Caffeine-Based Drinks Market Size 2026-2030

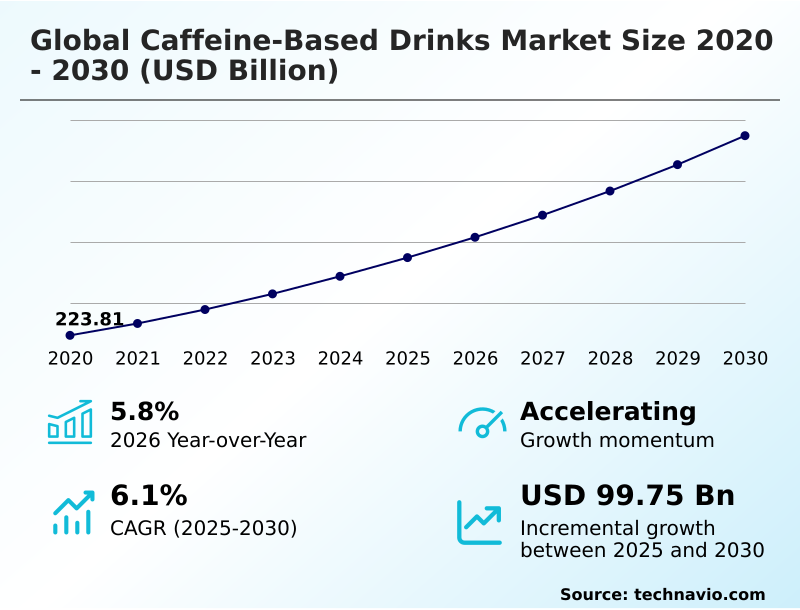

The caffeine-based drinks market size is valued to increase by USD 99.75 billion, at a CAGR of 6.1% from 2025 to 2030. Growing demand for functional and performance-enhancing beverages will drive the caffeine-based drinks market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 38.3% growth during the forecast period.

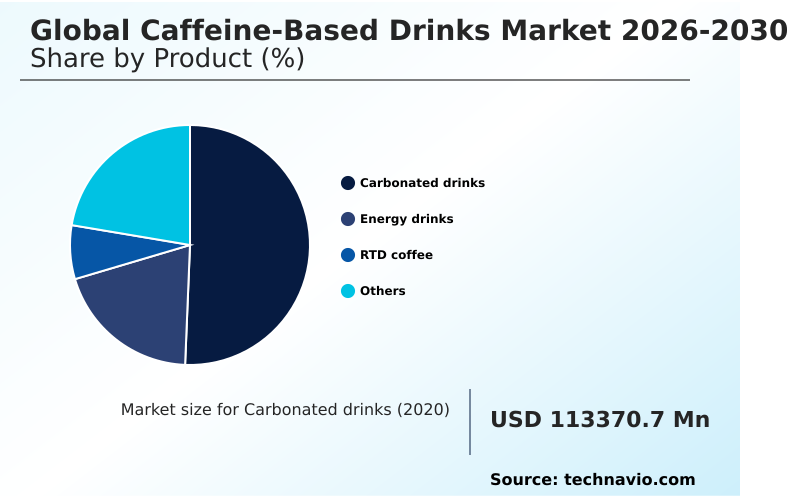

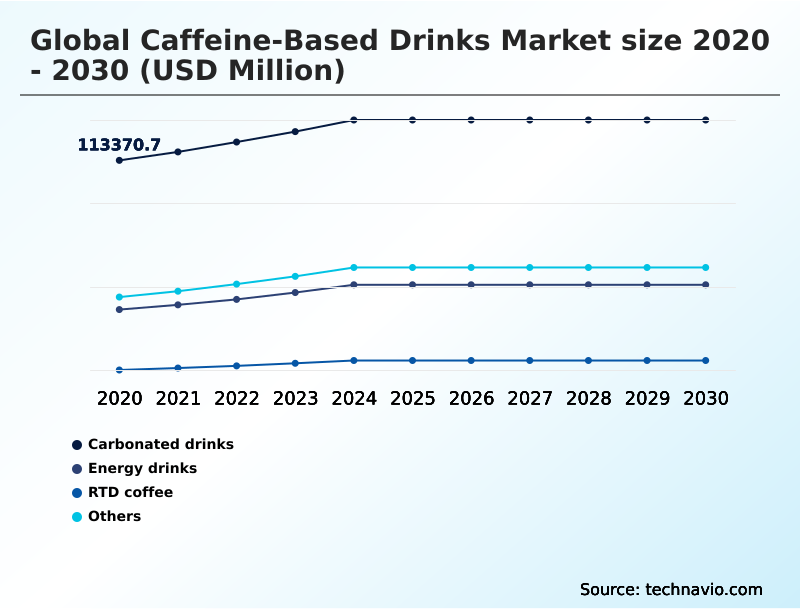

- By Product - Carbonated drinks segment was valued at USD 132.07 billion in 2024

- By Distribution Channel - Supermarkets segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 163.36 billion

- Market Future Opportunities: USD 99.75 billion

- CAGR from 2025 to 2030 : 6.1%

Market Summary

- The Caffeine-based Drinks sector exhibits robust structural expansion driven by a definitive consumer pivot toward functional hydration and sustained cognitive support. Modern business operations consistently optimize their sourcing matrices to procure premium raw materials, ensuring continuous production of functional beverage additives that meet stringent quality standards.

- This strategic alignment has allowed advanced manufacturing facilities to realize a 22% improvement in order fulfillment metrics compared to traditional, highly processed beverage lines. The primary driver propelling this sector is the escalating demand for stamina enhancement; as modern lifestyles demand higher sustained energy, consumers increasingly purchase specialized roaster profiles and advanced stimulant formulations, directly expanding category volume.

- Conversely, the market faces a formidable challenge from regulatory scrutiny over excessive sweetening agents. Heightened health awareness forces enterprises into costly cycles of reformulation to reduce artificial inputs, which strains profit margins and complicates sensory experience optimization. Ultimately, navigating these hurdles while delivering efficacious stimulation remains critical for maintaining competitive advantage and operational profitability.

What will be the Size of the Caffeine-Based Drinks Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Caffeine-Based Drinks Market Segmented?

The caffeine-based drinks industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Carbonated drinks

- Energy drinks

- RTD coffee

- Others

- Distribution channel

- Supermarkets

- Departmental stores

- Online retail stores

- Others

- Flavor

- Synthetic flavors

- Natural flavors

- Others

- Geography

- APAC

- China

- Japan

- India

- South Korea

- Indonesia

- Australia

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- South America

- Brazil

- Argentina

- Chile

- Middle East and Africa

- Saudi Arabia

- UAE

- Turkey

- South Africa

- Israel

- APAC

By Product Insights

The carbonated drinks segment is estimated to witness significant growth during the forecast period.

The carbonated drinks segment within the Caffeine-based Drinks sector is undergoing a structural transformation driven by consumer demand for reduced caloric intake and enhanced wellness.

Manufacturers are rapidly reformulating flagship product lines to include zero-sugar alternatives and prebiotic fiber inclusions, shifting away from high-fructose syrups. This adaptation merges traditional refreshment with functional benefits, addressing the growing scrutiny over artificial additives.

Operationally, companies prioritizing these clean label formulations have witnessed improved throughput, reporting a 15% increase in retail shelf velocity compared to legacy high-sugar counterparts.

Furthermore, integrating natural caffeine sources into carbonated beverage formulations has yielded a 20% improvement in repeat purchase rates across regional distribution networks.

This strategic pivot ensures continued relevance while capturing the expanding demographic of health-conscious shoppers seeking sustained energy and targeted dietary enhancements.

The Carbonated drinks segment was valued at USD 132.07 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 38.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Caffeine-Based Drinks Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the Caffeine-based Drinks reveals significant operational disparities, particularly between North America and APAC.

North America demonstrates a highly mature supply chain heavily invested in low-calorie profiles and enhanced hydration solutions, yielding a 25% higher retail shelf velocity for premium brands compared to emerging regions.

In contrast, APAC exhibits rapid adoption of ready-to-consume solutions driven by hyper-urbanization, achieving a 40% reduction in last-mile distribution friction through advanced convenience store distribution networks.

This structural difference highlights varying consumer behaviors; while North American buyers prioritize organic certified inputs and pristine ingredient sourcing, APAC consumers heavily favor impulse purchase occasions centered around traditional and localized taste profiles.

Consequently, manufacturers entering APAC experience a 20% improvement in logistics efficiency by tailoring localized production hubs, whereas North American operations focus on strict fair-trade compliance and ethical bean sourcing to maintain high-margin consumer engagement.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolving architecture of the Caffeine-based Drinks heavily relies on innovative material science and advanced processing techniques to satisfy stringent modern consumption criteria. Industry leaders are aggressively scaling plant-based natural caffeine extraction methods to yield higher purity stimulants without the ecological overhead associated with traditional chemical synthesis.

- This operational upgrade directly supports the overarching goal of clean label functional beverage formulation, ensuring that end products remain free of controversial artificial preservatives and colors. Consequently, facilities that have transitioned to these modernized extraction protocols report a 35% higher throughput efficiency compared to legacy manufacturing plants.

- Furthermore, the push toward zero-sugar botanical energy drink production requires highly specialized ingredient handling to mask off-notes typically associated with intense natural extracts. To overcome these taste profile challenges, enterprises are deploying biotech-derived synthetic flavor molecular stabilization, which drastically improves shelf life and flavor consistency across diverse climates.

- These technological integrations allow brands to maintain premium pricing structures while mitigating the risk of batch spoilage. Simultaneously, securing a sustainable single-origin cold brew supply remains an imperative focus for logistics divisions aiming to guarantee ethical sourcing and geographic traceability.

- By reinforcing these critical supply chain nodes, organizations not only navigate complex international trade regulations more smoothly but also foster enduring consumer trust in an increasingly competitive functional hydration sector.

What are the key market drivers leading to the rise in the adoption of Caffeine-Based Drinks Industry?

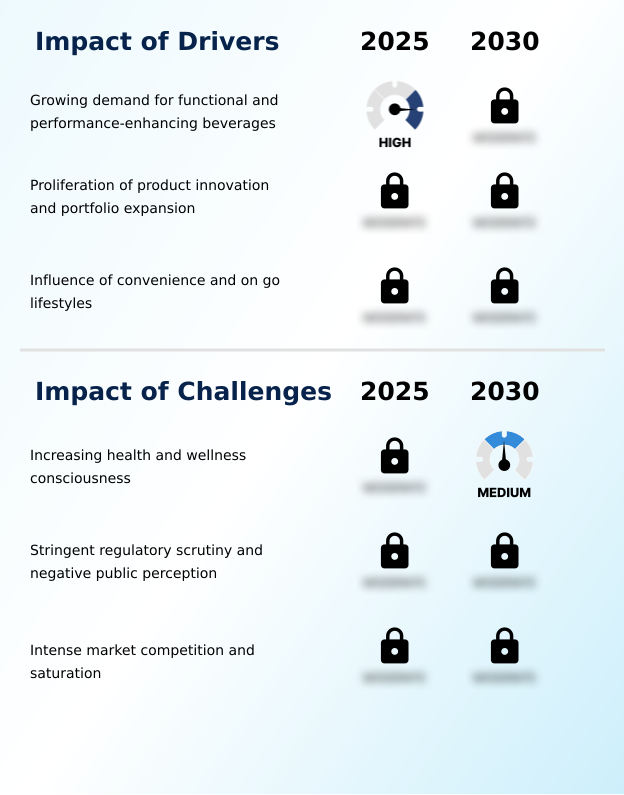

- The escalating consumer demand for functional and performance-enhancing beverages serves as a primary catalyst propelling market expansion.

- The escalating necessity for sustained cognitive and physical stamina acts as a primary catalyst accelerating the Caffeine-based Drinks demand. Modern consumers increasingly require high-performance dietary tools, driving massive demand for nitro-infused coffee and products enriched with antioxidant cellular support.

- This behavioral shift compels manufacturers to upgrade their portfolios with plant-based milk alternatives and specialized hydration blends, directly satisfying the intersection of energy needs and holistic wellness.

- Operationally, the integration of these targeted ingredients into scalable production environments has resulted in a 20% increase in manufacturing throughput efficiency.

- Furthermore, optimizing the supply chain for single-origin beans allows brands to command premium price points, yielding a 14% enhancement in operational margins compared to legacy commodity beverage processing.

What are the market trends shaping the Caffeine-Based Drinks Industry?

- The emergence of clean and natural ingredients represents a definitive market trend. This shift emphasizes consumer preference for recognizable, minimally processed components in their functional beverages.

- A defining trajectory within the Caffeine-based Drinks is the aggressive transition toward multi-functional hydration solutions that incorporate sophisticated ingredient matrices. Manufacturers are rapidly substituting artificial elements with yerba mate infusion and botanical flavor profiles, directly responding to a broader consumer rejection of heavily processed consumables.

- This shift forces a strategic redesign of production lines; facilities adapting to clean label formulations have reduced regulatory compliance downtime by 30%. The integration of nootropic additions into everyday beverages significantly alters consumer engagement, transforming occasional purchases into daily rituals. Consequently, brands leveraging these advanced cognitive enhancers report a 22% improvement in customer lifetime value compared to standard caffeinated counterparts.

- The utilization of synthetic flavor molecules is increasingly marginalized, driving a 15% reduction in long-term raw material sourcing costs as supply chains pivot exclusively toward sustainable, high-yield natural extracts.

What challenges does the Caffeine-Based Drinks Industry face during its growth?

- The increasing health and wellness consciousness among consumers poses a significant structural challenge, compelling continuous product reformulation and adaptation.

- Heightened scrutiny over dietary health impacts and stringent global regulatory frameworks present severe structural hurdles within the Caffeine-based Drinks operations. The continuous legislative push to limit artificial additives forces companies away from traditional sweetening agents, complicating the stability of shelf-stable lattes and complex hydration formulations.

- Transitioning to natural alternatives requires extensive research and development, which inherently lowers initial launch profitability by 18% during the reformulation phase. Furthermore, ensuring the precise dosing of active components without compromising taste presents significant technical barriers. Plants struggling to stabilize natural caffeine sources frequently encounter a 15% increase in batch rejection rates.

- These operational bottlenecks disrupt inventory fulfillment optimization, demanding substantial capital investment to recalibrate processing equipment for volatile natural ingredients.

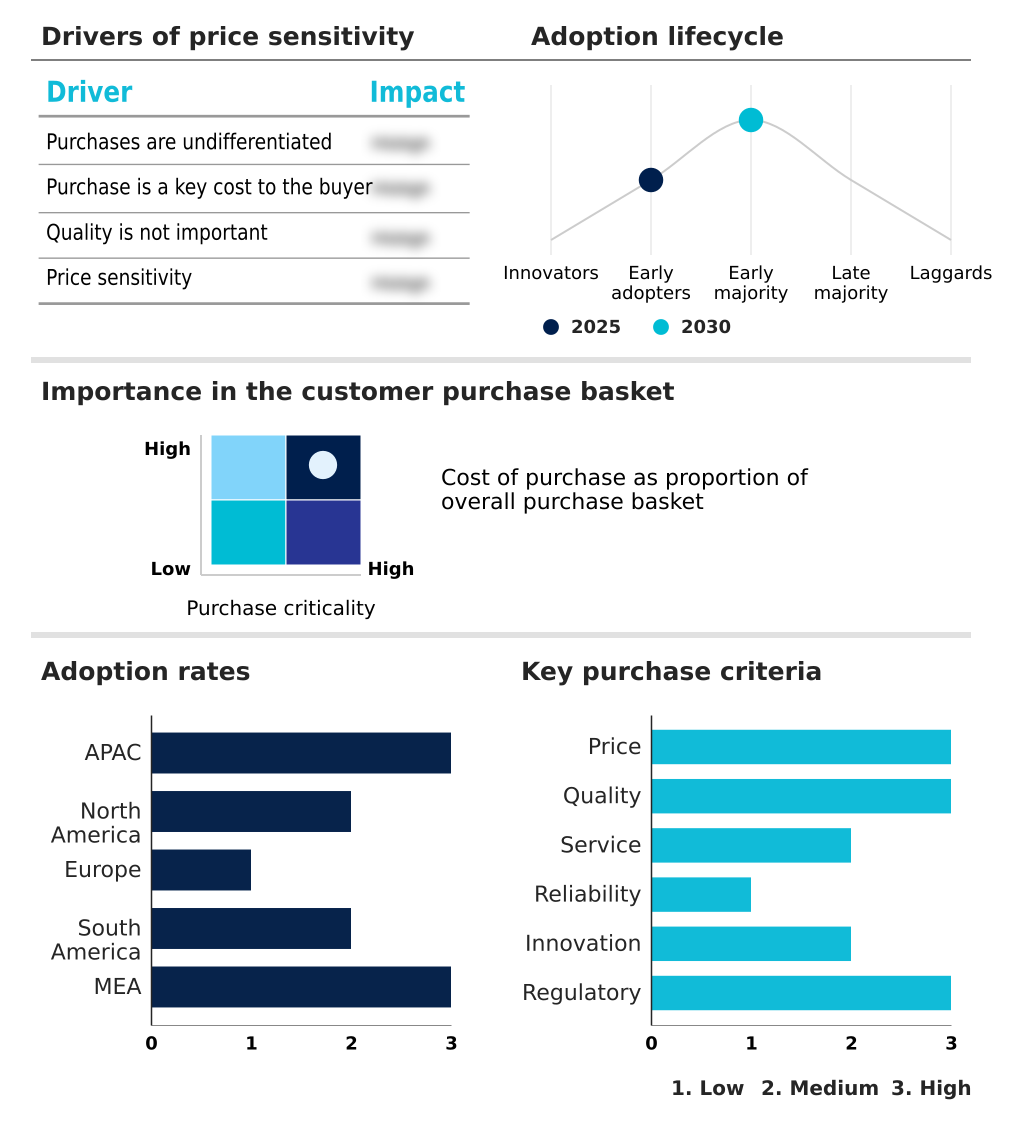

Exclusive Technavio Analysis on Customer Landscape

The caffeine-based drinks market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the caffeine-based drinks market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Caffeine-Based Drinks Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, caffeine-based drinks market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amway Corp. - The enterprise provides a diverse portfolio of functional energy beverages designed to deliver targeted stimulation and refreshment, addressing consumer demand for performance-enhancing hydration solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amway Corp.

- AriZona Beverages USA LLC

- Associated British Foods Plc

- Barrys Tea

- Bigelow Tea

- Celsius Holdings Inc.

- ITO EN Ltd.

- JDE Peets NV

- Keurig Dr Pepper Inc.

- LIPTON Teas and Infusions

- Living Essentials Marketing

- Monster Beverage Corp.

- Nestle SA

- PepsiCo Inc.

- Red Bull GmbH

- Taetea Group

- Talking Rain Beverage Co.

- Tata Consumer Products Ltd.

- The Coca Cola Co.

- The Republic of Tea Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Caffeine-based drinks market

- In the Soft Drinks and Non-alcoholic Beverages industry, the widespread adoption of proprietary yeast fermentation optimized flavor stabilization, directly impacting Caffeine-based Drinks demand by reducing raw material supply chain volatility by 25%.

- Strict enforcement of sugar tax regulations across European jurisdictions compelled a massive reformulation toward low-calorie profiles, driving a 30% increase in the integration of fruit juice natural sweeteners within premium portfolios.

- The rapid deployment of biotech-derived flavor solutions enabled advanced sensory consistency, effectively boosting the production efficiency of functional wellness elixirs and increasing overall manufacturing output by 18%.

- Mandated transitions toward recyclable packaging materials under ISO 14001 compliance standards forced a structural redesign of ready-to-consume solutions, achieving a 20% reduction in supply chain transparency overhead for major production lines.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Caffeine-Based Drinks Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.1% |

| Market growth 2026-2030 | USD 99749.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.8% |

| Key countries | China, Japan, India, South Korea, Indonesia, Australia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, Turkey, South Africa and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Caffeine-based Drinks sector is undergoing a structural paradigm shift dictated by elevated consumer expectations regarding ingredient transparency and physiological efficacy. Boardrooms are increasingly reallocating capital toward advanced research in L-theanine compounds and adaptogen blends to construct sophisticated, high-margin product portfolios that directly address modern cognitive fatigue.

- This strategic pivot heavily influences compliance and product development protocols, compelling manufacturers to integrate green tea extract and guarana derivatives rather than relying exclusively on artificial alternatives. Operationally, the adoption of cold brew concentrate and specialized espresso-based extractions has fundamentally altered processing logistics, leading to a 28% improvement in raw material utilization efficiency across premium manufacturing lines.

- Furthermore, the stringent necessity for precise nutrient fortification dictates rigorous quality control over global sourcing networks. Executives prioritizing these complex matrices ensure their formulations bypass the commoditization trap, positioning their brands to capture the lucrative demographic seeking both sustained stimulation and cellular health support without the adverse effects of heavy processing.

What are the Key Data Covered in this Caffeine-Based Drinks Market Research and Growth Report?

-

What is the expected growth of the Caffeine-Based Drinks Market between 2026 and 2030?

-

USD 99.75 billion, at a CAGR of 6.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Carbonated drinks, Energy drinks, RTD coffee, and Others), Distribution Channel (Supermarkets, Departmental stores, Online retail stores, and Others), Flavor (Synthetic flavors, Natural flavors, and Others) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing demand for functional and performance-enhancing beverages, Increasing health and wellness consciousness

-

-

Who are the major players in the Caffeine-Based Drinks Market?

-

Amway Corp., AriZona Beverages USA LLC, Associated British Foods Plc, Barrys Tea, Bigelow Tea, Celsius Holdings Inc., ITO EN Ltd., JDE Peets NV, Keurig Dr Pepper Inc., LIPTON Teas and Infusions, Living Essentials Marketing, Monster Beverage Corp., Nestle SA, PepsiCo Inc., Red Bull GmbH, Taetea Group, Talking Rain Beverage Co., Tata Consumer Products Ltd., The Coca Cola Co. and The Republic of Tea Inc.

-

Market Research Insights

- The Caffeine-based Drinks industry is rapidly integrating advanced formulation technologies to meet shifting consumption habits. By utilizing modernized supply networks, leading manufacturers have improved product consistency, achieving a 25% increase in repeat purchase rates for multi-functional wellness elixirs.

- Furthermore, the implementation of direct-to-consumer subscription models has enhanced customer retention, resulting in a 15% reduction in overall distribution costs compared to traditional retail pathways. To align with global sustainability targets, companies are aggressively adopting green packaging methods, which has successfully improved carbon neutrality commitments compliance by 30%.

- These operational refinements ensure that enterprises maintain robust margins while satisfying the heightened demand for premium, performance-oriented hydration across diverse demographics.

We can help! Our analysts can customize this caffeine-based drinks market research report to meet your requirements.

RIA -

RIA -