Chronic Wound Care Market Size 2024-2028

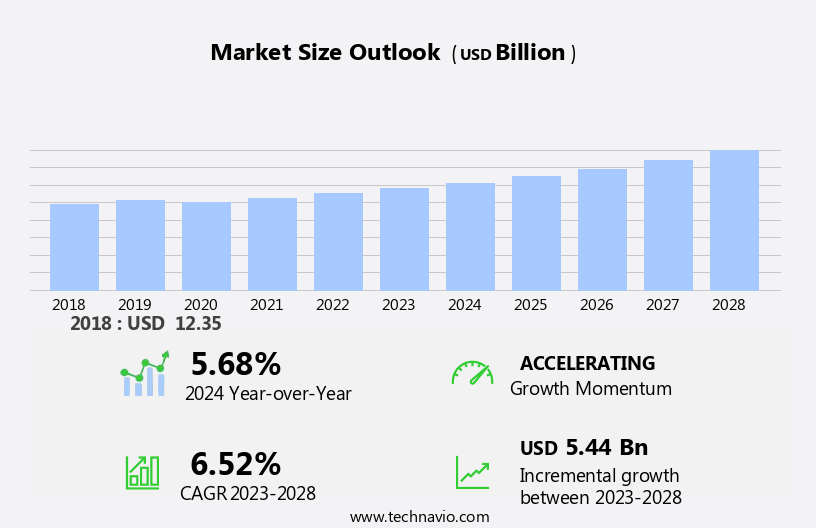

The chronic wound care market size is forecast to increase by USD 5.44 billion at a CAGR of 6.52% between 2023 and 2028.

- Chronic wounds, including surgical wounds and trauma wounds, pose a significant challenge to healthcare systems due to their prevalence and high treatment costs. Factors such as wound infections, compromised immune function, and poor circulation contribute to the complexity of managing these wounds. In response, the market for chronic wound care solutions is witnessing notable trends, including the increasing adoption of advanced wound care technologies like moist wound dressings. Hospitals and specialty clinics are integrating wound care teams to improve patient outcomes and reduce healthcare costs. However, the high expense of chronic wound treatment remains a significant challenge for both providers and patients.

What will be the Size of the Market During the Forecast Period?

- The market represents a significant and growing segment within the healthcare industry. Chronic wounds, such as those resulting from diabetes, pressure ulcers, venous ulcers, arterial ulcers, and other chronic diseases including cancer and autoimmune diseases, present unique challenges for effective treatment and healing. Chronic diseases, including diabetes, are a leading cause of chronic wounds. Diabetes-related foot ulcers alone account for a substantial portion of chronic wounds, with an estimated 15% of people with diabetes developing a foot ulcer at some point in their lives.

- Another significant contributor to chronic wounds is the changing lifestyle trends, leading to an increase in obesity, sedentary lifestyles, and unhealthy diets. These factors can result in a higher incidence of chronic wounds, particularly pressure ulcers, which affect individuals with limited mobility and those requiring extended hospital stays. The rising prevalence of chronic wounds is driving demand for advanced wound care solutions. Medical devices, such as medical tapes, bandages, and wound dressings, play a crucial role in the treatment and management of chronic wounds. These products are designed to promote wound healing, protect against infection, and provide a comfortable and secure covering for the wound.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Advanced dressing

- Traditional wound care

- Surgical wound care

- Wound therapy devices

- Application

- Diabetic foot ulcers

- Pressure ulcers

- Venous leg ulcers

- Geography

- North America

- US

- Europe

- Germany

- UK

- France

- Asia

- Japan

- Rest of World (ROW)

- North America

By Product Insights

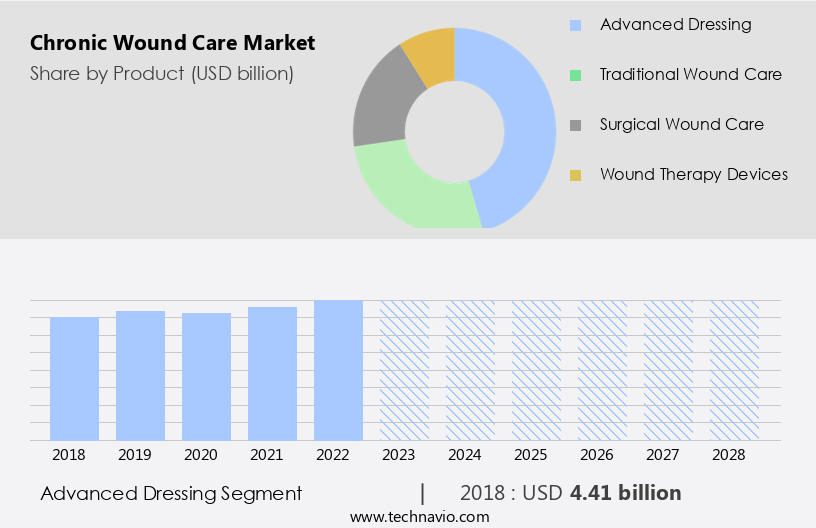

- The advanced dressing segment is estimated to witness significant growth during the forecast period.

In the realm of chronic wound care, various supplies play a pivotal role in ensuring optimal healing. Among these, sterilization supplies and hand sanitizers are essential for maintaining a clean and hygienic environment. Obesity is a significant contributor to chronic wounds, particularly in the form of lower extremity amputations. Advanced wound dressings, such as hydrocolloid, gel, film, alginate, and foam dressings, are utilized to protect the surrounding tissue and wound base. These dressings absorb exudate or hold onto moisture, enabling the wound to heal effectively. Advanced wound dressings, like alginate, offer high absorbency and transform into a gel upon contact with the wound surface.

Furthermore, this gel can be effortlessly removed with a dressing or washed off with sterile saline. Traditional wound dressings and surgical wound dressings also hold importance in wound care. Wound therapy devices, such as negative pressure wound therapy and electrical stimulation, further enhance the healing process. The market for chronic wound care supplies is segmented into the hospital segment and home healthcare segment. The hospital segment accounts for a larger share due to the availability of advanced medical facilities and specialized care. The home healthcare segment is expected to witness significant growth due to the increasing trend of home-based healthcare and the convenience it offers to patients.

Get a glance at the market report of share of various segments Request Free Sample

The advanced dressing segment was valued at USD 4.41 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

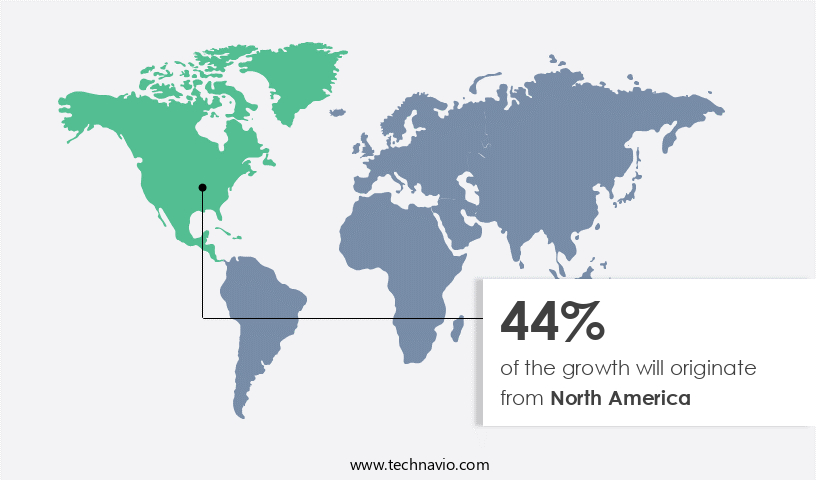

- North America is estimated to contribute 44% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In North America, the market is experiencing significant growth due to the rising number of individuals with chronic, non-healing wounds. Factors contributing to this trend include an aging population, increased prevalence of chronic health conditions such as diabetes and obesity, and an uptick in accidents and surgeries. To address these complex needs, manufacturers of medical devices and healthcare providers are focusing on developing advanced products and treatments that enhance wound healing and minimize costs. Innovations like the use of bioactive materials and smart dressings have significantly improved chronic wound care, among other technological advancements. The industry's expansion is essential in reducing hospital admissions and improving the quality of life for those affected by acute and chronic wounds.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of the Chronic Wound Care Market?

The rising prevalence of chronic wounds is the key driver of the market.

- The market in the US is experiencing notable expansion due to the increasing prevalence of chronic wounds, which can last for over three months. Chronic wounds are commonly associated with various conditions such as diabetes, sports injuries, autoimmune diseases, cancer, and obesity. Diabetic foot ulcers, for instance, develop in people with diabetes, often due to nerve damage and poor circulation. These ulcers can worsen if left untreated, leading to potential complications like lower extremity amputations. Moreover, chronic diseases like pressure ulcers, venous ulcers, arterial ulcers, and diabetic ulcers are also significant contributors to the market's growth. Advanced wound dressings, medical tapes, bandages, drug delivery products, respiratory supplies, sterilization supplies, and hand sanitizers are some of the essential wound care products in demand.

- The market is segmented into hospitals and home healthcare, with surgical procedures being a significant driver for the hospital segment. In-home care settings, patient support programs and traditional wound care techniques are prevalent. Wound therapy devices like Negative Pressure Wound Therapy (NPWT) systems and foam dressings are increasingly popular due to their ability to maintain a moist wound environment and prevent excessive moisture buildup. Factors like changing lifestyles, increasing chronic health conditions, and accidents contribute to the rising number of chronic wound cases. Additionally, medical tourism and the geriatric population's growing needs further fuel market growth. The active therapy and bioactive therapy segments are gaining traction due to their effectiveness in promoting the healing process.

What are the market trends shaping the Chronic Wound Care Market?

Increasing adoption of advanced wound care technologies is the upcoming trend in the market.

- The market in the US is experiencing a notable shift towards the utilization of advanced wound care technologies. Factors fueling this trend include the escalating prevalence of chronic wounds, the expanding geriatric population, and the demand for enhanced treatment modalities. Chronic wounds, such as diabetic foot ulcers, pressure ulcers, and venous leg ulcers, pose a substantial healthcare concern due to their complex nature and potential complications. These complications can lead to pain, disability, and diminished quality of life for patients. In response, specialized wound care centers have emerged, offering targeted treatments to expedite the healing process. Advanced wound care technologies encompass a range of products and techniques, including medical tapes, bandages, drug delivery systems, respiratory supplies, sterilization supplies, hand sanitizers, and various types of wound dressings.

- These innovations cater to the unique needs of chronic wounds, addressing issues like autoimmune diseases, obesity, lower extremity amputations, and compromised immune function or poor circulation. The market is segmented into the hospital and home healthcare sectors, with surgical procedures and medical tourism also playing a role in its growth. Active therapies and bioactive therapies, such as foam dressings, moist wound environments, and advanced wound dressing materials, are increasingly being adopted to optimize the healing process. The market is further driven by the rising number of chronic health conditions and lifestyle factors contributing to chronic wound cases, as well as trauma cases and patient support programs.

What challenges does the Chronic Wound Care Market face during its growth?

The high cost of chronic wound treatment is a key challenge affecting the market growth.

- Chronic wounds, such as those resulting from sports injuries, diabetes, changing lifestyles leading to obesity, and chronic diseases like cancer and autoimmune diseases, require specialized and prolonged care. The treatment process for chronic wounds involves various interventions, including wound assessment, infection control, debridement, offloading, and the use of advanced wound dressings, medical tapes, bandages, drug delivery products, respiratory supplies, sterilization supplies, and hand sanitizers. These interventions often need to be repeated over an extended period, leading to increased costs. One significant contributor to the high cost of chronic wound care is the need for specialized healthcare professionals, such as wound care teams, who possess expertise in managing these complex conditions.

- Their extensive training and experience add to the overall cost. Additionally, the use of advanced wound therapy devices, such as Negative Pressure Wound Therapy (NPWT) systems, foam dressings, and moist wound dressings, also contributes to the high cost. Moreover, chronic wounds, including diabetic foot ulcers, pressure ulcers, venous ulcers, arterial ulcers, and surgical wounds, can lead to lower extremity amputations, hospital admissions, and increased healthcare services utilization. The high prevalence of chronic health conditions and lifestyle factors, such as obesity and accidents, contribute to the increasing number of chronic wound cases. In the US market, the market caters to the needs of various end-users, including hospitals and specialty clinics.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- B.Braun SE

- Baxter Regional Medical Center

- Bioventus LLC

- Brightwake Ltd.

- Cardinal Health Inc.

- Coloplast AS

- ConvaTec Group Plc

- Essity AB

- Integra Lifesciences Corp.

- Johnson and Johnson

- Medline Industries LP

- Medtronic Plc

- Mil Laboratories Pvt. Ltd.

- MiMedx Group Inc.

- Paul Hartmann AG

- Smith and Nephew plc

- Welcare Industries SpA

- Zimmer Biomet Holdings Inc.

- DermaRite Industries LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Chronic wounds, such as those caused by sports injuries, diabetes, changing lifestyles, chronic diseases like cancer and autoimmune diseases, and surgical procedures, can be challenging to heal due to factors like antimicrobial resistance and compromised immune function. Advanced wound care solutions include medical tapes, bandages, drug delivery products, sterilization supplies, and hand sanitizers. These products cater to various end-use segments, including hospitals and home healthcare, and address different types of wounds, such as diabetic foot ulcers, pressure ulcers, and venous ulcers. Active and bioactive therapies, including foam dressings and polymer-based dressings infused with bioactive agents, promote a moist wound environment essential for the healing process.

Furthermore, wound therapy devices, such as negative pressure wound therapy systems, also play a crucial role in managing chronic wounds. In-home care settings, active therapy and bioactive wound care dressings facilitate the healing process for patients with chronic health conditions and lifestyle factors contributing to delayed wound healing. Wound care teams employ various techniques to address trauma cases, surgical wounds, burn injuries, and other chronic wounds, ensuring optimal patient outcomes.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

166 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.52% |

|

Market Growth 2024-2028 |

USD 5.44 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.68 |

|

Key countries |

US, Germany, UK, France, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -