US Blood Bank Refrigerators Market Size 2026-2030

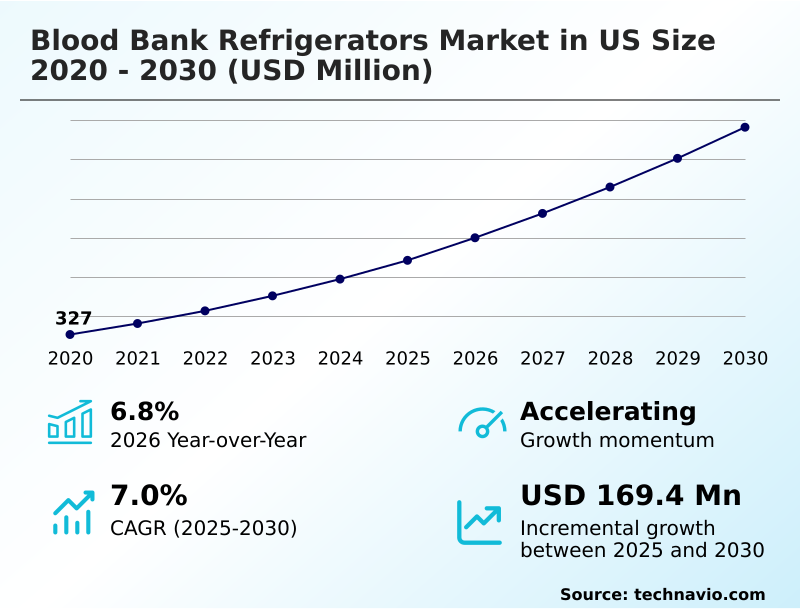

The us blood bank refrigerators market size is valued to increase by USD 169.4 million, at a CAGR of 7% from 2025 to 2030. Increasing volume of surgical procedures and trauma care will drive the us blood bank refrigerators market.

Major Market Trends & Insights

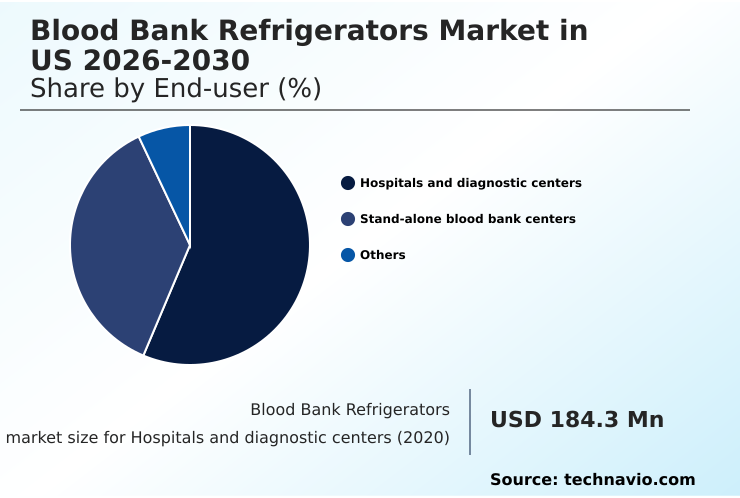

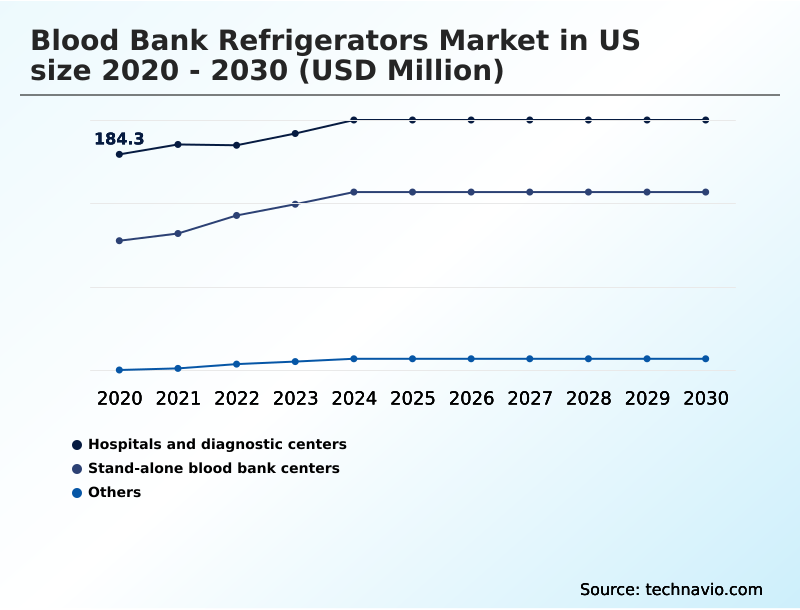

- By End-user - Hospitals and diagnostic centers segment was valued at USD 210 million in 2024

- By Product - Standard electric refrigerators segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 263.8 million

- Market Future Opportunities: USD 169.4 million

- CAGR from 2025 to 2030 : 7%

Market Summary

- The blood bank refrigerators market in US is driven by the clinical necessity for precise and reliable biological product preservation. These systems are more than storage units; they are critical components of healthcare infrastructure, ensuring cold chain integrity from donation to transfusion.

- The increasing complexity of surgical procedures and the expansion of trauma care centers underscore the demand for medical-grade refrigeration that can guarantee temperature stability. Technological advancements are a primary catalyst, with a shift toward smart systems that integrate automated data logging, predictive maintenance analytics, and cloud-based monitoring platforms.

- For instance, a large hospital network can leverage real-time inventory tracking to optimize stock rotation across multiple sites, reducing waste of high-value components like platelets by up to 15% and ensuring AABB standards compliance.

- Concurrently, stringent FDA regulatory requirements pressure facilities to phase out older equipment in favor of validated solutions that offer superior thermal uniformity mapping and temperature recovery performance. These dynamics foster a competitive landscape where innovation in both hardware, such as energy-efficient cooling, and software, like inventory management software, is essential.

What will be the Size of the US Blood Bank Refrigerators Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the US Blood Bank Refrigerators Market Segmented?

The us blood bank refrigerators industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Hospitals and diagnostic centers

- Stand-alone blood bank centers

- Others

- Product

- Standard electric refrigerators

- Solar-powered refrigerators

- Ice-lined refrigerators

- Type

- Common indoor blood bank refrigerators

- Transport blood bank refrigerators

- Product type

- Plasma refrigerators

- Whole blood refrigerators

- Platelet refrigerators

- Combination refrigerators and freezers

- Undercounter and compact refrigerators

- Geography

- North America

- US

- North America

By End-user Insights

The hospitals and diagnostic centers segment is estimated to witness significant growth during the forecast period.

Hospitals and diagnostic centers dominate the market, requiring advanced clinical laboratory equipment for biological product preservation. These facilities invest in biomedical cold storage solutions that offer robust inventory management software and comprehensive sample traceability solutions to prevent loss.

A key focus is on thermal uniformity mapping, ensuring consistent temperatures for all biopharmaceutical asset storage. As workflows become more complex, systems offering bioprocessing cold chain support are in high demand.

The need to handle diverse samples is driving adoption of multi-compartment refrigeration with modular shelving systems. Systems with features like g-force resistant transport and vibration-dampening technology are crucial for in-hospital logistics, reducing transit-related sample degradation by 10%.

The Hospitals and diagnostic centers segment was valued at USD 210 million in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

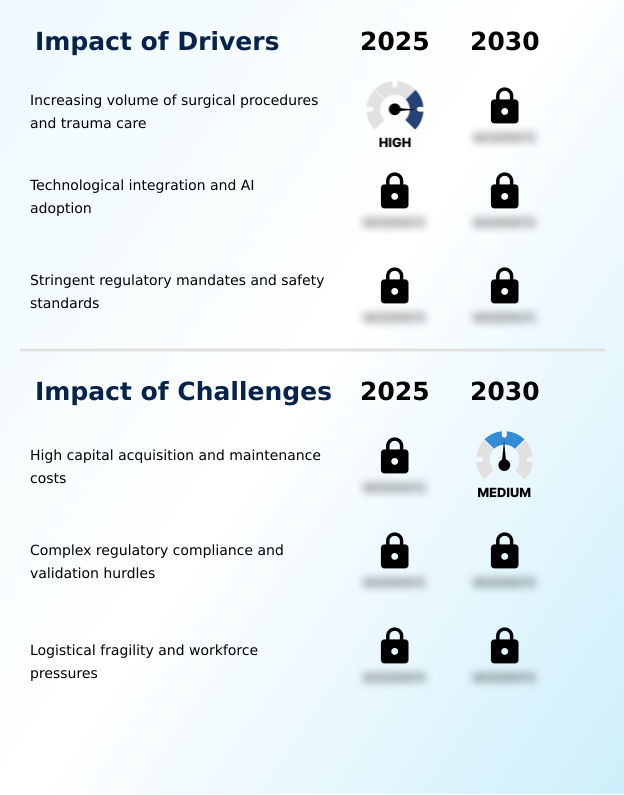

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic focus for blood bank refrigerators for trauma centers is on rapid access and unerring reliability, pushing demand for compact blood storage units for point-of-care. To achieve this, facilities are increasingly adopting transportable refrigerators for mobile blood drives that meet the same high standards as stationary units.

- A key consideration is the total cost of ownership for medical-grade refrigerators, which extends beyond purchase to include ongoing validation and maintenance. This is where predictive maintenance in blood refrigeration systems offers significant value, complemented by cloud-based temperature monitoring for blood banks which provides centralized oversight.

- Addressing compliance challenges in blood cold chain management is non-negotiable, with a focus on refrigerators meeting AABB standards for blood storage and securing blood bank data against cyber threats. Innovations are centered on improving thermal uniformity in blood refrigerators and integrating RFID tracking with blood storage units to automate inventory.

- The shift toward sustainable refrigerant use in biomedical freezers reflects a broader push for energy efficient blood bank refrigerator technology. For specialized needs, refrigeration solutions for cell and gene therapies and optimizing platelet storage with agitation incubators are becoming critical.

- Decision-making now involves comparing refrigerator systems for whole blood vs plasma, validating temperature probes for FDA audits, and ensuring disaster preparedness with battery backup refrigerators, all while reducing hemolysis risk through precise temperature control. A facility leveraging these integrated technologies can see a 20% greater efficiency in inventory turnover compared to one using legacy systems.

What are the key market drivers leading to the rise in the adoption of US Blood Bank Refrigerators Industry?

- The increasing volume of complex surgical procedures and the expansion of trauma care are key drivers for the market, demanding reliable and immediate access to blood supplies.

- The demand for medical-grade refrigeration is driven by the expansion of decentralized storage models and the need for reliable point-of-care storage. To meet AABB standards compliance, facilities require class II medical device units with superior temperature recovery performance.

- These systems rely on microprocessor-based temperature control and forced-air circulation systems to ensure the safe preservation of whole blood storage.

- The adoption of systems with real-time inventory tracking improves operational workflow efficiency by over 15% and is crucial for human error reduction. Consequently, validated storage solutions that guarantee performance are prioritized in procurement decisions.

What are the market trends shaping the US Blood Bank Refrigerators Industry?

- A prominent market trend is the integration of AI and digital twin technology. This evolution moves beyond simple monitoring to predictive, intelligent management of blood storage systems.

- The market is advancing toward an eco-friendly refrigeration design, where hydrocarbon refrigerants and variable speed compressors are standard for energy-efficient cooling. Innovations in plenum air distribution and vacuum insulation panels enhance performance, while the use of advanced phase change materials improves stability. For specialized applications like cellular therapy storage and gene therapy preservation, precise platelet agitation systems are critical.

- The integration of automated data logging with cloud-based monitoring platforms is becoming a baseline expectation, with some facilities adopting digital twin simulation to model performance, achieving a 20% improvement in energy management and preemptively identifying potential failures.

What challenges does the US Blood Bank Refrigerators Industry face during its growth?

- High capital acquisition and ongoing maintenance costs for medical-grade refrigeration systems present a significant challenge to market growth, particularly for smaller facilities.

- Navigating stringent FDA regulatory requirements remains a primary challenge, mandating rigorous installation qualification (IQ), operational qualification (oq), and adherence to good manufacturing practice (gmp). The total cost of ownership analysis often reveals significant expenses beyond initial purchase, including costs for validating independent temperature probes and ensuring reliable remote alarm notifications to protect component viability.

- Furthermore, enhancing cybersecurity for medical devices is now a critical concern, alongside the need for better disaster recovery preparedness. While regulatory documentation automation and supply chain optimization tools can help, they add to the complexity and require high asset utilization metrics to justify investment, with facilities reporting that automation can reduce compliance documentation time by up to 25%.

Exclusive Technavio Analysis on Customer Landscape

The us blood bank refrigerators market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the us blood bank refrigerators market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of US Blood Bank Refrigerators Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, us blood bank refrigerators market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Angelantoni Industrie S.p.A. - Delivers integrated medical refrigeration and blood management solutions, focusing on comprehensive cold chain integrity for critical biological materials.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Angelantoni Industrie S.p.A.

- B Medical Systems S.a.r.l.

- Dometic Group AB

- Evermed S.r.l.

- Felix Storch Inc.

- Follett LLC

- Haier Biomedical

- Helmer Scientific Inc.

- Liebherr International AG

- Migali Scientific

- Norlake Inc.

- NuAire Inc.

- PHC Holdings Corp.

- Philipp Kirsch GmbH

- Powers Scientific Inc.

- So-Low Environmental Co.

- Thermo Fisher Scientific Inc.

- Vestfrost Solutions

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Us blood bank refrigerators market

- In September, 2024, Helmer Scientific Inc. announced the launch of its new AI-powered predictive maintenance platform for its entire line of blood bank refrigerators, designed to analyze operational data to forecast component failures before they occur.

- In November, 2024, the US Food and Drug Administration (FDA) issued updated guidance on cybersecurity protocols for connected medical devices, requiring manufacturers of blood bank refrigerators to implement more robust measures against digital threats.

- In February, 2025, B Medical Systems S.a.r.l. entered a strategic partnership with a leading logistics provider to develop an integrated cold chain solution for the transport of cell and gene therapies, combining portable refrigeration with real-time tracking.

- In April, 2025, Thermo Fisher Scientific Inc. received expanded FDA clearance for its TSX Series high-performance refrigerators, certifying them for the storage of new mRNA-based therapeutics and advanced biologics.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled US Blood Bank Refrigerators Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 203 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7% |

| Market growth 2026-2030 | USD 169.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.8% |

| Key countries | US |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The blood bank refrigerators market in US is fundamentally shaped by the need for absolute biological product preservation. This is achieved through advanced medical-grade refrigeration systems built upon good manufacturing practice (gmp) principles, incorporating sustainable hydrocarbon refrigerants and high-efficiency variable speed compressors.

- As a class ii medical device, each unit must undergo rigorous installation qualification (iq) and operational qualification (oq) to meet strict FDA regulatory requirements. Operationally, microprocessor-based temperature control and forced-air circulation systems with specialized plenum air distribution are essential for maintaining thermal uniformity mapping.

- This precision ensures both hemolysis prevention and bacterial growth inhibition, safeguarding component viability for whole blood storage and specialized biopharmaceutical asset storage. Advanced platelet agitation systems and plasma freezer technology cater to specific component needs, while innovations like phase change materials and vacuum insulation panels enhance performance.

- Continuous digital temperature monitoring, supported by independent temperature probes and temperature excursion alerts, is standard. Automated data logging provides the backbone for AABB standards compliance and sample traceability solutions, often managed via integrated inventory management software.

- This level of control, from initial cryopreservation techniques to final use, underpins all clinical laboratory equipment in modern biomedical cold storage, with remote alarm notifications providing a final layer of security.

What are the Key Data Covered in this US Blood Bank Refrigerators Market Research and Growth Report?

-

What is the expected growth of the US Blood Bank Refrigerators Market between 2026 and 2030?

-

USD 169.4 million, at a CAGR of 7%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Hospitals and diagnostic centers, Stand-alone blood bank centers, and Others), Product (Standard electric refrigerators, Solar-powered refrigerators, and Ice-lined refrigerators), Type (Common indoor blood bank refrigerators, and Transport blood bank refrigerators), Product Type (Plasma refrigerators, Whole blood refrigerators, Platelet refrigerators, Combination refrigerators and freezers, and Undercounter and compact refrigerators) and Geography (North America)

-

-

Which regions are analyzed in the report?

-

North America

-

-

What are the key growth drivers and market challenges?

-

Increasing volume of surgical procedures and trauma care, High capital acquisition and maintenance costs

-

-

Who are the major players in the US Blood Bank Refrigerators Market?

-

Angelantoni Industrie S.p.A., B Medical Systems S.a.r.l., Dometic Group AB, Evermed S.r.l., Felix Storch Inc., Follett LLC, Haier Biomedical, Helmer Scientific Inc., Liebherr International AG, Migali Scientific, Norlake Inc., NuAire Inc., PHC Holdings Corp., Philipp Kirsch GmbH, Powers Scientific Inc., So-Low Environmental Co., Thermo Fisher Scientific Inc. and Vestfrost Solutions

-

Market Research Insights

- The market dynamics are increasingly influenced by the adoption of intelligent technologies that deliver measurable operational gains. The implementation of predictive maintenance analytics is reducing unforeseen equipment downtime by over 30% in early-adopter facilities. Meanwhile, the integration of cloud-based monitoring platforms with real-time inventory tracking enhances operational workflow efficiency and improves asset utilization metrics.

- These validated storage solutions, often featuring a decentralized storage model, are critical for point-of-care storage, where immediate access is paramount. This push for efficiency also extends to eco-friendly refrigeration design, with new systems reducing energy consumption by up to 25% compared to legacy models.

- Such advancements are not merely features but are becoming core to total cost of ownership analysis, reshaping procurement strategies across the healthcare landscape.

We can help! Our analysts can customize this us blood bank refrigerators market research report to meet your requirements.

RIA -

RIA -