Battery Chargers Market Size 2024-2028

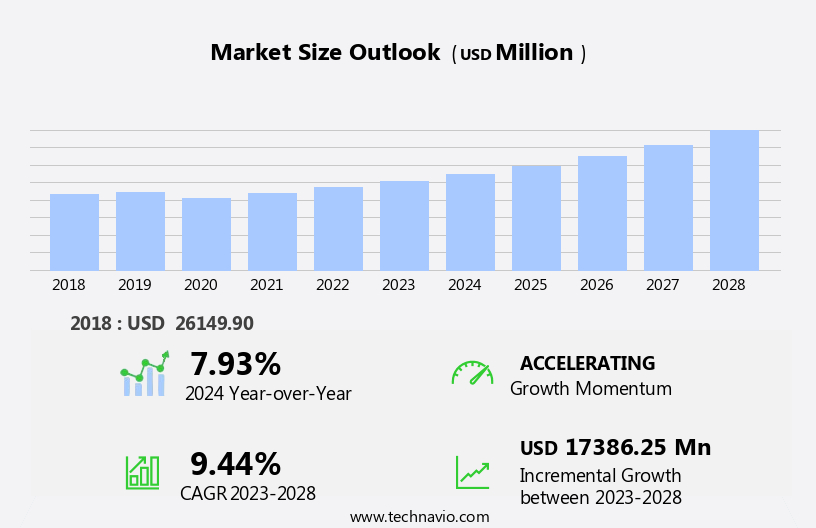

The battery chargers market size is forecast to increase by USD 17.39 billion, at a CAGR of 9.44% between 2023 and 2028.

- The market is witnessing significant growth, driven by the increasing adoption of electric vehicles and the rising demand for automatic battery chargers. These trends are shaped by the global shift towards sustainable energy solutions and the convenience offered by automatic chargers. However, the market faces challenges, primarily in the form of compatibility issues with various battery types and models. Manufacturers must address these challenges by ensuring their chargers are universally compatible or offering customized solutions for specific battery types.

- By focusing on innovation and addressing compatibility concerns, companies can capitalize on the growing market demand and gain a competitive edge.

What will be the Size of the Battery Chargers Market during the forecast period?

The battery charger market is characterized by its continuous evolution and dynamic nature, driven by advancements in charging technologies and their applications across various sectors. Charging current, from level 1 to level 3, is a critical aspect of this market, with fast charging and charging optimization gaining significant attention due to their ability to reduce charging times and improve efficiency. Energy storage solutions, such as batteries with increased capacity and advanced power delivery, are essential components of this market, with lithium-ion batteries leading the charge. Industries like consumer electronics, electric vehicles, and renewable energy are major consumers of these charging technologies.

Charging services, including charging stations and charging networks, are becoming increasingly important as the demand for convenient and reliable charging solutions grows. Short circuit protection, charging security, and charging analytics are essential features that ensure safe and efficient charging. Battery life and battery health are significant concerns, leading to the development of charging management systems and battery management systems. Nickel-cadmium, lead-acid, nickel-metal hydride, and lithium-ion batteries are among the popular types of batteries used, each with its unique advantages and challenges. Resonant charging, wireless charging, and inductive charging are emerging charging technologies that offer greater convenience and flexibility. Charging infrastructure, charging reliability, and charging networks are essential for ensuring seamless charging experiences.

Temperature control, over-discharge protection, and overcharging protection are crucial safety features. The market for charging solutions is vast and diverse, with applications ranging from portable chargers and power banks to charging adapters, power tools, and emergency power supplies. Charging protocols and charging speeds are essential factors in optimizing charging efficiency and reducing charging time. Solar chargers and smart charging are becoming increasingly popular as renewable energy sources gain traction. In conclusion, the battery charger market is a dynamic and evolving landscape, driven by technological advancements and the growing demand for efficient and convenient charging solutions across various industries. Charging current, energy storage, battery capacity, power delivery, and charging optimization are key areas of focus, with safety and reliability being critical considerations.

The market for charging solutions is vast and diverse, with applications ranging from consumer electronics to electric vehicles and renewable energy.

How is this Battery Chargers Industry segmented?

The battery chargers industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Electronic products

- Vehicles (EV)

- Industrial machinery

- Others

- Type

- Wired

- Wireless

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

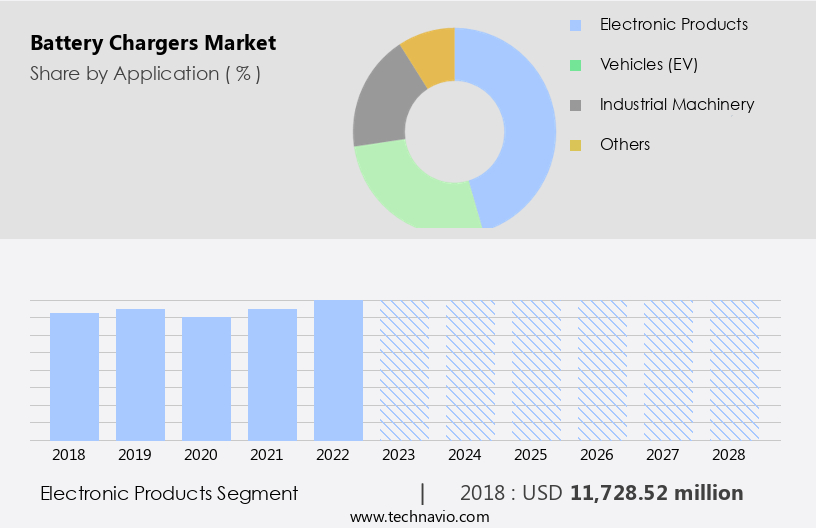

By Application Insights

The electronic products segment is estimated to witness significant growth during the forecast period.

The market for battery chargers has experienced significant growth due to the increasing use of portable electronic devices such as smartphones, tablets, laptops, wearables, and wireless earbuds. Consumers require reliable charging solutions to keep their devices powered throughout the day. Fast charging technology is gaining popularity, as consumers seek quick and convenient charging options. Manufacturers are responding by producing fast-charging battery chargers that can efficiently replenish device batteries, minimizing downtime and enhancing user experience. The proliferation of multiple electronic devices per household necessitates the ownership of multiple chargers. In addition, various charging technologies, including level 3 charging, resonant charging, and wireless charging, cater to diverse consumer needs.

Energy storage solutions, such as lithium-ion batteries and grid storage, are integral to the battery charger market's expansion. Charging optimization, charging analytics, and charging management systems further improve charging efficiency and effectiveness. The integration of charging services, charging security, and charging safety features adds value to battery chargers. Medical devices, renewable energy, power tools, and off-grid power applications also contribute to the market's growth. Battery capacity, charging voltage, charging data, and charging software are essential considerations for manufacturers to meet consumer demands. The battery charger market encompasses a wide range of products, from portable chargers and charging docks to charging stations and solar chargers.

The market's evolution includes advancements in charging speeds, charging efficiency, charging protocols, and charging infrastructure. Temperature control, overcharging protection, and battery management systems ensure optimal charging performance and battery health.

The Electronic products segment was valued at USD 11.73 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

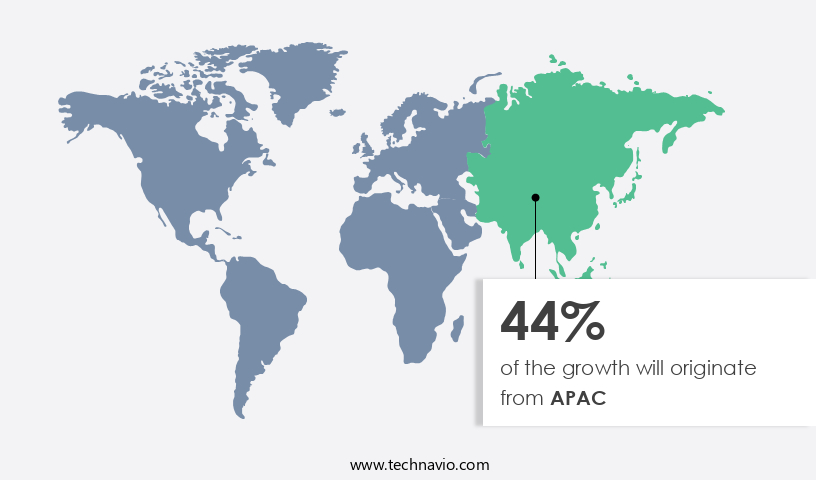

APAC is estimated to contribute 44% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the dynamic and evolving technology landscape, battery chargers play a pivotal role in powering various electronic devices, electric vehicles, and renewable energy systems. The Asia Pacific region, particularly China, India, and Southeast Asian nations, are experiencing rapid economic growth and urbanization, leading to increased adoption of these technologies. With growing urban populations, the demand for portable electronic devices such as smartphones, laptops, tablets, and wearable devices is surging. Battery chargers are essential accessories for these devices, ensuring they remain functional throughout the day. The transition towards electrification of transportation is gaining momentum in APAC countries, driven by concerns about air pollution, energy security, and climate change.

Electric cars, buses, scooters, and bicycles are becoming increasingly popular, leading to a significant increase in demand for electric vehicle chargers. Charging infrastructure is being developed at a rapid pace to support this transition. Battery chargers come in various forms, including Level 1, Level 2, and DC Fast Charging. Fast charging and Level 3 charging are gaining popularity due to their ability to quickly charge batteries, reducing charging time. Charging optimization and energy storage are critical considerations for efficient charging. Lead-acid, nickel-cadmium, nickel-metal hydride, lithium-ion, and other battery types require specific charging protocols to ensure battery health and longevity.

Power delivery, charging voltage, and safety are essential factors in battery charger design. Short circuit protection, overcharging protection, and battery management systems help prevent damage to batteries and ensure charging efficiency. Renewable energy sources such as solar and wind are increasingly being integrated with battery storage systems for backup power and off-grid applications. Inductive and wireless charging technologies are gaining traction in consumer electronics and electric vehicles, offering convenience and ease of use. Charging analytics, charging software, and charging management systems help optimize charging processes and improve overall efficiency. Charging services, charging docks, and charging stations are becoming essential components of the charging infrastructure.

Battery degradation and battery life are critical concerns for battery charger manufacturers and users alike. Charging cables and charging adapters must be designed to ensure charging reliability and prevent overcharging or undercharging. Temperature control and over-discharge protection are essential features for maintaining battery health and ensuring safe charging. In conclusion, the battery charger market is experiencing significant growth due to the increasing adoption of electronic devices, electric vehicles, and renewable energy systems. APAC countries are at the forefront of this trend, with China, India, and Southeast Asian nations leading the way. Battery chargers come in various forms, including portable chargers, charging stations, and charging services, and are essential accessories for ensuring the functionality and longevity of batteries.

Charging optimization, energy storage, power delivery, and safety are critical considerations for battery charger design. The market is witnessing innovation in charging technologies, including fast charging, Level 3 charging, inductive charging, and wireless charging, to meet the evolving needs of consumers and businesses.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Battery Chargers Industry?

- The significant growth in the electric vehicle market can be attributed to the increasing adoption of these eco-friendly vehicles by consumers.

- The expanding electric vehicle (EV) market is fueling the demand for advanced battery chargers. With the rise in global EV sales, there is a growing requirement for reliable and efficient charging infrastructure. Battery chargers are essential components of charging stations, enabling the efficient recharge of EV batteries. The increasing popularity of EVs necessitates the development of innovative charging technologies. These include fast-charging solutions that significantly reduce charging times and bidirectional chargers that offer vehicle-to-grid (V2G) and vehicle-to-home (V2H) capabilities. Effective battery management is crucial in maintaining battery health and charging reliability. Advanced battery chargers offer features such as overcharging protection, temperature control, and over-discharge protection.

- Charging cables and ac/dc converters are also integral components of the charging infrastructure. Off-grid power applications, such as emergency power and remote locations, also rely on battery chargers for power supply. The development of charging networks is essential to support the growing demand for EVs. As the market for EVs continues to evolve, the need for advanced battery chargers will persist, driving innovation and growth in the sector.

What are the market trends shaping the Battery Chargers Industry?

- The increasing need for convenience and efficiency in charging devices has led to a significant rise in the demand for automatic battery chargers. This trend is expected to continue in the upcoming market. Automatic battery chargers offer several advantages, including the ability to charge multiple devices simultaneously and the elimination of the need for manual intervention. As a result, they have become an essential accessory for both personal and professional use.

- Automatic battery chargers have gained popularity due to their ability to charge batteries automatically without the need for manual intervention. These chargers offer several advantages, including fast charging capabilities and advanced charging algorithms that optimize the charging process. The charging algorithms ensure efficient energy transfer and help preserve battery health by preventing overcharging and undercharging. Trickle charging and smart charging profiles are common features in automatic chargers, which help extend battery life and maintain optimal performance.

- Industrial and automotive applications particularly benefit from these features as they require frequent charging and depend on the consistent availability of fully charged batteries. Overall, automatic battery chargers offer a convenient and efficient solution for charging various types of rechargeable batteries.

What challenges does the Battery Chargers Industry face during its growth?

- The growth of the industry is hindered by compatibility issues with battery chargers, which pose a significant challenge.

- In the realm of battery technology, ensuring compatibility between chargers and the batteries they power is essential for safe and efficient charging. With diverse battery chemistries, voltages, and charging protocols, this challenge is particularly prominent. Lead-acid batteries, such as those found in cars, come in various types, including flooded, absorbent glass mats (AGM), and sealed lead-acid. Each type necessitates specific charging voltages and algorithms to prevent overcharging, undercharging, or battery damage. Industrial battery chargers play a crucial role in powering equipment, from material handling vehicles and warehouse automation systems to renewable energy systems. These chargers may be integrated into larger systems, necessitating a deep understanding of charging optimization, energy storage, power delivery, and short circuit protection.

- Fast charging and level 3 charging have gained significant attention in recent research. Lithium-ion batteries, for instance, require specific charging protocols to maintain battery life and prevent thermal runaway. Nickel-cadmium batteries, while less common, also require unique charging methods. Resonant charging and charging services are alternative charging methods that offer advantages in terms of efficiency and compatibility. Energy storage systems, including grid storage, also rely on advanced battery chargers to ensure optimal performance and longevity. The integration of these systems into larger power grids necessitates a high degree of charging optimization and power delivery. In conclusion, the compatibility of battery chargers with the batteries they power is a critical consideration.

- Understanding the specific charging requirements of various battery types, such as lead-acid, lithium-ion, and nickel-cadmium, is essential for ensuring safe, efficient, and long-lasting charging. Additionally, advanced charging methods, such as fast charging, level 3 charging, and resonant charging, offer advantages in terms of efficiency and compatibility.

Exclusive Customer Landscape

The battery chargers market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the battery chargers market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, battery chargers market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alexander Battery Technologies - The company specializes in engineered battery charging solutions, including custom chargers tailored to the unique specifications of various battery packs. Our offerings ensure optimal charging efficiency and longevity, catering to diverse industries and applications. These advanced chargers are meticulously designed to meet specific charging requirements, enhancing overall system performance and reliability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alexander Battery Technologies

- CHILWEE GROUP Co.

- CTEK Sweden AB

- EnerSys

- Enertechups

- Exide Technologies

- FSP Group

- GERMAREL GmbH

- La Marche Manufacturing Co.

- LG Electronics Inc.

- Micropower Group AB

- Motor Applications Corp.

- POWERTRON INDIA PVT. LTD

- Pro Charging Systems

- RB Solar Energy

- Robert Bosch GmbH

- Samlex Europe B.V.

- Samsung Electronics Co. Ltd.

- Schumacher Electric Corp.

- Shenzhen Depowersupply Electrical Co., Ltd.

- ShenZhen QuawinTEC Technology Co., Ltd. Â

- Stanley Black and Decker Inc.

- The Brookwood Group

- The NOCO Co.

- Volt Control System

- VTEK ELECTRIC ITH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Battery Chargers Market

- In February 2023, Tesla, a leading electric vehicle (EV) manufacturer, unveiled its new Megacharger, a high-power charging station capable of delivering up to 20 miles of range per minute for Tesla's Semi trucks and Model X and S Plaid vehicles (Tesla Press Release, 2023). This development signifies a significant advancement in charging infrastructure, aiming to reduce charging times for EVs, making long-distance travel more viable.

- In July 2024, BYD Company Limited, a major Chinese battery manufacturer, announced a strategic partnership with Ford Motor Company to supply batteries and electric vehicle platforms for Ford's new EV lineup (Ford Press Release, 2024). This collaboration marks a significant expansion of BYD's presence in the global automotive market and underscores the growing importance of partnerships between battery manufacturers and automakers.

- In October 2024, LG Chem, a leading global battery manufacturer, raised USD1.8 billion in a share sale to fund its expansion into the battery recycling business (Reuters, 2024). This investment represents a significant shift in the battery industry, as companies focus on circular economy solutions to address the environmental impact of lithium-ion batteries and secure a sustainable supply of raw materials.

- In December 2025, the European Union passed the Battery Regulation, setting strict rules for the production, collection, treatment, and recycling of batteries (European Commission, 2025). This regulatory development is expected to drive innovation in battery technology, improve sustainability, and ensure a consistent supply of batteries for the growing EV market in Europe.

Research Analyst Overview

- The market is witnessing significant growth, driven by the increasing adoption of energy storage solutions and the proliferation of electric vehicles (EVs). Charging safety standards are becoming increasingly stringent to ensure reliable and efficient energy transfer. Power management systems, including demand response and energy efficiency, are essential for optimizing battery usage and reducing energy waste. Charging cybersecurity is also gaining importance to protect against potential threats during the charging process. Energy harvesting and battery recycling are emerging trends, offering opportunities for cost savings and reducing environmental impact. Charging infrastructure development is accelerating, with smart grids and wireless power transfer technologies enabling seamless integration of renewable energy sources.

- Power electronics, charging algorithms, and integrated circuits are key components enabling advanced charging functionality. Fuel cells and charging regulations are also influencing the market, with regulations driving the adoption of standardized charging protocols and fuel cells providing an alternative to batteries for certain applications. Charging network expansion and energy management systems are essential for managing the increasing demand for charging infrastructure and ensuring grid stability. Thermal management is crucial for maintaining optimal charging temperatures and extending battery life.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Battery Chargers Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

165 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.44% |

|

Market growth 2024-2028 |

USD 17386.25 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.93 |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Battery Chargers Market Research and Growth Report?

- CAGR of the Battery Chargers industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the battery chargers market growth of industry companies

We can help! Our analysts can customize this battery chargers market research report to meet your requirements.

RIA -

RIA -