Blood Screening Market Size 2024-2028

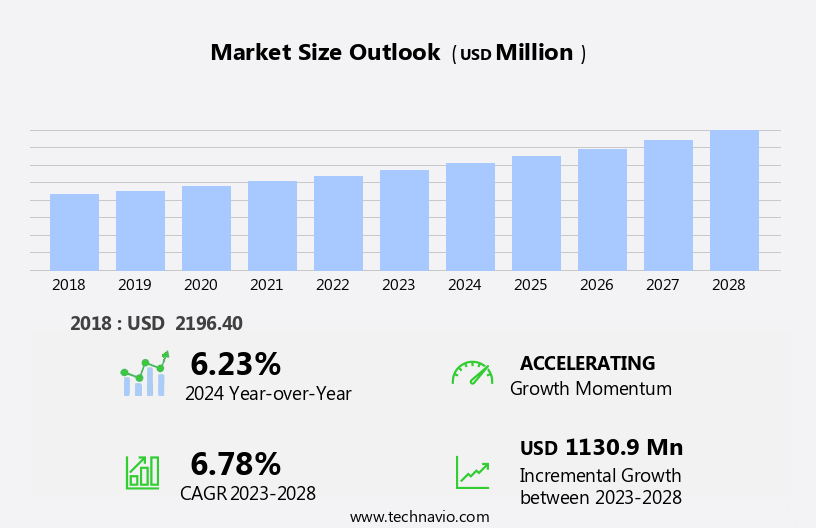

The blood screening market size is forecast to increase by USD 1.13 billion, at a CAGR of 6.78% between 2023 and 2028.

- The market is driven by the escalating demand for blood transfusions due to various medical conditions, infectious diseases, and surgeries. The automation of the blood screening process is another significant factor fueling market growth. However, the high cost associated with blood screening remains a notable challenge. The automation of blood screening processes is streamlining operations and enhancing accuracy, which is increasingly becoming a priority for healthcare providers. Despite this, the high cost of blood screening, including the cost of reagents and equipment, continues to pose a significant obstacle for market expansion. Companies seeking to capitalize on market opportunities must focus on cost reduction strategies and developing cost-effective solutions.

- Additionally, collaboration with healthcare providers and governments to subsidize the cost of blood screening for patients in need could be a potential growth strategy. Overall, the market presents significant opportunities for innovation and growth, with a focus on cost reduction and automation being key strategies for success.

What will be the Size of the Blood Screening Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in technology and the expanding scope of applications across various sectors. Automated sample handling and quality control metrics are essential components of modern blood screening processes, ensuring accuracy and efficiency. Blood cell counters, diagnostic algorithms, and infection detection systems play a pivotal role in identifying key indicators such as erythrocyte sedimentation rate, platelet function testing, and blood gas analyzers. Molecular diagnostics, blood typing reagents, and differential blood count are integral to the identification of genetic disorders, infectious diseases, and other health conditions. Coagulation testing, including partial thromboplastin time and prothrombin time, and immunoassay methods, are crucial for diagnosing and monitoring conditions related to lipid profiles, anemia, thrombosis, and glucose levels.

D-dimer testing, leukemia markers, and thrombosis biomarkers are essential for diagnosing and monitoring blood clotting disorders. Hematology analyzers, serum protein electrophoresis, and microfluidic devices facilitate the rapid and accurate analysis of blood samples. Blood viscosity measurement and point-of-care testing offer convenience and efficiency in various clinical settings. Blood culture systems and lab information systems streamline the overall blood screening process, ensuring seamless integration of data and results. Blood separation technology enables the isolation of specific components for further analysis, expanding the capabilities of blood screening applications. The ongoing unfolding of market activities and evolving patterns underscores the dynamic nature of the market.

How is this Blood Screening Industry segmented?

The blood screening industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Component

- Reagents and kits

- Instruments

- Software and services

- End-user

- Blood bank

- Hospitals

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

By Component Insights

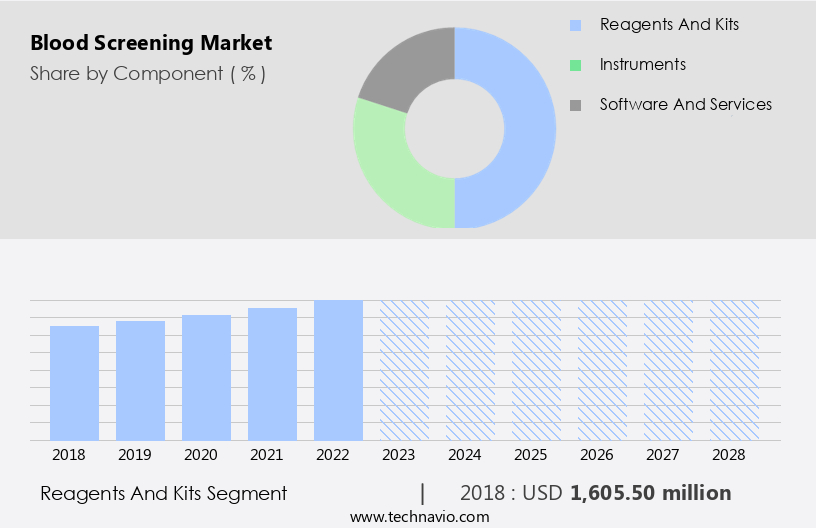

The reagents and kits segment is estimated to witness significant growth during the forecast period.

In the realm of blood screening, reagents and kits play a pivotal role in ensuring the safety and efficacy of donated blood. These essential laboratory components are utilized to detect infectious diseases and other health risks through various testing methods. Reagents function by reacting chemically with specific components in a blood sample, such as antigens or antibodies. Their selection is based on factors like specificity, sensitivity, and reliability in identifying particular pathogens. Automated sample handling systems streamline the testing process, enhancing efficiency and reducing human error. Quality control metrics are implemented to maintain consistency and accuracy in the results.

Lipid profiles, partial thromboplastin time, prothrombin time, and fibrinogen assays are integral to coagulation testing. Hemolysis detection, complete blood count, and blood cell counters provide valuable information about the blood's composition. Diagnostic algorithms, infection detection, erythrocyte sedimentation rate, platelet function testing, blood gas analyzers, molecular diagnostics, and blood typing reagents are some of the advanced technologies employed in blood screening. Differential blood count, d-dimer testing, leukemia markers, glucose monitoring, anemia indicators, thrombosis biomarkers, and coagulation testing are essential for comprehensive blood analysis. Immunoassay methods, blood culture systems, blood separation technology, lab information systems, hematology analyzers, serum protein electrophoresis, microfluidic devices, and blood viscosity measurement are other advanced techniques used to optimize blood screening processes.

Point-of-care testing and blood group typing further enhance the convenience and accuracy of blood screening. The market for these technologies is continually evolving, driven by advancements in technology and the increasing demand for safe and efficient blood screening solutions.

The Reagents and kits segment was valued at USD 1.61 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

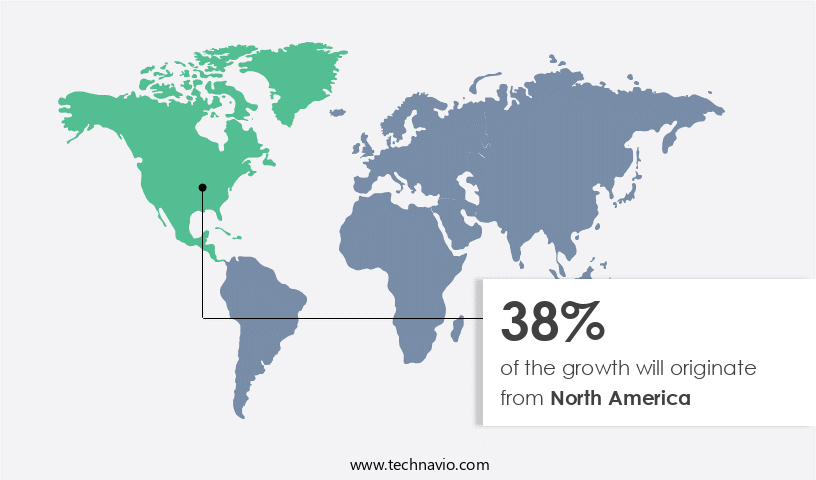

North America is estimated to contribute 38% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is witnessing significant growth due to the increasing importance of ensuring the safety of the blood supply and preventing the transmission of infectious diseases. In 2023, North America held the largest market share in this domain. Advanced technologies, such as automated sample handling, quality control metrics, lipid profiles, partial thromboplastin time, prothrombin time, fibrinogen assay, hemolysis detection, complete blood count, patient sample management, blood cell counters, diagnostic algorithms, infection detection, erythrocyte sedimentation rate, platelet function testing, blood gas analyzers, molecular diagnostics, blood typing reagents, differential blood count, d-dimer testing, leukemia markers, glucose monitoring, anemia indicators, thrombosis biomarkers, coagulation testing, immunoassay methods, blood culture systems, blood separation technology, lab information systems, hematology analyzers, serum protein electrophoresis, microfluidic devices, blood viscosity measurement, point-of-care testing, and blood group typing, are driving the market's evolution.

In North America, the market's growth is fueled by factors such as advancements in medical technology, increased awareness of blood safety, regulatory requirements, and healthcare needs.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Blood Screening Industry?

- The escalating demand for blood transfusions serves as the primary market driver.

- Blood screening is a vital process ensuring the safety of the blood supply by identifying potential infections or diseases in donated blood. With advancements in medical treatments, surgeries, organ transplants, and trauma care, the demand for safe and compatible blood products continues to rise. In emergencies, rapid and accurate blood screening becomes crucial to meet the urgent need for transfusions. Automated sample handling systems and advanced diagnostic techniques, such as lipid profiles, partial thromboplastin time, prothrombin time, fibrinogen assay, hemolysis detection, and complete blood count, contribute significantly to the efficiency and accuracy of blood screening.

- Quality control metrics ensure consistent results and maintain the integrity of the blood supply. Patient sample management is essential to maintain the traceability and accountability of blood samples throughout the screening process. The integration of technology, such as barcode scanning and electronic records, streamlines the process and reduces the risk of errors. The importance of comprehensive and efficient blood screening processes cannot be overstated, as the safety of the blood supply is paramount. Ensuring the accuracy and reliability of blood screening results is crucial in maintaining public health and trust in the blood transfusion system.

What are the market trends shaping the Blood Screening Industry?

- Blood screening processes are increasingly being automated to keep up with the latest market trends. This automation enhances efficiency and accuracy in the screening process.

- Blood screening, a critical aspect of healthcare diagnostics, has experienced significant advancements due to automation. Automated blood cell counters, for instance, streamline the process of analyzing blood components, such as erythrocytes, leukocytes, and platelets, ensuring accuracy and efficiency. Diagnostic algorithms, integrated into these systems, facilitate infection detection by analyzing various parameters. Moreover, advanced technologies like platelet function testing, blood gas analyzers, and molecular diagnostics have revolutionized the field. These technologies enable real-time analysis of blood samples, providing quick and reliable results. Blood typing reagents and differential blood count kits are essential components in blood screening, ensuring accurate identification and classification of blood types and analyzing the relative proportions of different types of blood cells.

- Automation also extends to data management, with electronic health records, laboratory information systems, and data analytics becoming essential tools. These digital solutions enhance efficiency, minimize manual record-keeping, and reduce data errors. Point-of-care automated systems perform rapid diagnostic tests for various blood screening markers, providing quick results and improving patient care. Overall, automation and digitalization are transforming blood screening, ensuring improved accuracy, efficiency, and patient outcomes.

What challenges does the Blood Screening Industry face during its growth?

- The elevated expenses linked to the blood screening process pose a significant challenge to the industry's growth trajectory.

- Blood screening is an essential component of healthcare, ensuring the safety of blood transfusions and aiding in the diagnosis and monitoring of various medical conditions. However, the high cost of implementing and maintaining advanced blood screening technologies poses a significant challenge. The expenses accumulate over time due to the cost of reagents, kits, and consumables, particularly for high-throughput processes. State-of-the-art screening technologies incorporate sophisticated equipment, instruments, and robotic systems, which incur substantial initial costs. Maintaining quality control standards necessitates additional resources for validation, monitoring, and adherence to regulatory guidelines, further increasing costs for companies. Key blood screening tests include d-dimer testing for thrombosis, leukemia markers for cancer detection, glucose monitoring for diabetes management, and anemia indicators for assessing iron deficiency.

- Coagulation testing is essential for diagnosing and managing bleeding disorders, while immunoassay methods facilitate the detection of various biomarkers. Blood culture systems ensure the safety of blood products by identifying potential contaminants, and blood separation technology facilitates the isolation of specific components for further analysis. Despite these benefits, the high cost of these technologies remains a significant barrier to their widespread adoption in healthcare systems and blood banks.

Exclusive Customer Landscape

The blood screening market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the blood screening market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, blood screening market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Apollo Hospitals Enterprise Ltd - The company specializes in blood screening tests, including the BCAL test, a lipid biomarker assessment.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Apollo Hospitals Enterprise Ltd

- Aster Clinical Lab LLP

- BCAL Diagnostics Ltd.

- Becton Dickinson and Co.

- Bio Rad Laboratories Inc.

- Dr Lal PathLabs Ltd.

- Eurofins Scientific SE

- F. Hoffmann La Roche Ltd.

- Grifols SA

- Harley Street Health Checks UK Ltd.

- Hemogenomics Pvt. Ltd.

- Laboratory Corp. of America Holdings

- Mankind Pharma Ltd.

- Metropolis Healthcare Ltd.

- QuidelOrtho Corp.

- Siemens Healthineers AG

- Syantra Inc.

- Thermo Fisher Scientific Inc.

- Vijaya Diagnostic Centre Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Blood Screening Market

- In January 2024, Roche Diagnostics, a leading diagnostics company, announced the launch of its new automated blood screening system, Cobas hb 511, which can test for 13 different parameters in a single sample, significantly increasing efficiency in diagnostic laboratories (Roche Diagnostics Press Release).

- In March 2024, Siemens Healthineers and Philips signed a strategic partnership to integrate their respective blood screening solutions, aiming to enhance interoperability and improve patient care (Siemens Healthineers Press Release).

- In April 2024, Grifols, a global healthcare company, completed the acquisition of Talecris Biotherapeutics, a leading plasma protein therapeutics company, expanding Grifols' presence in the plasma-derived medicines market and increasing its capacity to collect and process plasma for blood screening tests (Grifols Press Release).

- In May 2025, the US Food and Drug Administration (FDA) approved the use of point-of-care blood screening tests for detecting COVID-19 antibodies, enabling faster and more accessible diagnostic services (FDA Press Release).

Research Analyst Overview

- The market encompasses various technologies and methods for diagnosing and monitoring diseases, including PCR technology, electrochemical sensors, and chromatographic methods. Test result interpretation relies on reference intervals and clinical decision support systems, which utilize data analytics platforms to ensure patient data privacy. Sample preparation methods, such as ELISA techniques and immunofluorescence assays, are crucial for accurate test results. Troubleshooting guides and calibration procedures are essential for maintaining the performance of advanced technologies like next-generation sequencing, microarray technology, and mass spectrometry. Pre-analytical workflows and quality assurance protocols ensure regulatory compliance and maintain sensitivity and specificity. PCR technology and ELISA techniques have high negative predictive values, making them valuable for ruling out diseases.

- On the other hand, flow cytometry and immunofluorescence assays offer high positive predictive values for disease detection. Clinical decision support systems and lab automation systems streamline workflows and improve efficiency, while maintenance protocols and troubleshooting guides ensure the longevity of these systems. Disease risk assessment and calibration procedures are integral parts of the blood screening process, providing valuable insights for patient care. Assay standardization and regulatory compliance are essential for ensuring accurate and reliable test results, while optical biosensors and mass spectrometry offer high sensitivity and specificity for disease detection. Pre-analytical workflows and quality assurance protocols ensure the accuracy and reliability of test results, ultimately improving patient outcomes.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Blood Screening Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

162 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.78% |

|

Market growth 2024-2028 |

USD 1130.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.23 |

|

Key countries |

US, China, Germany, Canada, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Blood Screening Market Research and Growth Report?

- CAGR of the Blood Screening industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the blood screening market growth of industry companies

We can help! Our analysts can customize this blood screening market research report to meet your requirements.

RIA -

RIA -