Concierge Medicine Market Size 2026-2030

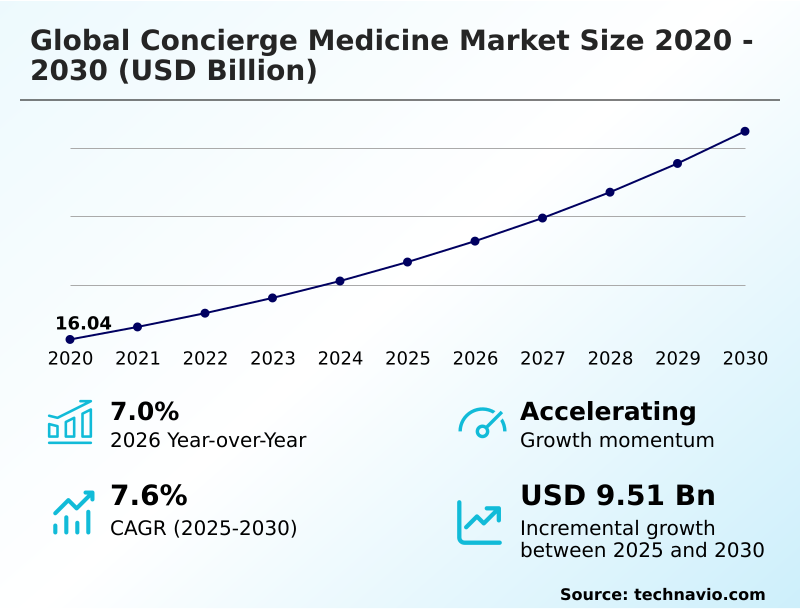

The concierge medicine market size is valued to increase by USD 9.51 billion, at a CAGR of 7.6% from 2025 to 2030. High prevalence of CVD will drive the concierge medicine market.

Major Market Trends & Insights

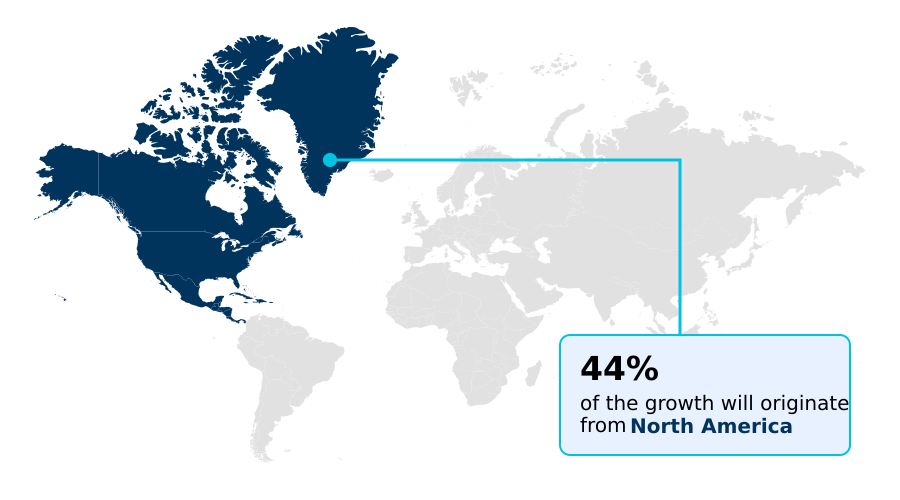

- North America dominated the market and accounted for a 43.6% growth during the forecast period.

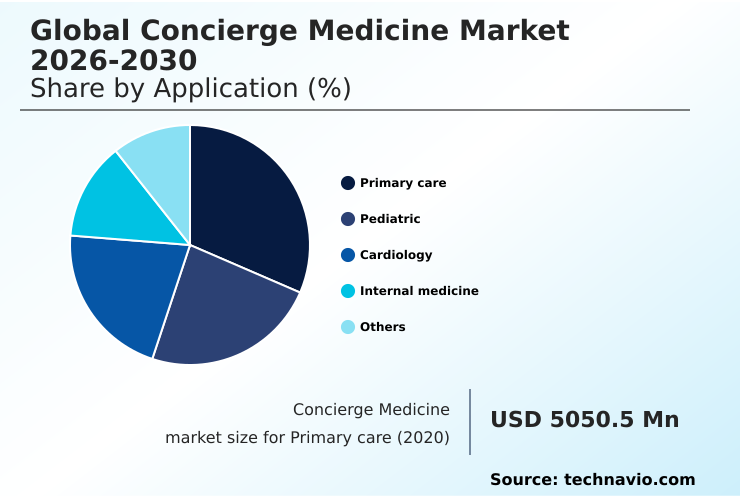

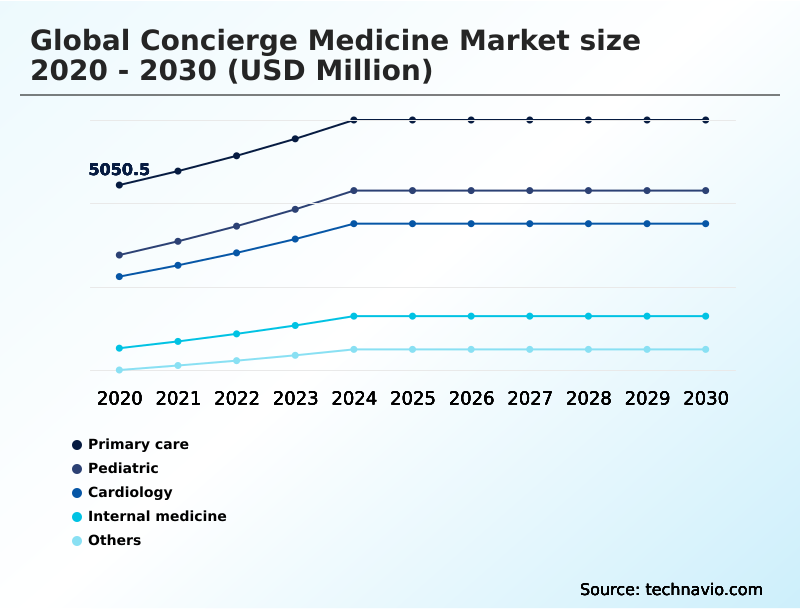

- By Application - Primary care segment was valued at USD 6.23 billion in 2024

- By Ownership - Group segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 15.14 billion

- Market Future Opportunities: USD 9.51 billion

- CAGR from 2025 to 2030 : 7.6%

Market Summary

- The concierge medicine market is defined by its shift away from transactional, volume-based healthcare toward a relationship-focused, membership-based framework. This model enables physicians to maintain significantly smaller patient panels, facilitating extended, in-depth consultations and 24/7 accessibility that are increasingly sought after by consumers. It prioritizes preventive care, personalized wellness strategies, and proactive management of chronic conditions.

- The expansion is no longer limited to general primary care; it now includes specialized fields like cardiology, pediatrics, and mental health, where continuous, coordinated oversight is crucial for optimal outcomes. For instance, corporations are integrating concierge services into executive benefits packages, ensuring leadership teams receive immediate medical attention to minimize health-related productivity disruptions.

- This approach not only improves patient satisfaction and health outcomes but also offers physicians a sustainable career path with greater clinical autonomy and reduced administrative burden. The integration of digital health tools, including telemedicine and remote monitoring, further enhances its value proposition by delivering a seamless, high-touch care experience that traditional systems struggle to replicate.

What will be the Size of the Concierge Medicine Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Concierge Medicine Market Segmented?

The concierge medicine industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Primary care

- Pediatric

- Cardiology

- Internal medicine

- Others

- Ownership

- Group

- Standalone

- End-user

- Individual

- Corporate organization

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Application Insights

The primary care segment is estimated to witness significant growth during the forecast period.

Primary care is the cornerstone of the concierge medicine market, functioning as a fee-for-service alternative that prioritizes proactive health management and a strong patient-physician relationship.

This retainer medicine model allows for unhurried consultations and deep dives into patient history, which is critical for effective wellness plan coordination. Practitioners serve as dedicated health advocacy services, offering personalized primary care that conventional systems cannot match.

The shift is driven by widespread dissatisfaction with impersonal, high-volume healthcare, leading to membership models that report over 50% higher patient retention.

By focusing on preventive health screenings and patient advocacy, these practices deliver a higher standard of continuous care, solidifying the segment's dominant market position through enhanced clinical autonomy.

The Primary care segment was valued at USD 6.23 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 43.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Concierge Medicine Market Demand is Rising in North America Get Free Sample

The market's geographic landscape is led by North America, which is projected to account for 43.6% of incremental growth, driven by high consumer demand for premium healthcare access and the prevalence of corporate wellness packages.

This region sees strong adoption of executive health programs and longevity medicine protocols. Europe follows as a mature market, with boutique medical practices gaining traction as an alternative to strained public systems.

However, the most rapid expansion is occurring in Asia, where a growing affluent class is fueling demand for specialized concierge services and virtual care integration.

In this region, telehealth consultations are bridging infrastructure gaps and expanding access to high-quality care, making it the fastest-growing market globally.

This global expansion is supported by subscription-based revenue models that offer financial stability for providers and predictable costs for members.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of concierge medicine is marked by its expanding applications and increasingly sophisticated business structures. The model's effectiveness in managing long-term health is evident in its use for concierge medicine for chronic conditions, where patient satisfaction rates are consistently higher compared to traditional care settings.

- This is particularly beneficial for concierge services for geriatric patients, who require more intensive oversight. On the corporate front, the ROI of employer-sponsored concierge health is becoming a key justification for corporate concierge health benefits, which are now a staple in executive retention strategies.

- A critical debate in the industry remains direct primary care vs concierge, with the latter offering a more comprehensive suite of services, including navigating specialist referrals in concierge care. Technology integration in concierge care is central to this differentiation, with platforms now incorporating robust data privacy in concierge health platforms.

- This has enabled the growth of specialized areas like concierge cardiology practice models and concierge medicine for mental health. For entrepreneurs, understanding the startup costs for a concierge practice and the viability of a hybrid concierge practice financial model is crucial.

- Key metrics like the concierge physician panel size impact directly influence service quality, while offerings like executive physicals in concierge medicine and wellness coaching in concierge medicine define the premium experience. Moreover, emerging concierge medicine and telehealth trends and options like concierge medicine for family plans are broadening market appeal, while comparing concierge medicine networks becomes essential for consumers.

- The cost structure, including pediatric concierge medicine cost, remains a key consideration for market penetration.

What are the key market drivers leading to the rise in the adoption of Concierge Medicine Industry?

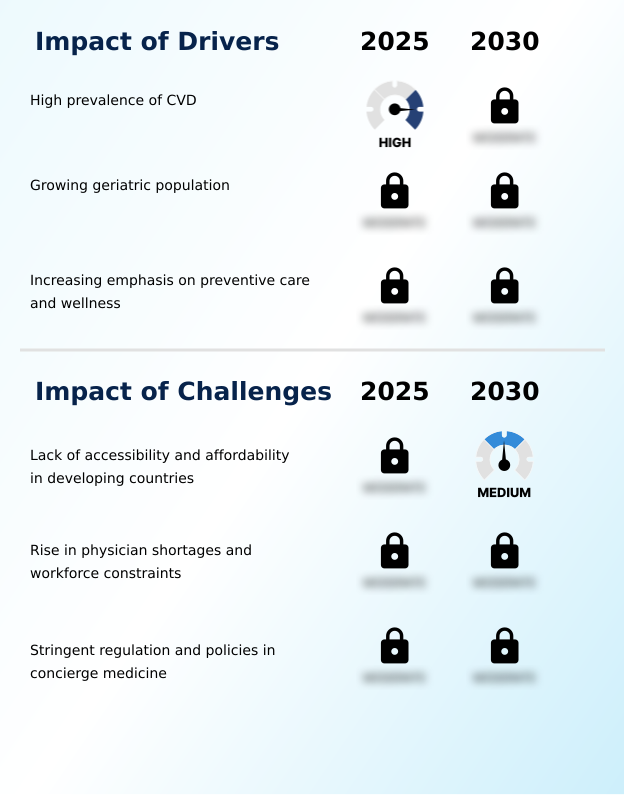

- The high global prevalence of cardiovascular diseases is a key driver for the market, as its management requires the continuous monitoring and proactive engagement inherent to the concierge model.

- Market growth is significantly driven by the increasing need for effective chronic disease management and a societal shift toward preventive wellness. The concierge model's structure, which allows for unhurried consultations and 24/7 physician availability, is ideal for managing complex conditions.

- This approach helps individuals achieve 35% higher adherence to preventive health screenings and wellness plan coordination.

- A key factor is the growing geriatric population, which benefits from the model's enhanced oversight and house call options; patients in this demographic often see a 20% reduction in avoidable hospital admissions.

- This value-based care transition also addresses systemic issues like physician burnout mitigation by offering practitioners greater clinical autonomy and a more sustainable work environment compared to high-volume, fee-for-service systems.

What are the market trends shaping the Concierge Medicine Industry?

- The integration of advanced technologies is transforming concierge medicine from a premium service into a proactive, data-rich health experience. This shift scales personalization while retaining direct physician access.

- Key market trends are centered on the fusion of technology and holistic health, creating a more responsive, high-touch care model. The adoption of AI-driven diagnostics and remote patient monitoring is enabling continuous health monitoring outside of clinical settings. This integrated care delivery approach, supported by advanced integrated digital health platforms, allows for proactive interventions.

- Holistic health services are becoming a standard offering, with medical service bundling now including services like genetic testing integration. Practices are leveraging on-demand medical services to provide immediate care, with some reporting up to a 40% reduction in administrative time due to AI-driven ambient listening tools.

- Furthermore, integrated wellness programs that track biometric data are demonstrating a 25% improvement in key health markers, showcasing the model's effectiveness in producing measurable outcomes.

What challenges does the Concierge Medicine Industry face during its growth?

- The lack of accessibility and affordability, particularly in developing nations, presents a significant challenge to market expansion, as the model relies on out-of-pocket spending and dense urban infrastructure.

- Key challenges center on affordability and accessibility, which temper market growth despite its benefits. The subscription-based revenue structure of the retainer medicine model creates a cost barrier, with membership fees representing over 70% of total healthcare spending for some patients, particularly in developing economies. This makes the fee-for-service alternative a more viable option for the majority.

- Furthermore, physician shortages are exacerbated as the model relies on limited patient panel sizes, which can increase wait times for non-members by up to 15% in certain areas. Providers are exploring hybrid concierge models to balance premium healthcare access with broader service availability.

- Navigating this landscape requires careful medical service navigation, as access to a preferred specialist network access is not always guaranteed, even within boutique medical practices.

Exclusive Technavio Analysis on Customer Landscape

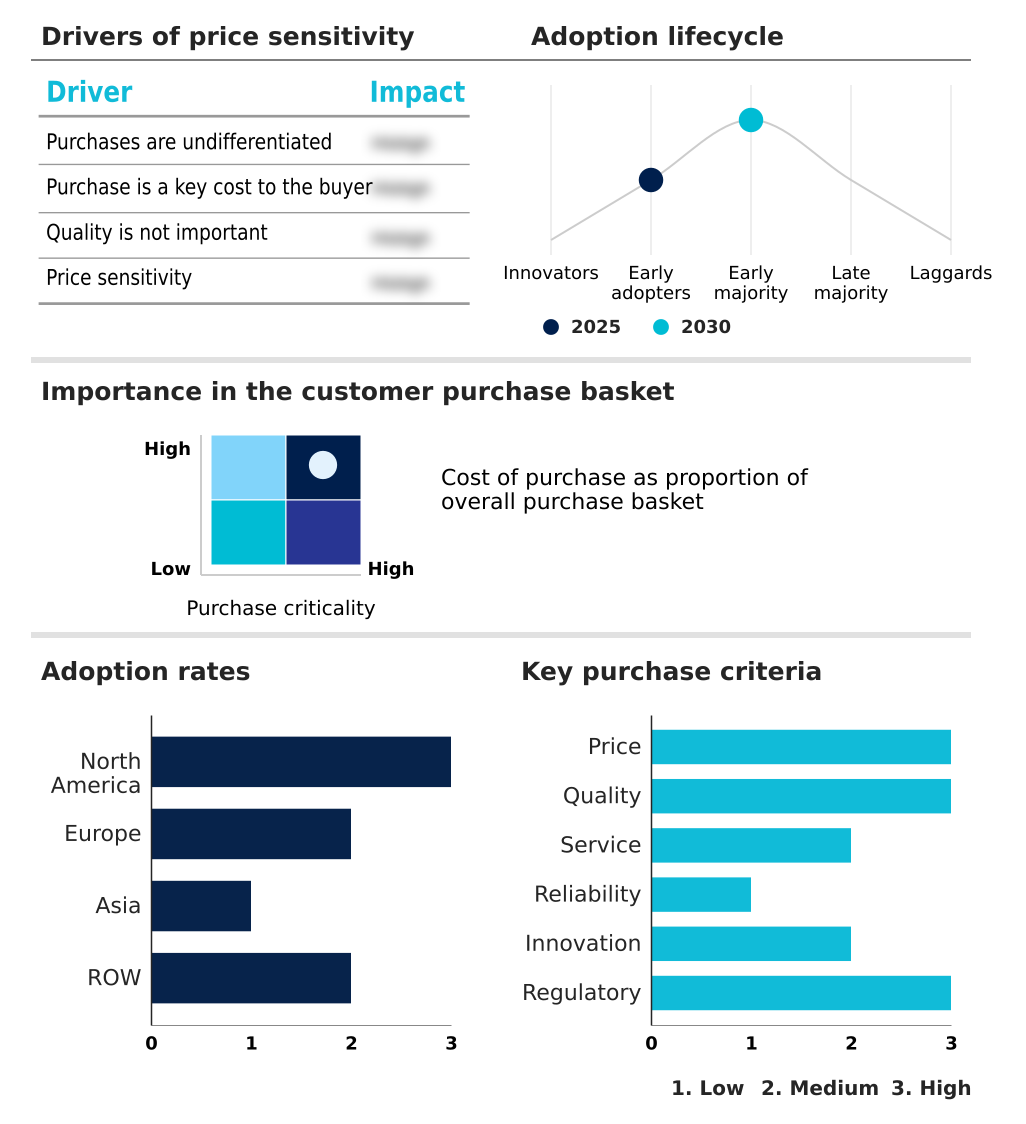

The concierge medicine market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the concierge medicine market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Concierge Medicine Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, concierge medicine market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

1Life Healthcare Inc. - Delivering personalized primary care through a national physician network, focused on preventive wellness programs and enhanced patient access beyond traditional insurance-based models.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 1Life Healthcare Inc.

- Atrium Health

- Baylor Scott and White Health

- Castle Connolly Health Partners

- Cedars Sinai Health System

- Concierge Choice Physicians

- Crossover Health

- Diamond Physicians

- MD2 International LLC.

- MDVIP Inc.

- PartnerMD LLC

- Peninsula Doctor

- PreferredMD Inc.

- Premise Health

- Privia Health Group Inc.

- SignatureMD Inc.

- Sollis Health

- Specialdocs Consultants LLC

- The Cleveland Clinic Foundation

- WorldClinic

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Concierge medicine market

- In January, 2025, 1Life Healthcare Inc. announced a strategic partnership with Montefiore Health System to coordinate primary and specialty care in New York, integrating its membership-based model with a large hospital network.

- In February, 2026, MDVIP Inc. celebrated its 100th consecutive quarter of growth and established a new corporate headquarters in Florida to support its expanding network of over one thousand four hundred physicians.

- In January, 2026, Crossover Health and Premise Health entered into a definitive agreement to merge, creating a unified entity that serves millions of members and accelerates the development of advanced primary health models for employers.

- In 2025, Sollis Health expanded its footprint by launching a new facility in San Francisco, designed to provide its members with 24-hour emergency-level care without traditional hospital wait times.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Concierge Medicine Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 286 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.6% |

| Market growth 2026-2030 | USD 9510.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.0% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Thailand, Indonesia, Brazil, Argentina, Saudi Arabia, UAE, Colombia, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The concierge medicine market is fundamentally reshaping the patient-physician relationship through its retainer medicine model, which grants direct physician access and fosters clinical autonomy. This membership-based healthcare structure enables internal medicine specialists and other providers to offer a high-touch care model with limited patient panels, ensuring comprehensive, personalized primary care.

- Central to its value are proactive health management and rigorous preventive health screenings, which are critical for effective chronic disease management. The integration of advanced diagnostic tools and AI-driven diagnostics is becoming standard, with recent figures indicating that 66% of physicians now use AI, a statistic influencing boardroom decisions on technology investments.

- Providers increasingly serve as health advocacy services, offering medical service navigation and wellness plan coordination. The model supports virtual care integration and remote patient monitoring, expanding into specialized concierge services like executive health programs and cutting-edge longevity medicine protocols, all sustained by a predictable subscription-based revenue stream that defines its departure from traditional fee-for-service care.

What are the Key Data Covered in this Concierge Medicine Market Research and Growth Report?

-

What is the expected growth of the Concierge Medicine Market between 2026 and 2030?

-

USD 9.51 billion, at a CAGR of 7.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Primary care, Pediatric, Cardiology, Internal medicine, and Others), Ownership (Group, and Standalone), End-user (Individual, and Corporate organization) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

High prevalence of CVD, Lack of accessibility and affordability in developing countries

-

-

Who are the major players in the Concierge Medicine Market?

-

1Life Healthcare Inc., Atrium Health, Baylor Scott and White Health, Castle Connolly Health Partners, Cedars Sinai Health System, Concierge Choice Physicians, Crossover Health, Diamond Physicians, MD2 International LLC., MDVIP Inc., PartnerMD LLC, Peninsula Doctor, PreferredMD Inc., Premise Health, Privia Health Group Inc., SignatureMD Inc., Sollis Health, Specialdocs Consultants LLC, The Cleveland Clinic Foundation and WorldClinic

-

Market Research Insights

- Market dynamics are increasingly shaped by corporate adoption and technological integration, moving beyond individual memberships. Data shows that employer-sponsored memberships now account for 58% of enrollees in certain direct primary care models, highlighting a strategic shift in corporate wellness packages to ensure premium healthcare access for key personnel.

- This trend is complemented by rapid technology adoption; approximately 66% of physicians have integrated artificial intelligence into their practices, using it for tasks from diagnostic support to administrative automation. This synergy of employer funding and advanced technology is making boutique medical practices more scalable and financially viable.

- The fee-for-service alternative is proving its value by offering enhanced care coordination services and mitigating physician burnout, thereby attracting more practitioners to these innovative membership models.

We can help! Our analysts can customize this concierge medicine market research report to meet your requirements.

RIA -

RIA -