Chemical Tanker Market Size 2026-2030

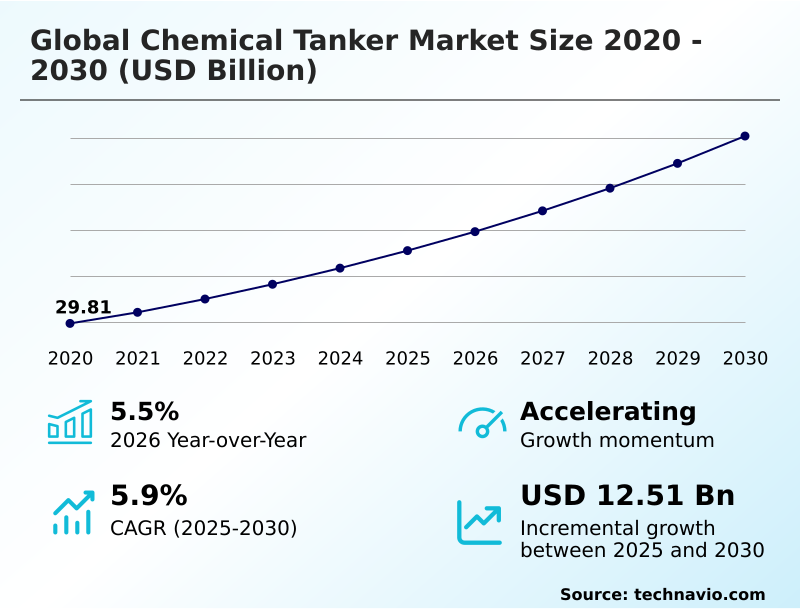

The chemical tanker market size is valued to increase by USD 12.51 billion, at a CAGR of 5.9% from 2025 to 2030. Stringent environmental regulations and drive for sustainability will drive the chemical tanker market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 52.7% growth during the forecast period.

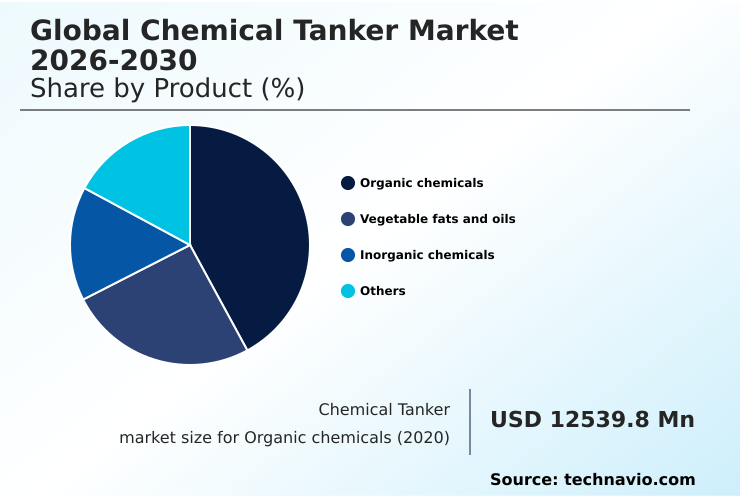

- By Product - Organic chemicals segment was valued at USD 14.81 billion in 2024

- By Type - Inland segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 20.44 billion

- Market Future Opportunities: USD 12.51 billion

- CAGR from 2025 to 2030 : 5.9%

Market Summary

- The chemical tanker market is navigating a period of significant transformation, defined by the convergence of stringent environmental mandates and rapid technological advancement. Fundamentally, the market facilitates global industrial activity by ensuring the safe and efficient seaborne transport of bulk liquid chemicals, a critical link in countless supply chains.

- Demand is increasingly shaped not just by cargo volumes but by the quality and sophistication of the vessels themselves. For instance, a decision to invest in a newbuild with dual-fuel propulsion versus retrofitting an existing vessel with an exhaust gas cleaning system highlights the strategic tightrope operators must walk.

- This choice balances immense capital intensity against the long-term risks of asset value obsolescence and evolving regulatory pressures. This dynamic, coupled with the growing trade of high-value specialty chemicals requiring advanced cargo segregation and stainless steel tanks, fosters a bifurcated market. Modern, efficient, and versatile parcel tankers command premium freight rates, incentivizing continuous fleet renewal.

- Concurrently, the accelerated adoption of digitalization, from voyage optimization systems to predictive maintenance protocols, is creating a more intelligent and responsive shipping ecosystem where data-driven operational models are a key competitive differentiator.

What will be the Size of the Chemical Tanker Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Chemical Tanker Market Segmented?

The chemical tanker industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

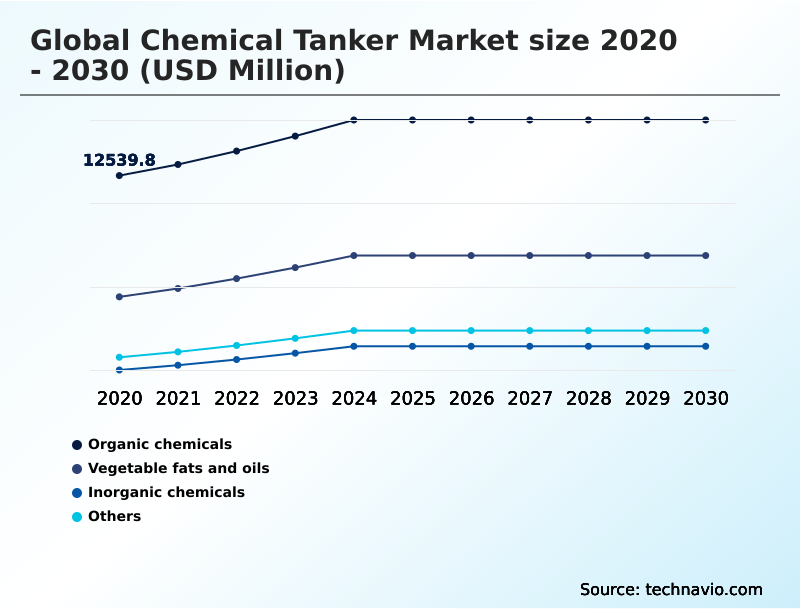

- Product

- Organic chemicals

- Vegetable fats and oils

- Inorganic chemicals

- Others

- Type

- Inland

- Coastal

- Deep sea

- Vessel orientation

- IMO 3

- IMO 2

- IMO 1

- Geography

- APAC

- China

- Japan

- South Korea

- Europe

- Germany

- The Netherlands

- UK

- North America

- US

- Canada

- Mexico

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Product Insights

The organic chemicals segment is estimated to witness significant growth during the forecast period.

The organic chemicals segment is foundational to the chemical tanker market, driven by global industrial production. This category includes fundamental building blocks like methanol and aromatics, transported from large-scale production hubs to manufacturing centers.

Trade dynamics are shaped by feedstock costs and the development of new production capacities, which can alter established long-haul chemical trade route optimization.

Vessels in this trade require advanced cargo containment systems, such as stainless steel cargo tank integrity or specialized epoxy coatings, to handle products that are often aggressive in nature.

The dual role of methanol as both a key cargo and a burgeoning alternative marine fuel is a unique dynamic, driving innovation in tanker design and positioning the segment at the forefront of decarbonization in chemical shipping.

The Organic chemicals segment was valued at USD 14.81 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 52.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Chemical Tanker Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the chemical tanker market is dominated by APAC, which accounts for over 52% of the incremental growth, driven by massive industrial and consumer demand in China and India.

This region functions as a primary destination for long-haul voyages carrying bulk liquid chemicals from production hubs in the Middle East and North America, underscoring the importance of long-haul chemical trade route optimization.

Europe remains a critical market, distinguished by its stringent regulatory environment and focus on high-value chemical cargo handling, which has increased operational compliance costs by an estimated 8%.

North America, particularly the US Gulf Coast, is a major export hub leveraging cost-advantaged feedstock.

The global nature of this trade reinforces the essential role of chemical tankers in facilitating complex international commerce, with operators navigating diverse regional dynamics and addressing maritime skills gap challenges to maintain service integrity worldwide.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the strategic complexities of the global chemical tanker market requires a deep understanding of intertwined technical, commercial, and regulatory pressures. Ensuring bulk liquid chemical transport safety remains paramount, compelling operators to invest in vessels that meet stringent IMO II chemical tanker specifications and feature advanced cargo containment system requirements.

- This focus on quality is crucial for high-value chemical cargo handling, where maintaining product purity is a key performance metric. Concurrently, the industry is grappling with an alternative marine fuel adoption strategy to achieve decarbonization in chemical shipping.

- This transition creates a significant challenge in managing asset value obsolescence risk, as decisions on dual-fuel tanker investment analysis have long-term financial implications. Firms undertaking fleet renewal and modernization financing must weigh the benefits of new technology against inherent market cyclicality. Effective specialized chemical parcel tanker operations depend on sophisticated logistics and predictive maintenance for marine assets to maximize utilization.

- For trade within the US, ensuring Jones Act compliant chemical transport adds another layer of operational planning. Ultimately, success hinges on a holistic approach that integrates environmental regulation compliance in shipping with sustainable chemical supply chain logistics, all while mitigating geopolitical risk in shipping.

What are the key market drivers leading to the rise in the adoption of Chemical Tanker Industry?

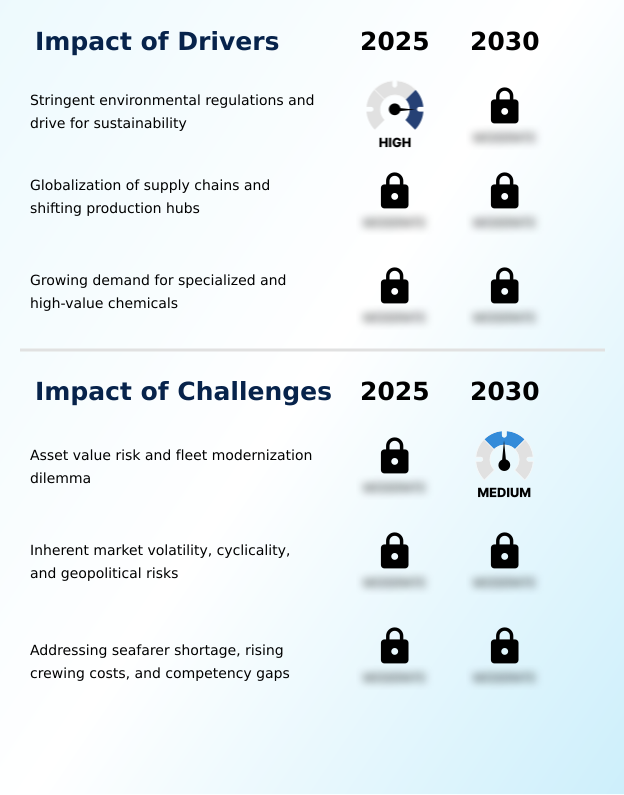

- Stringent environmental regulations and the overarching drive for sustainability serve as paramount drivers, compelling a systemic shift toward more responsible and technologically advanced shipping practices.

- Market growth is propelled by powerful structural and regulatory forces. Stringent environmental regulations, particularly those targeting greenhouse gas emissions, are a primary driver for fleet modernization and the adoption of alternative fuels, creating a clear preference for modern, fuel-efficient vessels.

- The globalization of chemical supply chains has geographically dislocated production and consumption, increasing average voyage distances and boosting tonne-mile demand by over 25% on key trade routes.

- This dynamic benefits all vessel types, from those with specialized IMO 1 certification to standard IMO 3 tankers.

- Furthermore, escalating demand for specialized and high-value chemicals, which require superior cargo integrity, fuels the need for sophisticated tankers equipped with stainless steel tanks. These high-specification vessels can command freight premiums of up to 15%, incentivizing investment in advanced assets.

What are the market trends shaping the Chemical Tanker Industry?

- The accelerated adoption of digitalization and advanced data analytics is an emerging trend. This shift toward data-driven operational models is fundamentally reshaping fleet management and competitive strategies.

- Key trends reshaping the chemical tanker market center on digitalization and structural evolution. The accelerated integration of advanced data analytics is creating a more efficient ecosystem, where voyage optimization platforms can reduce fuel consumption by up to 14%. This shift enables holistic fleet performance management and proactive predictive maintenance strategies, minimizing unscheduled downtime.

- Concurrently, the industry is witnessing persistent market consolidation, with mergers and vessel pooling arrangements creating larger, integrated operators. These entities leverage economies of scale and offer the global service coverage demanded by major charterers.

- A third critical trend is the heightened focus on crew competence and addressing the widening skills gap, with leading companies investing heavily in advanced training to manage increasingly complex vessels and dual-fuel propulsion technologies, enhancing operational safety.

What challenges does the Chemical Tanker Industry face during its growth?

- The profound uncertainty surrounding long-term asset values, which creates a complex fleet modernization dilemma for shipowners, presents a key challenge for the industry.

- The chemical tanker market confronts significant strategic challenges, primarily asset value risk stemming from technological and regulatory uncertainty around decarbonization. This fleet modernization dilemma complicates investment, as a newbuild vessel today faces potential obsolescence, with some 10-year-old conventional tankers seeing their value decline by 40% more than dual-fuel counterparts.

- The market's inherent volatility and cyclicality, driven by the mismatch between rigid supply and fluctuating demand, makes long-term financial planning exceptionally difficult. Compounding these issues is a critical human element challenge: a growing seafarer shortage and a widening competency gap.

- The need for crews skilled in managing advanced systems has driven crewing costs up by approximately 15% in recent years, impacting operational expenses and posing a direct risk to safety and sustainability.

Exclusive Technavio Analysis on Customer Landscape

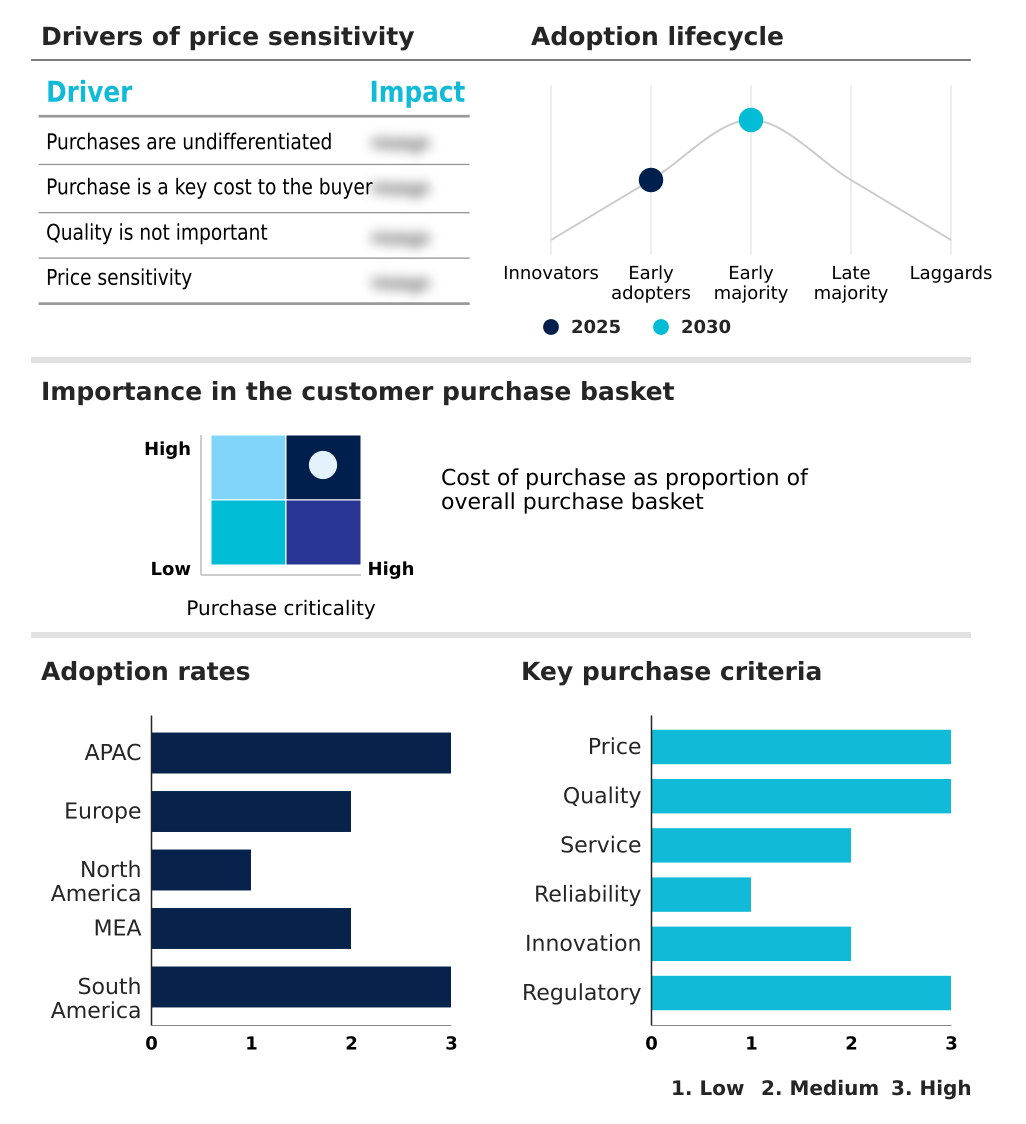

The chemical tanker market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the chemical tanker market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Chemical Tanker Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, chemical tanker market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AceTankers - Analysis focuses on operators providing global seaborne transportation through modern, specialized product and chemical tankers capable of carrying diverse cargoes.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AceTankers

- Ardmore Shipping Corporation

- Bahri

- IINO Kaiun Kaisha Ltd.

- IMC Ship Management Pte Ltd.

- Kawasaki Kisen Kaisha Ltd.

- KOYO KAIUN Co. Ltd.

- M.T.M. Ship Management Pte Ltd

- MOL CHEMICAL TANKERS PTE. LTD.

- Navig8 Group

- PT BERLIAN LAJU TANKER TBK

- Seatrans Chemical Tankers

- Stena Bulk

- Stolt Nielsen Ltd.

- UltraTank

- Uni-Tankers

- Wilmar International Ltd.

- Womar Pools Pte Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Chemical tanker market

- In August 2025, Castrol launched a new range of MHP marine lubricants specifically formulated for vessels using alternative fuels, supporting the industry's energy transition.

- In May 2025, Brazil's Port of Açu secured financing from the International Finance Corporation to expand its infrastructure and support its transition to a low-carbon model, enhancing regional trade capabilities.

- In March 2025, Odfjell retrofitted its chemical tanker, the BOW Olympus, with four eSAILs, a wind propulsion system designed to reduce fuel consumption and greenhouse gas emissions.

- In January 2025, Hercules Tanker Management announced the addition of the Hercules Galaxy, a modern IMO Type 2 chemical tanker, to its fleet, reflecting ongoing fleet renewal in North America.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Chemical Tanker Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.9% |

| Market growth 2026-2030 | USD 12505.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.5% |

| Key countries | China, Singapore, Japan, South Korea, India, Indonesia, Germany, The Netherlands, Belgium, UK, France, Spain, US, Canada, Mexico, UAE, Saudi Arabia, Qatar, Iran, South Africa, Brazil, Argentina and Venezuela |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The chemical tanker market is defined by a strategic push toward technological and environmental evolution. The operational core involves sophisticated vessels, including parcel tankers equipped with numerous segregated stainless steel tanks, designed to transport a vast array of products from commodity vegetable oils to high-hazard IMO 1 cargoes.

- A primary boardroom-level focus is capital allocation for fleet modernization, driven by the need to comply with tightening regulations on carbon intensity. For example, investment in dual-fuel propulsion systems, capable of running on alternative fuels like methanol or liquefied natural gas, is a direct response to this pressure.

- Vessels with this capability can achieve a carbon intensity reduction of over 20% compared to conventional designs. This technological shift, which includes innovations like wind propulsion systems and advanced epoxy coatings, is creating a two-tier market. Modern, eco-friendly ships with advanced cargo segregation capabilities command higher freight rates, while older tonnage faces accelerated value depreciation.

- This dynamic is intensified by the adoption of predictive maintenance and voyage optimization systems, which are becoming standard for ensuring safety and efficiency in transporting sensitive specialty chemicals.

What are the Key Data Covered in this Chemical Tanker Market Research and Growth Report?

-

What is the expected growth of the Chemical Tanker Market between 2026 and 2030?

-

USD 12.51 billion, at a CAGR of 5.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Organic chemicals, Vegetable fats and oils, Inorganic chemicals, and Others), Type (Inland, Coastal, and Deep sea), Vessel Orientation (IMO 3, IMO 2, and IMO 1) and Geography (APAC, Europe, North America, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Stringent environmental regulations and drive for sustainability, Asset value risk and fleet modernization dilemma

-

-

Who are the major players in the Chemical Tanker Market?

-

AceTankers, Ardmore Shipping Corporation, Bahri, IINO Kaiun Kaisha Ltd., IMC Ship Management Pte Ltd., Kawasaki Kisen Kaisha Ltd., KOYO KAIUN Co. Ltd., M.T.M. Ship Management Pte Ltd, MOL CHEMICAL TANKERS PTE. LTD., Navig8 Group, PT BERLIAN LAJU TANKER TBK, Seatrans Chemical Tankers, Stena Bulk, Stolt Nielsen Ltd., UltraTank, Uni-Tankers, Wilmar International Ltd. and Womar Pools Pte Ltd.

-

Market Research Insights

- The chemical tanker market's dynamics are shaped by the intricate balance between a volatile demand landscape and a capital-intensive, inelastic supply side. Navigating chemical tanker market cyclicality requires robust risk management to counter fluctuating freight rates. Advanced voyage optimization systems are being adopted to enhance vessel operational efficiency, with some operators reporting fuel consumption reductions of up to 12%.

- Furthermore, the move toward a data-driven operational model allows for predictive maintenance, which can decrease unscheduled downtime by over 25%, directly improving asset utilization. The commercial viability of a fleet is increasingly tied to its environmental performance, forcing strategic decisions around fleet renewal and modernization financing to manage long-term asset value risk and secure favorable chartering decisions.

We can help! Our analysts can customize this chemical tanker market research report to meet your requirements.

RIA -

RIA -