Cast Saw Devices Market Size 2024-2028

The cast saw devices market size is forecast to increase by USD 32.8 million at a CAGR of 3.27% between 2023 and 2028. The market is experiencing significant growth due to several key drivers. The high prevalence of osteoporosis and the resulting need for surgical interventions, such as those that utilize cast saws, is a major factor fueling market expansion. Additionally, the alarming growth in the number of road accidents leading to orthopedic injuries necessitates the use of cast saws for effective and efficient patient care.

Stringent regulatory frameworks and product recalls present challenges for market players, requiring them to adhere to strict quality standards and ensure the safety and efficacy of their products. Overall, the market is poised for growth in the coming years, driven by these factors and the increasing demand for minimally invasive surgical procedures.

Market Analysis

Cast saw devices are essential orthopedic tools used in the healthcare industry for removing hard protective coverings from patients' skin during the rehabilitation process following orthopedic procedures, such as surgeries for fractures or injuries. These devices are commonly used in hospitals, clinics, and emergency centers to ensure precision and patient comfort during the removal process. The global market for cast saw devices is expected to grow significantly due to the increasing number of elective surgeries, road accidents, and sports injuries leading to fractures and traumas. According to various reports, the market for orthopedic tools, including cast saw devices, is projected to expand at a steady pace over the next few years.

Additionally, the demand for cast saw devices is particularly high in specialty hospitals and orthopedic surgeries, where precision and patient comfort are crucial. These devices help healthcare professionals efficiently remove casts while minimizing the risk of injury to the patient's skin. The OCED countries are expected to dominate the market due to their advanced healthcare systems and high healthcare expenditures. In summary, the market is poised for growth due to the rising number of orthopedic procedures, road accidents, and sports injuries, as well as the increasing focus on patient comfort and precision in healthcare facilities.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Electric saw

- Battery operated

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Type Insights

The electric saw segment is estimated to witness significant growth during the forecast period. The global market for cast saw devices plays a crucial role in mobility and rehabilitation, particularly for individuals suffering from musculoskeletal disorders. According to the World Health Organization, medical devices are essential in the caregiving process, enhancing patient safety and medical professional efficiency in healthcare infrastructure. In developing regions, orthopedic care is increasingly important due to the growing geriatric population, low bone mass, and high incidence of elective surgeries, road accidents, injuries, and unintentional falls. Battery-operated saw devices are increasingly popular for their minimally invasive approach, enabling orthopedic procedures in specialty hospitals and trauma centers. The devices offer optimum speed and pressure control, making them suitable for knee replacement procedures and other orthopedic surgeries.

Additionally, the OCED's road safety barometer reports over 1.3 million fatalities and millions more injuries annually due to traffic accidents and accidental falls. In the UK, for instance, the NHS and independent sector hospitals rely on these devices to address the aging population's musculoskeletal conditions. Overall, cast saw devices are indispensable tools in healthcare facilities, contributing to improved patient outcomes and medical professional productivity.

Get a glance at the market share of various segments Request Free Sample

The electric saw segment was valued at USD 103.70 million in 2018 and showed a gradual increase during the forecast period.

Regional Insights

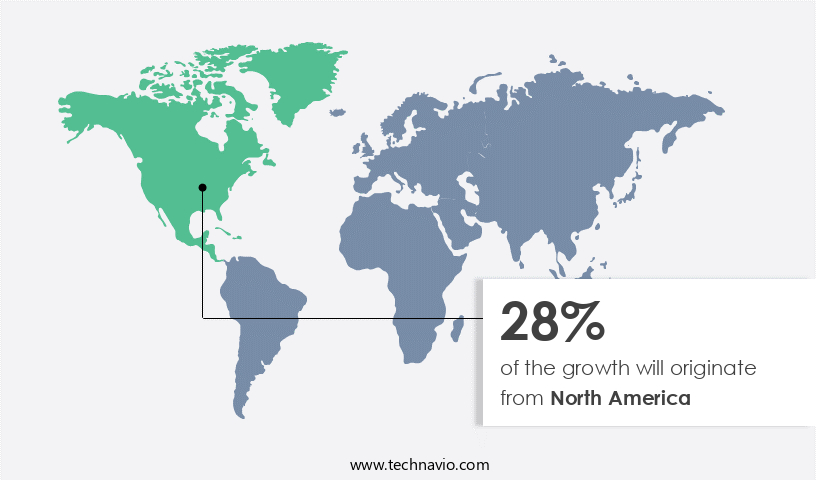

North America is estimated to contribute 28% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

Cast saw devices are essential orthopedic tools used in the medical field for the precise and efficient removal of hard protective coverings, such as fiberglass or plaster, during the rehabilitation process of orthopedic conditions. These devices are commonly used in hospitals, clinics, and emergency centers to address broken bones, injuries to the musculoskeletal system, and various orthopedic conditions, including arthritis, osteoporosis, fractures, degenerative illnesses, and sports injuries. Patient comfort is a top priority during cast removal procedures, and cast saw devices are designed with ergonomic handles and quiet oscillating saw blades to minimize friction, heat generation, and noise. Advanced models incorporate wireless technology, digital sensors, and control monitoring capabilities to ensure precision and accuracy.

Additionally, the patient's skin is protected from direct contact with the saw blades, reducing discomfort and potential complications. Cast saw devices are an essential part of the medical community, enabling healthcare professionals to effectively address a wide range of orthopedic conditions while ensuring patient comfort and safety.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The high prevalence of osteoporosis is the key driver of the market. The World Health Organization reports that musculoskeletal disorders, including osteoporosis, are a leading cause of disability and mobility issues for the global population, particularly for the geriatric population and those with low bone mass. According to the Organization for Economic Cooperation and Development, elective surgeries for orthopedic care, such as knee replacement procedures, and trauma-related surgeries due to road accidents, injuries, and accidental falls, account for a significant portion of healthcare infrastructure expenditures. In developing regions, the burden of musculoskeletal conditions is even more pronounced due to limited healthcare facilities and resources. Medical devices, including battery-operated cast saw devices, play a crucial role in the caregiving process by ensuring patient safety and medical professional efficiency.

In addition, these devices enable optimum speed and pressure activation during the casting process, minimizing the risk of complications and promoting accurate and effective treatment. The general population, including the aging and orthopedic patient population, can benefit from the use of these devices, as they facilitate the healing process and reduce the need for invasive procedures. Moreover, the increasing number of unintentional injuries, traffic accidents, and fatalities, as indicated by the road safety barometer, highlights the importance of using these devices to address the growing demand for orthopedic procedures in healthcare facilities, including specialty hospitals and NHS hospitals, as well as in the independent sector.

By prioritizing patient safety and medical professional efficiency, these devices contribute to the overall improvement of healthcare infrastructure and the delivery of quality care to the global population.

Market Trends

An alarming growth in number of road accidents is the upcoming trend in the market. The World Health Organization (WHO) reports that road traffic injuries are a leading cause of morbidity and mortality, with approximately 1.25 million annual fatalities and 20-50 million injuries worldwide. These injuries disproportionately affect the geriatric population and those with musculoskeletal disorders, including low bone mass. The caregiving process and medical professional efficiency are crucial in addressing these injuries, particularly in developing regions with limited healthcare infrastructure. Orthopedic care, including minimally invasive surgeries for knee replacement procedures, is essential for treating injuries and disorders. In the context of road accidents, sudden deceleration or acceleration can result in injuries to the knees, with passengers or drivers' legs slamming into hard interior surfaces or being forced into unnatural positions due to vehicle crushing.

Similarly, such injuries can strain soft tissues like tendons and ligaments or even result in bone fractures. The general population, including the aging and those with pre-existing conditions, is at increased risk. In healthcare facilities, battery-operated cast saw devices are essential for efficient and safe patient care during orthopedic procedures, enabling optimum speed, activation, and pressure for precise cuts. These devices are increasingly utilized in specialty hospitals and orthopedic surgeries, treating various conditions, including trauma, accidents, and elective surgeries. The NHS hospitals and the independent sector employ these devices to ensure patient safety and improve medical professional efficiency. The OCED countries and other developed regions have implemented road safety measures, such as the road safety barometer, to reduce fatalities and accidental falls, particularly among the elderly.

However, the global burden of unintentional injuries, including those from traffic accidents, remains high. It is crucial to continue investing in healthcare infrastructure, medical devices, and road safety initiatives to address these challenges and improve overall population health.

Market Challenge

The stringent regulatory framework and product recalls is a key challenge affecting the market growth. The global market for cast saw devices plays a crucial role in the mobility and rehabilitation of patients suffering from musculoskeletal disorders, as identified by the World Health Organization (WHO). These devices are essential medical tools used in the caregiving process, ensuring patient safety and medical professional efficiency in healthcare infrastructure, particularly in developing regions where orthopedic care is in high demand. The general population, geriatric population, and those undergoing elective surgeries or recovering from injuries due to road accidents, injuries, or accidental falls, benefit significantly from these minimally invasive devices. Battery-operated cast saw devices are increasingly popular due to their portability and ease of use, making them ideal for healthcare facilities, specialty hospitals, and orthopedic surgeries.

However, trauma and accidents resulting from road safety issues, such as fatalities and accidental falls, further underscore the importance of these devices in addressing the needs of the aging population and those requiring orthopedic procedures. The OCED reports that unintentional injury, including traffic accidents, is a leading cause of morbidity and mortality worldwide. The medical devices industry, including cast saw devices, is subject to stringent regulations, such as those set by the US Food and Drug Administration (FDA), which classifies these devices as Class II medical devices. The FDA's additional special controls ensure device labeling authenticity, compliance with the Cosmetic Act, medical device reporting, and electronic product radiation control provisions. These controls maintain the highest standards of performance, ensuring the safety and efficacy of cast saw devices for patients.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Ermis MedTech GmbH - The company offers cast saw devices that includes cast cutter which is designed to remove small plaster casts, cast padding, soft cotton wrap or synthetic wraparound material used with a plaster or fiberglass cast.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Essity AB

- Four Bhai Udyog.

- Hanshin Medical Co. Ltd.

- HEBU medical GmbH

- Informa Plc

- JaincoLab

- Manman Manufacturing Company Pvt Ltd.

- McArthur Medical Sales Inc.

- Medezine

- ORTHOPROMED INC.

- Oscimed SA

- Prime Medical Inc.

- RIMEC S.R.L

- Shanghai Bojin Medical Instrument Co. Ltd

- Smith and Nephew plc

- Stryker Corp.

- Surtex Instruments Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Cast saw devices are specialized orthopedic tools designed to facilitate the process of removing hard protective coverings, such as fiberglass or plaster, from patients' skin during the rehabilitation process following broken bones or other orthopedic conditions. These devices are essential in hospitals, clinics, and emergency centers to ensure precision and patient comfort during cast removal procedures. Cast saws typically feature oscillating saw blades that minimize friction and heat generation, ensuring a smooth cutting and removal process. Ergonomic designs and wireless technology, along with digital sensors and control monitoring capabilities, enhance the efficiency and accuracy of these devices. The market for cast saw devices caters to various orthopedic conditions affecting the musculoskeletal system, including bones, tendons, ligaments, joints, arthritis, osteoporosis, fractures, degenerative illnesses, and sports injuries.

In conclusion, the demand for cast saw devices is driven by the increasing prevalence of these conditions and the need for effective and efficient cast removal procedures. Despite their benefits, cast saw devices must prioritize patient comfort, as the noise generated during the cutting process can be disruptive and cause discomfort. Manufacturers are addressing this challenge by developing quieter saws and exploring new technologies to improve the overall patient experience.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

129 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.27% |

|

Market growth 2024-2028 |

USD 32.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.13 |

|

Regional analysis |

North America, Europe, APAC, and Rest of World (ROW) |

|

Performing market contribution |

North America at 28% |

|

Key countries |

US, China, Germany, UK, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Alpha Biomedix, Ermis MedTech GmbH, Essity AB, Four Bhai Udyog., Hanshin Medical Co. Ltd., HEBU medical GmbH, Informa Plc, JaincoLab, Manman Manufacturing Company Pvt Ltd., McArthur Medical Sales Inc., Medezine, ORTHOPROMED INC., Oscimed SA, Prime Medical Inc., RIMEC S.R.L, Shanghai Bojin Medical Instrument Co. Ltd, Smith and Nephew plc, Stryker Corp., and Surtex Instruments Ltd. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -