Coronary Artery Bypass Grafting Market Size 2024-2028

The coronary artery bypass grafting market size is forecast to increase by USD 30.3 million, at a CAGR of 4.49% between 2023 and 2028.

- The Coronary Artery Bypass Grafting (CABG) market is experiencing significant growth due to the rising prevalence of coronary artery diseases (CVDs) worldwide. The increasing geriatric population, a demographic with a higher risk for CVDs, further fuels market expansion. However, the availability of alternative treatments, such as percutaneous coronary intervention (PCI) and drug-eluting stents, poses a challenge to the CABG market. These minimally invasive procedures offer shorter hospital stays and quicker recovery times, making them attractive alternatives for patients and healthcare providers.

- As a result, CABG market participants must focus on innovation, cost-effectiveness, and patient outcomes to maintain their competitive edge. Effective collaboration between industry players, regulatory bodies, and healthcare providers can help address these challenges and ensure the continued growth of the CABG market.

What will be the Size of the Coronary Artery Bypass Grafting Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The coronary artery bypass grafting (CABG) market continues to evolve, driven by advancements in surgical techniques, anesthesia management, and postoperative care. Off-pump CABG, which minimizes the use of cardiopulmonary bypass, has gained popularity due to its potential benefits in reducing complications and improving patient outcomes. Myocardial revascularization, a key application of CABG, enables the restoration of blood flow to the heart muscle, addressing coronary artery disease and enhancing long-term survival. Anticoagulation therapy plays a crucial role in preventing graft failure and thrombosis, while surgical instruments and aortocoronary bypass techniques facilitate precise and efficient procedures. Angiographic assessment is essential for evaluating graft patency and identifying potential complications such as graft stenosis or bypass conduit failure.

Surgical planning, perfusion techniques, and wound healing are critical components of the CABG process, with infection control and patient selection criteria playing a significant role in minimizing complications and optimizing outcomes. The ongoing research and development in this field continue to unfold, with minimally invasive CABG, radial artery grafts, and internal mammary artery usage emerging as potential game-changers. The evolving nature of CABG market dynamics encompasses various aspects, including ventricular function, reoperation rates, quality of life, and surgical mortality rates. As the market continues to progress, graft patency, bypass surgery complications, and graft failure remain key areas of focus for researchers and healthcare providers alike.

Hypothermic cardioplegia and saphenous vein graft disease are ongoing challenges that require continuous attention and innovation.

How is this Coronary Artery Bypass Grafting Industry segmented?

The coronary artery bypass grafting industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product Type

- On-pump

- Off-pump

- Minimally invasive surgery

- Geography

- North America

- US

- Canada

- Europe

- Russia

- APAC

- China

- India

- Rest of World (ROW)

- North America

By Product Type Insights

The on-pump segment is estimated to witness significant growth during the forecast period.

The global Coronary Artery Bypass Grafting (CABG) market is witnessing significant advancements, with a focus on enhancing patient outcomes and reducing complications. Anesthesia management plays a crucial role in ensuring a smooth surgical experience, particularly during off-pump CABG procedures, which minimize the risk of postoperative complications. Myocardial revascularization, a key component of CABG, is achieved through various techniques, including aortocoronary bypass and internal mammary artery grafting. Anticoagulation therapy is essential to prevent graft failure and thrombosis, while surgical instruments and perfusion techniques facilitate efficient grafting and wound healing. Angiographic assessment is critical for evaluating graft patency and identifying graft stenosis or bypass conduit failure.

Infection control measures are integral to minimizing surgical site infections and improving long-term survival rates. Patient selection criteria, surgical planning, and minimally invasive CABG techniques are driving innovation in the CABG market. Hypothermic cardioplegia, a technique used to protect the heart during surgery, and blood management strategies contribute to reducing surgical mortality rates and improving quality of life. However, complications such as vein graft disease, reoperation rates, and ventricular function issues remain challenges. Surgical techniques, such as radial artery grafting and saphenous vein grafting, continue to evolve, while graft patency and bypass surgery complications remain areas of ongoing research.

Infection control, patient selection, and surgical planning are essential factors influencing the market's dynamics. The CABG market is expected to grow as advancements in technology and surgical techniques improve patient outcomes and reduce complications.

The On-pump segment was valued at USD 46.80 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

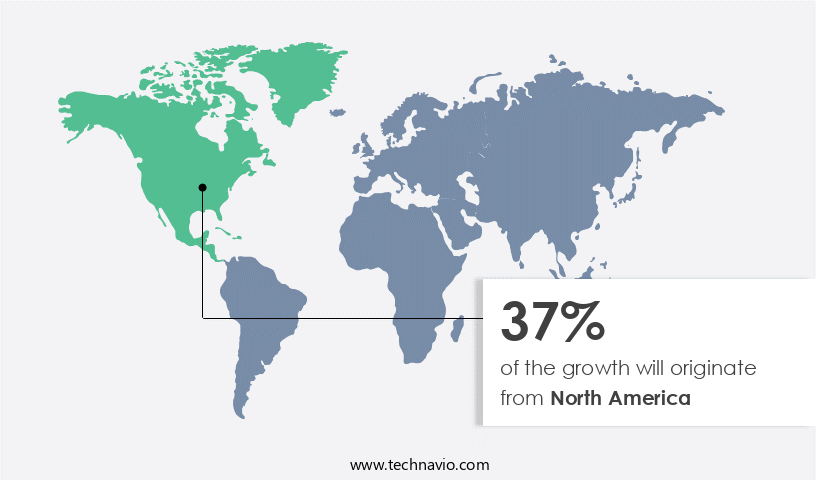

North America is estimated to contribute 37% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The Coronary Artery Bypass Grafting (CABG) market in North America is currently leading the global landscape due to several factors. The presence of advanced healthcare infrastructure, highly skilled medical professionals, and extensive healthcare insurance coverage are key contributors to the region's dominance. Furthermore, increasing R&D expenditure by companies, high adoption of technologically advanced products, and the availability of less invasive treatment options, such as off-pump CABG and minimally invasive CABG, are propelling market growth. In the US, the Centers for Medicare & Medicaid Services (CMS) provide extensive healthcare insurance coverage, making it the major revenue contributor to the North American CABG market.

Myocardial revascularization procedures, including CABG, are crucial for managing coronary artery disease (CAD) and improving long-term survival rates. Surgical planning, perfusion techniques, and angiographic assessment play a vital role in ensuring successful CABG outcomes. Anticoagulation therapy and infection control are essential aspects of postoperative recovery and patient care. The market also focuses on addressing complications, such as graft failure, graft stenosis, and surgical mortality rates, through advancements in bypass conduits, surgical techniques, and blood management. The goal is to enhance patient quality of life and reduce reoperation rates while maintaining optimal ventricular function and minimizing complications. Patient selection criteria and surgical mortality rates are critical factors influencing market dynamics.

Hypothermic cardioplegia and saphenous vein grafts are commonly used techniques, while internal mammary artery grafts offer better long-term patency. The market is also addressing challenges related to vein graft disease and arterial graft complications through ongoing research and development efforts.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The Coronary Artery Bypass Grafting (CABG) market continues to evolve with advancements in surgical techniques and technologies aimed at improving patient outcomes and reducing postoperative complications. One such innovation is the use of left anterior descending artery bypass, which enhances myocardial perfusion and reduces ischemic damage. Improved myocardial perfusion techniques, such as selective cannulation and antegrade cerebral perfusion, further minimize complications. Minimally invasive CABG techniques, including off-pump and robotic-assisted procedures, offer benefits like less trauma, faster recovery, and lower risk of stroke and atrial fibrillation. The impact of radial artery graft patency on long-term outcomes is significant, as it increases graft durability and reduces the need for repeat revascularization. Effective management of cardiopulmonary bypass, including optimal temperature control and hemodynamic stability, plays a crucial role in enhancing surgical outcomes for CABG patients. Patient selection criteria, such as age, comorbidities, and coronary anatomy, are essential in determining the success of the procedure. Graft stenosis detection methods, including intravascular ultrasound and angiography, help identify and address early signs of graft failure. Risk factors for graft failure, such as diabetes, smoking, and hypertension, should be carefully managed to ensure optimal graft function. Postoperative cognitive dysfunction is a common concern for CABG patients, and enhanced recovery protocols, including early mobilization and multimodal analgesia, can help minimize its impact. Assessment of ventricular function, using techniques like ejection fraction and cardiac output monitoring, allows for timely intervention in cases of postoperative heart failure. Management of postoperative bleeding, through techniques like hemostatic agents and blood salvage, and prevention of graft thrombosis, using anticoagulation and antiplatelet therapy, are essential in reducing morbidity and mortality. Minimizing surgical site infection through strict sterile technique and prophylactic antibiotics is another critical aspect of CABG care. The surgical experience of the healthcare team significantly influences CABG outcomes. Adherence to evidence-based practices and continuous professional development are essential in maintaining high-quality care and improving patient outcomes in the market.

What are the key market drivers leading to the rise in the adoption of Coronary Artery Bypass Grafting Industry?

- The rising prevalence of cardiovascular diseases (CVDs) serves as the primary market driver, significantly contributing to its growth.

- Coronary Artery Bypass Grafting (CABG) is a surgical procedure used to improve blood flow to the heart by bypassing blocked or narrowed coronary arteries. Complications from CABG surgery include graft stenosis, graft patency issues, and hypothermic cardioplegia-related complications. Graft stenosis, or the narrowing of the grafted artery, can lead to recurring angina or even the need for repeat revascularization. Graft patency, or the maintenance of blood flow through the graft, can be affected by various factors such as surgical techniques and blood management. Hypothermic cardioplegia, a method used to protect the heart during surgery by cooling it, can lead to complications such as arrhythmias and organ dysfunction.

- Minimally invasive CABG techniques have emerged as an alternative to traditional open-heart surgery, offering potential benefits such as reduced trauma, shorter hospital stays, and quicker recovery times. Surgical techniques and blood management strategies continue to evolve to improve outcomes and reduce complications in CABG surgery.

What are the market trends shaping the Coronary Artery Bypass Grafting Industry?

- The geriatric population is experiencing significant growth, making it an emerging market trend. This demographic shift presents numerous opportunities for professionals and businesses catering to the unique needs of older adults.

- The global population aging trend is a significant driver in the growth of the myocardial revascularization market, particularly for procedures such as Coronary Artery Bypass Grafting (CABG). The geriatric population, defined as individuals aged 65 years and above, is expanding rapidly worldwide. According to the United Nations, the global geriatric population was 702.9 million in 2019 and is projected to reach 727 million in 2020. In developing countries like India, the geriatric population is expected to increase by 41% over the next decade, reaching 194 million in 2031. This demographic shift is attributed to improved healthcare systems, longer life expectancy, and declining fertility rates.

- The aging population is at a higher risk of developing cardiac blockages due to poor lifestyle choices and age-related health issues. As a result, the demand for CABG procedures, including off-pump and aortocoronary bypass techniques, is increasing. These procedures aim to improve blood flow to the heart by grafting a healthy blood vessel from another part of the body to bypass the blocked coronary artery. Anesthesia management, surgical instruments, anticoagulation therapy, and postoperative recovery are crucial aspects of CABG procedures. Angiographic assessment is used to evaluate the success of the procedure and identify any potential complications.

- Cardiopulmonary bypass, a critical component of CABG, is used to maintain blood circulation during the surgery. Ensuring harmonious coordination between these elements is essential for a successful and immersive patient experience.

What challenges does the Coronary Artery Bypass Grafting Industry face during its growth?

- The growth of the industry is significantly influenced by the limited availability of viable alternatives.

- The Coronary Artery Bypass Grafting (CABG) market faces challenges due to the availability of alternative treatments for coronary artery disease (CAD). These alternatives include heart repair and replacement devices, commissurotomy, percutaneous balloon mitral valvuloplasty, and vitamin D medications. Heart repair and replacement devices offer an alternative by repairing or replacing defective heart valves, which are susceptible to valvular heart diseases such as valve stenosis and regurgitation. Vitamin D3 medications, like cholecalciferol, help restore damaged cardiovascular epithelial cells, while blood thinners such as aspirin prevent blood clots, potentially reducing the need for CABG surgery.

- Surgical planning, perfusion techniques, and wound healing are crucial factors influencing the success of CABG procedures. Long-term survival rates and infection control are essential considerations for patients undergoing CABG, ensuring the best possible outcomes.

Exclusive Customer Landscape

The coronary artery bypass grafting market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the coronary artery bypass grafting market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, coronary artery bypass grafting market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - The Graftmaster RX brand, under the company's portfolio, specializes in providing coronary artery bypass grafting solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Aesculap Inc.

- AtriCure Inc.

- Aruga Technologies

- Bentley InnoMed GmbH

- BIOTRONIK SE and Co. KG

- Boston Scientific Corp.

- Cook Group Inc.

- Cryolife Inc.

- Gebruder Martin GmbH and Co. KG

- Genesee BioMedical Inc.

- Getinge AB

- Johnson and Johnson Services Inc.

- KARL STORZ SE and Co. KG

- Medtronic Plc

- Saphena Medical Inc.

- Scanlan International

- Stryker Corp.

- Teleflex Inc.

- Terumo Corp.

- VasoPrep Surgical

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Coronary Artery Bypass Grafting Market

- In January 2024, Medtronic, a leading medical technology company, announced the successful implantation of the first patient with the IN.PACT Admiral Drug-Coated Balloon (DCB) in a Coronary Artery Bypass Grafting (CABG) surgery. This marks a significant technological advancement in the field, as DCBs are typically used in percutaneous coronary interventions (PCI), not CABG procedures (Medtronic Press Release, 2024).

- In March 2024, Abbott Laboratories and St. Jude Medical, two major players in the cardiovascular devices market, completed their merger, creating a new entity, Abbott's Cardiovascular and Neuromodulation business. This merger aims to strengthen their position in the CABG market by combining their extensive portfolios and expertise (Abbott Press Release, 2024).

- In April 2025, the US Food and Drug Administration (FDA) approved Edwards Lifesciences' Sapien 3 Transcatheter Heart Valve for use in patients undergoing CABG surgery. This approval expands the indications for the Sapien 3 valve, making it the first transcatheter aortic valve replacement (TAVR) system approved for use in conjunction with CABG procedures (Edwards Lifesciences Press Release, 2025).

- In May 2025, Siemens Healthineers and the University of California, San Francisco (UCSF) Health partnered to establish the UCSF Siemens Center for Advanced Heart Failure and Transcatheter Valve Therapies. This collaboration aims to advance research and clinical applications of transcatheter technologies, including those used in CABG procedures, to improve patient outcomes (Siemens Healthineers Press Release, 2025).

Research Analyst Overview

- The Coronary Artery Bypass Grafting (CABG) market is characterized by a focus on enhancing perioperative management and minimizing complications. Neurological deficits and cardiac tamponade remain significant concerns, necessitating meticulous surgical precision and intraoperative monitoring. Transfusion requirements and blood loss are ongoing challenges, with a growing emphasis on reducing both through advanced surgical techniques and expertise. Quality indicators, such as graft occlusion and restenosis prevention, are crucial for long-term follow-up and optimal patient outcomes. Complication management, including wound infection rate and anastomotic technique, is a key area of research. Surgical experience, bypass duration, and renal dysfunction also impact patient experiences and graft survival rate.

- Thrombosis risk and graft occlusion are addressed through rigorous surgical expertise and postoperative care. Arterial harvesting techniques and risk stratification are essential for minimizing complications and ensuring successful CABG procedures. Intraoperative monitoring and postoperative care are vital components of the overall surgical experience, with ongoing efforts to improve outcomes and reduce morbidity.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Coronary Artery Bypass Grafting Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

141 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.49% |

|

Market growth 2024-2028 |

USD 30.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.21 |

|

Key countries |

US, China, Russia, Canada, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Coronary Artery Bypass Grafting Market Research and Growth Report?

- CAGR of the Coronary Artery Bypass Grafting industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the coronary artery bypass grafting market growth of industry companies

We can help! Our analysts can customize this coronary artery bypass grafting market research report to meet your requirements.

RIA -

RIA -