Bioplastics For Agribusiness Market Size 2024-2028

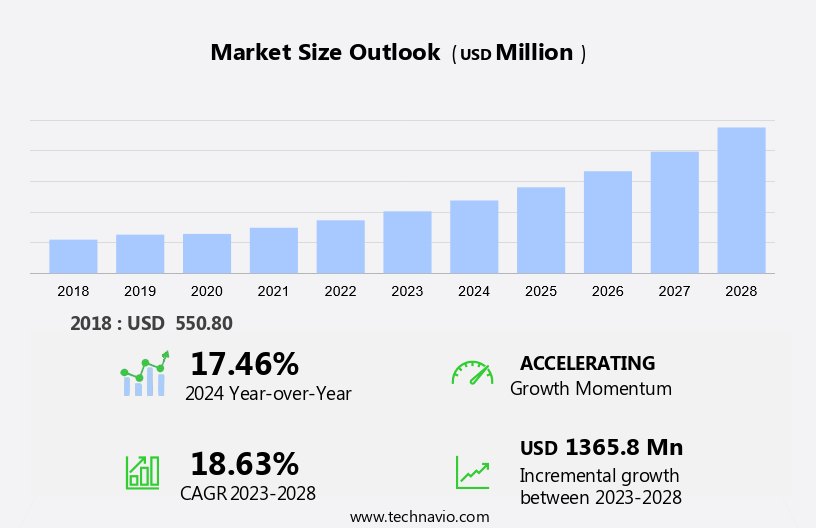

The bioplastics for agribusiness market size is forecast to increase by USD 1.37 billion at a CAGR of 18.63% between 2023 and 2028.

- The bioplastics market for agribusiness is experiencing significant growth due to the increasing emphasis on environmental sustainability. Companies are investing heavily in research and development of innovative bioplastics, such as Polybutylene Succinate, to meet this demand. However, the cost-effectiveness of conventional plastics remains a challenge. In the US, agribusinesses are integrating bioplastics into their operations through the use of greenhouses and irrigation systems.

- Additionally, biomaterials are also being utilized for silage storage to extend the shelf life of crops and reduce waste. The adoption of compostable bioplastics is also on the rise, as they offer a sustainable alternative to traditional plastic packaging. As the focus on sustainability continues to grow, the bioplastics market for agribusiness is poised for continued expansion. This trend is expected to drive market growth and provide opportunities for companies to offer eco-friendly solutions to their clients.

What will be the Size of the Market During the Forecast Period?

- Bioplastics, derived from renewable biomass, are gaining significant attention in the agribusiness sector due to their eco-friendly properties. These bio-based polymers offer sustainable alternatives to traditional plastic materials, contributing to waste management and environmental sustainability. Bioplastics find extensive applications in agriculture, including biodegradable packaging, planting containers, greenhouse materials, and controlled-release fertilizers. Biodegradable bioplastics and compostable bioplastics are particularly popular due to their ability to decompose naturally, reducing the environmental impact of plastic waste. Aliphatic polyesters and cellulose-based bioplastics are two common types of bioplastics used in agribusiness.

- Additionally, aliphatic polyesters, such as polylactic acid and polyhydroxyalkanoates, are derived from renewable resources like corn starch and sugarcane. Cellulose-based bioplastics, made from plant fibers, offer excellent biodegradability and can be used as mulch in greenhouses and irrigation systems. Organic polyethylene and starch-based bioplastics are other types of bioplastics used in agriculture. Organic polyethylene, a biodegradable alternative to conventional polyethylene, is used for making greenhouse films and mulch films. Starch-based bioplastics are used for manufacturing planting pots and seedling trays. Environmental regulations are increasingly driving the adoption of bioplastics in agribusiness.

- Furthermore, farming practices that prioritize sustainability and reduce environmental impact are also adopting bioplastics. Biodegradable bioplastics offer a solution to plastic waste, while compostable bioplastics contribute to organic waste management. Bioplastics offer sustainable alternatives to traditional plastic materials in the agribusiness sector. From biodegradable packaging and planting containers to greenhouse materials and controlled-release fertilizers, bioplastics contribute to waste management, environmental sustainability, and farming practices. As environmental regulations become stricter and consumers demand more eco-friendly solutions, the use of bioplastics in agribusiness is expected to grow.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Biodegradable

- Non-Biodegradable

- Application

- Greenhouse

- Irrigation

- Others

- Geography

- Europe

- Germany

- UK

- France

- Italy

- APAC

- China

- North America

- US

- South America

- Middle East and Africa

- Europe

By Type Insights

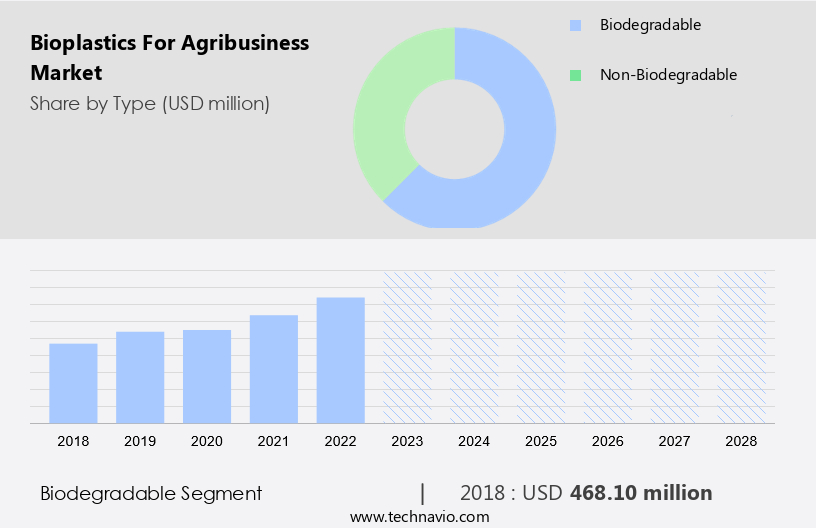

- The biodegradable segment is estimated to witness significant growth during the forecast period.

Biodegradable bioplastics are eco-friendly alternatives to traditional plastics, designed to decompose into harmless components through natural biological processes. Two common types are Polylactic Acid (PLA), derived from renewable resources like corn starch, and Polyhydroxyalkanoates (PHA), produced by microorganisms. PLA is used in agricultural applications such as mulch films and plant pots, while PHA is employed for soil conditioning and biodegradable films.

Similarly, starch-based bioplastics, derived from natural starches, are utilized for seedling trays and packaging. The adoption of biodegradable bioplastics is on the rise in developing economies in Asia Pacific and the Middle East and Africa, due to increasing environmental concerns and regulations. These sustainable agricultural practices not only reduce greenhouse gas emissions and pollution but also improve energy efficiency. For instance, biodegradable mulch films enhance soil moisture retention, reduce the need for irrigation, and improve crop yield. Therefore, the use of biodegradable bioplastics in agribusiness is a significant step towards sustainable farming practices and eco-friendly business operations.

Get a glance at the market report of share of various segments Request Free Sample

The biodegradable segment was valued at USD 468.10 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

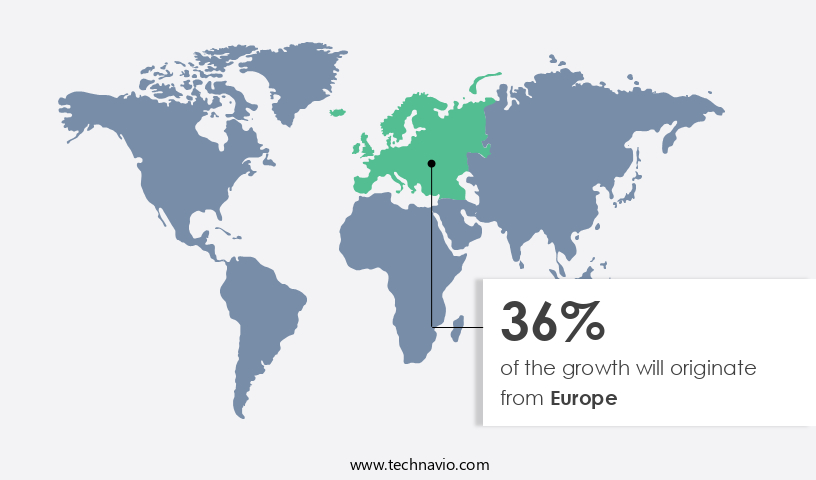

- Europe is estimated to contribute 36% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In Europe, the bioplastics market for agribusiness holds substantial importance due to the region's commitment to sustainability and environmental stewardship. Major European countries, including Germany, France, Italy, and the UK, significantly contributed to the European the market in 2023. The primary reason for the adoption of bioplastics in European agribusiness is the heightened awareness of the environmental consequences of conventional plastics.

Additionally, the European Union (EU) has taken a leading role in implementing stringent regulations and guidelines to minimize plastic waste and encourage the utilization of eco-friendly alternatives. As a result, there is a rising demand for bioplastics within the agribusiness sector, as businesses strive to comply with these regulations and cater to the evolving expectations of eco-conscious consumers. Bioplastics, such as starch-based bioplastics and polylactic acid, are increasingly being used for planting containers, greenhouse materials, and controlled-release fertilizers in Europe's agribusiness sector.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Bioplastics For Agribusiness Market?

Increasing focus on environmental sustainability is the key driver of the market.

- Bioplastics have emerged as a promising solution for the agribusiness sector, offering sustainable alternatives to traditional petroleum-based plastics. These biodegradable biomaterials are derived from renewable resources such as bio-based polymers, including Aliphatic Polyesters, Cellulose-Based Bioplastics, Organic Polyethylene, Polylactic acid, Polyhydroxyalkanoates, Protein-based bioplastics, and Starch-based bioplastics.

- Moreover, agricultural applications of bioplastics include biodegradable mulch films for improved crop yield, farming practices, and waste management. Biodegradable bioplastics, compostable bioplastics, and degradable bioplastics are gaining popularity due to their ability to reduce greenhouse gas emissions and address environmental issues. Thus, such factors are driving the growth of the market during the forecast period.

What are the market trends shaping the Bioplastics For Agribusiness Market?

The increasing focus of vendors on the development of innovative bioplastics is the upcoming trend in the market.

- Bioplastics have gained significant attention in the agribusiness sector due to their biodegradable and bio-based properties. These eco-friendly alternatives to traditional petroleum-based plastics offer numerous agricultural applications, including compostability and waste management. Bioplastics, such as aliphatic polyesters, cellulose-based bioplastics, organically derived polyethylene, and starch-based bioplastics, are increasingly used in farming practices for greenhouse materials, package films, planting containers, and controlled-release fertilizers.

- Moreover, the adoption of bioplastics promotes sustainable agricultural practices, and energy efficiency, and reduces toxicity and greenhouse gas emissions. Environmental regulations, such as the Single-Use Plastics Directive and green procurement incentives, are driving the market growth. Thus, such trends will shape the growth of the market during the forecast period.

What challenges does Bioplastics For Agribusiness Market face during the growth?

The cost-effectiveness of conventional plastic over bioplastics is a key challenge affecting the market growth.

- Bioplastics have gained significant attention in the agribusiness sector due to their biodegradable and bio-based properties. These eco-friendly alternatives to traditional petroleum-based plastics offer numerous agricultural applications, including compostability and waste management.

- Moreover, bioplastics are made from various biodegradable polymers, such as Aliphatic Polyesters, Cellulose-Based Bioplastics, Organic Polyethylene, Starch-based bioplastics, Polylactic acid, Polyhydroxyalkanoates, and Protein-based bioplastics. These biomaterials can be used for creating biodegradable mulch films, planting containers, greenhouse materials, controlled-release fertilizers, and various components in irrigation systems. Hence, the above factors will impede the growth of the market during the forecast period.

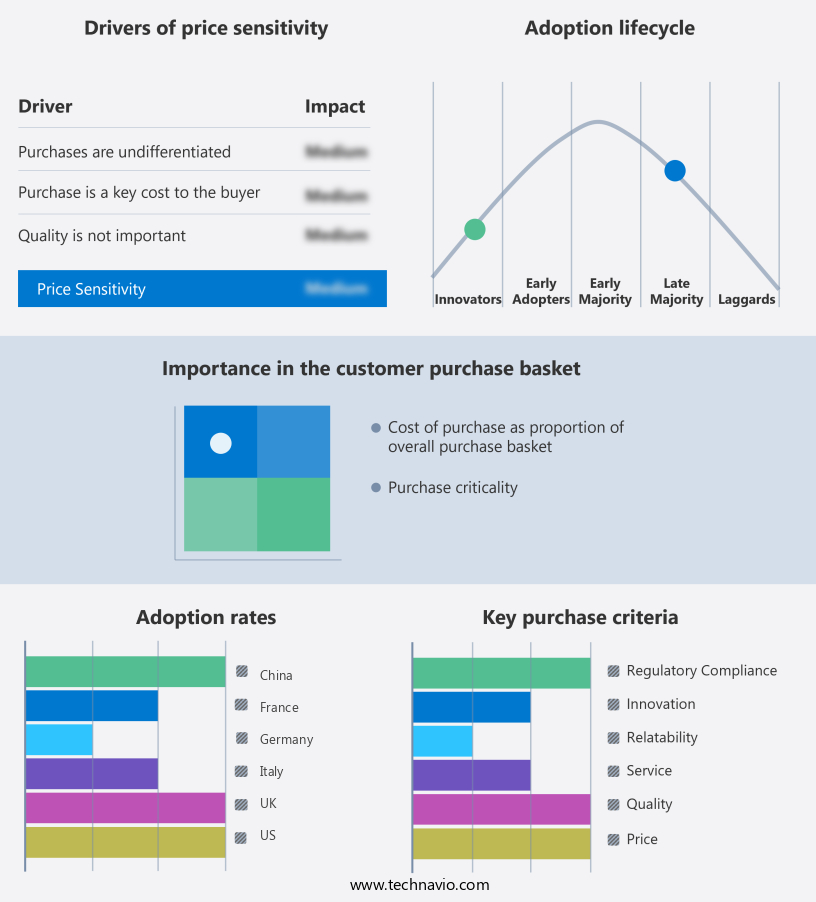

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ADBioplastics

- Arkema SA

- Avantium

- BASF SE

- Biome Bioplastics Ltd.

- Braskem

- Eastman Chemical Co.

- Fkur Kunststoff GmbH

- Futamura Group

- Futerro SA

- good natured Products Inc.

- Green Dot Bioplastics Inc.

- KURARAY Co. Ltd.

- Mitsubishi Chemical Group Corp.

- Novamont S.p.A.

- Polymateria Ltd

- PTT Global Chemical Public Co. Ltd.

- Secos Group Ltd.

- Tipa Ltd.

- TotalEnergies SE

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Bioplastics have emerged as a promising solution for the agribusiness market, offering sustainable alternatives to traditional petroleum-based plastics. These biodegradable polymers, derived from renewable resources, are gaining traction due to their compatibility with agricultural applications. Bioplastics are compostable and degradable, making them ideal for use in waste management systems and reducing the environmental impact of single-use plastics. Bioplastics offer several advantages for agribusiness, including improved crop yield, energy efficiency, and sustainable farming practices. They are used in various applications such as biodegradable mulch films, greenhouse materials, and planting containers. Bioplastics made from aliphatic polyesters, cellulose-based bioplastics, starch-based bioplastics, polylactic acid, polyhydroxyalkanoates, protein-based bioplastics, and biodegradable bioplastics are commonly used in the agribusiness sector.

Additionally, the use of bioplastics in agriculture also addresses environmental concerns such as toxicity and greenhouse gas emissions. Bioplastics have a lower carbon footprint compared to traditional plastics and contribute to sustainable agricultural practices. Governments and organizations offer grants and funding to encourage the adoption of bioplastics in the agribusiness sector, and there are regulatory incentives such as the Single-Use Plastics Directive and green procurement incentives. Bioplastics are used in various applications in the agribusiness sector, including greenhouses, irrigation systems, biomaterials, and silage storage. Biodegradable bioplastics and compostable bioplastics are preferred for their ability to break down naturally and reduce waste. Polybutylene succinate, a type of biodegradable bioplastic, is commonly used in irrigation systems and mulch. Bioplastics offer a sustainable solution for the agribusiness market, addressing environmental concerns while improving efficiency and productivity.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

201 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 18.63% |

|

Market growth 2024-2028 |

USD 1.37 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

17.46 |

|

Key countries |

US, China, Germany, France, UK, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across Europe, APAC, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -