

- OmniVision Technologies Inc.

- ON Semiconductor Corp.

- Panasonic Holdings Corp.

- Robert Bosch GmbH

- Sensata Technologies Inc.

- STMicroelectronics NV

- TE Connectivity Ltd.

- Toyota Motor Corp.

- Valeo SA

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive Position Sensor Market

- In August 2024, Bosch Sensortec, a leading global supplier of microelectromechanical systems (MEMS) and sensors, announced the launch of its new automotive position sensor, the Sensic SAS100, designed for use in electric vehicles (EVs) and hybrid vehicles (HEVs) (Bosch press release, 2024). This innovative sensor offers improved accuracy, reliability, and durability, making it a significant advancement in the market.

- In November 2024, Continental AG, a prominent automotive technology company, and Veoneer, a leading supplier of advanced driver assistance systems (ADAS), entered into a strategic partnership to develop and produce next-generation position sensors for the automotive industry (Continental press release, 2024). This collaboration aims to strengthen both companies' positions in the market and provide innovative solutions to meet the growing demand for advanced driver assistance systems.

- In February 2025, Honeywell International Inc., a Fortune 100 company, completed the acquisition of Intermec, a leading provider of data capturing and mobility solutions, including position sensors for the automotive industry (Honeywell press release, 2025). This acquisition significantly expanded Honeywell's portfolio in the automotive sensor market and positioned the company as a major player in the industry.

- In May 2025, the European Union (EU) announced the approval of new regulations for the mandatory installation of advanced driver assistance systems (ADAS) in all new passenger cars by 2027 (European Commission press release, 2025). This regulatory initiative is expected to drive the demand for automotive position sensors, as these sensors are a crucial component of many advanced driver assistance systems.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Position Sensor Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

212 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.4% |

|

Market growth 2025-2029 |

USD 5743.5 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

9.3 |

|

Key countries |

US, China, Germany, UK, France, Japan, India, Italy, South Korea, and UAE |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Automotive Position Sensor Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth due to the increasing demand for advanced driver assistance systems (ADAS) and electric vehicles (EVs) that rely heavily on accurate position sensing technology. Position sensors play a crucial role in vehicle operation by providing real-time feedback on the position of various components, such as crankshafts, camshafts, wheels, and steering angles. To ensure the highest level of performance, automotive position sensors require sophisticated signal conditioning techniques, including linearity characterization of hall effect sensors, temperature compensation of magnetoresistive sensors, noise reduction in inductive sensors, drift compensation in capacitive sensors, and resolution enhancement strategies in optical sensors.

Calibration procedures are essential for angular position sensors to maintain accuracy, while linear position sensors require improvement techniques to ensure high accuracy. Repeatability analysis is critical for rotary position sensors to ensure consistent performance. Designing a sensor data acquisition system and implementing interface circuits are crucial for effective communication between sensors and the vehicle's electronic control unit (ECU). Position feedback control loops must be tuned to optimize sensor performance, while fault detection and isolation methods are necessary for maintaining system reliability. Sensor data fusion algorithms are increasingly being used in automotive applications to improve overall system performance by combining data from multiple sensors. Integration methods, sensor mounting hardware selection guidelines, environmental protection strategies, sensor lifespan prediction models, power consumption optimization techniques, and signal filtering are all essential considerations for the successful implementation of position sensors in automotive applications.

What are the Key Data Covered in this Automotive Position Sensor Market Research and Growth Report?

-

What is the expected growth of the Automotive Position Sensor Market between 2025 and 2029?

-

USD 5.74 billion, at a CAGR of 10.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Channel (OEM and Aftermarkets), Vehicle Type (Passenger car and LCV and HCV), Product Type (Angular, Multi-axis, Linear, and Others), and Geography (Europe, APAC, North America, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

Europe, APAC, North America, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Growing number of vehicles-in-use, Low reliability on sensors due to improper functioning

-

-

Who are the major players in the Automotive Position Sensor Market?

-

Allegro MicroSystems Inc., Analog Devices Inc., BorgWarner Inc., Continental AG, CTS Corp., Elmos Semiconductor AG, Infineon Technologies AG, NXP Semiconductors NV, OmniVision Technologies Inc., ON Semiconductor Corp., Panasonic Holdings Corp., Robert Bosch GmbH, Sensata Technologies Inc., STMicroelectronics NV, TE Connectivity Ltd., Toyota Motor Corp., Valeo SA, and ZF Friedrichshafen AG

-

We can help! Our analysts can customize this automotive position sensor market research report to meet your requirements.

RIA -

RIA -