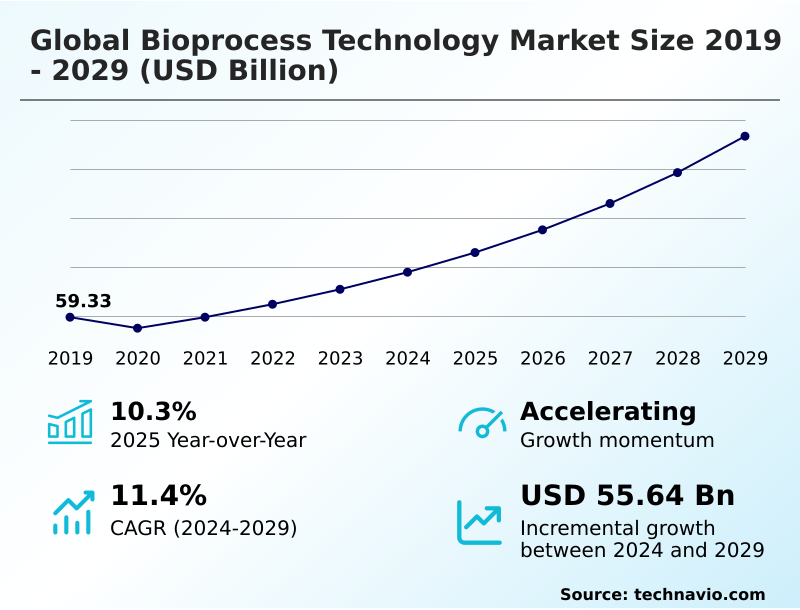

Bioprocess Technology Market Size 2025-2029

The bioprocess technology market size is valued to increase by USD 55.64 billion, at a CAGR of 11.4% from 2024 to 2029. Increase in infectious diseases will drive the bioprocess technology market.

Major Market Trends & Insights

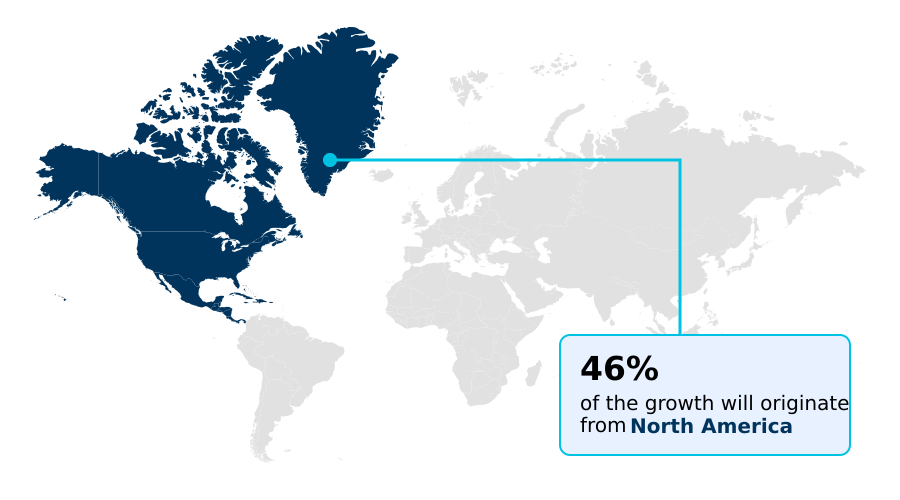

- North America dominated the market and accounted for a 46.4% growth during the forecast period.

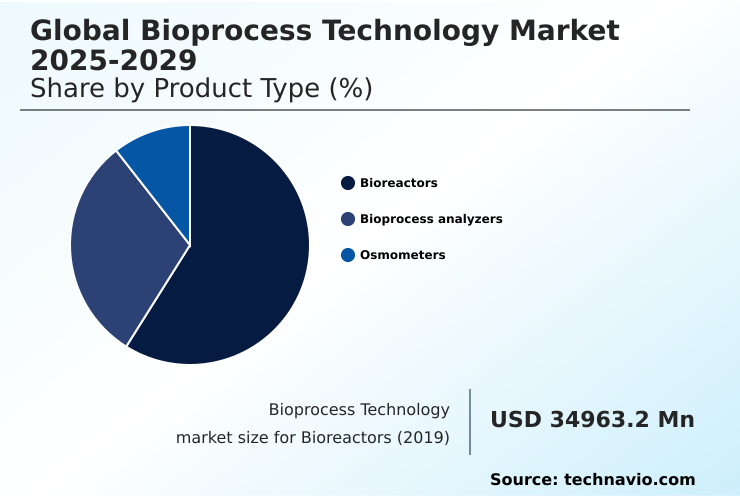

- By Product Type - Bioreactors segment was valued at USD 40.68 billion in 2023

- By Application - Cell and gene therapy segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 74.04 billion

- Market Future Opportunities: USD 55.64 billion

- CAGR from 2024 to 2029 : 11.4%

Market Summary

- The bioprocess technology market is foundational to modern medicine, enabling the manufacture of complex biologics from living cells. This sector is characterized by a significant shift from traditional pharmaceuticals to advanced therapies, including monoclonal antibodies and cell and gene therapies, which demand highly specialized production environments.

- A core industry focus involves leveraging single-use systems and automation to enhance efficiency and mitigate contamination risks. For instance, a biopharmaceutical firm implementing process analytical technology (PAT) can monitor critical quality attributes in real-time, reducing batch deviations and ensuring consistent product quality, which is crucial for regulatory compliance.

- This drive for innovation in upstream and downstream processing is balanced by challenges such as ensuring the scalability of manufacturing processes, managing complex global supply chains for critical raw materials, and navigating the rigorous validation requirements for new therapeutic modalities. The continued evolution of bioprocessing methods is essential to meet the growing global demand for life-saving treatments.

What will be the Size of the Bioprocess Technology Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Bioprocess Technology Market Segmented?

The bioprocess technology industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

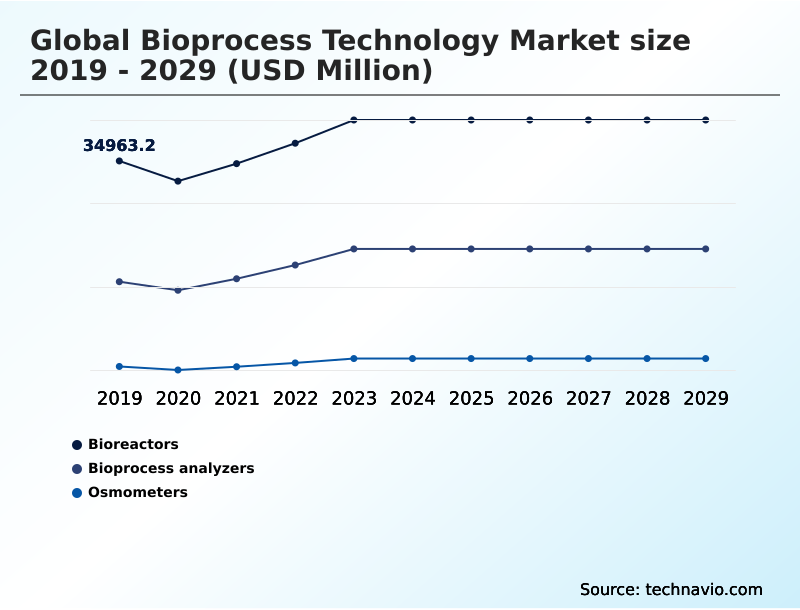

- Product type

- Bioreactors

- Bioprocess analyzers

- Osmometers

- Application

- Cell and gene therapy

- Monoclonal antibodies

- Recombinant proteins

- End-user

- Biopharmaceutical companies

- Contract manufacturing organizations

- Academic research institutes

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Product Type Insights

The bioreactors segment is estimated to witness significant growth during the forecast period.

The bioreactors segment is central to biopharmaceutical production, providing the controlled environment for mammalian cell culture and other processes. Market momentum is driven by the growing pipeline of complex biologics, including monoclonal antibodies and cell and gene therapy products.

A significant driver is the widespread single-use technology adoption, with disposable bioreactors offering greater agility for flexible manufacturing facilities. These systems eliminate extensive cleaning and validation, reducing facility changeover times by over 80%.

This efficiency is critical for accelerating tech transfer and enabling both fed-batch culture and emerging continuous biomanufacturing strategies.

As the industry moves toward process intensification, demand for innovative reactor designs that support aseptic processing and provide end-to-end solutions continues to increase.

The Bioreactors segment was valued at USD 40.68 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 46.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Bioprocess Technology Market Demand is Rising in North America Get Free Sample

North America leads the market, contributing over 46% of incremental growth, driven by its mature cGMP biomanufacturing ecosystem. High adoption of bioprocess analyzers, osmometers, and automated cell counting for controlling suspension culture processes underpins its dominance.

Europe follows, with hubs specializing in biologics. The Asia region exhibits the most rapid expansion, with investment in modular bioprocessing facilities increasing by over 20% annually.

This growth is fueled by building local capabilities in media formulation, aseptic sampling, and establishing working cell bank infrastructure.

Advanced techniques like closed system processing and aseptic fluid transfer, validated through bioprocess simulation, are becoming standard to ensure quality and regulatory alignment globally.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Achieving operational excellence in the global bioprocess technology market 2025-2029 hinges on mastering highly specific and interconnected manufacturing disciplines. The successful continuous manufacturing for recombinant proteins requires not just advanced bioreactors but also a robust strategy for managing raw material variability bioprocessing.

- As companies adopt high-throughput process development strategies, the tech transfer for biologic drug substance becomes a critical checkpoint where scale-down models for process validation are essential. A key focus is on the downstream purification of monoclonal antibodies, where optimizing tangential flow filtration system design and implementing effective viral clearance validation for biologics are paramount.

- The challenges in viral vector scale-up for gene therapies necessitate unique automation solutions for aseptic processing and improved cryopreservation of cell therapy products. Organizations are increasingly turning to bioprocess data analytics and modeling to inform decisions, from optimizing cell culture media formulation to designing a perfusion bioreactor for high-density culture.

- Integrating a single use bioreactor validation process into a quality management system that also addresses regulatory compliance for advanced therapies is now standard practice. This integrated approach, which offers end-to-end solutions for gene therapy, can improve supply chain robustness by over 50% compared to fragmented operational models.

What are the key market drivers leading to the rise in the adoption of Bioprocess Technology Industry?

- The rising prevalence of infectious diseases worldwide is a key market driver, fueling demand for rapid development and large-scale production of vaccines and cell-based therapies.

- Demand for sophisticated bioprocess technologies is primarily driven by the expanding pipeline of advanced therapy medicinal products and legacy biologics. The complex requirements for viral vector manufacturing and the production of recombinant proteins necessitate advanced solutions for drug substance manufacturing.

- The need for rapid scalability assessment and robust process validation is critical, particularly for allogeneic cell therapy scale-up, where manufacturing a single lot can treat numerous patients.

- Efficient cell banking protocols, including the establishment of a master cell bank, can shorten development timelines by 15%.

- Furthermore, innovations supporting both adherent cell culture and autologous cell therapy workflow are vital for expediting the path to a biologics license application, addressing urgent clinical needs and driving market expansion.

What are the market trends shaping the Bioprocess Technology Industry?

- An upcoming market trend is the globalization of clinical trials, driven by lower costs and greater patient access in developing nations. This expansion increases the demand for bioprocess technologies to support accelerated drug development.

- A primary trend is the integration of digitalization through bioprocess automation and advanced analytics. PAT implementation enables in-line monitoring of critical process parameters, which improves batch-to-batch consistency by up to 25%. This quality by design approach, supported by sophisticated bioprocess modeling, is transforming both microbial fermentation and suspension culture workflows.

- The adoption of perfusion bioreactors facilitates integrated bioprocessing and continuous operations, which can increase volumetric productivity by more than threefold compared to traditional methods. These advancements in process analytical technology and bioprocess control strategy are essential for optimizing cell line development and accelerating the timeline for novel modalities like mRNA vaccine production, ensuring more robust and efficient manufacturing.

What challenges does the Bioprocess Technology Industry face during its growth?

- A significant challenge affecting industry growth is the scarcity of trained laboratory professionals qualified to operate advanced bioprocess equipment and interpret complex experimental results.

- Key challenges center on manufacturing complexity and supply chain resilience. Raw material variability, especially in critical components like chromatography resins, can impact process performance, leading to batch failure rates that can exceed 5% in unoptimized workflows. Downstream purification remains a significant bottleneck, with multi-step processes for harvest and recovery and endotoxin removal adding considerable time and cost.

- The shift to single-use systems introduces concerns around leachables and extractables, requiring rigorous testing. Furthermore, effective viral clearance studies and robust cryopreservation techniques are non-negotiable for product safety and stability. Implementing advanced bioreactor sensor technology helps mitigate some risks, but the high cost of technologies like disposable chromatography and tangential flow filtration systems remains a barrier for many organizations.

Exclusive Technavio Analysis on Customer Landscape

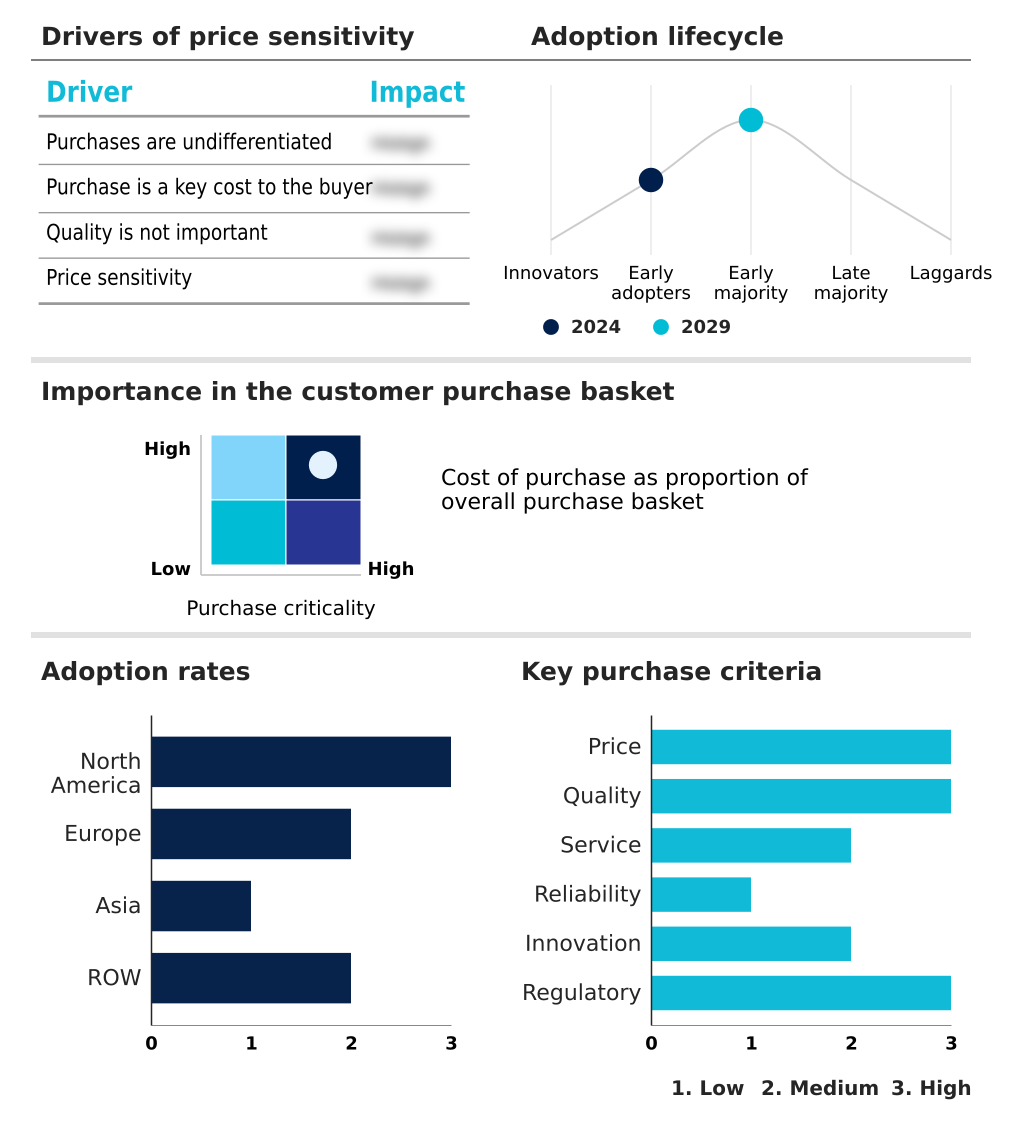

The bioprocess technology market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the bioprocess technology market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Bioprocess Technology Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, bioprocess technology market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Boehringer Ingelheim GmbH - Provides integrated bioprocess solutions, including advanced cell culture media and microbial host systems, to support complex biopharmaceutical development and manufacturing.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Boehringer Ingelheim GmbH

- Catalent Inc.

- Charles River Laboratories

- Corning Inc.

- Danaher Corp.

- Emerson Electric Co.

- Eppendorf SE

- Fujifilm Diosynth Biotechnologies USA Inc.

- General Electric Co.

- ILC Dover LP

- Koninklijke Philips NV

- Lonza Group Ltd.

- Merck KGaA

- Nova Biomedical Corp.

- Repligen Corp.

- Sartorius AG

- STADA Arzneimittel AG

- Thermo Fisher Scientific Inc.

- Univercells SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Bioprocess technology market

- In September 2024, Danaher Corp. announced the acquisition of a leading process analytical technology (PAT) firm to strengthen its real-time monitoring capabilities for continuous biomanufacturing.

- In November 2024, Thermo Fisher Scientific Inc. launched its next-generation single-use bioreactor platform, designed to improve scalability and process control for cell and gene therapy manufacturing.

- In February 2025, Sartorius AG entered a strategic partnership with a leading AI software company to integrate predictive analytics into its downstream processing workflows, aiming to optimize purification yields.

- In April 2025, Lonza Group Ltd. received FDA approval for its new large-scale viral vector manufacturing facility, significantly expanding its capacity to support late-stage gene therapy clinical trials.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Bioprocess Technology Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 294 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11.4% |

| Market growth 2025-2029 | USD 55635.4 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 10.3% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Thailand, Indonesia, Brazil, Saudi Arabia, UAE, Turkey, Argentina, Colombia, South Africa and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The bioprocess technology market is defined by the complex integration of upstream processing and downstream purification to enable biopharmaceutical production. Central to this is the choice between mammalian cell culture and microbial fermentation, with techniques like fed-batch culture and perfusion bioreactors optimizing output. Core equipment, including advanced bioreactors, bioprocess analyzers, and osmometers, are pivotal for control.

- The industry's shift toward single-use bioreactors reflects a boardroom-level focus on reducing capital expenditure and increasing operational flexibility. This move is supported by bioprocess automation and process analytical technology, which, when applied under a quality by design framework, can reduce process deviations by 25%. Key activities such as cell line development, cell banking, and using defined cryopreservation techniques are fundamental.

- For biologics like monoclonal antibodies, recombinant proteins, and products from viral vector manufacturing, purification requires high-purity chromatography resins, tangential flow filtration, and affinity chromatography. Ensuring safety through sterile filtration, endotoxin removal, and rigorous aseptic processing via aseptic sampling is non-negotiable.

- Ultimately, successful cGMP biomanufacturing depends on robust process validation and a clear scalability assessment to transition from development to commercial-scale harvest and recovery, especially for complex cell and gene therapy applications.

What are the Key Data Covered in this Bioprocess Technology Market Research and Growth Report?

-

What is the expected growth of the Bioprocess Technology Market between 2025 and 2029?

-

USD 55.64 billion, at a CAGR of 11.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product Type (Bioreactors, Bioprocess analyzers, and Osmometers), Application (Cell and gene therapy, Monoclonal antibodies, and Recombinant proteins), End-user (Biopharmaceutical companies, Contract manufacturing organizations, Academic research institutes, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increase in infectious diseases, Lack of trained laboratory professionals

-

-

Who are the major players in the Bioprocess Technology Market?

-

Boehringer Ingelheim GmbH, Catalent Inc., Charles River Laboratories, Corning Inc., Danaher Corp., Emerson Electric Co., Eppendorf SE, Fujifilm Diosynth Biotechnologies USA Inc., General Electric Co., ILC Dover LP, Koninklijke Philips NV, Lonza Group Ltd., Merck KGaA, Nova Biomedical Corp., Repligen Corp., Sartorius AG, STADA Arzneimittel AG, Thermo Fisher Scientific Inc. and Univercells SA

-

Market Research Insights

- The market's momentum is driven by a strategic shift toward technologies that enhance manufacturing agility and speed. The adoption of single-use systems has been pivotal, reducing contamination risks by over 90% compared to traditional stainless-steel infrastructures. This transition to disposable components facilitates the implementation of flexible manufacturing and continuous bioprocessing, which can shorten process development timelines by up to 40%.

- Concurrently, process intensification is a key dynamic, enabling higher product titers and greater throughput within smaller facility footprints. These advancements are critical for meeting the production demands of both commercial-scale biologics and personalized cell therapies, where efficiency and control are paramount for clinical success.

We can help! Our analysts can customize this bioprocess technology market research report to meet your requirements.

RIA -

RIA -