Europe Chiller Market Size 2026-2030

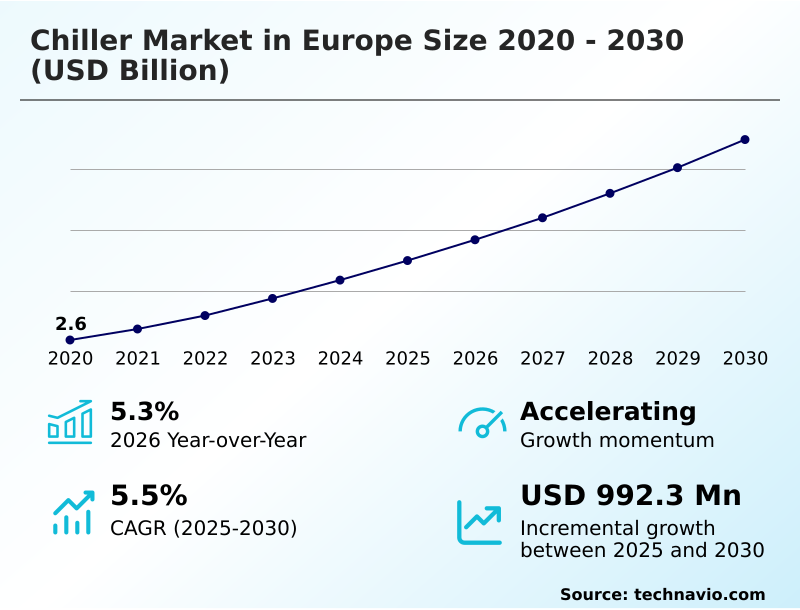

The Europe Chiller Market size was valued at USD 3.25 billion in 2025, growing at a CAGR of 5.5% during the forecast period 2026-2030.

Major Market Trends & Insights

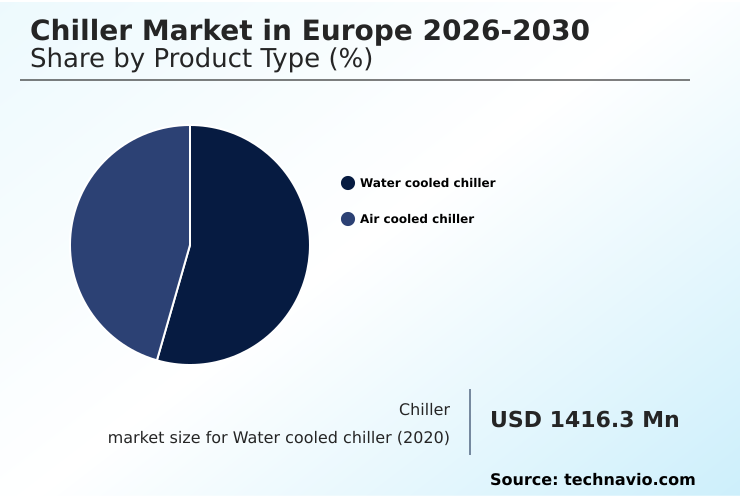

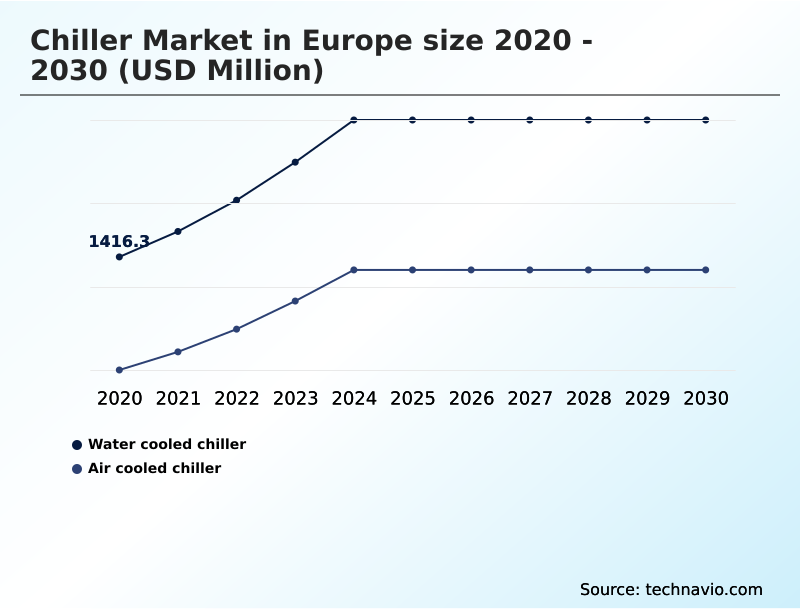

- By Product Type - Water cooled chiller segment was valued at USD 1.70 billion in 2024

- By Type - Screw chillers segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 1.64 billion

- Market Future Opportunities 2025-2030: USD 992.3 million

- CAGR from 2025 to 2030 : 5.5%

Market Summary

- The chiller market in Europe is defined by a mandatory transition towards high-efficiency, sustainable cooling technologies, with new regulations accelerating the refrigerant phase-down by over 40% compared to previous targets. This shift is driven by stringent F-gas regulation compliance, compelling manufacturers to abandon high-GWP substances and invest in systems using natural refrigerants.

- For example, an industrial processing facility must now evaluate not just the initial capital expenditure (CAPEX) but also the long-term operational expenditure (OPEX) related to refrigerant availability and carbon taxes, making total cost of ownership (TCO) a critical metric.

- A primary challenge remains the skilled labor shortage, where a lack of technicians trained in new refrigerant handling protocols can lead to 15% longer downtimes. This regulatory and operational landscape necessitates the adoption of advanced thermal management solutions to maintain both compliance and competitiveness in an evolving market.

What will be the Size of the Europe Chiller Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Europe Chiller Market Segmented?

The europe chiller industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product type

- Water cooled chiller

- Air cooled chiller

- Type

- Screw chillers

- Scroll chillers

- Centrifugal chillers

- Others

- Application

- Industrial

- Commercial

- Residential

- Geography

- Europe

- Germany

- France

- UK

- Europe

How is the Europe Chiller Market Segmented by Product Type?

The water cooled chiller segment is estimated to witness significant growth during the forecast period.

The water cooled chiller segment represents 55.1% of the chiller market in Europe, primarily serving large-scale applications where high-efficiency is critical.

This segment's adoption is driven by superior energy performance, with water-cooled systems demonstrating up to 30% greater efficiency than comparable air-cooled units in high-load industrial processes.

The segment is segmented by the use of hydrofluoro-olefins (HFOs) and variable speed drive (VSD) technology, which optimize part-load performance and comply with stringent regulations.

For instance, the integration of magnetic bearing technology in centrifugal compressors is becoming standard for reducing total cost of ownership (TCO).

Consequently, the market is characterized by a move towards advanced thermal management solutions and plug-and-play modules that improve both operational efficiency and environmental compliance within the building management systems.

The Water cooled chiller segment was valued at USD 1.70 billion in 2024 and showed a gradual increase during the forecast period.

What are the key Drivers, Trends, and Challenges in the Europe Chiller Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Analyzing water cooled vs air cooled chiller efficiency reveals that operational context is paramount, with water-cooled systems offering up to 30% better performance in stable, high-load industrial settings. However, the impact of F-gas regulation on chiller selection is steering decisions toward long-term compliance over initial cost, complicating procurement.

- The benefits of centrifugal chiller magnetic bearing technology, such as a 10% reduction in maintenance costs and lower noise, are driving its adoption in sensitive commercial environments. Examining screw chiller part-load performance shows significant efficiency gains from variable speed drives, making them ideal for fluctuating demand profiles.

- Nonetheless, natural refrigerant adoption challenges in chillers, including flammability and toxicity concerns, require specialized engineering and stringent safety protocols, impacting system design and installation. The technical complexities mean that a thorough evaluation of cooling requirements is essential for ensuring both regulatory adherence and operational effectiveness across diverse applications.

What are the key market drivers leading to the rise in the adoption of Europe Chiller Industry?

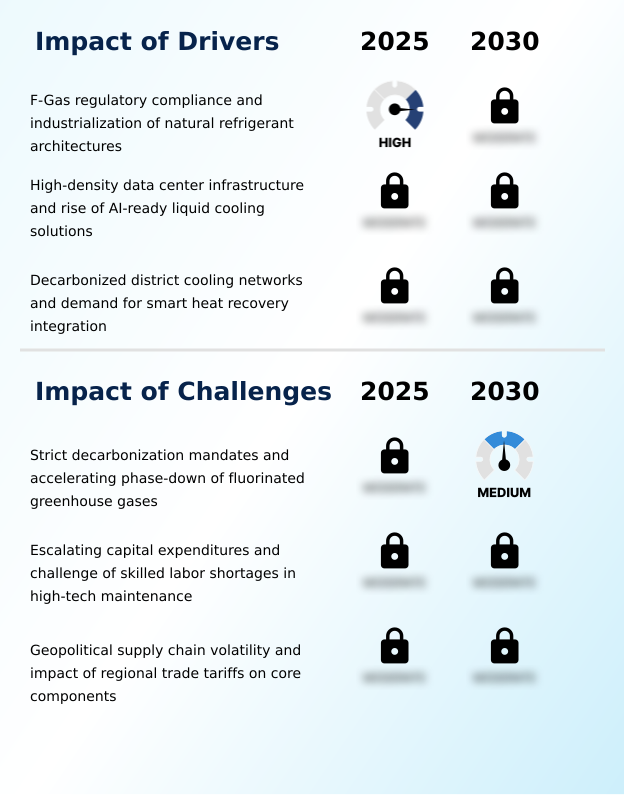

- Compliance with F-Gas regulations and the subsequent industrialization of natural refrigerant architectures serve as a primary driver, reshaping product design and investment priorities across the market.

- Strict decarbonization mandates are a primary market driver, compelling a rapid transition toward chillers that utilize natural refrigerants and low-GWP hydrofluoro-olefins (HFOs).

- This shift is in direct response to F-gas regulation compliance, which has accelerated the refrigerant phase-down and made adherence a prerequisite for market access.

- The expansion of high-density data center infrastructure is another significant factor, with demand for sophisticated thermal management solutions growing at over 16% annually. This surge fuels the adoption of high-capacity systems designed to improve power usage effectiveness (PUE).

- Furthermore, the growth of decarbonized district cooling networks, which integrate heat recovery and thermal energy storage, creates sustained demand for large-scale, energy-efficient chiller plants that contribute to net-zero emissions targets.

What are the market trends shaping the Europe Chiller Industry?

- The institutionalization of modular scalability is a defining market trend, with prefabricated, plug-and-play chiller plants becoming standard for rapid deployment in high-growth sectors.

- The institutionalization of modular chiller design is a primary trend, with prefabricated, plug-and-play modules now representing over 40% of new deployments in mission-critical facilities. This shift enables incremental capacity scaling, reducing initial capital expenditure (CAPEX) and shortening project timelines by up to 30%.

- Driven by the need for agility in fast-growing sectors like data centers, this approach favors operational expenditure (OPEX) models. Another key trend is the rise of Cooling-as-a-Service (CaaS), a performance-based model where customers pay for cooling outcomes rather than equipment.

- This service-oriented approach aligns with circular economy principles and incentivizes providers to maximize efficiency through predictive maintenance alerts and advanced controls, ensuring optimized system performance and extending asset lifecycles within building management systems.

What challenges does the Europe Chiller Industry face during its growth?

- Strict decarbonization mandates and the accelerating phase-down of fluorinated greenhouse gases present a significant challenge, demanding rapid innovation and costly redesigns from manufacturers.

- Intensive regulatory volatility, led by the stringent implementation of the revised F-gas Regulation, presents a formidable market challenge, increasing R&D costs by an estimated 15% as manufacturers re-engineer products for natural refrigerants.

- This is compounded by escalating capital expenditures and a pervasive skilled labor shortage, with a lack of certified technicians hindering the installation and maintenance of complex systems featuring magnetic bearing technology. Furthermore, geopolitical supply chain volatility, including anti-dumping duties and regional trade tariffs on essential electronic controls and compressors, has inflated procurement costs by approximately 12%.

- This instability disrupts manufacturing schedules and forces companies to balance cost optimization against the need for more resilient, localized supply networks, affecting total cost of ownership (TCO) for end-users.

Exclusive Technavio Analysis on Customer Landscape

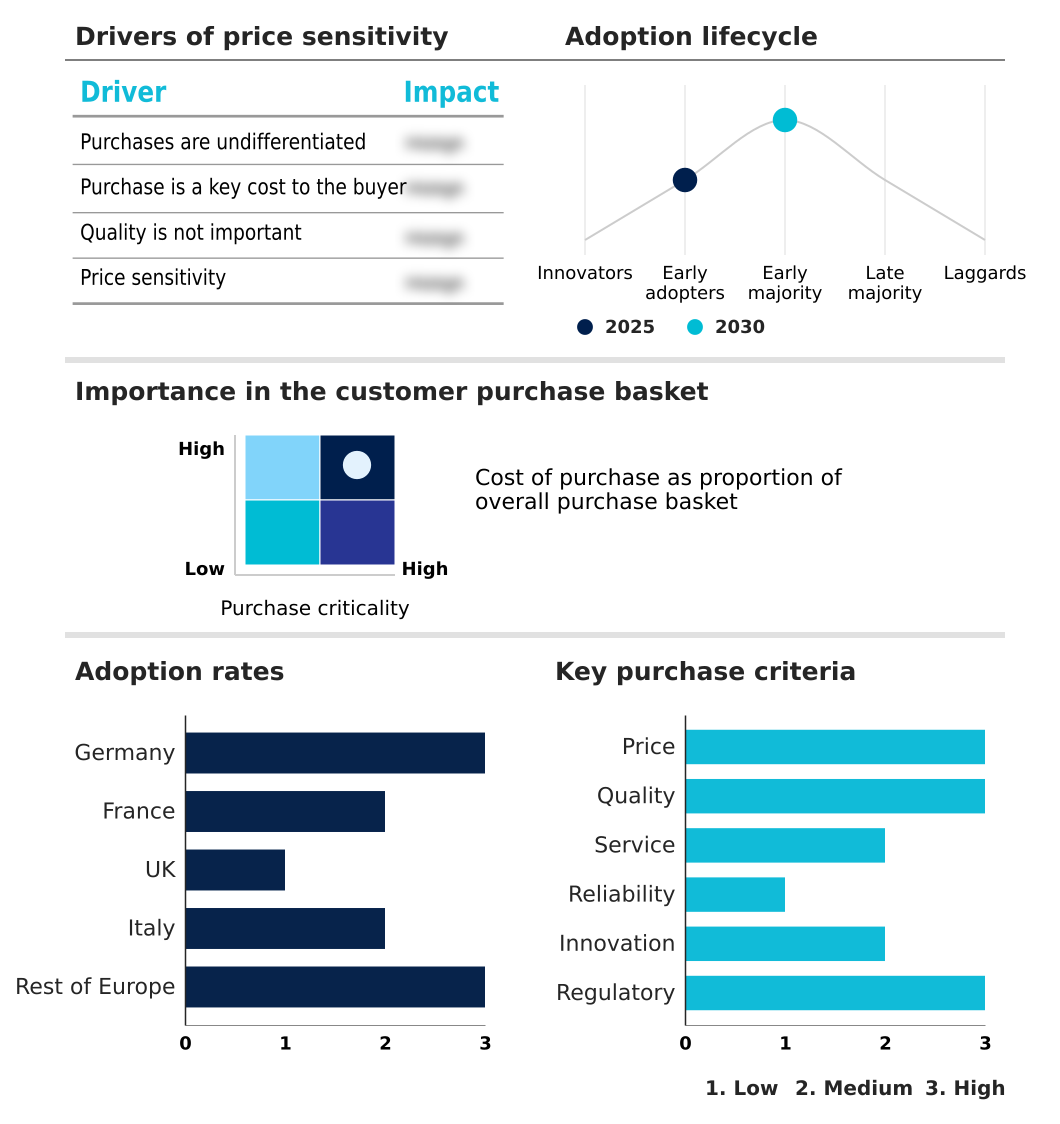

The europe chiller market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the europe chiller market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Europe Chiller Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, europe chiller market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Carrier Global Corp. - Vendors provide high-efficiency chiller systems, incorporating advanced inverter-driven technology, modular designs, and sustainable refrigerants to address commercial and industrial cooling needs with enhanced energy management.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Carrier Global Corp.

- Daikin Industries Ltd.

- Danfoss AS

- FlaktGroup Holding GmbH

- Haier Smart Home Co. Ltd.

- Honeywell International Inc.

- Ingersoll Rand Inc.

- Johnson Controls International

- Kaltra GmbH

- Kirloskar Group

- LG Electronics Inc.

- MIDEA Group Co. Ltd.

- Mitsubishi Electric Corp.

- Modine Manufacturing Co.

- Nortek

- Panasonic Holdings Corp.

- Regal Rexnord Corp.

- Samsung Electronics Co. Ltd.

- Systemair AB

- Trane Technologies Plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Electrical Components and Equipment industry, the enforcement of stringent environmental standards, such as F-gas regulations, directly accelerates the transition to low-GWP refrigerants in the chiller market in Europe 2026-2030, compelling manufacturers to invest heavily in natural refrigerant architectures and hydrofluoro-olefins (HFOs).

- A widespread shift toward Industry 4.0 and automation in manufacturing is increasing demand for process cooling applications, driving the adoption of smart chillers with predictive maintenance alerts and enhanced building management systems integration, improving operational reliability by over 25%.

- Increasing investments in smart grid infrastructure and demand-response asset programs are fostering the development of energy-resilient cooling systems, including hybrid chillers that can switch between power sources, enhancing grid stability and reducing operational expenditure (OPEX) for end-users.

- Supply chain volatility and the implementation of regional trade tariffs on core components like semiconductors and specialized metals are forcing a strategic realignment toward localized sourcing, impacting the capital expenditure (CAPEX) and production timelines for chiller manufacturers.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Europe Chiller Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 218 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.5% |

| Market growth 2026-2030 | USD 992.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.3% |

| Key countries | Germany, France, UK, Italy and Rest of Europe |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The chiller market in Europe ecosystem is a complex network where raw material suppliers of copper and aluminum, providing over 60% of the heat exchanger materials, are influenced by global commodity prices. Manufacturers like Carrier and Daikin integrate these components with advanced technologies such as variable speed drives and low-GWP refrigerants sourced from specialized chemical producers.

- The entire value chain operates under the strict oversight of regulatory bodies enforcing F-gas regulations, which dictate product design and market access. Distribution channels range from direct sales for large industrial projects to extensive networks of HVAC contractors for commercial and residential installations, who are also a key source of aftermarket services.

- End-users, from data center operators to hospitals, drive demand based on total cost of ownership and energy efficiency, creating a feedback loop that influences future R&D and product innovation.

What are the Key Data Covered in this Europe Chiller Market Research and Growth Report?

-

What is the expected growth of the Europe Chiller Market between 2026 and 2030?

-

The Europe Chiller Market is expected to grow by USD 992.3 million during 2026-2030, registering a CAGR of 5.5%. Year-over-year growth in 2026 is estimated at 5.3%%. This acceleration is shaped by f-gas regulatory compliance and industrialization of natural refrigerant architectures, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Product Type (Water cooled chiller, and Air cooled chiller), Type (Screw chillers, Scroll chillers, Centrifugal chillers, and Others), Application (Industrial, Commercial, and Residential) and Geography (Europe). Among these, the Water cooled chiller segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers Europe. Country-level analysis includes Germany, France, UK, Italy and Rest of Europe, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is f-gas regulatory compliance and industrialization of natural refrigerant architectures, which is accelerating investment and industry demand. The main challenge is strict decarbonization mandates and accelerating phase-down of fluorinated greenhouse gases, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Europe Chiller Market?

-

Key vendors include Carrier Global Corp., Daikin Industries Ltd., Danfoss AS, FlaktGroup Holding GmbH, Haier Smart Home Co. Ltd., Honeywell International Inc., Ingersoll Rand Inc., Johnson Controls International, Kaltra GmbH, Kirloskar Group, LG Electronics Inc., MIDEA Group Co. Ltd., Mitsubishi Electric Corp., Modine Manufacturing Co., Nortek, Panasonic Holdings Corp., Regal Rexnord Corp., Samsung Electronics Co. Ltd., Systemair AB and Trane Technologies Plc. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape, where the top five vendors account for over 45% of market share, is shaped by strategic acquisitions and technological innovation focused on sustainability. Key players such as Johnson Controls and Trane Technologies are expanding their portfolios to include next-generation thermal management technologies, with new magnetic bearing chillers offering a 20% increase in capacity density.

- These moves are a direct response to the escalating demand from high-density data center applications and the need for compliance with European Union sustainability directives. Manufacturers are integrating low-GWP refrigerants and AI-driven diagnostics to meet stringent F-gas regulations.

- However, the industry grapples with geopolitical supply chain volatility, which has increased procurement costs for essential components by approximately 12%, forcing companies to re-evaluate sourcing strategies and balance cost optimization with regional resilience.

We can help! Our analysts can customize this europe chiller market research report to meet your requirements.

RIA -

RIA -