Baby Food Packaging Market Size 2024-2028

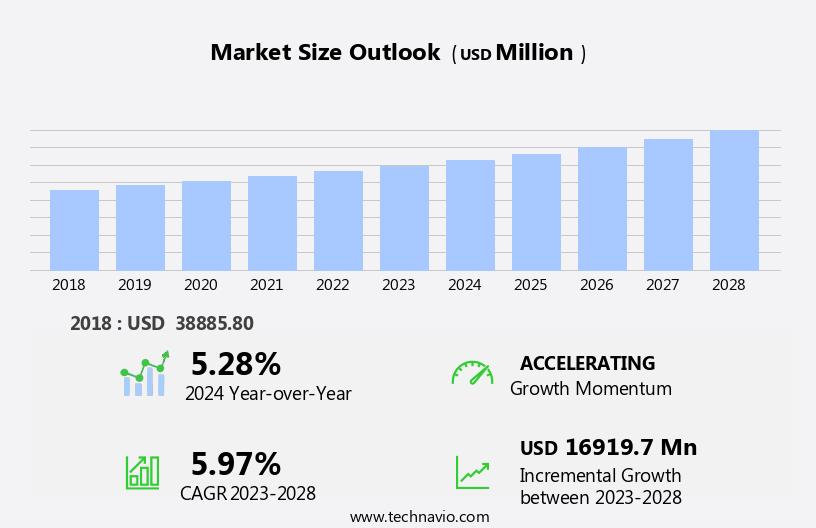

The baby food packaging market size is forecast to increase by USD 16.92 billion at a CAGR of 5.97% between 2023 and 2028.

What will be the Size of the Baby Food Packaging Market During the Forecast Period?

How is this Baby Food Packaging Industry segmented and which is the largest segment?

The baby food packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Milk formula

- Prepared baby food

- Dried baby food

- Others

- Packaging

- Rigid packaging

- Flexible packaging

- Geography

- APAC

- China

- India

- North America

- US

- Europe

- Germany

- Middle East and Africa

- South America

- Brazil

- APAC

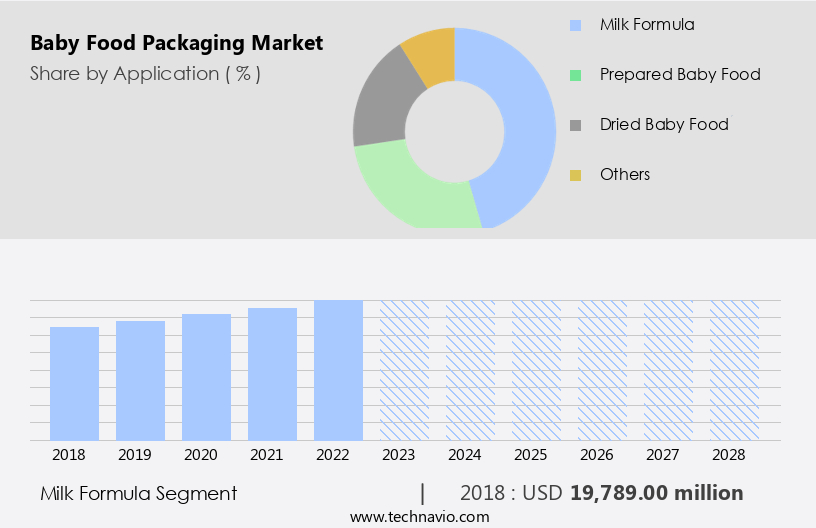

By Application Insights

The milk formula segment is estimated to witness significant growth during the forecast period. The market encompasses various types of packaging for milk formula, dried baby food, and prepared baby food. In 2023, milk formula held the largest market share due to population growth and changing demographics. Sustainability is a growing concern, leading to the demand for eco-friendly packaging solutions, such as recyclable, biodegradable, or renewable materials. Milk formula comes in various forms, including powder, liquid concentrate, and ready-to-use, each requiring specific packaging. Working parents prefer larger pack sizes and convenient packaging, such as flexible plastic packs, stand-up pouches, and liquid carton packaging. Baby food manufacturers employ food technologies to ensure nutritional content, purity, and safety.

Sustainable packaging materials, like thin wall packaging and lightweight options, are increasingly popular. Brands focus on brand recognition, loyalty, and promotional activity through retail space, graphics, logos, and social media pages.

Get a glance at the market report of various segments Request Free Sample

The Milk formula segment was valued at USD 19.79 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

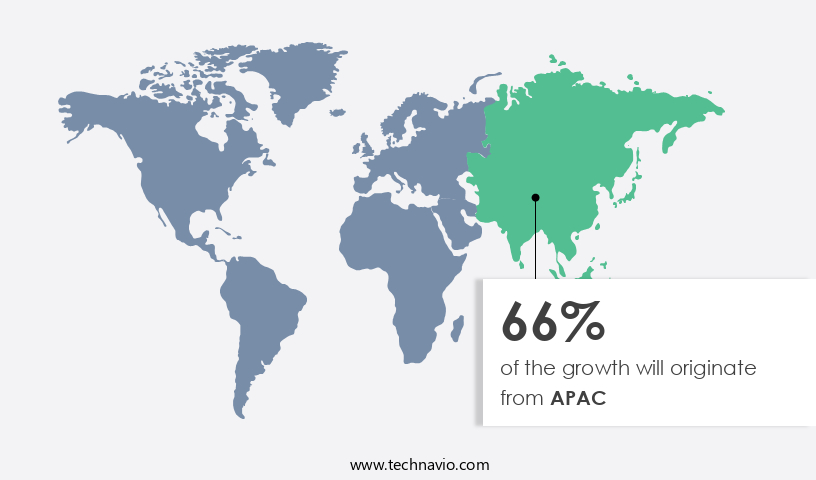

APAC is estimated to contribute 66% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The APAC the market is projected to expand due to improved economic conditions in countries like China, India, Indonesia, and Australia. This economic growth has led to increased investments in various sectors, including baby food, as urbanization and changing lifestyles drive demand for convenient, packaged options. The e-commerce sector's significant growth is a major catalyst for market expansion. Consumers In the region are shifting towards packaged foods, including baby food and ready-to-eat meals, over traditional, cooked options. Sustainable packaging materials, such as eco-friendly pouches and cartons, are gaining popularity due to increasing environmental concerns. Baby food manufacturers prioritize food safety and employ advanced food technologies to ensure product quality and nutritional content.

The market caters to infants and toddlers, offering various formats like liquid milk formula, dried baby food, powder milk formula, prepared baby food, and pureed food in packaging solutions such as plastic containers, folding cartons, stand-up pouches, and liquid carton packaging.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Baby Food Packaging Industry?

- Increase in demand for pouch packaging is the key driver of the market.The market is witnessing a significant shift towards flexible packaging, particularly pouches, due to their convenience and sustainability. Pouches offer advantages such as sealability, ease of use, and portability, making them a preferred choice for working parents and infants or toddlers on-the-go. New advancements in pouch technology, including fitments and improved product evacuation, are expected to further reduce costs and increase consumer appeal. Compared to rigid packaging materials like Glass jars, Metal Cans, and Plastic containers, pouches are more lightweight and offer a smaller carbon footprint. This eco-friendly trend aligns with the growing demand for sustainable packaging materials and recyclable packaging solutions.

The market for prepared baby food, liquid milk formula, dried baby food, and powder milk formula is anticipated to grow steadily during the forecast period, with stand-up pouches being a key packaging solution.

What are the market trends shaping the Baby Food Packaging market?

- Portion-controlled packaging is the upcoming market trend.In the baby food market, portion-controlled packaging plays a significant role in catering to the needs of working parents and caregivers. Prepackaged individual portions of baby food, available in various formats such as pouches, containers, and cartons, eliminate the need for measuring and preparing food each time, ensuring quick and easy servings. These options also help parents maintain precise portion sizes, promoting healthy eating habits for infants and toddlers. The demand for portion-controlled packaging is driven by factors including convenience, safety, and hygiene. Parents value the convenience of ready-to-serve baby food, which saves time and effort. Additionally, safety and hygiene concerns are addressed through the use of airtight containers and pouches that preserve the nutritional content and prevent contamination.

Flexible packaging, such as stand-up pouches and thin-wall containers, are popular choices due to their lightweight and easy-to-use features. Eco-friendly packaging, including biodegradable materials and recyclable packaging, is also gaining popularity among environmentally-conscious parents. Baby food manufacturers are continuously exploring food technologies to improve the nutritional content of their products, offering a range of options such as liquid milk formula, dried baby food, powder milk formula, and prepared baby food. These products are available in various packaging formats, including bottles, metal cans, cartons, jars, and pouches. Parents today are increasingly seeking sustainable packaging materials, such as paper and paperboard, for their baby food products.

These materials offer advantages such as lightweight, reusability, and ease of use, while also reducing the environmental impact of disposable packaging. Brand recognition and loyalty are essential factors In the baby food market, and packaging plays a crucial role in establishing a strong brand identity. Effective use of graphics, logos, and designs on packaging can help differentiate products and attract customers. In conclusion, the baby food market is driven by the demand for convenient, safe, and eco-friendly packaging solutions. Parents seek portion-controlled packaging that offers ease of use, hygiene, and precision, while also addressing their concerns for the environment.

Baby food manufacturers continue to innovate and explore new packaging technologies to meet the evolving needs of parents and caregivers.

What challenges does the Baby Food Packaging Industry face during its growth?

- High food perishability of baby food products is a key challenge affecting the industry growth.Baby food packaging is a crucial aspect of ensuring the safety and preservation of perishable items for infants and toddlers. companies face challenges in packaging these products due to their sensitivity to environmental factors, necessitating specialized materials and preservatives for extended shelf life. For instance, plastic containers with airtight seals and metal cans are commonly used for liquid milk formula, while glass jars and paperboard cartons are preferred for dried baby food and prepared foods, respectively. Eco-friendly packaging solutions, such as flexible plastic packs, eco-friendly pouches, and thin wall packaging made of biodegradable materials, are gaining popularity among working parents.

However, defects in packaging can adversely impact the quality and safety of the baby food, as demonstrated by the discovery of heavy metals in certain baby food products in 2021. Therefore, packaging companies must prioritize safety concerns and invest in high-quality, sustainable packaging materials, such as recyclable paper and paperboard, to maintain brand recognition and loyalty among consumers. Promotional activities, including graphics, logos, designs, and nutritional content, also play a significant role in attracting consumers to ready nutrition products. Overall, baby food manufacturers must balance the need for convenient, flexible, and eco-friendly packaging with the importance of maintaining the nutritional integrity and safety of their products.

Exclusive Customer Landscape

The baby food packaging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the baby food packaging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, baby food packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

ABC Packaging Direct - The market encompasses innovative solutions for sustainable and recyclable packaging. One notable offering includes AmPrima PE Plus Recycle-Ready Solutions for Liquid Pouches, which prioritize recyclability and reduce environmental impact. Additionally, AmLite HeatFlex packaging provides flexibility and heat resistance, making it an optimal choice for baby food applications. These advanced packaging solutions cater to the evolving demands of the baby food industry, ensuring product safety, convenience, and eco-friendliness.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABC Packaging Direct

- Amcor Plc

- AptarGroup Inc.

- Ardagh Group SA

- Ashtonne Packaging

- BEAPAK

- Berry Global Inc.

- Cascades Inc.

- Dow Chemical Co.

- DS Smith Plc

- Guala Pack S.p.a.

- Logos Packaging

- Mondi Plc

- Printpack Inc.

- ProAmpac Holdings Inc.

- Sealed Air Corp.

- Silgan Holdings Inc.

- Smurfit Kappa Group

- Sonoco Products Co.

- Winpak Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The baby food market is a significant sector withIn the broader food industry, catering to the unique nutritional needs of infants and toddlers. This market encompasses various packaging formats, each offering distinct advantages to parents and caregivers. Packaging plays a crucial role in preserving the nutritional content and ensuring the safety of baby food. Plastic containers, jars, and metal cans have long been popular choices due to their durability and airtight seals. However, there is a growing trend towards more eco-friendly and convenient packaging solutions. Paperboard cartons and pouches have gained popularity due to their lightweight and flexible nature.

These packaging formats offer several benefits, including ease of use, portability, and recyclability. Eco-friendly pouches made of single material, such as biodegradable films, are increasingly being adopted to reduce environmental impact. Larger pack sizes in folding cartons and stand-up pouches cater to the needs of working parents who require convenient and time-saving options. These packaging solutions also offer ample space for graphics, logos, and designs, making them effective for brand recognition and loyalty. Safety concerns are a top priority in baby food packaging. Food processing technologies ensure the food remains free from contamination and maintains its nutritional value.

Barrier bags made of plastic or other materials help preserve the food's freshness and prevent spoilage. Ready nutrition products, such as liquid milk formula and dried baby food, often come in plastic containers or eco-friendly pouches. Powder milk formula is typically packaged in metal cans or stand-up pouches to maintaIn the product's quality and prevent contamination. The market for baby food packaging is diverse and dynamic, with various packaging materials and formats catering to the evolving needs of parents and caregivers. Factors such as convenience, sustainability, and safety continue to influence the development of new packaging solutions. As the demand for eco-friendly and convenient packaging grows, manufacturers are exploring sustainable packaging materials, such as recyclable paper and paperboard, and thin wall packaging.

These materials offer reduced weight, improved recyclability, and a smaller carbon footprint. Brand recognition and loyalty are essential In the baby food market, and packaging plays a crucial role in establishing a strong brand identity. Social media pages and promotional activities help boost brand awareness and engage consumers. In conclusion, the market is a dynamic and evolving sector, driven by the needs of parents and caregivers. Packaging formats, materials, and technologies continue to adapt to meet the demands for convenience, sustainability, and safety. The future of baby food packaging is focused on eco-friendly, convenient, and safe solutions that cater to the unique needs of infants and toddlers.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

181 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.97% |

|

Market growth 2024-2028 |

USD 16919.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.28 |

|

Key countries |

China, US, India, Germany, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Baby Food Packaging Market Research and Growth Report?

- CAGR of the Baby Food Packaging industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the baby food packaging market growth of industry companies

We can help! Our analysts can customize this baby food packaging market research report to meet your requirements.

RIA -

RIA -