Coconut Alcohol Market Size 2024-2028

The coconut alcohol market size is forecast to increase by USD 170.78 million, at a CAGR of 4.86% between 2023 and 2028.

- The market is experiencing significant growth due to increasing consumer preferences for natural and plant-based alcoholic beverages. This trend is driving the market, with numerous new product launches in the coconut alcohol segment. However, the difficulty in sourcing tender coconuts remains a challenge for market players. Producers must ensure a consistent supply of high-quality coconuts to meet the growing demand for coconut alcohol. These beverages are also gluten-free, low in sugar, and rich in beneficial nutrients, making them an attractive alternative to traditional alcoholic drinks like black grape juice or beer. As the market expands, innovation and sustainability will be key factors for success. Companies must focus on developing eco-friendly production methods and creating unique product offerings to differentiate themselves in the competitive landscape. Overall, the market is poised for growth, with opportunities for new entrants and established players alike.

What will be the Size of the Coconut Alcohol Market During the Forecast Period?

- The market encompasses a range of coconut-based alcoholic beverages, including spirits such as coconut rum and whiskey, liquors like coconut liquor and arrack, and wines. This market has experienced significant growth due to increasing health-consciousness among consumers, as coconut-based alcohol offers unique health benefits derived from the coconut tree and its fruit. The production process involves fermentation of coconut sap or the juice of flower buds, followed by distillation to produce the desired alcohol content.

- Moreover, coconut sap, a byproduct of coconut tree tapping, is also used to create coconut wine. Additionally, the popularity of solid food trends, such as coconut oil and chips, has further boosted the market. The palm tree family, which includes coconut trees, provides an abundant source of sugars, making coconut alcohol a sustainable and eco-friendly alternative to traditional alcoholic beverages.

How is this Coconut Alcohol Industry segmented and which is the largest segment?

The coconut alcohol industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Distribution Channel

- Offline

- Online

- Type

- Coconut wine

- Beer

- Others

- Geography

- APAC

- China

- North America

- US

- Europe

- UK

- South America

- Middle East and Africa

- APAC

By Distribution Channel Insights

- The offline segment is estimated to witness significant growth during the forecast period.

The market is experiencing growth due to increasing consumer preference for healthier alcoholic beverages, such as Coconut Water Wine. The offline distribution segment, including supermarkets and hypermarkets, dominates the market. This is largely due to urbanization and changing consumer lifestyles, which have led to an increase in demand for convenience and a wide selection of products. Retailers offer promotions and easy price comparisons, while the large shelf space in these stores allows for a diverse range of offerings from various companies. Market participants are expanding their geographical reach by collaborating with major retailers like Walmart Inc. Consumers continue to seek out new and healthier alcoholic beverage options, driving the demand for coconut alcohol.

Get a glance at the Coconut Alcohol Industry report of share of various segments Request Free Sample

The offline segment was valued at USD 414.85 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

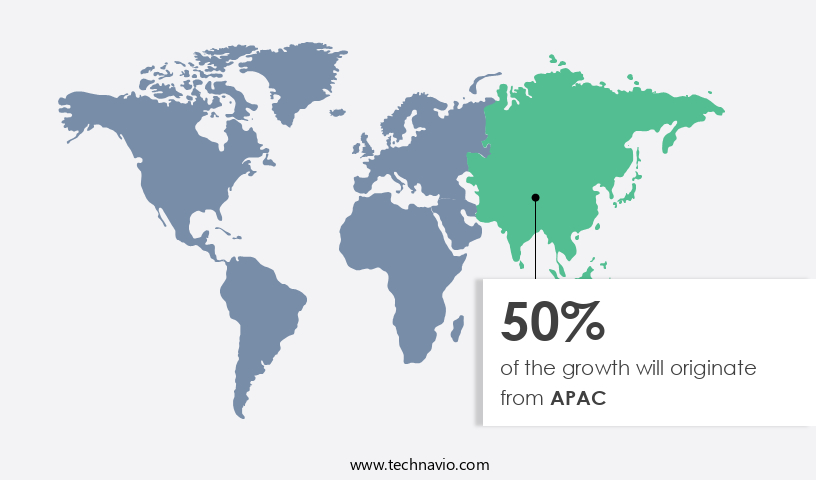

- APAC is estimated to contribute 50% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The Asia Pacific (APAC) region dominates The market due to the rising consumer preference for unique and tropical flavors. Key factors driving market growth include increasing health-consciousness and awareness about the benefits of coconut alcohol, the expanding food service industry serving coconut-based alcoholic beverages, and the growing consumer spending on alcoholic beverages such as wines, spirits, and beer in countries like China and India. Coconut spirits, liquor, wine, arrack, rum, and whiskey are popular categories in the market. APAC's high consumption level of coconut alcohol compared to other regions and the increasing disposable income of consumers in the region contribute to the market's growth.

Market Dynamics

Our coconut alcohol market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of the Coconut Alcohol Industry?

Increasing consumer preference for natural and plant-based alcoholic beverages is the key driver of the market.

- The market is thriving due to the growing preference for natural and plant-based alcoholic drinks. This trend is driven by the rise in health-conscious consumers seeking beverages that align with their dietary choices and wellness goals. Coconut spirits, liquor, wine, arrack, rum, and whiskey are popular choices in this category, offering exotic flavors with tropical notes. Distillers employ various fermentation techniques to extract the alcohol from coconut sap, water, fruit, or chips. These eco-friendly alternatives to traditional alcohol production methods are gaining traction in the beverage industry, as they avoid the use of artificial additives and chemicals commonly found in mass-produced alcoholic drinks.

- Moreover, coconut-based alcoholic beverages are also gluten-free and low in sugar, making them appealing to a wider audience. They are rich in beneficial nutrients like vitamins and minerals, derived from the coconut tree and its various parts, such as sap, oil, and chips. Sustainable cultivation practices, such as avoiding pesticides and ensuring optimal soil conditions, contribute to the sustainability goals of the market. As consumers become increasingly aware of the environmental impact of their choices, the demand for coconut alcohol is expected to continue growing. Coconut alcohol is versatile and can be used as a mixer in cocktails or enjoyed on its own.

What are the market trends shaping the Coconut Alcohol Industry?

New coconut alcohol product launches are the upcoming trend in the market.

- The market is experiencing growth due to the increasing demand for health-conscious alcoholic beverages. Coconut-based spirits, such as coconut liquor, rum, and whiskey, are gaining popularity for their exotic flavors and tropical notes. Coconut wine and coconut arrack are also emerging as eco-friendly alternatives to traditional alcoholic beverages. Manufacturers are adopting innovative fermentation techniques and coconut distillation processes to create high-quality coconut alcohol. These beverages offer healthier lifestyles as they are gluten-free, low in sugar, and rich in beneficial nutrients like vitamins and minerals. Coconut water, coconut oil, chips, sap, and toddy are also used in the production of these alcoholic drinks.

- Furthermore, new product launches by regional and international players are driving the growth of The market. For instance, Watertown Whiskey, a US-based whiskey brand, recently introduced a coconut whiskey product. These new product launches increase competition among companies and offer a competitive edge. However, it is essential to ensure sustainable cultivation practices, such as avoiding pesticides and focusing on soil conditions, to meet sustainability goals. The beverage industry is embracing these coconut-based alcoholic beverages, with pubs and pub culture incorporating them into their offerings. The market for these products is expected to continue growing as consumers seek out natural ingredients and healthier alcohol options.

What challenges does the Coconut Alcohol Industry face during its growth?

Difficulty in sourcing tender coconuts is a key challenge affecting the industry's growth.

- The market is experiencing growth due to the increasing demand for health-conscious alcoholic beverages, such as coconut spirits, liquor, wine, and rum. Coconut distillation and fermentation techniques are used to produce these exotic beverages, which offer tropical notes and unique flavors. However, the sourcing of tender coconuts is a significant challenge for market growth. Coconuts are primarily grown in tropical regions with specific climate requirements, including high humidity and temperatures. As a result, countries such as Indonesia, the Philippines, India, Sri Lanka, Mexico, Brazil, and Vietnam are the major suppliers of coconuts for the production of coconut alcohol.

- Moreover, companies have had to source coconuts from these countries to meet the rising demand, which can lead to higher prices due to supply chain complexities. In response, some distillers are exploring eco-friendly alternatives, such as using coconut water, sap, chips, or toddy as raw materials. These sustainable cultivation practices align with the beverage industry's sustainability goals and reduce the need for artificial additives and chemicals in the processing of coconut alcohol. The market for coconut-based alcoholic beverages is expected to continue growing as consumers seek out healthier lifestyles and natural ingredients.

Exclusive Customer Landscape

The coconut alcohol market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

The coconut alcohol industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Anheuser Busch InBev SA NV

- Bacardi Ltd.

- Becle SAB de CV

- Brinley Gold Shipwreck

- Campari Group

- Charles Jacquin et Cie. Inc.

- CoCo Vodka

- COTTON and REED

- CREAMY CREATION

- Diageo Plc

- Don Q Rum

- E. and J. Gallo Winery

- Fishbowl Spirits

- Heaven Hill Sales Co.

- HOUSE OF ELRICK

- Marigot Bay

- Molson Coors Beverage Co.

- NEITIV

- Paradise Rum

- Pernod Ricard SA

- Real McCoy Spirits Corp.

- Suntory Holdings Ltd.

- Watertown Whiskey

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Coconut-based alcoholic beverages, a captivating segment in the global alcohol industry, have been garnering significant attention due to their unique tropical notes and exotic flavors. These beverages, which include coconut spirits, liquor, wine, arrack, rum, and whiskey, offer a distinct taste profile that appeals to consumers seeking a departure from traditional alcoholic offerings. The production process of coconut-based alcoholic beverages involves distillation and fermentation techniques, which transform the natural sugars present in coconut sap, toddy, or coconut water into an alcoholic liquid. The result is a drink that boasts a smooth texture and a rich, complex flavor profile, often reminiscent of the tropical regions where these beverages originate.

In addition, as health-consciousness continues to be a driving force in consumer behavior, coconut-based alcoholic beverages have emerged as a popular choice for those seeking alternatives to alcoholic drinks laden with artificial additives and chemicals. The natural ingredients used in the production of these beverages, coupled with their eco-friendly production methods, align well with sustainability goals and the growing trend towards sustainable cultivation practices in the beverage industry. Despite the allure of these beverages, the production process can be complex. Coconut distillation requires careful attention to soil conditions, pesticide use, and sustainable practices to ensure the highest quality product. The palm tree family, which includes the coconut tree, plays a crucial role in the production of these beverages.

Furthermore, the coconut fruit, a rich source of vitamins and minerals, provides the essential sugars necessary for fermentation. Coconut water, another byproduct of the coconut tree, has gained popularity as a mixer in cocktails due to its natural sweetness and low sugar content. It offers a healthier alternative to traditional mixers, making it a preferred choice for those following gluten-free or low-sugar diets. The affordability of coconut-based alcoholic beverages, coupled with their unique taste and health benefits, has led to their increasing popularity in pub culture. Consumers are drawn to the exotic flavors and the opportunity to explore new alcoholic beverage options, making this segment a dynamic and growing market.

Moreover, as the demand for natural, eco-friendly alternatives to traditional alcoholic beverages continues to rise, the coconut-based alcoholic beverages market is poised for continued growth. The industry is expected to see innovation in production methods, packaging, and distribution channels, making these beverages more accessible to consumers around the world. Therefore, the coconut-based alcoholic beverages market is an intriguing and dynamic segment of the global alcohol industry. With their unique taste profile, health benefits, and eco-friendly production methods, these beverages offer a compelling alternative to traditional alcoholic offerings. As consumers continue to seek out natural, sustainable options, the market for coconut-based alcoholic beverages is expected to thrive.

|

Coconut Alcohol Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

151 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.86% |

|

Market Growth 2024-2028 |

USD 170.78 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.9 |

|

Key countries |

US, China, Indonesia, Sri Lanka, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the Coconut Alcohol industry during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of industry companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -