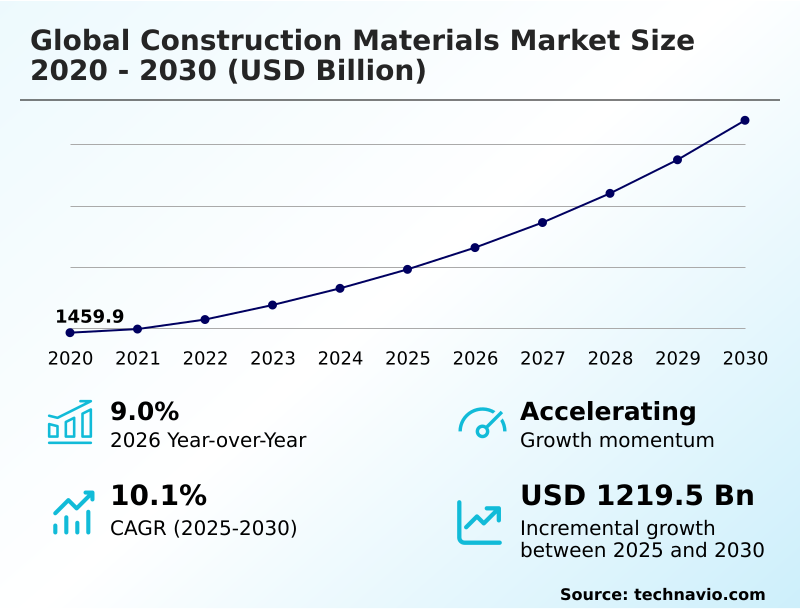

Construction Materials Market Size 2026-2030

The construction materials market size is valued to increase by USD 1219.5 billion, at a CAGR of 10.1% from 2025 to 2030. Increasing number of smart cities will drive the construction materials market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 43.7% growth during the forecast period.

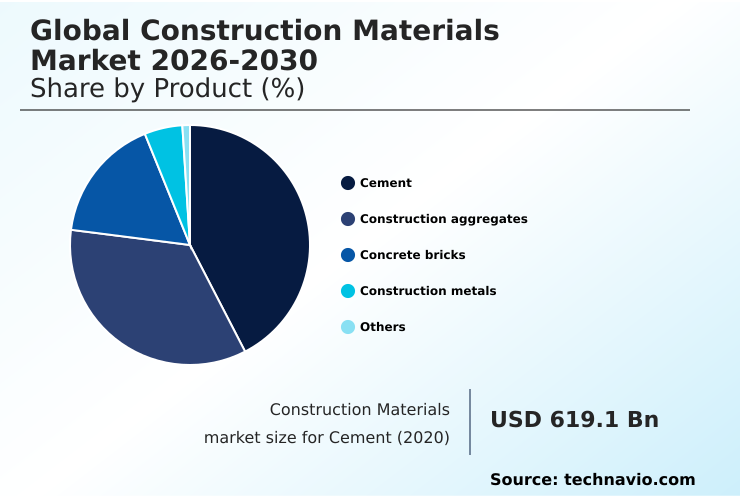

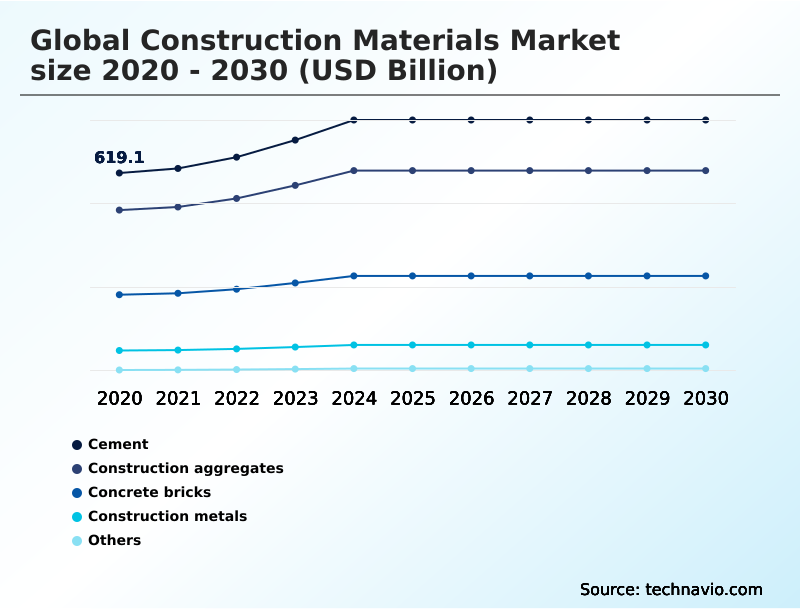

- By Product - Cement segment was valued at USD 781.7 billion in 2024

- By End-user - Commercial segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1737.6 billion

- Market Future Opportunities: USD 1219.5 billion

- CAGR from 2025 to 2030 : 10.1%

Market Summary

- The construction materials market is foundational to global economic development, driven by rapid urbanization, population growth, and extensive government investment in infrastructure. A significant shift toward sustainability is reshaping the industry, with stringent environmental regulations and green building standards compelling a move from traditional materials to innovative, low-carbon alternatives.

- This has spurred the development of eco-friendly products like low-carbon cement, recycled construction materials, and engineered wood, which are increasingly specified to meet green building certifications.

- For instance, a contractor managing a large-scale urban development project must now navigate complex supply chains to source materials that not only meet structural requirements but also comply with embodied carbon limits, impacting procurement strategies and project costs.

- Technological advancements, particularly Building Information Modeling (BIM) and material science innovations such as self-healing concrete, are further enhancing efficiency, optimizing resource usage, and positioning the construction materials market for continued, albeit more complex, evolution.

What will be the Size of the Construction Materials Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Construction Materials Market Segmented?

The construction materials industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Cement

- Construction aggregates

- Concrete bricks

- Construction metals

- Others

- End-user

- Commercial

- Industrial

- Residential

- Distribution channel

- Direct sales

- Distributors

- Online retail

- Specialty stores

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Product Insights

The cement segment is estimated to witness significant growth during the forecast period.

The cement segment is undergoing a significant transformation, driven by a focus on circular economy principles and stricter environmental regulations.

Demand is shifting from traditional formulations toward low-carbon cement and portland-limestone cement, which utilize supplementary cementitious materials to achieve embodied carbon reduction. This evolution, crucial for meeting net-zero building goals, requires a rigorous lifecycle assessment for new products.

Innovations in this area, while distinct from green steel production, are vital for developing the next generation of high-performance concrete.

The adoption of these advanced cementitious solutions now accounts for over 20% of material specifications in new urban infrastructure projects, demonstrating a clear market pivot toward sustainability and advanced material science, including building-integrated photovoltaics and smart glass technology.

The Cement segment was valued at USD 781.7 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 43.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Construction Materials Market Demand is Rising in APAC Get Free Sample

The global construction materials market is geographically dominated by the APAC region, which accounts for over 43% of the incremental growth, driven by rapid urbanization and massive infrastructure spending in countries like China and India.

This region exhibits a high-volume demand for traditional products like structural steel and materials for high-performance concrete, but there is also a discernible shift toward sustainable solutions like engineered wood products.

In contrast, the mature markets of North America and Europe, which contribute a combined share of over 42% to market expansion, focus on high-value renovation and retrofitting.

These regions prioritize advanced building composites and structural insulated panels to meet stringent green building certification requirements.

The adoption of prefabricated components in Europe has been shown to reduce on-site waste by up to 25%, reflecting a strong commitment to circular economy principles.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the global construction materials market increasingly requires a deep understanding of specific material performance and economic trade-offs. For example, the impact of green steel on construction costs is a critical variable for developers of large-scale commercial projects, as initial premium pricing must be weighed against long-term sustainability benefits and regulatory compliance.

- Similarly, evaluating the performance of bio-based insulation in cold climates is essential for residential builders aiming to meet stringent energy efficiency standards. A comprehensive lifecycle analysis of recycled aggregates in concrete helps infrastructure planners meet circular economy targets, with some studies showing it can reduce the need for virgin materials by up to 25% without compromising structural integrity.

- Further advancements in 3d printed construction materials are poised to disrupt traditional building timelines, while the role of fiber-reinforced polymers in retrofitting aging infrastructure offers a cost-effective alternative to complete replacement. These nuanced considerations are reshaping how firms approach material selection, procurement, and project design.

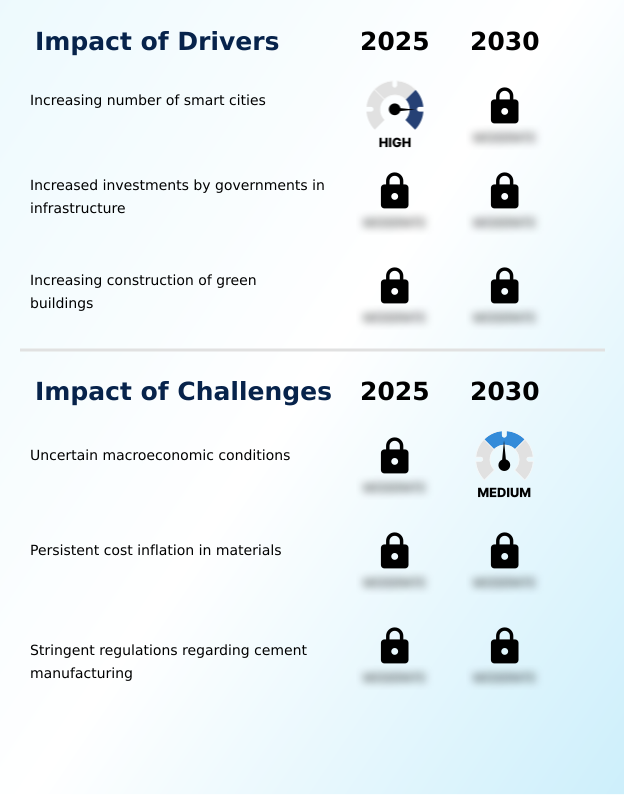

What are the key market drivers leading to the rise in the adoption of Construction Materials Industry?

- The increasing development of smart cities worldwide is a significant driver, fueling demand for innovative and technologically integrated construction materials.

- Market growth is significantly propelled by government-led infrastructure modernization and the global push for sustainable urban development.

- Investments in public works are fueling demand for foundational products like structural steel and precast concrete elements, with spending in some emerging economies increasing by over 10% annually.

- The rise of smart cities necessitates the use of advanced materials, including those for building-integrated photovoltaics and intelligent structural monitoring. Green building initiatives are also a major driver, increasing the specification of autoclaved aerated concrete and cross-laminated timber.

- The demand for materials that support decarbonization, such as those used in green steel production and low-carbon cement formulations, is accelerating.

- This dynamic environment is creating substantial opportunities for suppliers of innovative and eco-efficient building solutions, such as fly ash bricks.

What are the market trends shaping the Construction Materials Industry?

- The adoption of advanced technologies to enhance operational efficiency and productivity is a prominent trend shaping the market. This includes digitalization, automation, and innovative data management solutions to address long-standing industry challenges.

- The market is undergoing a significant transformation driven by the adoption of innovative products and processes. There is a strong trend toward using lightweight materials such as lightweight concrete blocks and advanced building composites to reduce structural loads and enhance design flexibility.

- The use of recycled aggregates and other recycled construction materials is becoming mainstream, with adoption rates increasing by over 15% in regulated markets. Technologies like building information modeling are optimizing material usage, while the demand for high-performance concrete and engineered wood products grows.

- Innovations in smart glass technology and low-emissivity coatings are improving energy efficiency in commercial buildings, and the adoption of geosynthetic materials is enhancing infrastructure resilience. This evolution reflects a broader industry shift toward materials that deliver superior performance, efficiency, and sustainability.

What challenges does the Construction Materials Industry face during its growth?

- Uncertain macroeconomic conditions, including slowing economic growth and high inflation, present a key challenge that can impede market growth by delaying projects.

- The market faces significant hurdles from persistent cost inflation and supply chain volatility, which have increased the price of key inputs like high-strength steel alloys and portland-limestone cement by over 20% in recent periods. Uncertain macroeconomic conditions are delaying project financing, while stringent regulations on cement manufacturing add compliance burdens.

- The industry must also contend with the complexities of integrating modern methods of construction and ensuring material traceability solutions across fragmented supply networks. The initial high cost of adopting innovative materials such as self-healing concrete and fiber-reinforced polymers presents a barrier for some contractors.

- Furthermore, the operational shifts required for off-site manufacturing and the use of structural insulated panels challenge traditional business models, creating a complex operating environment.

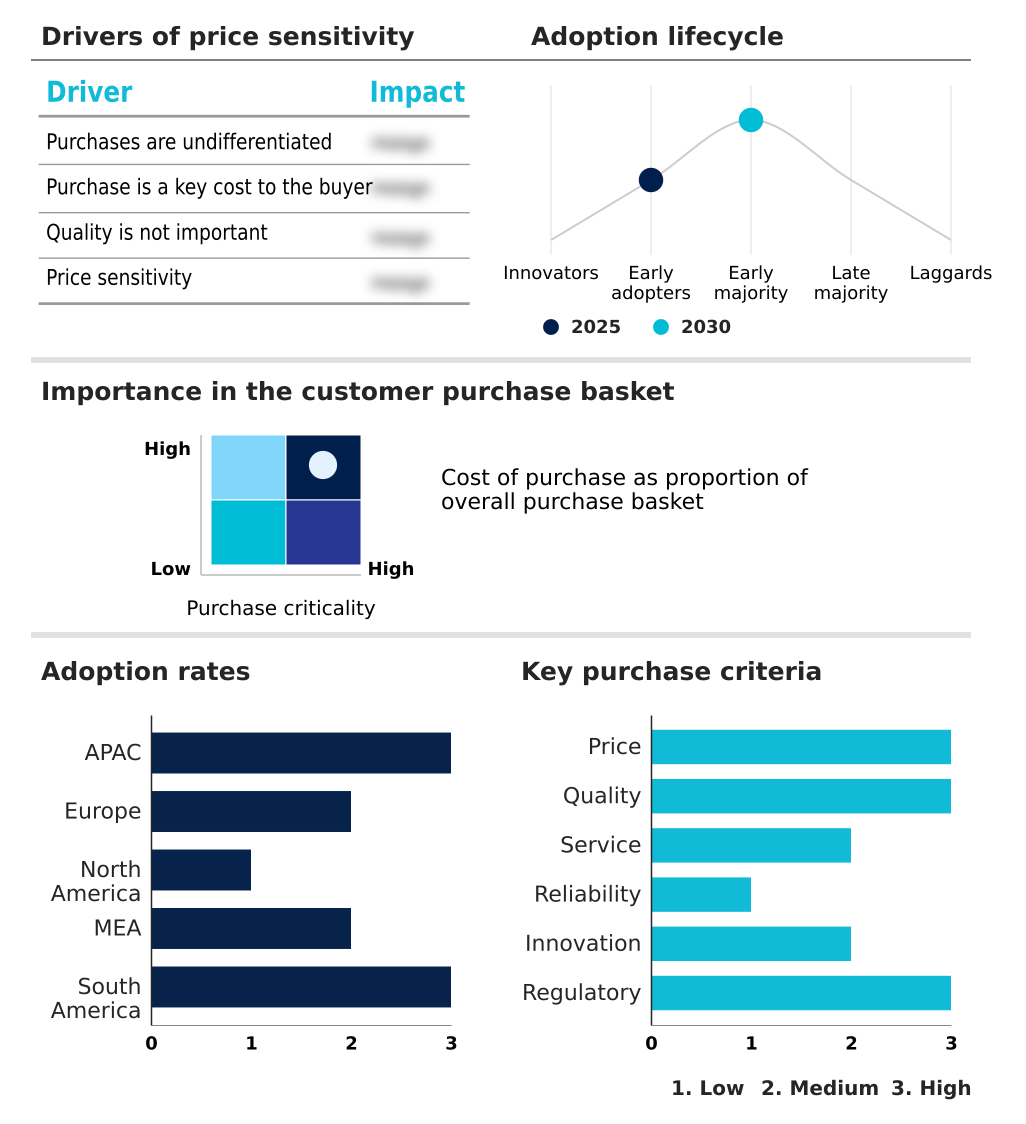

Exclusive Technavio Analysis on Customer Landscape

The construction materials market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the construction materials market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Construction Materials Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, construction materials market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ambuja Cements Ltd. - Key offerings include a diverse portfolio of cement and clinker for domestic and export markets, featuring specialized products for high-strength and dense concrete applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ambuja Cements Ltd.

- ArcelorMittal SA

- Boral Ltd.

- Buzzi S.p.A.

- Compagnie de Saint Gobain SA

- CRH Plc

- EUROCEMENT Group

- Everest Industries Ltd.

- Forterra Building Products Ltd.

- Grasim Industries Ltd.

- Heidelberg Materials AG

- Holcim Ltd.

- INTERCEMENT PARTICIPACOES SA

- JK Cement Ltd

- Knauf Digital GmbH

- LIXIL Corp.

- Sika AG

- Taiwan Cement Corp

- UltraTech Cement Ltd.

- Vicat

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Construction materials market

- In September 2025, CRH Plc completed its acquisition of Eco Material Technologies, a leading supplier of supplementary cementitious materials, to bolster its portfolio of low-carbon solutions for the North American construction market.

- In June 2025, Compagnie de Saint Gobain SA acquired Maturix, a technology firm specializing in wireless sensors for real-time concrete curing monitoring, to integrate into its digital platform for construction chemicals.

- In February 2025, Holcim Ltd. announced the launch of its ECOPact Prime series, a new range of low-carbon concrete that reduces CO2 emissions by up to 50% compared to standard concrete, targeting green building projects.

- In November 2024, ArcelorMittal SA entered a strategic partnership with a renewable energy provider to power its European steel mills, advancing its objective of large-scale green steel production for the construction industry.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Construction Materials Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 309 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10.1% |

| Market growth 2026-2030 | USD 1219.5 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.0% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The construction materials market is defined by a crucial pivot toward sustainable and high-performance solutions. The industry is moving beyond conventional products to adopt innovative materials such as low-carbon cement, recycled aggregates, and cross-laminated timber. This transition is driven by stringent environmental regulations and the need for greater efficiency in construction.

- For boardroom-level strategy, the focus has shifted to integrating materials like autoclaved aerated concrete and high-performance concrete to meet green building standards. The adoption of supplementary cementitious materials and portland-limestone cement is becoming widespread. Companies are also exploring advanced building composites and engineered wood products. Innovations such as self-healing concrete and fiber-reinforced polymers are gaining traction for specialized applications.

- The push for decarbonization is accelerating green steel production and the use of structural insulated panels. Modular construction components and lightweight concrete blocks are key to improving on-site productivity, with some firms achieving a 20% reduction in assembly time. Materials like fly ash bricks, low-emissivity coatings, and high-strength steel alloys are also becoming standard.

- The development of smart glass technology and building-integrated photovoltaics further underscores the market's technological evolution, involving geosynthetic materials and precast concrete elements.

What are the Key Data Covered in this Construction Materials Market Research and Growth Report?

-

What is the expected growth of the Construction Materials Market between 2026 and 2030?

-

USD 1219.5 billion, at a CAGR of 10.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Cement, Construction aggregates, Concrete bricks, Construction metals, and Others), End-user (Commercial, Industrial, and Residential), Distribution Channel (Direct sales, Distributors, Online retail, and Specialty stores) and Geography (APAC, Europe, North America, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing number of smart cities, Uncertain macroeconomic conditions

-

-

Who are the major players in the Construction Materials Market?

-

Ambuja Cements Ltd., ArcelorMittal SA, Boral Ltd., Buzzi S.p.A., Compagnie de Saint Gobain SA, CRH Plc, EUROCEMENT Group, Everest Industries Ltd., Forterra Building Products Ltd., Grasim Industries Ltd., Heidelberg Materials AG, Holcim Ltd., INTERCEMENT PARTICIPACOES SA, JK Cement Ltd, Knauf Digital GmbH, LIXIL Corp., Sika AG, Taiwan Cement Corp, UltraTech Cement Ltd. and Vicat

-

Market Research Insights

- The market is shaped by a strategic push toward modern methods of construction, where digital procurement platforms and off-site manufacturing are becoming standard. This shift drives efficiency, with projects adopting prefabricated building systems reporting construction timeline reductions of up to 30%. Concurrently, an emphasis on resilient infrastructure design is increasing the use of materials that meet stringent seismic retrofitting standards.

- Material traceability solutions are also gaining traction, offering greater transparency and improving supply chain integrity by over 15% in certain applications. The adoption of automated construction robotics and advanced material science is pivotal as the industry addresses persistent labor shortages and strives for higher productivity.

We can help! Our analysts can customize this construction materials market research report to meet your requirements.

RIA -

RIA -