Corneal Pachymetry Market Size 2024-2028

The corneal pachymetry market size is forecast to increase by USD 549.2 million, at a CAGR of 3.67% between 2023 and 2028.

- The market is driven by the increasing prevalence of refractive errors and glaucoma, two major eye conditions that require precise measurement of corneal thickness for effective diagnosis and treatment. This market trend is further fueled by companies' strategic focus on expanding their reach in emerging markets, where the demand for advanced ophthalmic diagnostic tools is on the rise. However, the market faces significant challenges, including high costs associated with corneal pachymetry devices and limited reimbursements for these procedures. These financial hurdles may hinder market growth and necessitate innovative pricing strategies or partnerships with healthcare providers and insurers to ensure affordability and accessibility for patients.

- Companies seeking to capitalize on market opportunities must navigate these challenges effectively, while also staying abreast of technological advancements and regulatory requirements to maintain a competitive edge.

What will be the Size of the Corneal Pachymetry Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in ocular biometry, data analytics, and corneal biomechanics. Clinical trials exploring myopia control and disease management employ corneal biomarkers to assess corneal health and predict surgical outcomes. Anterior segment analysis plays a crucial role in precision lens selection and surgical planning, while eye care professionals rely on medical device regulation for ensuring safety and efficacy. Corneal modeling and digital health solutions facilitate data analysis and predictive modeling, enabling healthcare IT to optimize treatment and improve patient engagement. Scheimpflug imaging and corneal topography offer insights into corneal deformation and ectasia, informing treatment decisions and enhancing surgical outcomes.

Corneal elasticity, corneal hydrodynamics, and corneal collagen are essential corneal properties under investigation, with emerging technologies such as artificial intelligence (AI) and machine learning (ML) driving new discoveries. Computer vision and image processing contribute to automated refractometry, while patient education and data security are essential components of eye health management. Corneal cross-linking and corneal transplant procedures benefit from these advancements, ensuring optimal treatment and improved patient outcomes. The ongoing unfolding of market activities and evolving patterns underscore the dynamic nature of the market, with continuous innovation and progress shaping its future.

How is this Corneal Pachymetry Industry segmented?

The corneal pachymetry industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Specialty clinics

- Hospitals

- Others

- Product

- Non-handheld

- Handheld

- Geography

- North America

- US

- Europe

- France

- Germany

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

.

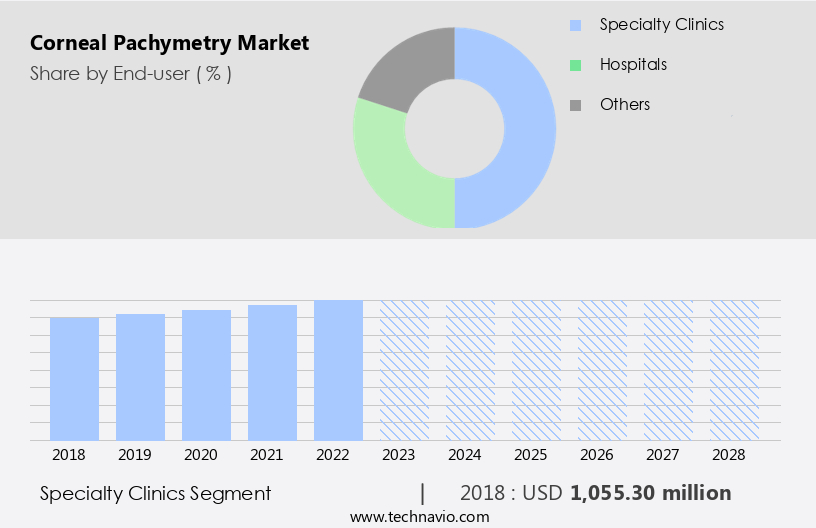

By End-user Insights

The specialty clinics segment is estimated to witness significant growth during the forecast period.

In The market, specialty clinics emerge as a significant growth driver. These clinics prioritize specialized eye care services and diagnostics for various corneal disorders, making them crucial end-consumers. The increasing prevalence of eye conditions like glaucoma and corneal diseases, coupled with heightened awareness for early detection and treatment, fuels the demand for advanced corneal pachymetry equipment in these clinics. Technological advancements, including portable and user-friendly devices, further accelerate adoption. As a result, the specialized clinics sector is anticipated to continue its substantial impact on the market's expansion throughout the forecast period. Corneal pachymetry plays a pivotal role in ocular biometry, enabling precise measurement of corneal thickness.

This data is integral to disease management, surgical planning, postoperative monitoring, and treatment optimization. Corneal biomechanics, a crucial aspect of eye health, is also assessed through corneal pachymetry. Additionally, myopia control and corneal biomarkers are gaining attention in the market, driving the need for accurate and reliable corneal thickness measurements. Data analytics, healthcare IT, and digital health are transforming the market by facilitating data-driven decision-making. Anterior segment analysis, corneal elasticity, and corneal stiffness are essential corneal parameters that can be evaluated using corneal pachymetry data. Predictive modeling and machine learning algorithms are being employed to enhance treatment outcomes and improve patient care.

Emerging technologies, such as artificial intelligence and computer vision, are also poised to revolutionize the market. Eye care professionals rely on corneal pachymetry for precise lens selection, ensuring optimal refractive surgery results. Corneal cross-linking, a popular treatment for corneal diseases, also necessitates accurate corneal thickness measurements. Medical device regulation ensures the safety and efficacy of corneal pachymetry devices, while patient engagement and education are vital for successful treatment outcomes. Corneal modeling, corneal hydrodynamics, and surgical outcomes are critical areas of research in the market. Scheimpflug imaging, corneal ectasia, and corneal deformation are some of the corneal disorders that corneal pachymetry helps diagnose and monitor.

Corneal transplant and corneal simulation are other applications of corneal pachymetry, highlighting its versatility and importance in the field of eye care.

The Specialty clinics segment was valued at USD 1055.30 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 50% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the North American market, the US plays a significant role in the growing ocular biometry industry. This is primarily due to increased healthcare expenditure on managing ocular diseases, such as glaucoma and refractive errors. The adoption of advanced non-invasive diagnostic tools, like data analytics, corneal biomechanics, and anterior segment analysis, is on the rise. The aging population, availability of skilled medical professionals, and well-equipped healthcare infrastructure further fuel market growth. According to the Centers for Disease Control and Prevention (CDC), approximately 2.89 million Americans aged 40 and above were diagnosed with glaucoma in 2014. This number is projected to increase to 4 million by 2020.

Incorporating digital health, healthcare it, and machine learning, industry trends include myopia control, corneal biomarkers, disease management, and precision lens selection. Corneal thickness measurement, surgical planning, postoperative monitoring, and corneal topography are essential components of preoperative assessment. Emerging technologies, such as corneal modeling, corneal simulation, and predictive modeling, are revolutionizing the field of ocular care. Furthermore, patient engagement, refractive surgery, contact lens fitting, and corneal cross-linking are gaining popularity. Data security and image processing are crucial aspects of this market, ensuring patient privacy and accurate analysis. The integration of artificial intelligence and healthcare informatics in ocular biometry is expected to optimize treatment and surgical outcomes.

Corneal transplant, corneal deformation, and corneal hydrodynamics are areas of ongoing research. Overall, the US market for ocular biometry is witnessing significant growth, driven by the need for early disease detection and advanced diagnostic tools.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Corneal Pachymetry Industry?

- The rising prevalence of refractive errors and glaucoma serves as the primary market driver, significantly increasing market demand for diagnostic tools and treatments in the ophthalmology sector.

- The market is witnessing significant growth due to the increasing prevalence of refractive errors and eye diseases. Myopia, a common vision impairment condition, is a major driver in this market. Myopia, or nearsightedness, affects an individual's ability to see distant objects clearly. This condition can lead to more serious vision-threatening conditions, such as retinal breaks, detachment, and glaucoma. Although the cause of myopia is not clear, it is often genetic or results from prolonged exposure to digital screens. Patient engagement is a crucial factor in the growth of the market. Advanced technologies, such as automated refractokeratometry, image processing, and computer vision, are improving patient education and eye health management.

- Furthermore, corneal cross-linking, a surgical procedure used to treat keratoconus and other corneal diseases, is increasing the demand for corneal pachymetry. Data security is a significant concern in the market. The sensitive nature of eye health data requires robust security measures to protect patient privacy. Companies are investing in advanced security systems to ensure the confidentiality, integrity, and availability of patient data. In conclusion, the market is experiencing growth due to the increasing prevalence of refractive errors and eye diseases, advancements in technology, and the importance of patient engagement and data security. With continued research and development, this market is poised for continued growth and innovation.

- Recent research suggests that the market will continue to expand, offering opportunities for companies to provide innovative solutions to meet the evolving needs of patients.

What are the market trends shaping the Corneal Pachymetry Industry?

- The focus of companies on enhancing their presence in emerging markets is an emerging market trend. This strategic move is essential for business growth in the global marketplace.

- The global market for corneal pachymetry is experiencing significant growth due to several factors. The expanding middle class in emerging economies, such as China, India, and Brazil, presents a substantial new customer base with increased access to corneal pachymeter devices and diagnostic services, as well as the financial resources to afford them. Moreover, rising healthcare expenditures, growing disposable income, and improving healthcare infrastructure in these regions contribute to the increasing demand for corneal pachymetry. Key companies entering these markets will not only discover new growth opportunities but also reap the benefits of the first-mover advantage, high economic growth rates, and increasing government initiatives in these countries.

- Advancements in ocular biometry, data analytics, corneal biomechanics, and clinical trials for myopia control are driving innovation in the market. Corneal biomarkers, disease management, anterior segment analysis, and precision lens selection are also gaining importance in the field of eye care. Medical device regulation ensures the safety and efficacy of these devices, ensuring the delivery of accurate and reliable results. Corneal modeling and modeling techniques are also advancing, providing more accurate measurements and improving the overall accuracy and reliability of corneal pachymetry.

What challenges does the Corneal Pachymetry Industry face during its growth?

- The high costs associated with corneal pachymetry, coupled with limited reimbursements, poses a significant challenge to the industry's growth trajectory.

- Advanced corneal pachymetry, a critical tool for measuring corneal thickness, plays a pivotal role in surgical planning, postoperative monitoring, and treatment optimization. Corneal pachymetry aids in assessing corneal elasticity and corneal stiffness, which are essential factors in predictive modeling for ophthalmic procedures. Digital health technologies and healthcare IT solutions have facilitated data analysis and interpretation, enabling more accurate and efficient diagnoses. However, the adoption of advanced corneal pachymetry is hindered by the high costs of corneal pachymeters and diagnostic procedures. The average global cost of a corneal pachymeter is USD2,750, and the prices for specific models, such as Accutome's AccuPach VI Pachymeter and PachPen Handheld Pachymeter, are USD2,768 and USD2,358, respectively.

- The reimbursement scenario for corneal pachymetry varies significantly across countries, which further limits its accessibility. In conclusion, the high cost of corneal pachymetry and inconsistent reimbursement policies present significant challenges to its widespread adoption. Despite these hurdles, the potential benefits of corneal pachymetry in improving patient outcomes and enhancing the overall quality of ophthalmic care warrant continued exploration and innovation in this field. Emerging technologies, such as handheld devices and non-invasive imaging techniques, may offer more affordable and accessible alternatives for measuring corneal thickness and assessing corneal health.

Exclusive Customer Landscape

The corneal pachymetry market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the corneal pachymetry market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, corneal pachymetry market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AMETEK Inc. - The company specializes in advanced ophthalmic diagnostic tools, including the innovative ipac pachymeter.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AMETEK Inc.

- Canon Inc.

- Carl Zeiss AG

- CSO S.r.l

- DGH Technology Inc.

- Escalon Medical Corp.

- EssilorLuxottica

- Halma Plc

- Konan Medical Inc.

- MEDA Co. Ltd.

- MicroMedical Devices Inc.

- NIDEK Co. Ltd.

- OCULUS Optikgerate GmbH

- Optikon 2000 SpA

- SCHWIND eye-tech-solutions GmbH

- Sonogage Inc.

- Tomey Corp.

- Ziemer Ophthalmic Systems AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Corneal Pachymetry Market

- In February 2023, Carl Zeiss Meditec AG introduced the IOLMaster 700, an advanced corneal pachymetry device that combines anterior and posterior measurements in a single scan, enhancing diagnostic accuracy. (Carl Zeiss Meditec AG press release)

- In July 2022, Topcon Corporation and Google announced a strategic partnership to integrate Google's artificial intelligence (AI) and machine learning (ML) technologies into Topcon's ophthalmic devices, including its corneal pachymetry systems, aiming to improve diagnostic precision. (Topcon Corporation press release)

- In April 2021, Nidek Co. Ltd. Received U.S. Food and Drug Administration (FDA) approval for its OPD-Scan III RED scanning laser ophthalmoscope, which includes a corneal pachymetry function. This approval expanded Nidek's product offerings in the market. (Nidek Co. Ltd. Press release)

- In March 2020, Optovue Inc. Raised USD40 million in a funding round led by Frazier Healthcare Partners, enabling the company to expand its product portfolio and accelerate research and development efforts in corneal pachymetry and other ophthalmic technologies. (BusinessWire)

Research Analyst Overview

- The market encompasses a range of technologies and applications, from software for measuring corneal thickness to devices and algorithms for analyzing corneal biomechanics. These tools play a crucial role in detecting and managing various corneal conditions, including infections, astigmatism, scarring, and irregularities. Corneal pachymetry accuracy is essential for refractive error correction and monitoring ocular surface diseases, such as dry eye and corneal ulcers. Advancements in corneal pachymetry algorithms and wavefront analysis enable more precise corneal curvature measurement and shape analysis, facilitating effective diagnosis and treatment of corneal diseases, including edema, decompensation, and infiltration. Corneal biomechanics research continues to uncover new insights into the complex interplay between corneal health and biomechanics, informing the development of innovative devices and software for corneal health screening and disease monitoring.

- Presbyopia correction and biomechanics models are emerging applications for corneal pachymetry, offering potential solutions for an aging population seeking vision correction alternatives. The market trends toward greater accuracy, reliability, and integration with other diagnostic tools, ensuring that corneal pachymetry remains a vital tool for ophthalmic professionals and researchers.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Corneal Pachymetry Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

163 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.67% |

|

Market growth 2024-2028 |

USD 549.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.49 |

|

Key countries |

US, Germany, Japan, China, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Corneal Pachymetry Market Research and Growth Report?

- CAGR of the Corneal Pachymetry industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the corneal pachymetry market growth of industry companies

We can help! Our analysts can customize this corneal pachymetry market research report to meet your requirements.

RIA -

RIA -