Content Protection Market Size 2024-2028

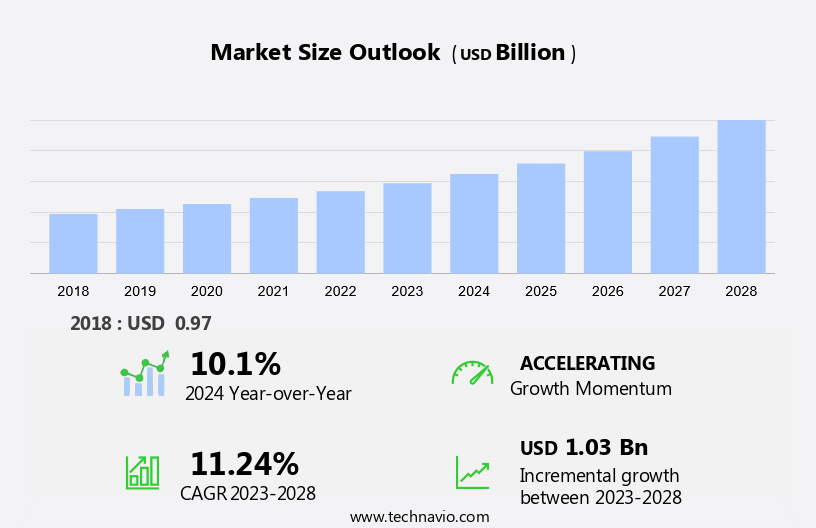

The content protection market size is forecast to increase by USD 1.03 billion at a CAGR of 11.24% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing adoption of digital content in various industries, including healthcare and corporate sectors. With the rise of streaming platforms and expansive digital libraries, the infrastructure required for content protection has become increasingly complex. This complexity introduces new challenges, such as the threat of ransomware incidents, data theft, and copyright infringement. As the number of cyber threats continues to grow, the importance of these strong solutions, enhanced by IoT and artificial intelligence, becomes more evident. Movies and TV shows are prime targets for piracy, with AI-driven security systems helping to detect and prevent unauthorized access, while IoT-enabled devices ensure real-time monitoring. This escalating threat leads to significant financial losses for content creators and distributors. Moreover, it also explores potential failures during implementation and the consequences that can result. By understanding these factors, businesses can make informed decisions about the solutions they adopt to safeguard their digital assets.

What will be the Size of the Market During the Forecast Period?

- The market is a critical segment in the digital business arena, as the proliferation of digital content and the increasing threat of unauthorized access pose significant challenges for content creators and owners. The protection of digital rights, intellectual property, and sensitive data is paramount in today's digital economy. Content protection, a fundamental aspect of digital security, encompasses various strategies and technologies aimed at securing digital content from unauthorized access, copying, tampering, and sharing. Digital Rights Management (DRM) policies are a key component of content protection, enabling content creators and owners to control access to their digital assets and monetize them effectively.

- Digital content, in its various forms, is a valuable asset for businesses. Intellectual property, including text, images, audio, and video, is a significant investment for content creators and owners. Unauthorized access, copying, or sharing can lead to substantial financial losses and reputational damage. To mitigate these risks, these solutions employ encryption, rendering digital content in an unreadable format for unauthorized users. Advanced algorithms and cryptographic keys are used to ensure that only authorized users can access and decrypt the content. Digital watermarking, both visible and invisible, is another effective strategy for proving ownership and tracking content distribution.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Large enterprise

- Small

- medium enterprise

- Type

- Conditional access systems

- Digital rights management

- Digital watermarking

- Others

- Geography

- North America

- Canada

- US

- Europe

- UK

- France

- APAC

- China

- South America

- Middle East and Africa

- North America

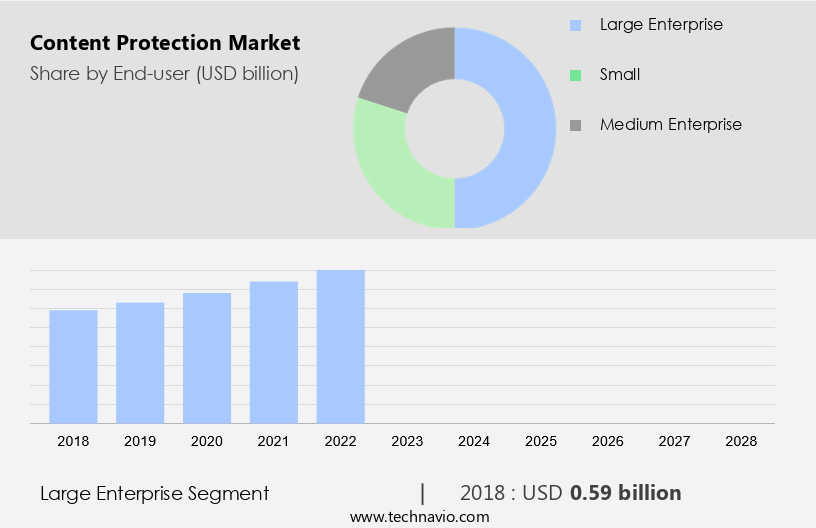

By End-user Insights

- The large enterprise segment is estimated to witness significant growth during the forecast period.

In today's business landscape, large enterprises are leading the charge in the market. The increasing generation of content within organizations necessitates a more adaptable and expansive approach to content protection. By implementing these solutions, businesses can efficiently manage and secure their digital assets, enabling them to expand or contract their protection measures as required. Moreover, the heightened threat of data breaches and cyber-attacks has intensified the importance of strong content protection. Content protection offers encryption techniques, such as algorithms and cryptographic keys, to ensure authorized users have access while keeping the content unreadable for unauthorized individuals. Decryption keys are provided to authorized users, allowing them to access the content while maintaining the integrity of the original data. As the need for advanced security measures continues to grow, content protection will remain a vital investment for large enterprises in safeguarding their future projects and valuable intellectual property.

Get a glance at the market report of share of various segments Request Free Sample

The Large enterprise segment was valued at USD 0.59 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

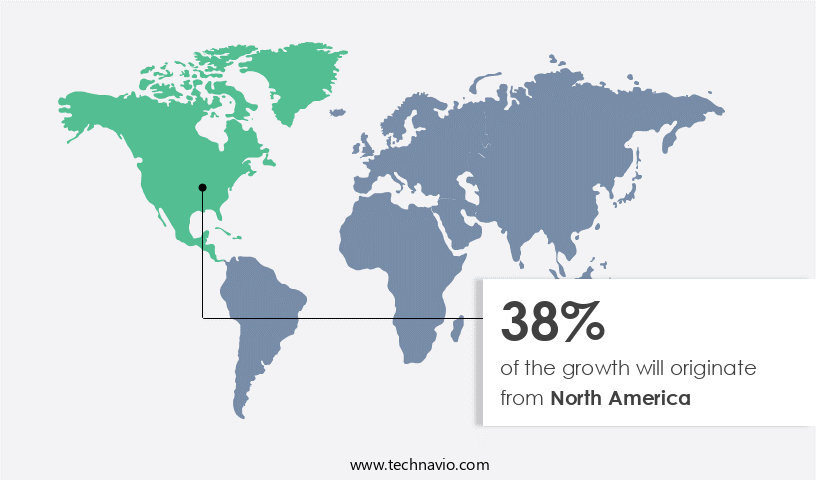

- North America is estimated to contribute 38% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The market represents a substantial share due to the integration of advanced technologies like automation, cloud solutions, and virtualization. The digital transformation of businesses, particularly those in remote locations, and the rising adoption of these systems among local enterprises are key growth drivers for the market in this region. The adoption of cloud-based technologies and virtualization in North America is motivating businesses to implement these solutions to secure their digital assets. Companies are increasingly utilizing cloud services for data storage and content processing, making it crucial to safeguard their intellectual property. Zero Trust architecture, continuous authentication, scalability, and flexibility are essential features that organizations seek in content protection platforms.

Multi DRM solutions cater to the needs of streaming services and various devices. Watermarking technologies ensure content traceability and integrity. These solutions enable businesses to secure their digital content, maintain data privacy, and comply with industry regulations.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of the Content Protection Market?

An increase in the adoption of content among various industries is the key driver of the market.

- Content protection has emerged as a vital component in the business landscape, particularly in sectors like IT and finance, as the importance of securing digital content and intellectual property becomes increasingly apparent. The market is experiencing significant growth due to the escalating number of cyber threats and data breaches. Unauthorized access to digital content poses a significant risk for businesses, and these solutions are essential for preventing copying, tampering, and piracy. Digital rights management (DRM) policies are a popular approach to content protection, employing encryption, algorithms, and cryptographic keys to secure content and restrict access to authorized users. Digital watermarking, both visible and invisible, is another effective strategy for proving ownership and tracking content distribution, discouraging unauthorized sharing.

- With the popularity of online streaming services, the demand for content protection solutions has risen. Zero Trust architecture, continuous authentication, and scalability are key features of modern content protection platforms. Businesses in media and entertainment, education, healthcare, and corporate sectors are increasingly relying on Multi DRM solutions to secure their digital content and sensitive data. The future lies in advanced technologies like blockchain, which offers immutable records and transparency, instilling trust and transparency in transactions. Content creators and owners can monetize their future projects and protect their intellectual property with these strong protection measures. The increasing prevalence of cyberattacks, data breaches, ransomware incidents, and copyright infringement underscores the need for effective solutions.

What are the market trends shaping the Content Protection Market?

A rise in the number of cyber threats is the upcoming trend in the market.

- In the digital age, content protection has emerged as a critical concern for businesses and content creators alike. Unauthorized access to digital content, intellectual property, and sensitive data pose significant risks, leading to financial losses, reputational damage, and legal issues. The market solutions, such as digital rights management (DRM), encryption, and digital watermarking, offer effective measures to secure digital content and deter unauthorized copying, tampering, and sharing. DRM policies help control access to digital content, ensuring that only authorized users possess decryption keys. Encryption algorithms and cryptographic keys play a crucial role in protecting data from unauthorized access and virus attacks.

- Digital watermarking, whether visible or invisible, can help prove ownership and track content distribution, discouraging unauthorized sharing. Businesses in various sectors, including media and entertainment, education, healthcare, and corporate sectors, are increasingly adopting the measures to safeguard their digital assets. The popularity of online streaming services and the rise in demand for remote work have further accentuated the need for strong content security. Zero Trust architecture, continuous authentication, scalability, and flexibility are essential features of modern content protection platforms. Multi DRM solutions cater to the diverse needs of streaming services and devices. Watermarking technologies help prevent piracy, a significant source of leaks, and protect the revenue streams of content creators and owners.

What challenges does the Content Protection Market face during the growth?

The possibility of failure during implementation is a key challenge affecting the market growth.

- The market is a critical segment in the digital landscape, focusing on safeguarding digital content and sensitive data from unauthorized access and intellectual property theft. Content security solutions encompass digital rights management (DRM) policies, encryption, algorithms, and cryptographic keys to ensure authorized users have access to content while discouraging unauthorized copying, tampering, and sharing. Businesses across various sectors, including media and entertainment, education, healthcare, and corporate sectors, are increasingly relying on content protection to monetize their future projects and protect their intellectual property. The popularity of online streaming services has led to a rise in demand for content protection measures due to the rising threat of cyberattacks, data breaches, and online piracy.

- Zero Trust architecture, continuous authentication, scalability, and flexibility are essential features of modern content protection solutions. Multi DRM solutions cater to the needs of various platforms and devices, while watermarking technologies offer visible and invisible options for proving ownership and tracking content distribution. Despite the benefits, implementation of content protection solutions can be complex and time-consuming. Service providers must manage various processes, including project management, vulnerability management, compliance, content management, event monitoring, and access management, to ensure flawless execution. The planning phase requires careful consideration of device configurations and their integration into an organization's network infrastructure. Content protection remains a crucial investment for businesses seeking to protect their digital assets and maintain trust with their customers.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adobe Inc.

- Alphabet Inc.

- Axinom GmbH

- Cisco Systems Inc.

- CommScope Holding Co. Inc.

- Digimarc Corp.

- EZDRM Inc.

- Friend MTS Ltd.

- Intel Corp.

- Intertrust Technologies Corp.

- Kudelski SA

- Locklizard Ltd.

- Microsoft Corp.

- NASPERS Ltd.

- RGB Spectrum

- Sony Group Corp.

- STMicroelectronics International N.V.

- Verance Corp.

- Verimatrix Inc.

- Wellav Technologies Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is a critical response to the growing demand for safeguarding digital content from unauthorized access and misuse. Content protection refers to the measures taken to secure digital rights management (DRM) for intellectual property and sensitive data. This includes encryption, algorithms, and cryptographic keys to ensure authorized users have access while discouraging unauthorized copying, tampering, and sharing. Digital content creators and owners seek to monetize their projects and protect future works from piracy and cyberattacks. The rise in remote work and online streaming services has led to a rise in demand for content protection solutions. Businesses in media and entertainment, education, healthcare, and corporate sectors are particularly vulnerable to data breaches and copyright infringement.

Furthermore, digital watermarking, both visible and invisible, is a popular content protection technique, proving ownership and tracking content distribution. Zero trust architecture, continuous authentication, and scalable multi-DRM solutions offer flexibility and protection for platforms, devices, and streaming services. Blockchain technology provides immutable records, transparency, and trust for content transactions. Content protection is essential in preventing the spread of viruses, ransomware incidents, and data theft. As the popularity of online streaming services grows, so does the need for strong protection measures. Content protection is a vital investment for businesses and individuals alike, ensuring the security and integrity of their digital assets.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

164 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 11.24% |

|

Market Growth 2024-2028 |

USD 1.03 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

10.1 |

|

Key countries |

US, Canada, China, UK, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -