Central Fill Pharmacy Automation Market Size 2024-2028

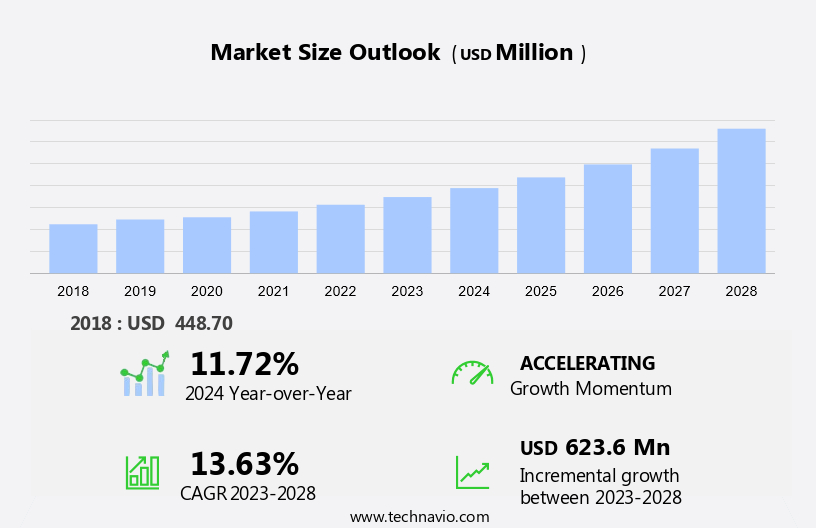

The central fill pharmacy automation market size is forecast to increase by USD 623.6 million at a CAGR of 13.63% between 2023 and 2028.

- The market In the healthcare sector is witnessing significant growth due to several key factors. The increasing adoption of automation solutions in healthcare is a major trend driving market growth. Automation solutions, such as robotics and automation systems, are increasingly being used for packaging and storing pharmaceutical products in central fill pharmacies. This not only improves efficiency but also reduces the risk of medication errors. Another factor fueling market growth is the outsourcing of pharmacy services to central fill facilities. These systems enable pharmacies to streamline their operations, reduce costs, and improve patient safety. Moreover, stringent government regulations for approval of pharmacy automation systems ensure the highest standards of safety and quality in medication dispensing.

- Home healthcare is another growing area for central fill pharmacy automation. With the increasing trend of home healthcare, there is a growing need for automated solutions to manage medication storage and dispensing. These systems provide an efficient and cost-effective solution for home healthcare providers to manage their medication inventory and ensure timely and accurate medication delivery to patients. Pharmaceutical equipment and professional services providers play a crucial role In the implementation and maintenance of these systems.

What will be the Size of the Central Fill Pharmacy Automation Market During the Forecast Period?

- The market encompasses the production and implementation of automated systems for medication preparation and prescription filling in healthcare facilities. This market is driven by several factors, including the growing patient pool and the increasing demand for patient safety and accuracy in pharmacy workflows. Automated tabletop systems and tension packaging solutions enable hospitals and pharmacies to streamline their operations and improve patient outcomes. The prevalence of chronic diseases and the centralization of prescription management have further fueled market growth. Pharmacists and skilled professionals are increasingly relying on automated dispensing systems to meet the rising pharmaceutical spending and comply with regulatory requirements.

- The market is characterized by a focus on electronic prescriptions and legally binding orders, as well as the integration of pharmacy management systems. Despite the benefits, challenges such as compliance with healthcare infrastructure and potential anti-dumping duties remain. Overall, the market is poised for continued expansion as healthcare organizations seek to enhance patient safety, improve medication accuracy, and optimize pharmacy workflows.

How is this Central Fill Pharmacy Automation Industry segmented and which is the largest segment?

The industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Inpatient pharmacy

- Outpatient pharmacy

- Retail pharmacy

- Type

- Equipment

- Services

- Geography

- North America

- US

- Europe

- Germany

- UK

- France

- APAC

- China

- South America

- Middle East and Africa

- North America

By Application Insights

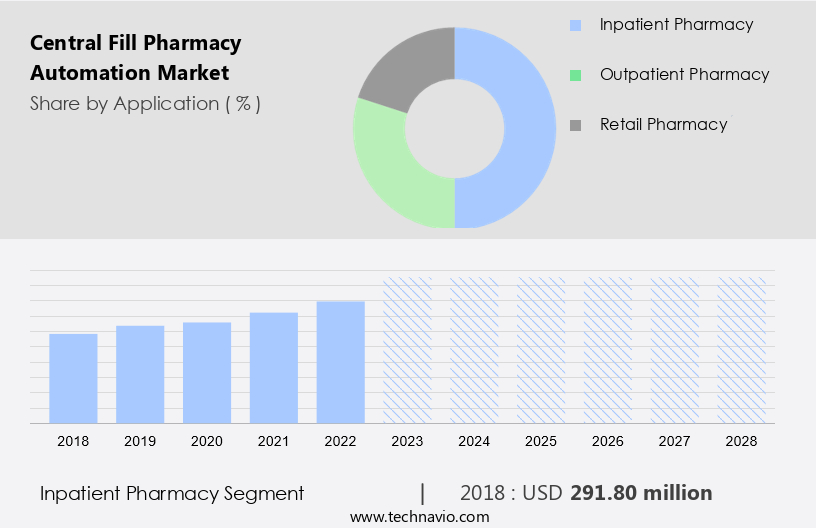

- The inpatient pharmacy segment is estimated to witness significant growth during the forecast period. The market is experiencing significant growth due to the increasing patient pool and the rising prevalence of chronic diseases requiring specialized medication. Pharmacists play a crucial role in inpatient care, improving patient outcomes through medication management, patient interviews, and counseling. Central fill pharmacy automation enhances pharmacist productivity and patient safety by reducing medication errors and streamlining pharmacy workflows. Technological advancements, such as automated dispensing and tension packaging, are essential to this market's growth.

- Hospitals and specialty pharmacies are major adopters of central fill pharmacy automation, particularly for compounding, controlled substance handling, and specialty drug dispensing. The market's attractiveness is further boosted by the increasing healthcare spending, healthcare infrastructure development, and compliance regulations. Initial investments in automation equipment and skilled professionals are necessary for successful implementation. The market is expected to continue growing, driven by the increasing burden on pharmacies and the need for accurate prescription filling and centralized prescription management.

Get a glance at the market report of share of various segments Request Free Sample

The Inpatient pharmacy segment was valued at USD 291.80 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

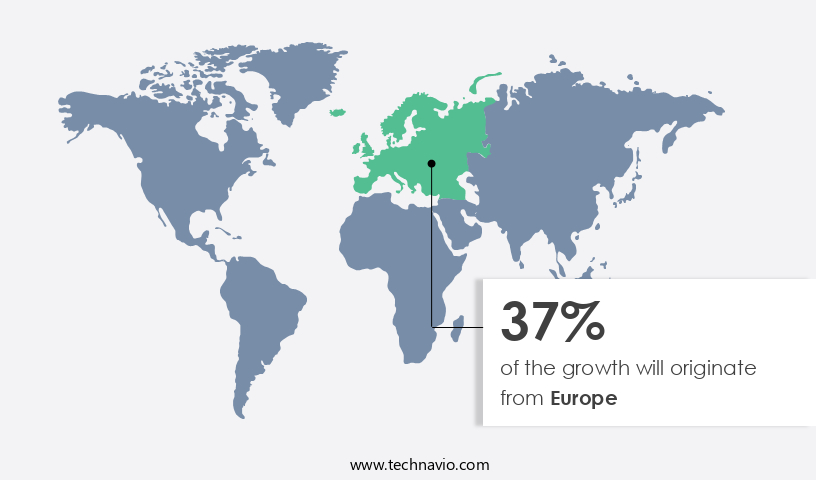

- Europe is estimated to contribute 37% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. Central fill pharmacy automation is a critical trend In the pharmaceutical industry, particularly in North America, which accounts for the largest market share. The US dominates this region due to its advanced healthcare infrastructure, comprising numerous hospitals and retail pharmacies. Central fill pharmacy automation is increasingly adopted to minimize medication errors, manage high prescription volumes, and cater to the needs of geriatric and obese patients.

For more insights on the market size of various regions, Request Free Sample

The growing prevalence of chronic diseases, such as diabetes and cardiovascular conditions, necessitates the use of specialized medication and compounding, further driving demand for central fill pharmacy automation. Automated tabletop systems, prescription filling, and tension packaging are essential components of this market. Pharmacists benefit from improved accuracy, streamlined workflows, and enhanced patient outcomes. Centralized prescription systems and automated dispensing are key features that contribute to the market's growth. Market players offer automated packaging and pharmaceutical equipment to meet the evolving needs of multispecialty hospitals, specialty medicine, and specialty drugs. The market is expected to continue growing due to increasing healthcare spending, pharmacy management, and the need for skilled professionals. Initial investments in automation technology can be substantial, but the long-term benefits in terms of compliance, process modeling, and market attractiveness make it a strategic position for pharmacies.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Central Fill Pharmacy Automation Industry?

- The rise in medication errors is the key driver of the market. Central fill pharmacy automation is a crucial solution for addressing the challenges posed by the increasing patient pool, particularly those requiring multiple medications. According to the Centers for Disease Control and Prevention (CDC), over half of Americans take multiple prescriptions daily, increasing the risk of medication errors. These errors can lead to significant health complications, resulting in emergency hospital visits and increased healthcare spending. Annually, hospitals incur an average cost of USD 60,000-USD 65,000 due to medication errors, amounting to a total expenditure of USD 3-6 billion. Central fill pharmacy automation, including automated tabletop systems and dispensing cabinets, plays a vital role in improving patient safety and staff productivity.

- Automated medication handling, such as tension packaging and compounding, is essential for managing complex patient profiles, especially for geriatric and obese patients. Technological development in pharmacy automation, including automated dispensing and packaging, has significantly reduced the prevalence of medication errors. Central fill pharmacy automation also supports the dispensing of controlled substances, specialty drugs, and compounding, ensuring regulatory compliance and accurate filling. This pharmacy model is increasingly attractive for multispecialty hospitals and specialty pharmacies due to its ability to improve pharmacy workflow, patient outcomes, and survival and quality of care for patients with chronic diseases. Initial investments in pharmacy automation may be high, but the long-term benefits, including increased process modeling, market attractiveness, and strategic positioning, far outweigh the costs.

What are the market trends shaping the Central Fill Pharmacy Automation Industry?

- Increasing adoption of automation in healthcare is the upcoming market trend. Central fill pharmacy automation is a significant trend In the healthcare sector, driven by the increasing adoption of technology to enhance patient safety and pharmacist productivity. Automated tabletop systems and medication dispensing solutions are transforming prescription filling processes, particularly in hospitals and multispecialty healthcare facilities. Automation reduces the burden on pharmacies by minimizing medication errors, improving accuracy of filling, and streamlining pharmacy workflows. Patient safety is a primary concern, especially for geriatric and obese patients, making automation an essential investment for healthcare providers. Automated dispensing systems also support the handling of controlled substances, specialty drugs, and compounding, which are prevalent in specialty pharmacies and outsourcing pharmacies.

- Technological development in automated packaging and pharmaceutical equipment further enhances the capabilities of central fill pharmacy automation. This shift towards automation contributes to data-driven insights, optimizing pharmacy performance and improving patient outcomes. Automation also supports compliance with regulations and initial investments in automation can lead to long-term savings and strategic positioning In the market.

What challenges does the Central Fill Pharmacy Automation Industry face during its growth?

- Stringent government regulations for approval of pharmacy automation systems is a key challenge affecting the industry growth. Central fill pharmacy automation refers to the use of automated tabletop systems for prescription filling in a centralized location, serving a large patient pool. Pharmacists at hospitals and other healthcare facilities employ these systems to enhance patient safety and staff productivity. Automation solution providers offer automated dispensing cabinets and tension packaging solutions to streamline medication handling. The prevalence of chronic diseases and the increasing population necessitate the adoption of pharmacy automation. Central fill pharmacy systems enable the handling of controlled substances and specialty drug dispensing with greater accuracy, reducing medication errors. The automation of pharmacy workflow leads to improved patient outcomes and centralized prescription management.

- Specialty medicine and specialty pharmacies are significant contributors to pharmaceutical spending. Automated packaging and pharmaceutical equipment are essential components of these pharmacy models, ensuring compliance with regulations and enhancing process modeling. Initial investments in pharmacy automation can be substantial but yield long-term benefits, including increased efficiency, skilled professionals, and market attractiveness. The technological development of pharmacy automation systems caters to the needs of geriatric and obese patients, addressing the burden on pharmacies. The automation of compounding and outsourcing pharmacies further expands the application areas of pharmacy automation. Despite the initial investments, the benefits of pharmacy automation, such as accuracy of filling, patient safety, and pharmacy management, make it a strategic positioning for healthcare infrastructure and pharmaceutical spending.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agilent Technologies Inc.

- ARxIUM Inc.

- Becton Dickinson and Co.

- Capsa Healthcare LLC

- Cornerstone Automation Systems LLC

- FORMULATRIX Inc.

- Gebr. Willach GmbH

- Innovation Associates

- KUKA AG

- LABEL ELETTRONICA S.R.L.

- McKesson Corp.

- Noritsu America Corp.

- Omnicell Inc.

- Oracle Corp.

- Quality Manufacturing Systems Inc.

- Rxsafe LLC

- ScriptPro LLC

- Sensum d.o.o.

- Tension Corp.

- Yuyama USA Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Central fill pharmacy automation refers to the implementation of technology and automated systems in pharmacies to streamline prescription filling processes. This approach allows for the centralized preparation and dispensing of medications, reducing manual labor and increasing efficiency. The growing patient pool and the prevalence of chronic diseases have placed significant tension on pharmacies, leading to a heightened focus on automation. The market is expanding as healthcare services increasingly adopt automated solutions to streamline medication dispensing, particularly for specialty pharmaceuticals that require precise handling and distribution. Pharmacists play a crucial role in this landscape, as they are responsible for ensuring patient safety and optimal medication outcomes. Central fill pharmacy automation offers several benefits, including improved patient safety, enhanced staff productivity, and increased accuracy of filling.

Moreover, the pharmaceutical industry has witnessed substantial technological development in recent years, with automation becoming a key trend. Central fill pharmacy automation encompasses various aspects, including automated dispensing, controlled substance management, and compounding. This automation not only benefits retail pharmacies but also outsources pharmacies and specialty pharmacies. The increasing burden on pharmacies due to the prevalence of chronic diseases and the rising healthcare spending has necessitated the adoption of central fill pharmacy automation. Specialty drugs and specialty medicine, which are often used to treat complex conditions, require specialized handling and packaging. Automated packaging solutions have emerged as a viable option to address these needs.

Furthermore, the pharmaceutical industry is subject to various regulations and compliance requirements, which can be challenging for pharmacies. Central fill pharmacy automation can help pharmacies navigate these complexities, ensuring legally binding processes and reducing the risk of medication errors. The market is characterized by its attractiveness to multispecialty hospitals and healthcare infrastructure, which often deal with a large volume of prescriptions. The use of electronic prescriptions and the centralized prescription filling process can lead to significant improvements in pharmacy workflow and patient outcomes. The pharmaceutical spending and healthcare infrastructure continue to evolve, with a growing emphasis on specialty medicine and generic medicines.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

156 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 13.63% |

|

Market growth 2024-2028 |

USD 623.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

11.72 |

|

Key countries |

US, Germany, UK, France, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the industry during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the market growth of industry companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -