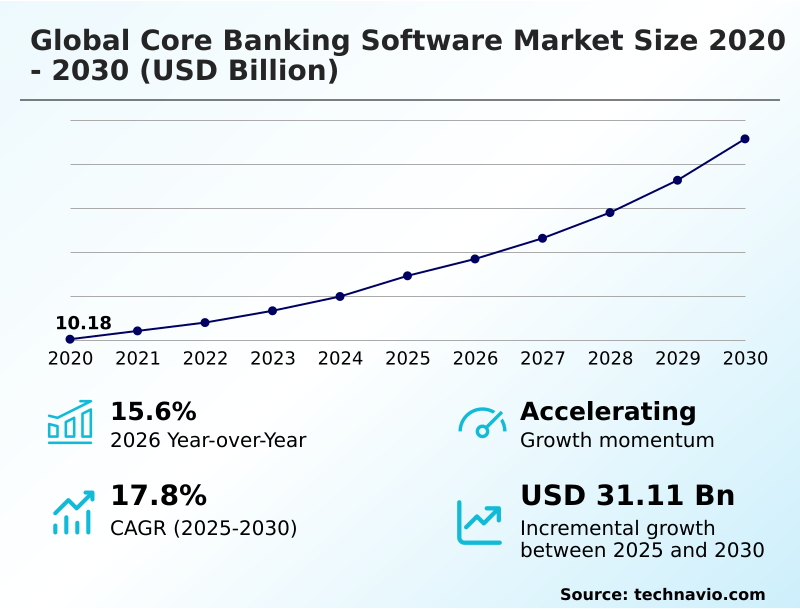

Core Banking Software Market Size 2026-2030

The core banking software market size is valued to increase by USD 31.11 billion, at a CAGR of 17.8% from 2025 to 2030. Accelerated integration of generative AI into core financial workflows will drive the core banking software market.

Major Market Trends & Insights

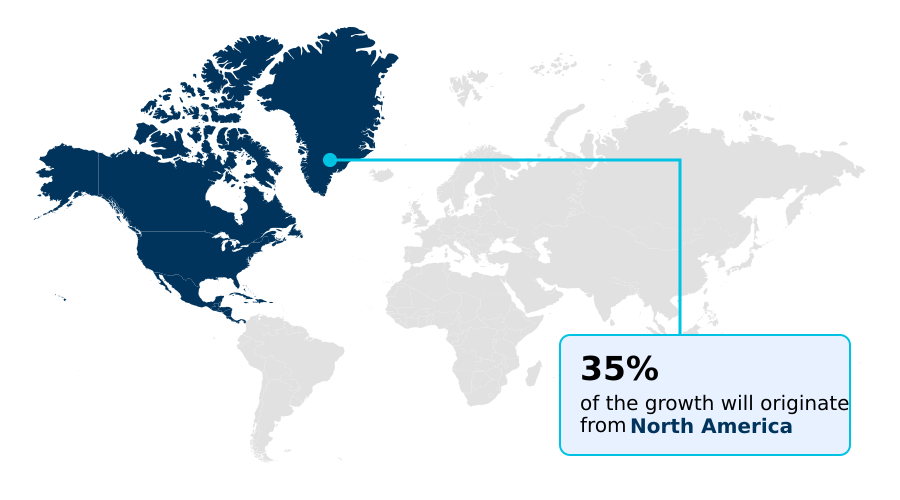

- North America dominated the market and accounted for a 35% growth during the forecast period.

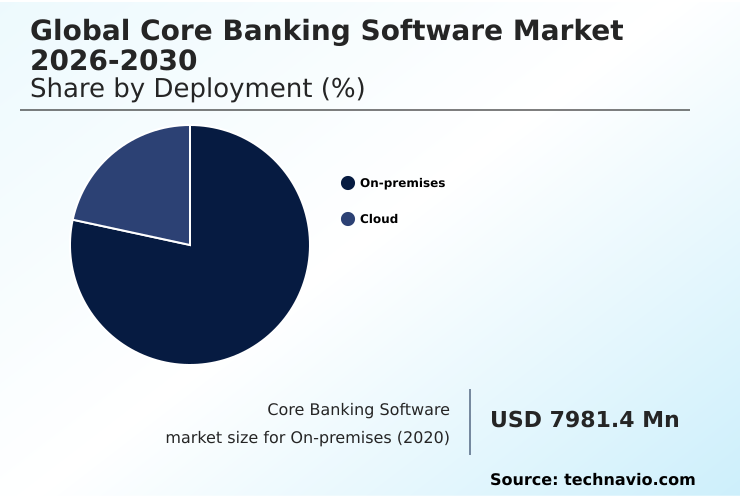

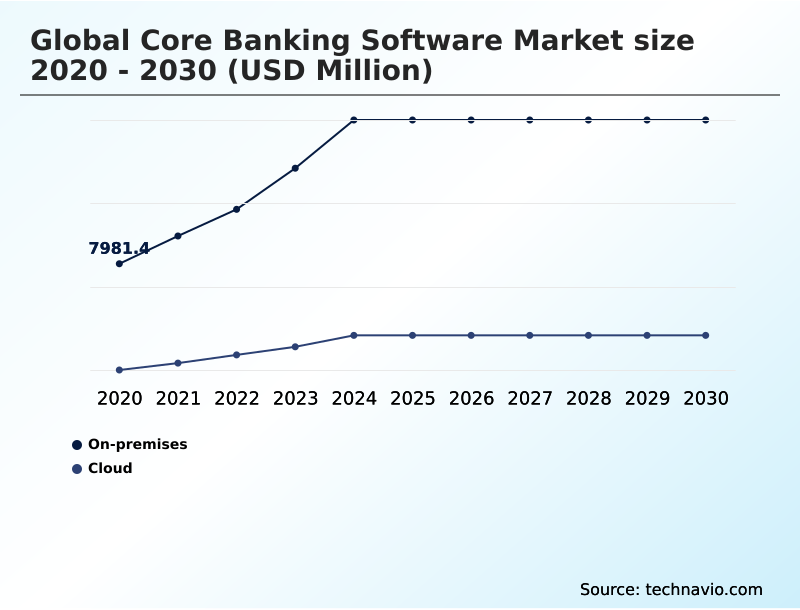

- By Deployment - On-premises segment was valued at USD 15.80 billion in 2024

- By End-user - Banks segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 45.52 billion

- Market Future Opportunities: USD 31.11 billion

- CAGR from 2025 to 2030 : 17.8%

Market Summary

- The core banking software market is undergoing a fundamental transformation as financial institutions move away from rigid, monolithic legacy systems toward more agile solutions. This shift is driven by the need to meet evolving customer expectations for digital services and to enhance operational efficiency.

- Modern platforms are increasingly built on a cloud-native core banking framework and feature an API-first architecture, enabling seamless fintech ecosystem integration and participation in the open banking ecosystem. A key business application is the optimization of lending processes, where automated loan origination and dynamic credit scoring algorithms can reduce approval times from days to hours, a critical competitive advantage.

- The adoption of microservices-based platforms allows banks to update specific functionalities, such as payment processing systems or compliance reporting modules, without overhauling their entire infrastructure.

- This modularity not only accelerates digital transformation in banking but also provides the scalable banking infrastructure needed to support real-time transaction processing and customer experience personalization, ensuring banks remain competitive in a rapidly changing financial landscape.

What will be the Size of the Core Banking Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Core Banking Software Market Segmented?

The core banking software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- On-premises

- Cloud

- End-user

- Banks

- Financial institutions

- Solution

- Retail banking core

- Commercial banking core

- Wealth and treasury management

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By Deployment Insights

The on-premises segment is estimated to witness significant growth during the forecast period.

While cloud adoption accelerates, on-premises deployment models remain critical for the global core banking software market, particularly for large financial institutions prioritizing direct control over their IT infrastructure.

This approach is central to effective data sovereignty management and addresses stringent financial data security standards. Organizations leverage these systems for regulatory technology integration and to ensure robust financial services cybersecurity.

However, the path often involves a core system replacement strategy that incorporates hybrid cloud solutions for banking, allowing for phased legacy system modernization.

This hybrid deployment for banks balances the security of on-premises control with the flexibility of cloud services, supporting scalable banking infrastructure while ensuring automated financial compliance.

This model offers a 15% improvement in security posture for institutions handling highly sensitive data.

The On-premises segment was valued at USD 15.80 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Core Banking Software Market Demand is Rising in North America Get Free Sample

The geographic landscape is defined by varied adoption rates, with North America leading in cloud adoption in banking due to the push for real-time transaction processing.

Financial institutions in the region are aggressively implementing SaaS for financial institutions to upgrade retail banking core solutions, achieving up to a 25% improvement in processing speeds.

In Europe, the focus is on open banking compliance, driving demand for advanced mobile banking backend systems. APAC is emerging as a high-growth region, with digital-native banks deploying cloud-native core banking to support commercial lending automation and wealth management integration.

These platforms enhance wealth and treasury platform capabilities, delivering significant real-time payment processing benefits across diverse markets and improving retail banking system features for millions of new digital users.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic discussions in the financial sector increasingly focus on core banking software market trends, particularly the impact of AI on core banking. Evaluating core banking software vendors is now a critical exercise, as institutions weigh the benefits of cloud-native core systems against the high cost of legacy system migration.

- The decision is especially crucial for new entrants, with core banking software for digital banks designed for agility. An effective API strategy for open banking is non-negotiable for competitiveness, enabling real-time payment systems integration and enhanced product offerings. Detailed analysis of retail banking core system features and commercial banking loan origination software is vital for meeting specific business needs.

- The technical hurdles are significant, with a strong focus on data migration tools for banking and ensuring security in cloud core banking. Firms exploring the composable banking architecture benefits are finding they can launch new products twice as fast as those on monolithic systems. Key automated functions include AI for mortgage underwriting automation and treasury management system automation.

- Success hinges on a deep understanding of regulatory compliance in banking software, the right BaaS platform technology stack, and delivering on the promise of personalizing customer banking experiences. The debate over on-premises vs cloud core banking continues, but the goal remains the same: efficient wealth management platform integration and a future-proof technology foundation.

What are the key market drivers leading to the rise in the adoption of Core Banking Software Industry?

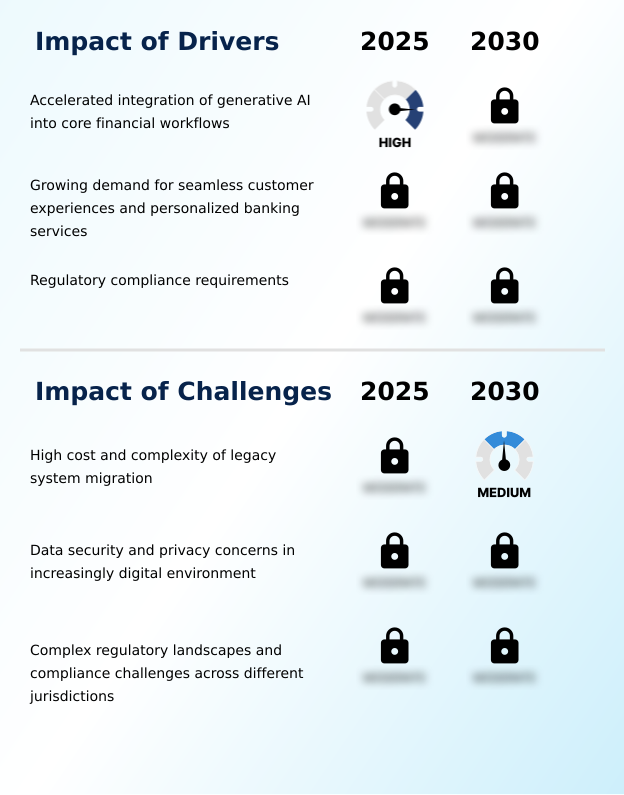

- The accelerated integration of generative AI into core financial workflows is a primary driver propelling the expansion of the core banking software market.

- The integration of generative AI in financial workflows is a significant market driver, revolutionizing processes like AI-powered credit underwriting and digital mortgage processing. This push toward modernizing banking technology enables advanced AI-driven risk management and highly efficient automated loan origination.

- Institutions leveraging AI report up to a 30% increase in accuracy for their credit scoring algorithms. These systems are central to customer experience personalization, using data analytics for personalization to create tailored financial products.

- Furthermore, the adoption of intelligent digital onboarding solutions and modernized payment processing systems showcases the tangible real-time payment processing benefits.

- This technological shift enables financial institutions to reduce manual intervention in key workflows by over 50%, enhancing both efficiency and customer satisfaction.

What are the market trends shaping the Core Banking Software Industry?

- The proliferation of composable banking architectures is an important trend. This shift allows financial institutions to innovate with greater agility by integrating modular, best-of-breed components.

- A definitive trend shaping the market is the shift toward a composable banking framework, which relies on an API-first architecture and modular banking software. This approach facilitates the building of a composable enterprise, allowing banks to integrate best-of-breed services via open banking APIs.

- Financial institutions that adopt microservices-based platforms achieve an average 40% faster time-to-market for new products compared to monolithic systems. This digital transformation in banking is crucial for effective fintech ecosystem integration and back-office operations automation. By enabling seamless API integration for financial services, banks can participate in the broader open finance ecosystem, significantly enhancing digital customer journeys.

- This strategy also leads to a 25% reduction in development costs through back-office process optimization.

What challenges does the Core Banking Software Industry face during its growth?

- The significant cost and inherent complexity of migrating from legacy systems represent a primary challenge constraining growth in the core banking software market.

- The high cost of legacy system migration remains a formidable barrier, with complex core banking transformation projects often exceeding budgets by up to 20%. These challenges of legacy system migration are compounded by the technical complexities of core banking data migration and ensuring uninterrupted multi-currency support.

- A complete core banking system replacement requires careful core banking vendor evaluation and adherence to core banking implementation best practices to avoid disrupting the existing financial institution IT infrastructure. Integrating new compliance reporting modules and digital ledger technology into legacy frameworks adds further expense.

- As a result, many organizations delay the move to next-generation banking platforms, with failed migration attempts leading to operational downtime in 1 out of 10 large-scale projects.

Exclusive Technavio Analysis on Customer Landscape

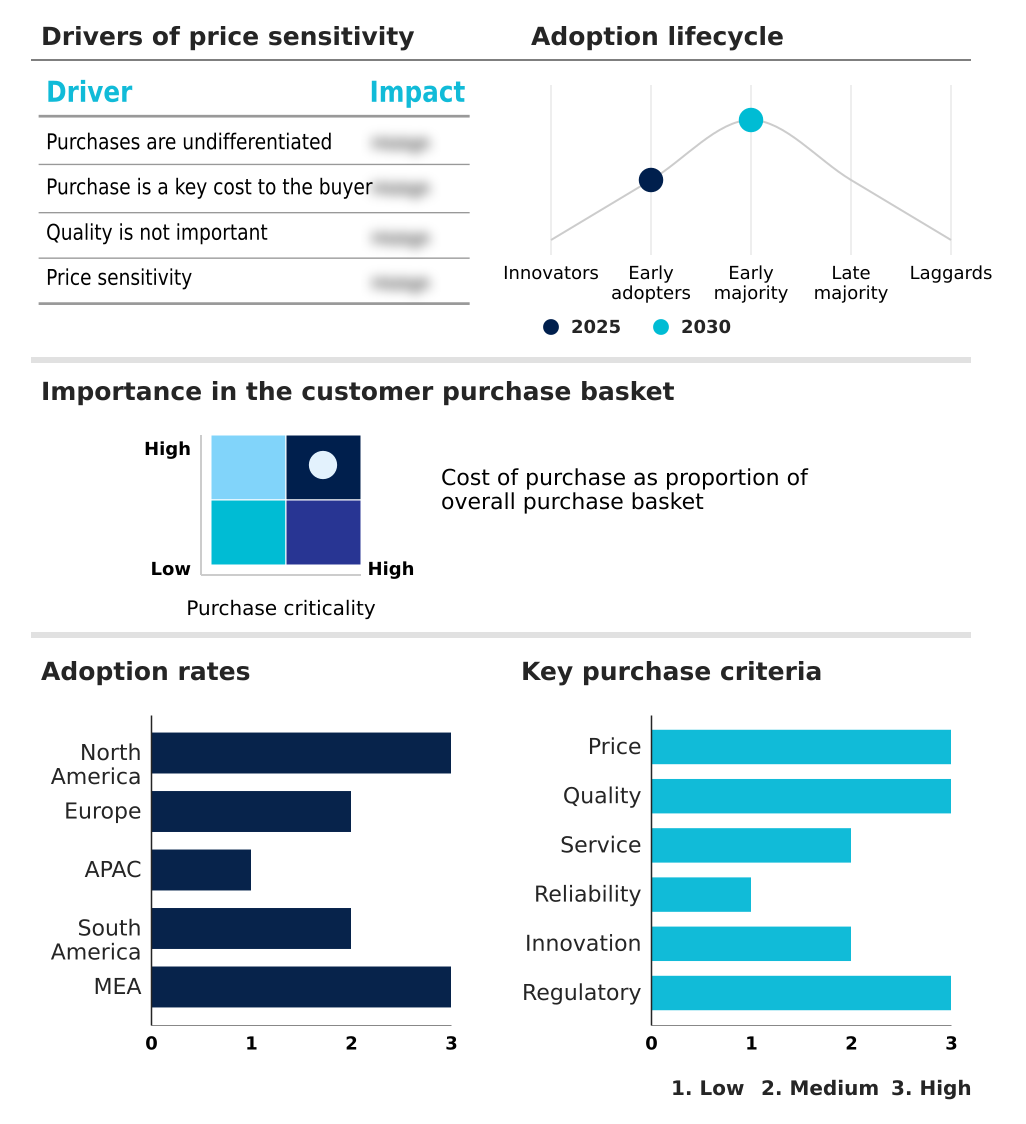

The core banking software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the core banking software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Core Banking Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, core banking software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Avaloq Group AG - Offers cloud-native, API-first core banking platforms designed to modernize financial institutions by enabling real-time processing and enhanced digital experiences for customers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Avaloq Group AG

- Azentio Software Pvt. Ltd.

- Backbase B.V.

- Capital Banking Solutions

- Fidelity National Information

- Finastra

- Fiserv Inc.

- Galileo Financial Technologies

- Intellect Design Arena Ltd.

- Intrasoft Technologies

- Jack Henry and Associates Inc.

- Mambu BV

- nCino Inc.

- Nucleus Software Exports Ltd.

- Oracle Corp.

- Profile Systems and Software SA

- Sopra Banking Software

- Tata Consultancy Services

- Temenos AG

- Thought Machine Group Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Core banking software market

- In August 2025, Wells Fargo initiated a strategic collaboration with Google Cloud for a multi-year migration of its core retail deposit systems to a distributed cloud environment, aiming to enhance the deployment of microservices.

- In June 2025, Banco Santander encountered technical challenges in its European core banking consolidation project, experiencing latency issues during the integration of localized legacy systems into a unified global platform.

- In May 2025, HSBC deployed an AI-native core module in its European retail operations, using machine learning to automate mortgage underwriting and reduce application processing times from days to minutes.

- In February 2025, Commonwealth Bank of Australia formed a partnership with a cloud-native provider to implement a composable core framework, targeting a 60% reduction in time-to-market for new business credit products.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Core Banking Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 285 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 17.8% |

| Market growth 2026-2030 | USD 31112.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 15.6% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is centered on a move from on-premises deployment models to cloud deployment models, including hybrid cloud solutions for banking. This digital transformation in banking necessitates legacy system modernization or a complete core banking system replacement. Modern systems are defined by cloud-native core banking and an API-first architecture, often built on microservices-based platforms.

- Key functionalities include real-time transaction processing, multi-currency support, and robust customer account management. The adoption of a composable banking framework allows for flexible wealth management integration alongside retail banking core solutions and commercial banking core services. Automation is critical, spanning back-office operations automation, automated loan origination with advanced credit scoring algorithms, and streamlined digital onboarding solutions.

- These platforms facilitate fintech ecosystem integration through open banking APIs and are crucial for banking-as-a-service (BaaS) platforms. Security and compliance are addressed through financial services cybersecurity, regulatory technology integration, and modules for compliance reporting and data sovereignty management.

- The infrastructure must be a scalable banking infrastructure, supporting mobile banking backend systems, advanced payment processing systems, treasury management systems, and even digital ledger technology. This comprehensive approach, which includes sophisticated core banking data migration strategies, has enabled some institutions to improve operational efficiency by over 25%.

What are the Key Data Covered in this Core Banking Software Market Research and Growth Report?

-

What is the expected growth of the Core Banking Software Market between 2026 and 2030?

-

USD 31.11 billion, at a CAGR of 17.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (On-premises, and Cloud), End-user (Banks, and Financial institutions), Solution (Retail banking core, Commercial banking core, and Wealth and treasury management) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Accelerated integration of generative AI into core financial workflows, High cost and complexity of legacy system migration

-

-

Who are the major players in the Core Banking Software Market?

-

Avaloq Group AG, Azentio Software Pvt. Ltd., Backbase B.V., Capital Banking Solutions, Fidelity National Information, Finastra, Fiserv Inc., Galileo Financial Technologies, Intellect Design Arena Ltd., Intrasoft Technologies, Jack Henry and Associates Inc., Mambu BV, nCino Inc., Nucleus Software Exports Ltd., Oracle Corp., Profile Systems and Software SA, Sopra Banking Software, Tata Consultancy Services, Temenos AG and Thought Machine Group Ltd.

-

Market Research Insights

- Market dynamics are heavily influenced by the strategic push toward modernizing banking technology and adopting next-generation banking platforms. A key driver is enhancing digital customer journeys, where institutions leveraging data analytics for personalization have seen customer retention rates improve by up to 15%.

- The move toward building a composable enterprise allows for greater agility, with the use of modular banking software reducing new product development cycles by 30%. Furthermore, cloud adoption in banking continues to accelerate, driven by the operational efficiencies of SaaS for financial institutions.

- Core banking transformation projects now focus on API integration for financial services, enabling participation in the wider open finance ecosystem and providing significant real-time payment processing benefits.

We can help! Our analysts can customize this core banking software market research report to meet your requirements.

RIA -

RIA -