Autonomous Mobile Robots Market Size 2026-2030

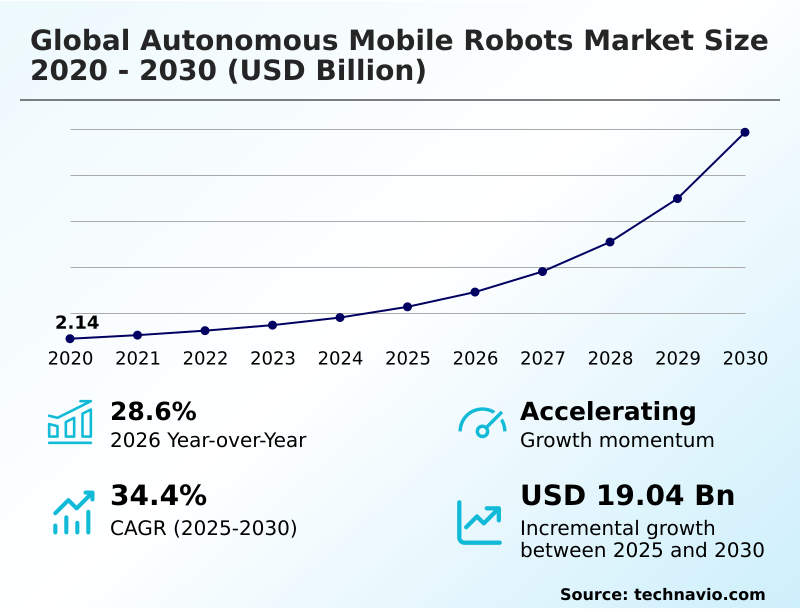

The autonomous mobile robots market size is valued to increase by USD 19.04 billion, at a CAGR of 34.4% from 2025 to 2030. Increasing labor shortages and rising workforce costs will drive the autonomous mobile robots market.

Major Market Trends & Insights

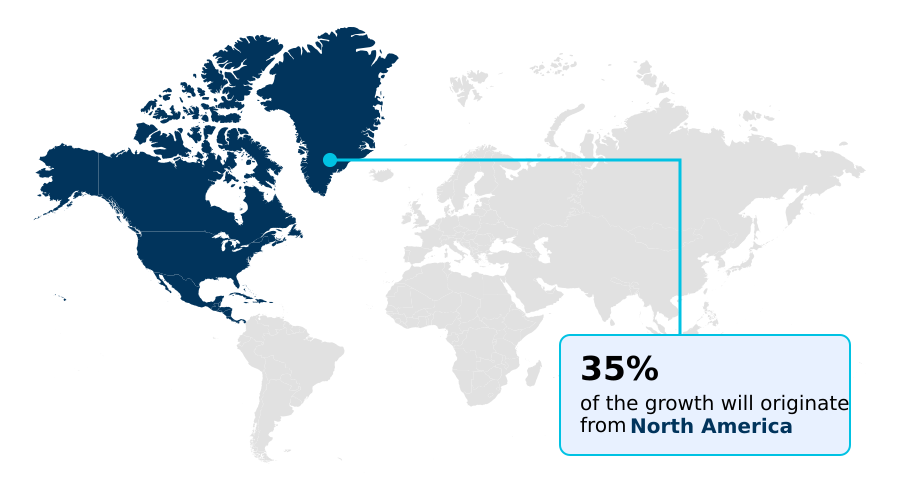

- North America dominated the market and accounted for a 35.4% growth during the forecast period.

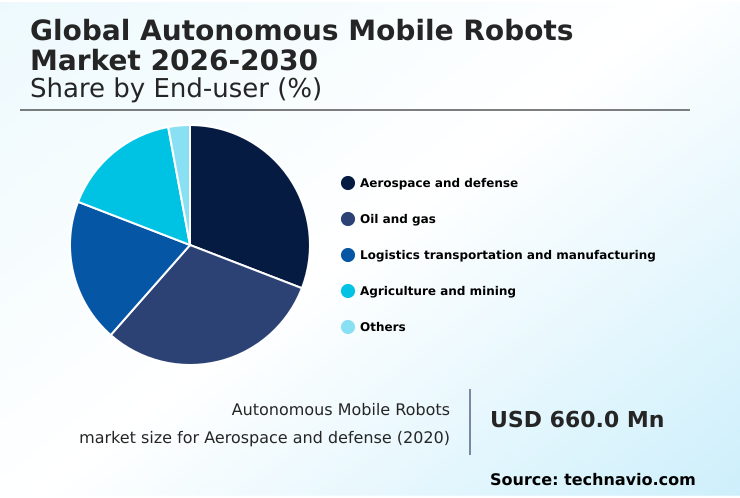

- By End-user - Aerospace and defense segment was valued at USD 1.45 billion in 2024

- By Component - Hardware segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 22.53 billion

- Market Future Opportunities: USD 19.04 billion

- CAGR from 2025 to 2030 : 34.4%

Market Summary

- The autonomous mobile robots market is undergoing a significant transformation, driven by the convergence of operational needs and technological maturity. Persistent labor shortages and the high velocity of e-commerce are compelling organizations to rethink intralogistics, moving beyond manual processes toward scalable automation.

- A key business scenario involves a third-party logistics provider adopting a flexible fleet of autonomous mobile robots to manage seasonal demand spikes without hiring temporary staff, thereby maintaining service level agreements and improving workforce utilization. This shift is facilitated by advancements in AI, which enable robots to navigate complex, dynamic warehouse environments safely alongside human workers.

- While the initial investment remains a consideration, the adoption of Robots-as-a-Service (RaaS) models is lowering the barrier to entry. However, achieving seamless interoperability between robots from different vendors and integrating them with existing warehouse management systems remains a critical hurdle for unlocking the full potential of these intelligent systems and realizing a truly connected, efficient supply chain.

What will be the Size of the Autonomous Mobile Robots Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Autonomous Mobile Robots Market Segmented?

The autonomous mobile robots industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

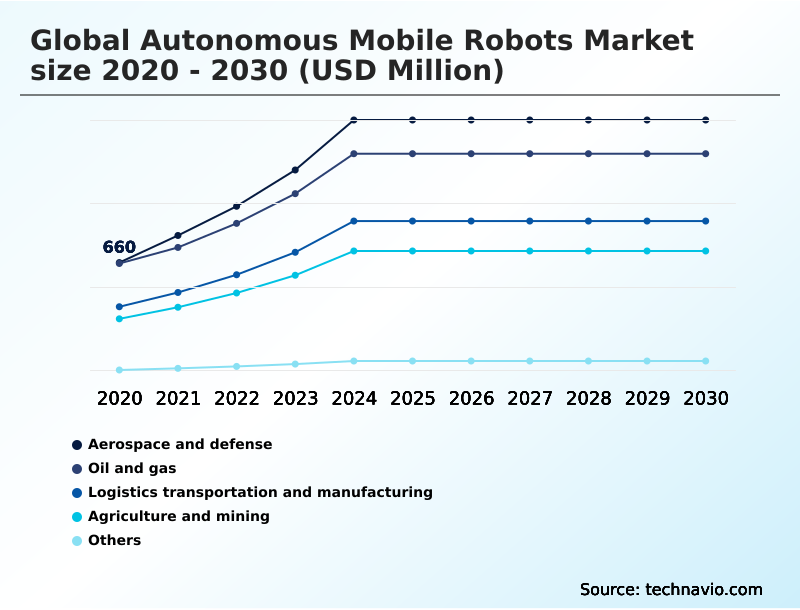

- Aerospace and defense

- Oil and gas

- Logistics transportation and manufacturing

- Agriculture and mining

- Others

- Component

- Hardware

- Software

- Services

- Technology

- Laser or LiDAR

- Vision guidance

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- South Korea

- Europe

- Germany

- UK

- France

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By End-user Insights

The aerospace and defense segment is estimated to witness significant growth during the forecast period.

In the aerospace and defense sector, autonomous logistics solutions are being deployed to modernize supply chains and manufacturing. These systems utilize advanced autonomous navigation and AI-driven path planning to ensure the precise and timely movement of critical components.

The use of vision-guided vehicles and quadrupedal robots enhances automated material handling in both assembly plants and forward-operating bases, improving mission readiness by reducing resupply turnaround times by over 30%.

This shift toward robotic process automation supports predictive maintenance for robots and increases operational resilience in contested environments.

The underlying industrial mobility platforms are also being adapted for adjacent applications, including mining automation robots, demonstrating the versatility of the core lidar sensor fusion technologies.

The Aerospace and defense segment was valued at USD 1.45 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Autonomous Mobile Robots Market Demand is Rising in North America Request Free Sample

The geographic landscape is characterized by distinct regional dynamics, with North America poised to contribute over 35.4% of the market's incremental growth, driven by mature e-commerce and logistics sectors.

In this region, visual slam technology and edge computing in robotics are key differentiators. Meanwhile, APAC is the fastest-growing region, where 5G enabled robotics and swarm intelligence are being rapidly adopted in smart factories, particularly in China and South Korea.

Europe focuses on precision manufacturing, championing interoperability for industrial transport vehicles and heavy-payload transport.

Across all regions, specialized applications are emerging, such as robotics in healthcare logistics and reverse logistics automation, where multi-camera 3d perception improves accuracy for tasks like autonomous inventory tracking.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Businesses evaluating the adoption of autonomous mobile robots must consider several strategic factors beyond initial procurement. A thorough analysis of the total cost of autonomous mobile robots deployment is essential, looking past the hardware price to include integration, training, and infrastructure modifications.

- Calculating the roi for warehouse automation robotics requires a clear understanding of expected efficiency gains and labor cost reductions. Adherence to safety standards for collaborative robots is non-negotiable, particularly when integrating amrs with wms systems to ensure seamless data flow and task management.

- Choosing the best amr for e-commerce fulfillment often involves a detailed comparison of lidar vs vision guidance for amrs, as each technology offers distinct advantages in different environments. For facilities with mixed fleets, overcoming amr interoperability challenges is a primary concern, making vda 5050 compliance for amrs a critical requirement in many sectors.

- The rise of raas models for small businesses is democratizing access, though a deep dive into amr fleet management software comparison remains crucial. The benefits of visual slam in amrs, such as enhanced flexibility, are driving adoption, especially in amr applications in automotive industry and for autonomous mobile robots for hospitals.

- Learning how to implement amrs in existing warehouse environments without significant disruption is key to success, often supported by open source software for mobile robots. Specialized use cases, like amr solutions for cold chain logistics and heavy-duty amrs for industrial transport, demonstrate the technology's adaptability, ultimately focused on reducing operational costs with amrs.

- Companies that successfully navigate these complexities often see productivity gains more than double those who take a piecemeal approach.

What are the key market drivers leading to the rise in the adoption of Autonomous Mobile Robots Industry?

- Increasing labor shortages coupled with rising workforce costs are key drivers compelling industries to adopt automation solutions.

- Market growth is primarily fueled by the intense pressures of modern commerce and persistent labor challenges. The rapid expansion of e-commerce fulfillment automation is a direct response to consumer demand for faster delivery, which requires advanced warehouse automation technologies.

- Systems built for goods-to-person picking, featuring collaborative mobile robots and sophisticated robotic picking systems, can handle peak season order volumes that are three to four times higher than average.

- These solutions, including specialized piece-picking robots and sortation robots, are essential for managing omni-channel fulfillment in automated fulfillment centers.

- With ai-powered fleet coordination, these warehouse robots and systems for robotic order picking directly address labor gaps that can reach up to 20% of the required workforce.

What are the market trends shaping the Autonomous Mobile Robots Industry?

- The integration of generative artificial intelligence with emerging humanoid form factors represents a transformative trend, creating a new class of general-purpose robots capable of complex reasoning and physical interaction.

- Key market trends are converging to create more intelligent and versatile automation. The development of foundation models for robotics and the emergence of the bipedal humanoid robot are pushing the boundaries of what general-purpose robots can accomplish in dynamic settings. This enables sophisticated humanoid robot deployment in flexible manufacturing systems designed for human interaction.

- Concurrently, the drive for interoperability standards like vda 5050 is critical for smart factory integration, allowing for advanced robotic fleet orchestration. This enables facilities to run mobile manipulators alongside other systems seamlessly. Using digital twin simulation, operators can now optimize workflows before deployment, improving task allocation efficiency by over 25% and paving the way for fully automated lights-out warehouses.

What challenges does the Autonomous Mobile Robots Industry face during its growth?

- Ensuring safe and reliable navigation in dynamic, unstructured environments presents a significant challenge to the widespread adoption and growth of the industry.

- Despite strong drivers, significant implementation hurdles persist. Ensuring safe human-robot collaboration in dense, dynamic environments remains a primary concern, necessitating advanced fleet management software and 3d vision cameras on mobile cobot systems. The lack of universal interoperability, despite efforts like the massrobotics interoperability standard, often complicates the integration of multi-vendor supply chain robotics, extending deployment timelines by several months.

- Furthermore, the high initial investment for automated guided vehicles (agvs) and other hardware is a barrier for many, even with the availability of robots-as-a-service (raas) models. Integrating these systems for tasks like automated pallet handling or just-in-time material delivery can require infrastructure upgrades that account for 15-20% of the total project cost.

Exclusive Technavio Analysis on Customer Landscape

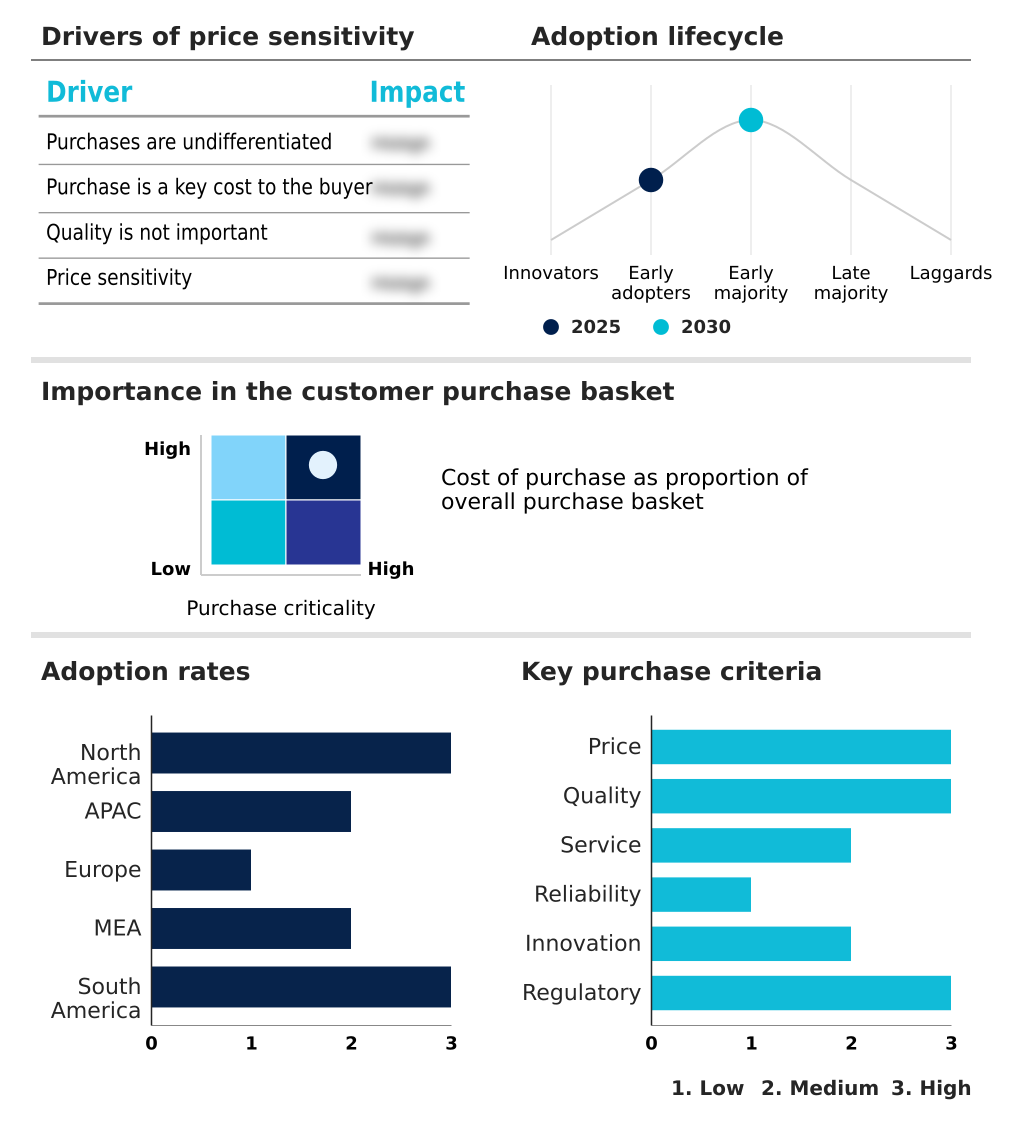

The autonomous mobile robots market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the autonomous mobile robots market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Autonomous Mobile Robots Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, autonomous mobile robots market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

6 River Systems Inc. - Offers collaborative mobile robot systems designed to streamline fulfillment automation and enhance warehouse operational workflows.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 6 River Systems Inc.

- ABB Ltd.

- Aethon Inc.

- AGILOX Services GmbH

- Clearpath Robotics Inc.

- Fetch Robotics Inc.

- Geekplus Technology Co. Ltd.

- Grey Orange Pte. Ltd.

- inVia Robotics Inc.

- KUKA AG

- Locus Robotics Corp.

- Magazino GmbH

- Mobile Industrial Robots AS

- OMRON Corp.

- Seegrid Corp.

- Swisslog Holding AG

- Symbotic Inc.

- Vecna Robotics Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Autonomous mobile robots market

- In September, 2024, Agility Robotics opened RoboFab, a 70,000-square-foot facility in Oregon dedicated to the mass production of its bipedal humanoid robot, Digit, for logistics applications.

- In October, 2024, ANYbotics entered into a long-term agreement with SLB to provide end-to-end robotics services, deploying its autonomous quadruped robot for inspection and maintenance in the oil and gas industry.

- In March, 2025, NVIDIA launched its Isaac GR00T foundation model and enhanced software libraries, providing a standardized, hardware-agnostic platform to accelerate the development of autonomous mobile robots and humanoids.

- In April, 2025, Locus Robotics announced it had surpassed the 5 billion picked items milestone, highlighting the scalability and success of its Robots-as-a-Service (RaaS) subscription model in warehouse fulfillment.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Autonomous Mobile Robots Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 303 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 34.4% |

| Market growth 2026-2030 | USD 19040.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 28.6% |

| Key countries | US, Canada, Mexico, China, Japan, South Korea, India, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, UAE, Saudi Arabia, South Africa, Israel, Egypt, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is rapidly evolving beyond simple conveyance, with a strategic pivot toward intelligent, collaborative systems. The integration of advanced autonomous navigation, including simultaneous localization and mapping and visual slam technology, is becoming standard. This allows for sophisticated human-robot collaboration and enables complex applications like robotic picking systems and mobile manipulation.

- Fleet management software now leverages ai-powered fleet coordination and swarm intelligence to orchestrate diverse fleets of collaborative mobile robots, piece-picking robots, and sortation robots. Interoperability standards, such as vda 5050 and the massrobotics interoperability standard, are addressing vendor lock-in, a key boardroom concern.

- This shift toward software-defined capabilities, supported by foundation models for robotics and edge computing in robotics, is crucial. As hardware like warehouse robots and vision-guided vehicles becomes more accessible through robots-as-a-service (raas) models, the focus shifts to optimizing robotic process automation to handle tasks like heavy-payload transport, with some deployments reducing order fulfillment cycle times by up to 40%.

What are the Key Data Covered in this Autonomous Mobile Robots Market Research and Growth Report?

-

What is the expected growth of the Autonomous Mobile Robots Market between 2026 and 2030?

-

USD 19.04 billion, at a CAGR of 34.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Aerospace and defense, Oil and gas, Logistics transportation and manufacturing, Agriculture and mining, and Others), Component (Hardware, Software, and Services), Technology (Laser or LiDAR, Vision guidance, and Others) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing labor shortages and rising workforce costs, Safety and navigation in dynamic, unstructured environments

-

-

Who are the major players in the Autonomous Mobile Robots Market?

-

6 River Systems Inc., ABB Ltd., Aethon Inc., AGILOX Services GmbH, Clearpath Robotics Inc., Fetch Robotics Inc., Geekplus Technology Co. Ltd., Grey Orange Pte. Ltd., inVia Robotics Inc., KUKA AG, Locus Robotics Corp., Magazino GmbH, Mobile Industrial Robots AS, OMRON Corp., Seegrid Corp., Swisslog Holding AG, Symbotic Inc. and Vecna Robotics Inc.

-

Market Research Insights

- Market dynamics are shifting as businesses leverage autonomous logistics solutions to achieve significant operational gains, with some facilities reporting that robotic order picking can be up to 80% faster than manual methods. The adoption of warehouse automation technologies is accelerating, driven by the need for more flexible manufacturing systems to support omni-channel fulfillment and just-in-time material delivery.

- This evolution in supply chain robotics enables companies to meet fluctuating consumer demands, improving throughput by more than double during peak seasons. As a result, investments in intralogistics automation and smart factory integration are becoming central to strategic planning, focusing on scalable and efficient automated material handling.

We can help! Our analysts can customize this autonomous mobile robots market research report to meet your requirements.